Key Insights

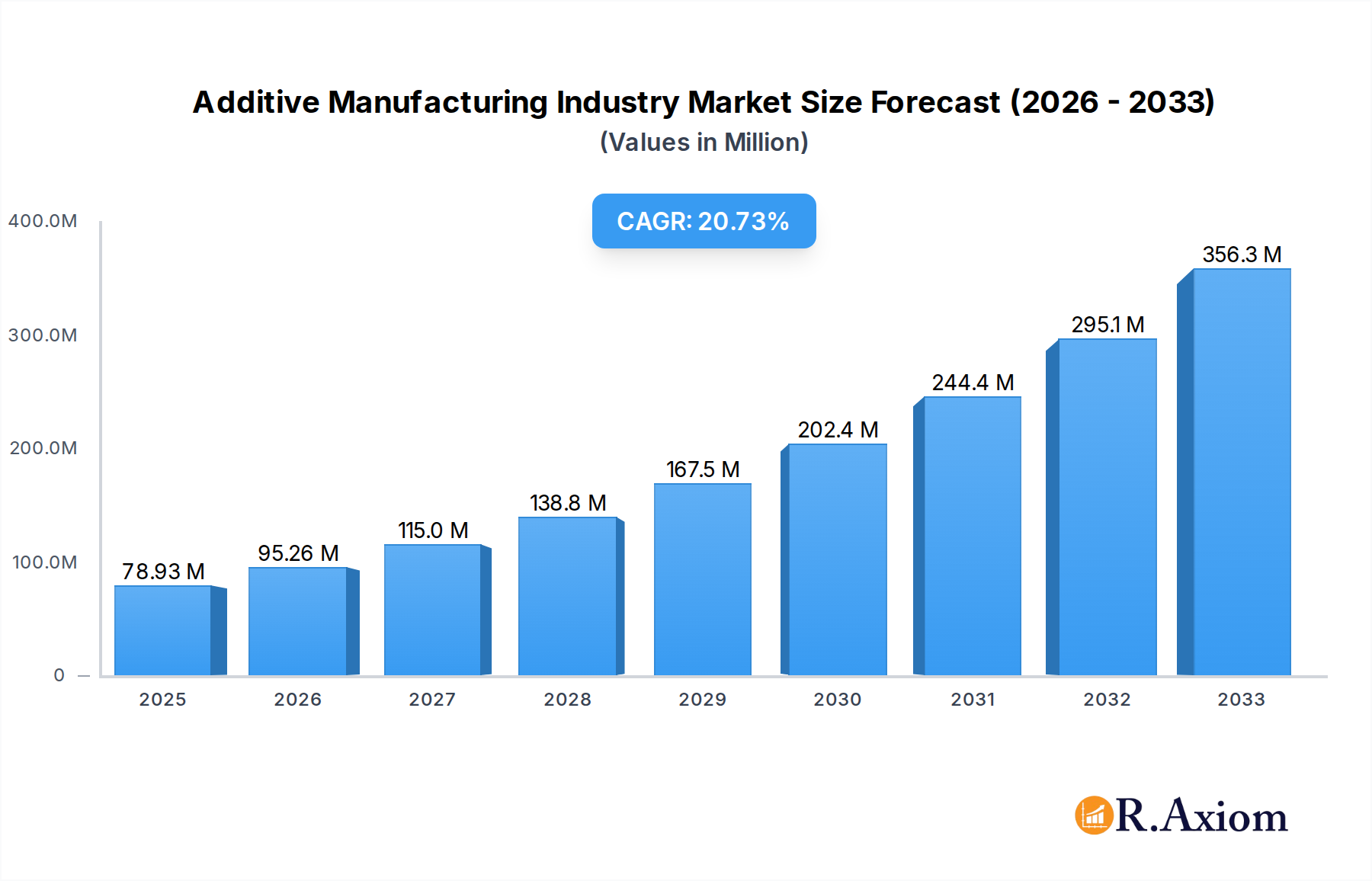

The Additive Manufacturing (AM), also known as 3D printing, industry is experiencing a robust expansion, projected to reach a market size of 78.93 Million in 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 20.70% through 2033. This significant growth is underpinned by a confluence of powerful drivers, including the increasing demand for customized and on-demand production, particularly in sectors like aerospace and defense, automotive, and healthcare. The ability of additive manufacturing to create complex geometries, reduce material waste, and accelerate product development cycles makes it an indispensable technology for innovation. Furthermore, advancements in materials science, with the development of high-performance plastics, metals, and ceramics suitable for AM, are expanding its application scope. The integration of sophisticated technologies such as Stereo Lithography, Fused Deposition Modelling, Laser Sintering, and Binder Jetting Printing is continuously enhancing the precision, speed, and cost-effectiveness of AM processes, further fueling market penetration.

Additive Manufacturing Industry Market Size (In Million)

The current market landscape is characterized by significant investment and innovation from key players like General Electric Company (GE Additive), 3D Systems Corporation, and Stratasys Ltd. These companies are at the forefront of developing new AM solutions and expanding their reach across various industries. Emerging trends include the growing adoption of AM for mass customization, enabling personalized medical implants and bespoke automotive components. The industrialization of AM is also a key trend, with companies exploring its use for end-of-line production and spare parts manufacturing, thereby reducing lead times and inventory costs. While the market presents immense opportunities, certain restraints, such as the initial high cost of advanced AM equipment and the need for specialized expertise, could temper growth in specific segments. However, the ongoing technological advancements and increasing accessibility are steadily overcoming these challenges, positioning the Additive Manufacturing industry for sustained and dynamic growth in the coming years.

Additive Manufacturing Industry Company Market Share

Additive Manufacturing Industry Market Concentration & Innovation

The Additive Manufacturing (AM) industry, also known as 3D printing, is characterized by a dynamic market concentration driven by continuous innovation. Key players like Mcor Technologies Ltd, General Electric Company (GE Additive), Optomec Inc, 3D Systems Corporation, Exone Company, SLM Solutions Group AG, EOS GmbH, Materialise NV, Stratasys Ltd, and EnvisionTEC GmbH are at the forefront of technological advancements and market expansion. While the market is competitive, strategic collaborations and mergers & acquisitions (M&A) are shaping its landscape. For instance, significant M&A activities are anticipated to further consolidate the market, with projected deal values in the multi-million dollar range as larger entities acquire innovative startups to expand their technology portfolios and market reach. Innovation drivers include the pursuit of higher resolution, faster print speeds, and the development of advanced materials like high-performance polymers and novel metal alloys. Regulatory frameworks are evolving to support safety, standardization, and intellectual property protection, fostering trust and adoption across diverse end-user industries such as aerospace, automotive, and healthcare. The increasing demand for customized products, on-demand manufacturing, and reduced lead times are significant end-user trends influencing investment and R&D. The threat of product substitutes, such as traditional manufacturing methods, is diminishing as AM technologies mature and offer competitive advantages in terms of cost-effectiveness for low-volume production and complex geometries.

Additive Manufacturing Industry Industry Trends & Insights

The Additive Manufacturing industry is poised for substantial growth, projected to achieve a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This robust expansion is fueled by a confluence of technological breakthroughs, evolving consumer preferences, and strategic industry initiatives. The market penetration of AM technologies is steadily increasing across various sectors, driven by its inherent advantages of design freedom, material efficiency, and rapid prototyping capabilities. Key growth drivers include the escalating demand for lightweight and complex components in the aerospace and defense sector, enabling fuel efficiency and enhanced performance. In the automotive industry, AM is revolutionizing the production of customized parts, tooling, and even end-use components, leading to reduced lead times and lower manufacturing costs. The healthcare sector is experiencing a significant transformation with the use of AM for patient-specific implants, prosthetics, surgical guides, and bioprinting applications, promising personalized and more effective medical treatments.

Technological disruptions are a constant feature of the AM landscape. Advancements in materials science are leading to the development of novel filaments, powders, and resins with enhanced mechanical, thermal, and biocompatible properties. Simultaneously, innovations in printing technologies, such as faster print speeds, higher resolution, and multi-material capabilities, are expanding the range of applications and improving the economics of AM. The emergence of large-format AM systems is enabling the production of larger, more complex structures, further pushing the boundaries of what is possible.

Consumer preferences are increasingly leaning towards personalized and on-demand products, a trend perfectly aligned with the capabilities of additive manufacturing. This shift is driving the adoption of AM for consumer goods, fashion, and customized medical devices. Furthermore, the industry is witnessing a growing emphasis on sustainability, with AM offering the potential for reduced material waste and localized production, thereby lowering transportation emissions.

Competitive dynamics are intensifying as established players and new entrants vie for market share. Strategic partnerships, such as the recent collaboration between Merz Dental and Nexa 3D, highlight the industry's focus on expanding market reach and developing specialized solutions. The ongoing evolution of the AM ecosystem, encompassing hardware, software, materials, and services, is creating a fertile ground for innovation and market expansion. The market size is expected to reach over a million dollars by the estimated year of 2025, with continuous growth projected throughout the forecast period.

Dominant Markets & Segments in Additive Manufacturing Industry

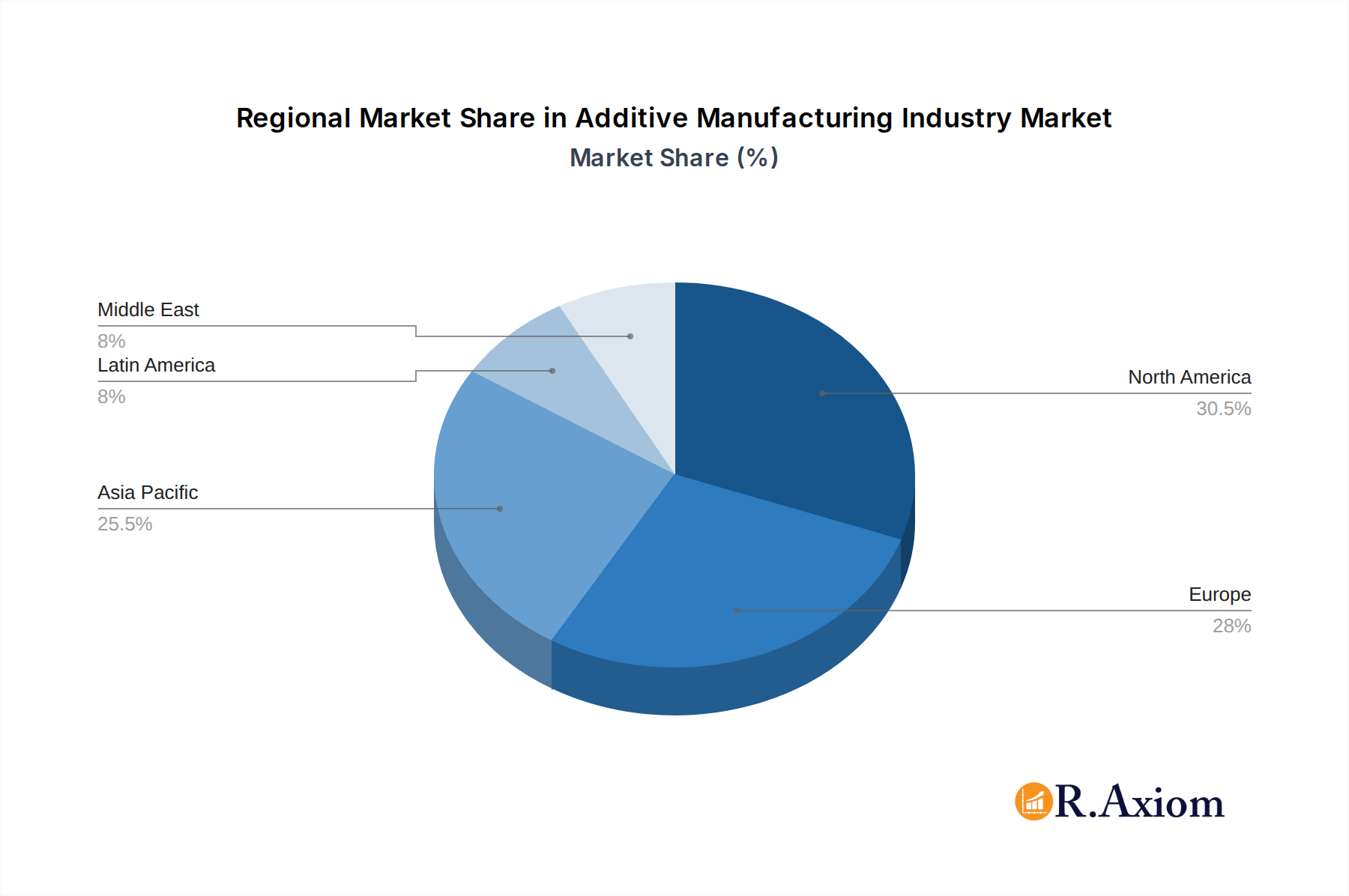

The Additive Manufacturing industry's dominance is multifaceted, with specific regions, countries, and segments exhibiting significant leadership. North America and Europe are currently the leading geographical markets, driven by strong government support, advanced technological infrastructure, and a high concentration of key industry players. Within these regions, countries like the United States, Germany, and France are at the forefront of AM adoption and innovation.

Technology Dominance:

- Laser Sintering (LS): This technology holds a dominant position, particularly in the production of complex metal and polymer parts for high-demand industries like aerospace and automotive. Its ability to produce strong, durable parts with excellent surface finish makes it a preferred choice for critical applications.

- Fused Deposition Modeling (FDM) / Fused Filament Fabrication (FFF): This technology is widely adopted for prototyping, tooling, and functional part production due to its cost-effectiveness, ease of use, and wide range of available materials. It is a significant driver of market penetration in industrial and educational sectors.

- Stereo Lithography (SLA): SLA excels in producing highly detailed and accurate parts, making it a dominant force in areas requiring high precision, such as dental applications, jewelry design, and intricate prototypes.

- Binder Jetting Printing: This technology is gaining increasing prominence, especially for its capability in mass production of metal parts, exemplified by GE Additive's recent advancements. Its potential for high throughput and cost-effectiveness at scale positions it for significant future growth.

End-User Dominance:

- Aerospace and Defense: This sector is a leading adopter of AM due to the critical need for lightweight, high-strength components, complex geometries, and on-demand part production for aircraft and defense systems. The ability to consolidate parts and reduce assembly time is a major advantage.

- Automotive: The automotive industry is rapidly embracing AM for prototyping, tooling, jigs, fixtures, and increasingly for producing end-use parts. The drive for customization, faster development cycles, and lightweighting makes AM an indispensable tool.

- Healthcare: AM is revolutionizing healthcare through patient-specific implants, prosthetics, dental solutions (orthodontic models, splints, surgical guides), and surgical tools. The ability to create customized medical devices tailored to individual patient anatomy is a key driver of dominance.

- Industrial: This broad segment encompasses manufacturing, tooling, and heavy machinery, where AM is utilized for creating complex tooling, spare parts, and specialized components, leading to improved efficiency and reduced downtime.

Material Dominance:

- Metals: The demand for high-performance metal parts in aerospace, automotive, and medical implants drives the dominance of metal AM. Advancements in metal powders and printing processes are continuously expanding its applications.

- Plastics: Plastics remain a dominant material category due to their versatility, cost-effectiveness, and widespread use in prototyping, consumer goods, and various industrial applications. Innovations in engineering-grade polymers are further enhancing their performance capabilities.

- Ceramics: While still an emerging segment compared to metals and plastics, ceramic AM is gaining traction for applications requiring high temperature resistance, chemical inertness, and wear resistance, particularly in specialized industrial and aerospace components.

Additive Manufacturing Industry Product Developments

Product innovations in the Additive Manufacturing industry are continuously expanding its capabilities and market reach. Recent developments highlight a focus on speed, precision, and material versatility. Companies are introducing advanced printers that offer significantly faster build times and higher resolutions, enabling the production of intricate and functional parts with exceptional accuracy. The development of novel material formulations, including advanced metal alloys, high-performance polymers, and biocompatible materials, is further broadening the application spectrum of AM. These advancements allow for the creation of components with enhanced mechanical properties, thermal resistance, and specialized functionalities, providing significant competitive advantages for manufacturers seeking to optimize designs and improve product performance across diverse sectors.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Additive Manufacturing industry, segmented across key dimensions to offer detailed insights. The Technology segmentation includes Stereo Lithography, Fused Deposition Modelling, Laser Sintering, Binder Jetting Printing, and Other Technologies. Each technology is analyzed for its market size, growth projections, and competitive dynamics, with Binder Jetting Printing expected to show significant future expansion due to its industrial-scale capabilities. The End User segmentation covers Aerospace and Defense, Automotive, Healthcare, Industrial, and Other End Users. The Aerospace and Defense and Healthcare segments are anticipated to experience robust growth due to the demand for specialized and customized solutions. The Material segmentation includes Plastic, Metals, and Ceramics. Metals and Plastics currently dominate the market, with Ceramics representing a rapidly growing niche market with high-value applications.

Key Drivers of Additive Manufacturing Industry Growth

The growth of the Additive Manufacturing industry is propelled by several interconnected factors. Technologically, the relentless pace of innovation in 3D printing hardware, software, and materials is a primary driver, enabling greater precision, speed, and complexity. Economically, the increasing demand for mass customization, on-demand production, and reduced lead times across industries like automotive and aerospace fuels AM adoption. The ability to reduce manufacturing costs for low-volume production and complex geometries is also a significant economic catalyst. Regulatory frameworks are increasingly supportive, with standardization initiatives and policies promoting the use of AM in critical sectors, fostering greater trust and investment. Furthermore, the growing emphasis on supply chain resilience and localized manufacturing further bolsters the appeal of additive manufacturing solutions.

Challenges in the Additive Manufacturing Industry Sector

Despite its immense potential, the Additive Manufacturing industry faces several challenges that can impede its widespread adoption and growth. Regulatory hurdles, particularly in highly regulated sectors like aerospace and healthcare, can slow down the approval and implementation of AM-produced parts. Supply chain issues, including the availability and consistency of high-quality raw materials, can impact production reliability and cost. Competitive pressures from established manufacturing methods, especially for high-volume production, still exist. Furthermore, the lack of a standardized workforce with the necessary skills and expertise in AM technologies presents a significant barrier. The initial capital investment for advanced AM equipment can also be substantial, posing a challenge for smaller enterprises.

Emerging Opportunities in Additive Manufacturing Industry

The Additive Manufacturing industry is ripe with emerging opportunities driven by continuous innovation and evolving market needs. The development of new advanced materials with enhanced properties, such as high-temperature resistance, conductivity, and biocompatibility, will unlock novel applications in specialized industries. The integration of artificial intelligence (AI) and machine learning (ML) into AM workflows for design optimization, process control, and quality assurance promises significant efficiency gains. The expansion of AM into new markets, including construction (3D printed buildings), food production, and sustainable energy solutions, presents vast growth potential. Furthermore, the increasing focus on circular economy principles will drive opportunities for AM in recycling and remanufacturing applications, reducing waste and promoting sustainability.

Leading Players in the Additive Manufacturing Industry Market

- Mcor Technologies Ltd

- General Electric Company (GE Additive)

- Optomec Inc

- 3D Systems Corporation

- Exone Company

- SLM Solutions Group AG

- EOS GmbH

- Materialise NV

- Stratasys Ltd

- EnvisionTEC GmbH

Key Developments in Additive Manufacturing Industry Industry

- March 2023: Merz Dental, a digital dentistry company, partnered with Nexa 3D, the polymer 3D printing leader. The partnership will support the consumers of Nexa 3D throughout Germany. The 3D printing platform is fast and accurate to increase professional and dental desktop 3D printing use. The desktop 3D printer serves a wide variety of engineering and dental applications, including orthodontic models, splints, and surgical guides.

- October 2022: US-based GE Additive launched its new Series 3 binder jet platform. This machine will help to create metal parts like castings on an industrial scale. The company has manufactured over 140,000 such components, which are 15% more fuel efficient than standard.

- July 2022: Toyota started producing stock parts using HP Multi Jet Fusion 3D printing and sold them alongside conventionally manufactured spares. This will assist the automotive company in optimizing the designs and lead times of newly-developed parts.

Strategic Outlook for Additive Manufacturing Industry Market

The strategic outlook for the Additive Manufacturing industry market is exceptionally promising, driven by sustained innovation and expanding applications across diverse sectors. Future growth catalysts will include the continued development of advanced materials, enabling the production of components with superior performance characteristics for demanding industries like aerospace, automotive, and healthcare. The increasing adoption of digital manufacturing strategies, including the integration of AI and ML for design optimization and process control, will further enhance efficiency and scalability. The growing demand for sustainable manufacturing solutions, where AM offers reduced material waste and localized production, will also play a crucial role. Strategic partnerships and M&A activities are expected to consolidate the market, fostering further technological advancements and broader market penetration, ensuring robust growth throughout the forecast period and beyond.

Additive Manufacturing Industry Segmentation

-

1. Technology

- 1.1. Stereo Lithography

- 1.2. Fused Deposition Modelling

- 1.3. Laser Sintering

- 1.4. Binder Jetting Printing

- 1.5. Other Technologies

-

2. End User

- 2.1. Aerospace and Defense

- 2.2. Automotive

- 2.3. Healthcare

- 2.4. Industrial

- 2.5. Other End Users

-

3. Material

- 3.1. Plastic

- 3.2. Metals

- 3.3. Ceramics

Additive Manufacturing Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Argentina

- 4.4. Rest of Latin America

- 5. Middle East

-

6. UAE

- 6.1. Saudi Arabia

- 6.2. Israel

- 6.3. South Africa

- 6.4. Rest of Middle East

Additive Manufacturing Industry Regional Market Share

Geographic Coverage of Additive Manufacturing Industry

Additive Manufacturing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Stereo Lithography

- 5.1.2. Fused Deposition Modelling

- 5.1.3. Laser Sintering

- 5.1.4. Binder Jetting Printing

- 5.1.5. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Aerospace and Defense

- 5.2.2. Automotive

- 5.2.3. Healthcare

- 5.2.4. Industrial

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Material

- 5.3.1. Plastic

- 5.3.2. Metals

- 5.3.3. Ceramics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East

- 5.4.6. UAE

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Additive Manufacturing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Stereo Lithography

- 6.1.2. Fused Deposition Modelling

- 6.1.3. Laser Sintering

- 6.1.4. Binder Jetting Printing

- 6.1.5. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Aerospace and Defense

- 6.2.2. Automotive

- 6.2.3. Healthcare

- 6.2.4. Industrial

- 6.2.5. Other End Users

- 6.3. Market Analysis, Insights and Forecast - by Material

- 6.3.1. Plastic

- 6.3.2. Metals

- 6.3.3. Ceramics

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Additive Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Stereo Lithography

- 7.1.2. Fused Deposition Modelling

- 7.1.3. Laser Sintering

- 7.1.4. Binder Jetting Printing

- 7.1.5. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Aerospace and Defense

- 7.2.2. Automotive

- 7.2.3. Healthcare

- 7.2.4. Industrial

- 7.2.5. Other End Users

- 7.3. Market Analysis, Insights and Forecast - by Material

- 7.3.1. Plastic

- 7.3.2. Metals

- 7.3.3. Ceramics

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Additive Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Stereo Lithography

- 8.1.2. Fused Deposition Modelling

- 8.1.3. Laser Sintering

- 8.1.4. Binder Jetting Printing

- 8.1.5. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Aerospace and Defense

- 8.2.2. Automotive

- 8.2.3. Healthcare

- 8.2.4. Industrial

- 8.2.5. Other End Users

- 8.3. Market Analysis, Insights and Forecast - by Material

- 8.3.1. Plastic

- 8.3.2. Metals

- 8.3.3. Ceramics

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Pacific Additive Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Stereo Lithography

- 9.1.2. Fused Deposition Modelling

- 9.1.3. Laser Sintering

- 9.1.4. Binder Jetting Printing

- 9.1.5. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Aerospace and Defense

- 9.2.2. Automotive

- 9.2.3. Healthcare

- 9.2.4. Industrial

- 9.2.5. Other End Users

- 9.3. Market Analysis, Insights and Forecast - by Material

- 9.3.1. Plastic

- 9.3.2. Metals

- 9.3.3. Ceramics

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Latin America Additive Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Stereo Lithography

- 10.1.2. Fused Deposition Modelling

- 10.1.3. Laser Sintering

- 10.1.4. Binder Jetting Printing

- 10.1.5. Other Technologies

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Aerospace and Defense

- 10.2.2. Automotive

- 10.2.3. Healthcare

- 10.2.4. Industrial

- 10.2.5. Other End Users

- 10.3. Market Analysis, Insights and Forecast - by Material

- 10.3.1. Plastic

- 10.3.2. Metals

- 10.3.3. Ceramics

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Middle East Additive Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Stereo Lithography

- 11.1.2. Fused Deposition Modelling

- 11.1.3. Laser Sintering

- 11.1.4. Binder Jetting Printing

- 11.1.5. Other Technologies

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Aerospace and Defense

- 11.2.2. Automotive

- 11.2.3. Healthcare

- 11.2.4. Industrial

- 11.2.5. Other End Users

- 11.3. Market Analysis, Insights and Forecast - by Material

- 11.3.1. Plastic

- 11.3.2. Metals

- 11.3.3. Ceramics

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. UAE Additive Manufacturing Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Technology

- 12.1.1. Stereo Lithography

- 12.1.2. Fused Deposition Modelling

- 12.1.3. Laser Sintering

- 12.1.4. Binder Jetting Printing

- 12.1.5. Other Technologies

- 12.2. Market Analysis, Insights and Forecast - by End User

- 12.2.1. Aerospace and Defense

- 12.2.2. Automotive

- 12.2.3. Healthcare

- 12.2.4. Industrial

- 12.2.5. Other End Users

- 12.3. Market Analysis, Insights and Forecast - by Material

- 12.3.1. Plastic

- 12.3.2. Metals

- 12.3.3. Ceramics

- 12.1. Market Analysis, Insights and Forecast - by Technology

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Mcor Technologies Ltd

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 General Electric Company (GE Additive)

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Optomec Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 3D Systems Corporation

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Exone Company

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 SLM Solutions Group AG*List Not Exhaustive

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 EOS GmbH

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Materialise NV

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Stratasys Ltd

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 EnvisionTEC GmbH

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Mcor Technologies Ltd

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Additive Manufacturing Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Additive Manufacturing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 3: North America Additive Manufacturing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Additive Manufacturing Industry Revenue (Million), by End User 2025 & 2033

- Figure 5: North America Additive Manufacturing Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Additive Manufacturing Industry Revenue (Million), by Material 2025 & 2033

- Figure 7: North America Additive Manufacturing Industry Revenue Share (%), by Material 2025 & 2033

- Figure 8: North America Additive Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Additive Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Additive Manufacturing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 11: Europe Additive Manufacturing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 12: Europe Additive Manufacturing Industry Revenue (Million), by End User 2025 & 2033

- Figure 13: Europe Additive Manufacturing Industry Revenue Share (%), by End User 2025 & 2033

- Figure 14: Europe Additive Manufacturing Industry Revenue (Million), by Material 2025 & 2033

- Figure 15: Europe Additive Manufacturing Industry Revenue Share (%), by Material 2025 & 2033

- Figure 16: Europe Additive Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Additive Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Additive Manufacturing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 19: Asia Pacific Additive Manufacturing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 20: Asia Pacific Additive Manufacturing Industry Revenue (Million), by End User 2025 & 2033

- Figure 21: Asia Pacific Additive Manufacturing Industry Revenue Share (%), by End User 2025 & 2033

- Figure 22: Asia Pacific Additive Manufacturing Industry Revenue (Million), by Material 2025 & 2033

- Figure 23: Asia Pacific Additive Manufacturing Industry Revenue Share (%), by Material 2025 & 2033

- Figure 24: Asia Pacific Additive Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Additive Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Additive Manufacturing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 27: Latin America Additive Manufacturing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Latin America Additive Manufacturing Industry Revenue (Million), by End User 2025 & 2033

- Figure 29: Latin America Additive Manufacturing Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Latin America Additive Manufacturing Industry Revenue (Million), by Material 2025 & 2033

- Figure 31: Latin America Additive Manufacturing Industry Revenue Share (%), by Material 2025 & 2033

- Figure 32: Latin America Additive Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America Additive Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East Additive Manufacturing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 35: Middle East Additive Manufacturing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 36: Middle East Additive Manufacturing Industry Revenue (Million), by End User 2025 & 2033

- Figure 37: Middle East Additive Manufacturing Industry Revenue Share (%), by End User 2025 & 2033

- Figure 38: Middle East Additive Manufacturing Industry Revenue (Million), by Material 2025 & 2033

- Figure 39: Middle East Additive Manufacturing Industry Revenue Share (%), by Material 2025 & 2033

- Figure 40: Middle East Additive Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East Additive Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: UAE Additive Manufacturing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 43: UAE Additive Manufacturing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 44: UAE Additive Manufacturing Industry Revenue (Million), by End User 2025 & 2033

- Figure 45: UAE Additive Manufacturing Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: UAE Additive Manufacturing Industry Revenue (Million), by Material 2025 & 2033

- Figure 47: UAE Additive Manufacturing Industry Revenue Share (%), by Material 2025 & 2033

- Figure 48: UAE Additive Manufacturing Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: UAE Additive Manufacturing Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 2: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 4: Global Additive Manufacturing Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 6: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 7: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 8: Global Additive Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 12: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 13: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 14: Global Additive Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 20: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 21: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 22: Global Additive Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: China Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Japan Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: India Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 28: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 29: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 30: Global Additive Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Brazil Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Mexico Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Argentina Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of Latin America Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 36: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 37: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 38: Global Additive Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 39: Global Additive Manufacturing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 40: Global Additive Manufacturing Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 41: Global Additive Manufacturing Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 42: Global Additive Manufacturing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 43: Saudi Arabia Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Israel Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: South Africa Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East Additive Manufacturing Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Additive Manufacturing Industry?

The projected CAGR is approximately 20.70%.

2. Which companies are prominent players in the Additive Manufacturing Industry?

Key companies in the market include Mcor Technologies Ltd, General Electric Company (GE Additive), Optomec Inc, 3D Systems Corporation, Exone Company, SLM Solutions Group AG*List Not Exhaustive, EOS GmbH, Materialise NV, Stratasys Ltd, EnvisionTEC GmbH.

3. What are the main segments of the Additive Manufacturing Industry?

The market segments include Technology, End User, Material.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.93 Million as of 2022.

5. What are some drivers contributing to market growth?

New and Improved Technologies to Drive Product Customization; Demand for Lightweight Construction in Automotive and Aerospace Industries.

6. What are the notable trends driving market growth?

Automotive to is expected Hold a Significant Share.

7. Are there any restraints impacting market growth?

Concerns over Intellectual Property Protection.

8. Can you provide examples of recent developments in the market?

March 2023 - Merz Dental, a digital dentistry company, partnered with Nexa 3D, the polymer 3D printing leader. The partnership will support the consumers of Nexa 3D throughout Germany. The 3D printing platform is fast and accurate to increase professional and dental desktop 3D printing use. The desktop 3D printer serves a wide variety of engineering and dental applications, including orthodontic models, splints, and surgical guides

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Additive Manufacturing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Additive Manufacturing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Additive Manufacturing Industry?

To stay informed about further developments, trends, and reports in the Additive Manufacturing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence