Key Insights

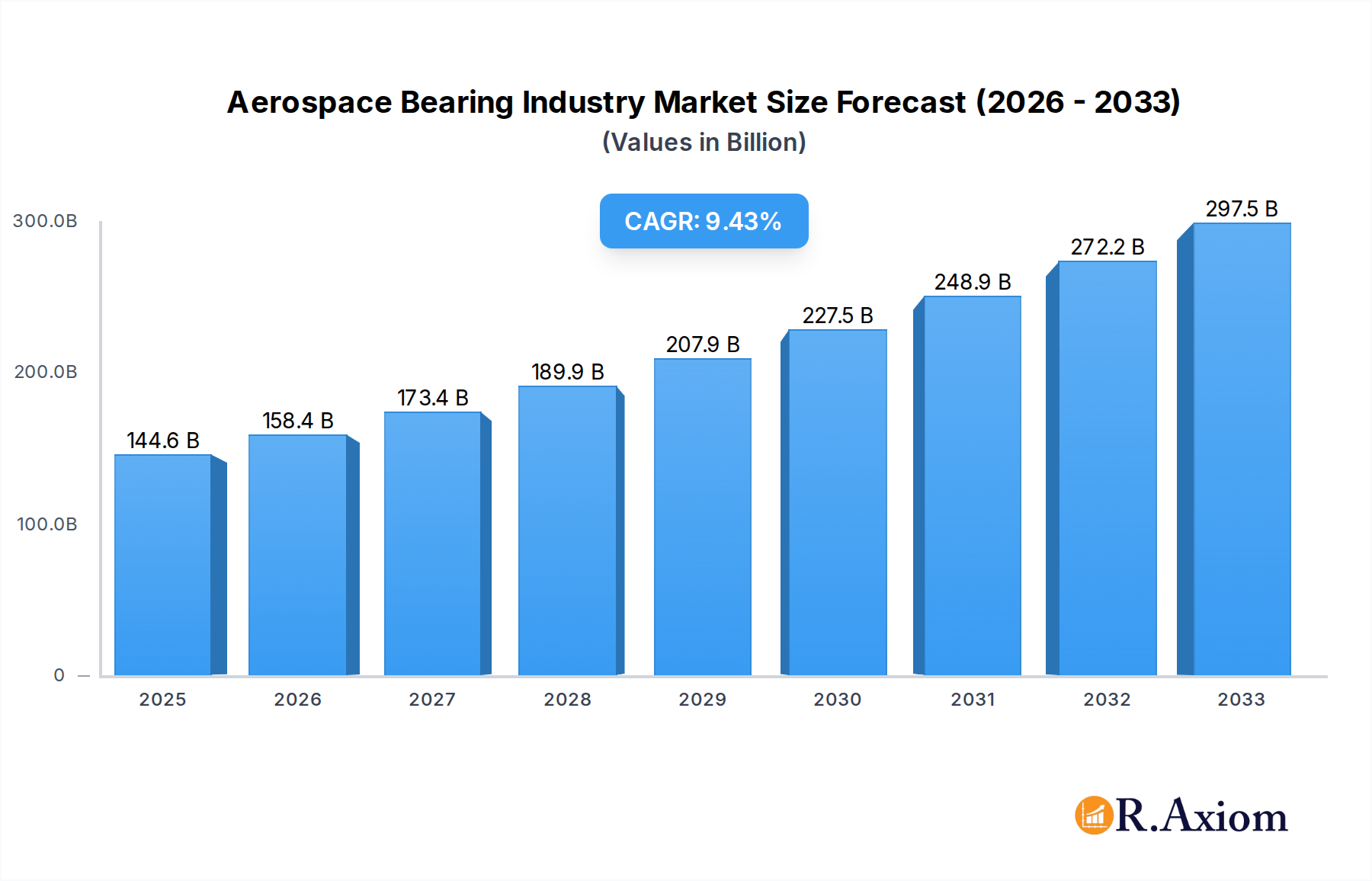

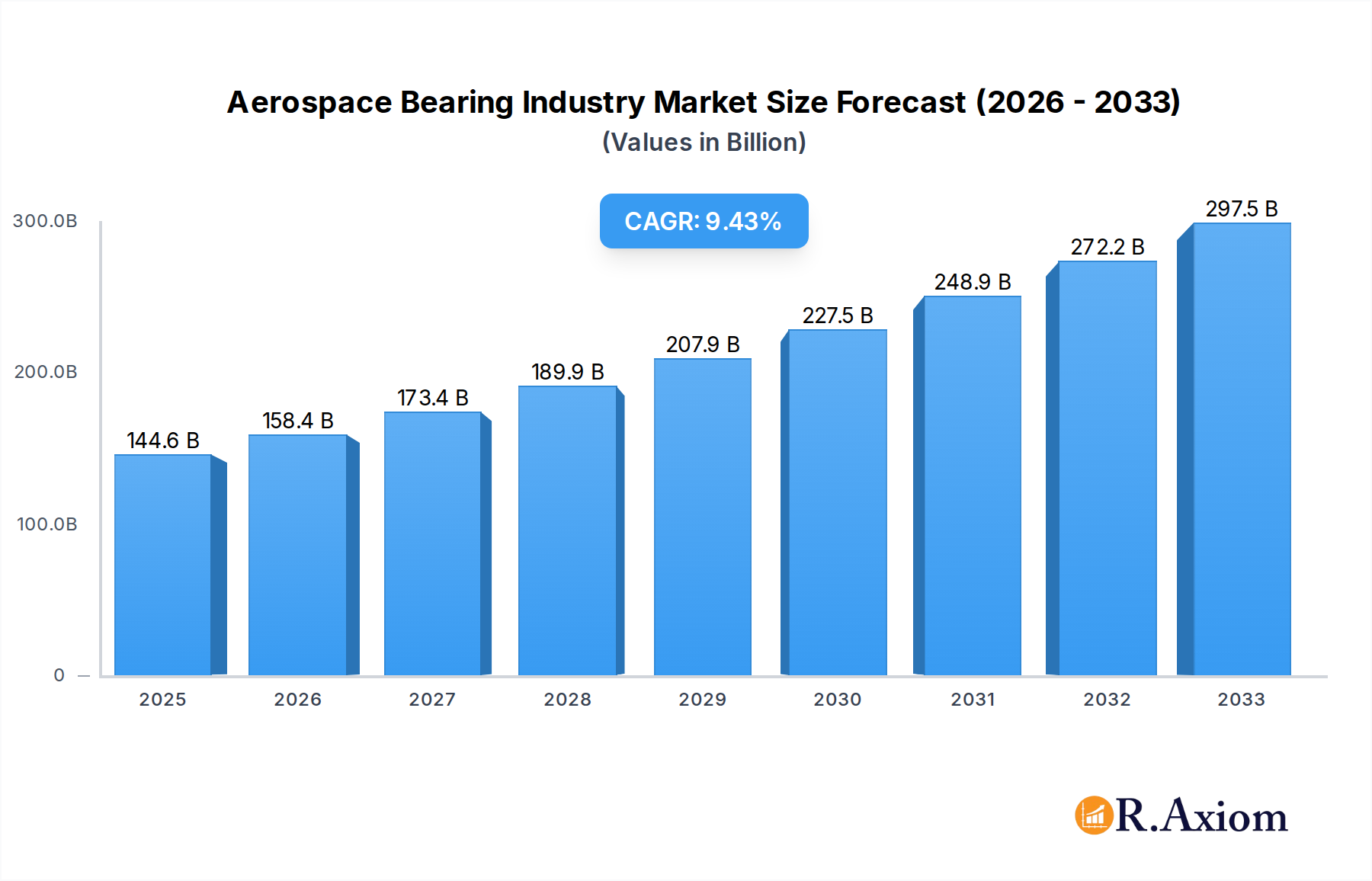

The global Aerospace Bearing Industry is poised for significant expansion, projecting a market size of $144,622.03 million in 2025 and a robust CAGR of 9.5% throughout the forecast period. This growth is underpinned by escalating demand for commercial aircraft, driven by increased air travel post-pandemic and the expansion of global trade routes. Furthermore, the defense sector's continuous need for advanced aircraft, including fighter jets and transport planes, alongside the burgeoning drone market for both military and civilian applications, are substantial growth catalysts. Innovations in material science, leading to lighter and more durable bearings, and advancements in bearing technology such as smart bearings with integrated sensors for predictive maintenance, are also key drivers. The industry is seeing a strong emphasis on performance, reliability, and reduced lifecycle costs, pushing manufacturers to develop more sophisticated and efficient bearing solutions.

Aerospace Bearing Industry Market Size (In Billion)

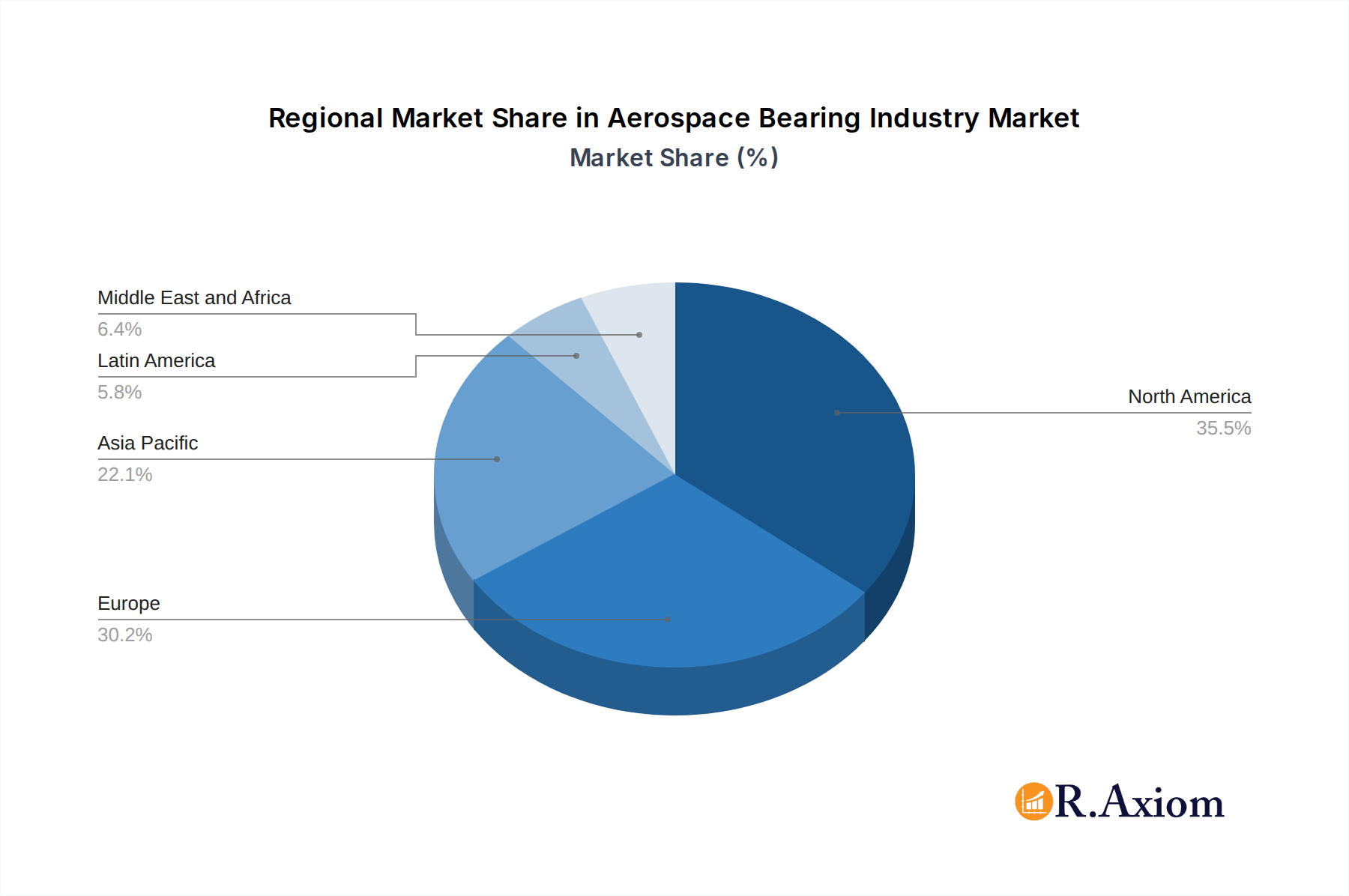

The market segmentation reveals a dynamic landscape with Fixed-wing aircraft dominating the platform segment, reflecting their widespread use in both commercial and military aviation. Within product types, Ball Bearings and Roller Bearings are expected to hold the largest share due to their versatility and proven performance in demanding aerospace environments. Applications like Engine and Aero-Structures are crucial, demanding high-precision and failure-resistant bearings. Key players like JTEKT, Kaman Speciality Bearings, and New Hampshire Ball Bearings are at the forefront of innovation, investing in research and development to meet evolving industry requirements. Geographically, North America and Europe are the leading markets, owing to the presence of major aircraft manufacturers and extensive MRO (Maintenance, Repair, and Overhaul) activities. However, the Asia Pacific region is expected to witness the fastest growth, fueled by the expanding aerospace manufacturing base in countries like China and India and increasing air connectivity.

Aerospace Bearing Industry Company Market Share

This comprehensive report delves into the dynamic Aerospace Bearing Industry, providing in-depth analysis and actionable insights for stakeholders. Covering the Study Period: 2019–2033, with Base Year: 2025, Estimated Year: 2025, and Forecast Period: 2025–2033, this research meticulously examines historical trends from 2019–2024. The global aerospace bearing market is projected to witness robust growth, driven by increasing demand for commercial and defense aircraft, coupled with advancements in lightweight materials and stringent safety regulations. The market encompasses a wide range of products including plain bearings, roller bearings, ball bearings, roller screws, and ball screws, crucial for applications in fixed-wing aircraft, rotary-wing aircraft, and UAVs. Key application areas include engines, aero-structures, landing gear, and other critical components. This report offers a strategic overview, detailed segmentation, competitive landscape, and future outlook for this vital industry.

Aerospace Bearing Industry Market Concentration & Innovation

The Aerospace Bearing Industry exhibits a moderate level of market concentration, with a few dominant players alongside a significant number of specialized manufacturers. Innovation remains a key differentiator, driven by the relentless pursuit of enhanced performance, reduced weight, and increased durability for aerospace applications. Regulatory frameworks, particularly those set by aviation authorities like the FAA and EASA, play a crucial role in shaping product development and market entry, ensuring the highest safety standards. Product substitutes, while present, often struggle to match the specialized performance and reliability requirements of aerospace bearings. End-user trends are increasingly focused on fuel efficiency, reduced maintenance, and the integration of smart technologies within bearing systems. Mergers and acquisitions (M&A) activities, with estimated deal values in the hundreds of millions, are instrumental in consolidating market share, expanding product portfolios, and acquiring critical technologies. For instance, strategic acquisitions in the past few years have seen companies bolstering their capabilities in advanced composite bearings and high-performance alloys, contributing to an estimated market share shift of several percentage points for acquiring entities. The continuous drive for miniaturization and increased load-bearing capacity without compromising on weight further fuels innovation within this sector.

Aerospace Bearing Industry Industry Trends & Insights

The Aerospace Bearing Industry is poised for significant expansion, with an anticipated Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period. This growth is propelled by a confluence of factors, including the post-pandemic surge in air travel, leading to increased demand for new aircraft and MRO services, and a substantial backlog of aircraft orders from both commercial airlines and defense sectors. Technological disruptions are at the forefront, with the increasing adoption of advanced composite materials for bearings offering superior strength-to-weight ratios and corrosion resistance. The integration of smart sensors and predictive maintenance capabilities within bearing systems is another transformative trend, enabling real-time monitoring and proactive issue resolution, thereby reducing downtime and operational costs. Consumer preferences, in this context, translate to an airline's demand for bearings that contribute to lower fuel consumption and extended service life. The competitive dynamics are characterized by intense R&D efforts, strategic partnerships, and a focus on niche markets. Market penetration of advanced bearing technologies is expected to deepen, particularly in the UAV and business aviation segments, where the demand for high-performance, lightweight solutions is paramount. Furthermore, governmental investments in defense modernization and space exploration are creating new avenues for growth and innovation in specialized aerospace bearings. The persistent need for reliability and safety in aerospace operations ensures that market penetration of certified, high-quality bearings remains a priority for all aircraft manufacturers.

Dominant Markets & Segments in Aerospace Bearing Industry

The Fixed-wing Platform segment is anticipated to continue its dominance in the aerospace bearing market, driven by the sheer volume of commercial aircraft production and extensive military aviation fleets. Within this segment, Engine applications represent a substantial market share, as bearings are critical components for propulsion systems, requiring extreme precision, high-temperature resistance, and unparalleled reliability. Economic policies favoring aviation infrastructure development and the growing demand for air cargo services are key drivers. The Asia-Pacific region is emerging as a significant growth hub, fueled by expanding domestic air travel, increasing defense budgets, and the establishment of local aerospace manufacturing capabilities.

- Key Drivers for Fixed-wing Dominance:

- Robust demand for commercial passenger and cargo aircraft.

- Significant investments in military aviation modernization programs globally.

- Technological advancements in engine efficiency and aircraft design.

- Expanding airline networks and increasing air passenger traffic.

Within Product Type, Roller Bearings and Ball Bearings are expected to capture the largest market share due to their widespread application across various aircraft systems, from landing gear to control surfaces. Their ability to handle high loads and rotational speeds makes them indispensable.

- Key Drivers for Roller & Ball Bearing Dominance:

- Proven reliability and performance in demanding aerospace environments.

- Versatility in handling radial and axial loads.

- Continuous improvements in material science and manufacturing techniques.

In terms of Application, Engine bearings are crucial, demanding the highest levels of precision and material integrity. Landing Gear applications are also critical, requiring bearings that can withstand immense shock loads and operational stresses.

- Key Drivers for Engine & Landing Gear Application Dominance:

- Critical safety and performance requirements for these vital aircraft systems.

- Continuous innovation in materials and lubrication for extreme conditions.

- Stringent certification processes ensuring utmost reliability.

The UAVs (Unmanned Aerial Vehicles) segment is experiencing the fastest growth, driven by increased military surveillance and reconnaissance missions, burgeoning commercial drone applications in logistics, agriculture, and infrastructure inspection, and ongoing research and development in autonomous flight systems.

- Key Drivers for UAV Segment Growth:

- Rapid expansion of military and commercial drone markets.

- Demand for lightweight, high-performance bearings for compact designs.

- Advancements in battery technology enabling longer flight times.

Aerospace Bearing Industry Product Developments

Product development in the aerospace bearing industry is intensely focused on enhancing material properties, reducing weight, and improving operational efficiency. Innovations include the development of advanced ceramic and composite bearings that offer superior performance in extreme temperatures and corrosive environments, alongside increased resistance to wear and fatigue. The integration of lubrication-free technologies and self-monitoring capabilities represents a significant competitive advantage, addressing the industry's demand for reduced maintenance and increased reliability. These developments are crucial for enabling next-generation aircraft designs and supporting the growing UAV sector.

Report Scope & Segmentation Analysis

This report segments the Aerospace Bearing Industry by Platform: Fixed-wing, Rotary Wing, and UAVs. The Fixed-wing segment is expected to maintain its leadership due to established markets. The Rotary Wing segment, encompassing helicopters, is critical for defense and specialized civilian operations. The UAVs segment is projected for the highest growth rate, driven by diverse applications.

The market is further segmented by Product Type: Plain bearings, Roller Bearings, Ball Bearings, Roller Screws, and Ball Screws. Roller Bearings and Ball Bearings are anticipated to hold significant market share. Roller Screws and Ball Screws are increasingly vital for actuation systems.

By Application, the report analyzes: Engine, Aero-Structures, Landing Gear, and Other Application. Engine and Landing Gear applications are paramount due to their critical role in aircraft safety and performance, and are expected to see substantial market sizes with consistent growth.

Key Drivers of Aerospace Bearing Industry Growth

The aerospace bearing industry's growth is primarily fueled by the steady increase in global air travel, driving demand for new commercial aircraft and replacement parts. Advancements in material science, leading to the development of lightweight yet incredibly durable composite and ceramic bearings, are critical innovation drivers. Furthermore, significant investments in defense sector modernization, including the development of advanced fighter jets and unmanned aerial vehicles, contribute substantially to market expansion. Stringent regulatory requirements for safety and performance in aviation also necessitate continuous product improvement and the adoption of cutting-edge bearing technologies. The burgeoning UAV market, with its diverse applications from surveillance to delivery, presents a particularly strong growth catalyst.

Challenges in the Aerospace Bearing Industry Sector

Despite robust growth prospects, the aerospace bearing industry faces several challenges. The extremely rigorous and lengthy certification processes for new aerospace components can significantly delay market entry and increase development costs. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, pose a persistent threat to production schedules and cost management. Intense competition from established players and emerging manufacturers, particularly from low-cost regions, puts pressure on profit margins. Furthermore, the high initial investment required for advanced manufacturing technologies and R&D can be a barrier for smaller companies. The industry's dependence on highly skilled labor for manufacturing and engineering also presents a challenge in terms of talent acquisition and retention.

Emerging Opportunities in Aerospace Bearing Industry

Emerging opportunities within the aerospace bearing industry are abundant and diverse. The rapid growth of the Unmanned Aerial Vehicle (UAV) sector, spanning defense, logistics, and agriculture, is creating substantial demand for specialized, lightweight, and high-performance bearings. The increasing focus on sustainable aviation and the development of electric and hybrid-electric aircraft present opportunities for novel bearing solutions that minimize friction and energy consumption. Furthermore, advancements in additive manufacturing (3D printing) offer the potential for producing complex, customized bearing components with improved material properties and reduced lead times. The growing trend towards digitalization and smart systems in aviation, including the integration of sensors for predictive maintenance within bearings, opens up new service-based revenue streams.

Leading Players in the Aerospace Bearing Industry Market

- August Steinmeyer GmbH

- JTEKT

- Beaver Aerospace and Defense Inc

- GGB Bearings Technology

- Kugel Aerospace and Defense

- New Hamphshire Ball bearings

- Kaman Speciality Bearings

- National Precision Bearings

- AST Bearings

- UmbraGroup

- Thomson Industries Inc

- Aurora Bearings

Key Developments in Aerospace Bearing Industry Industry

- October 2022: Marsh Brothers Aviation enhanced the low-weight appeal of DarkAero composite kit aircraft by providing composite bearings for three different applications on the soon-to-launch DarkAero 1, a self-build solution emphasizing composite materials.

- May 2022: Rolls-Royce and Schaeffler announced a 12-year rolling bearing deal to secure Rolls-Royce's rolling bearing supply chain until 2035, leveraging Schaeffler's reliable products and manufacturing technologies, with a focus on rolling bearing systems for aircraft engines in business and widebody aircraft growth areas.

Strategic Outlook for Aerospace Bearing Industry Market

The strategic outlook for the Aerospace Bearing Industry is overwhelmingly positive, driven by sustained demand from both commercial and defense sectors. Future growth catalysts include the continued expansion of the UAV market, the development of next-generation aircraft with advanced propulsion systems, and the increasing adoption of lightweight composite materials. Opportunities abound in developing smart bearings with integrated sensors for predictive maintenance and in supporting the transition towards sustainable aviation technologies. Companies that invest in R&D, focus on niche applications, and forge strategic partnerships will be well-positioned to capitalize on the evolving landscape and secure substantial market share in the coming years.

Aerospace Bearing Industry Segmentation

-

1. Platform

- 1.1. Fixed-wing

- 1.2. Rotary Wing

- 1.3. UAVs

-

2. Product Type

- 2.1. Plain bearings

- 2.2. Roller Bearings

- 2.3. Ball Bearings

- 2.4. Roller Screws

- 2.5. Ball Screws

-

3. Application

- 3.1. Engine

- 3.2. Aero-Structures

- 3.3. Landing Gear

- 3.4. Other Application

Aerospace Bearing Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Mexico

- 4.2. Brazil

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. South Africa

- 5.4. Rest of Middle East and Africa

Aerospace Bearing Industry Regional Market Share

Geographic Coverage of Aerospace Bearing Industry

Aerospace Bearing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Platform

- 5.1.1. Fixed-wing

- 5.1.2. Rotary Wing

- 5.1.3. UAVs

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Plain bearings

- 5.2.2. Roller Bearings

- 5.2.3. Ball Bearings

- 5.2.4. Roller Screws

- 5.2.5. Ball Screws

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Engine

- 5.3.2. Aero-Structures

- 5.3.3. Landing Gear

- 5.3.4. Other Application

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Platform

- 6. Global Aerospace Bearing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Platform

- 6.1.1. Fixed-wing

- 6.1.2. Rotary Wing

- 6.1.3. UAVs

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Plain bearings

- 6.2.2. Roller Bearings

- 6.2.3. Ball Bearings

- 6.2.4. Roller Screws

- 6.2.5. Ball Screws

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Engine

- 6.3.2. Aero-Structures

- 6.3.3. Landing Gear

- 6.3.4. Other Application

- 6.1. Market Analysis, Insights and Forecast - by Platform

- 7. North America Aerospace Bearing Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Platform

- 7.1.1. Fixed-wing

- 7.1.2. Rotary Wing

- 7.1.3. UAVs

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Plain bearings

- 7.2.2. Roller Bearings

- 7.2.3. Ball Bearings

- 7.2.4. Roller Screws

- 7.2.5. Ball Screws

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Engine

- 7.3.2. Aero-Structures

- 7.3.3. Landing Gear

- 7.3.4. Other Application

- 7.1. Market Analysis, Insights and Forecast - by Platform

- 8. Europe Aerospace Bearing Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Platform

- 8.1.1. Fixed-wing

- 8.1.2. Rotary Wing

- 8.1.3. UAVs

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Plain bearings

- 8.2.2. Roller Bearings

- 8.2.3. Ball Bearings

- 8.2.4. Roller Screws

- 8.2.5. Ball Screws

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Engine

- 8.3.2. Aero-Structures

- 8.3.3. Landing Gear

- 8.3.4. Other Application

- 8.1. Market Analysis, Insights and Forecast - by Platform

- 9. Asia Pacific Aerospace Bearing Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Platform

- 9.1.1. Fixed-wing

- 9.1.2. Rotary Wing

- 9.1.3. UAVs

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Plain bearings

- 9.2.2. Roller Bearings

- 9.2.3. Ball Bearings

- 9.2.4. Roller Screws

- 9.2.5. Ball Screws

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Engine

- 9.3.2. Aero-Structures

- 9.3.3. Landing Gear

- 9.3.4. Other Application

- 9.1. Market Analysis, Insights and Forecast - by Platform

- 10. Latin America Aerospace Bearing Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Platform

- 10.1.1. Fixed-wing

- 10.1.2. Rotary Wing

- 10.1.3. UAVs

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Plain bearings

- 10.2.2. Roller Bearings

- 10.2.3. Ball Bearings

- 10.2.4. Roller Screws

- 10.2.5. Ball Screws

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Engine

- 10.3.2. Aero-Structures

- 10.3.3. Landing Gear

- 10.3.4. Other Application

- 10.1. Market Analysis, Insights and Forecast - by Platform

- 11. Middle East and Africa Aerospace Bearing Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Platform

- 11.1.1. Fixed-wing

- 11.1.2. Rotary Wing

- 11.1.3. UAVs

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Plain bearings

- 11.2.2. Roller Bearings

- 11.2.3. Ball Bearings

- 11.2.4. Roller Screws

- 11.2.5. Ball Screws

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Engine

- 11.3.2. Aero-Structures

- 11.3.3. Landing Gear

- 11.3.4. Other Application

- 11.1. Market Analysis, Insights and Forecast - by Platform

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 August Steinmeyer GmbH

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 JTEKT

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Beaver Aerospace and Defense Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 GGB Bearings Technology

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Kugel Aerospace and Defense

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 New Hamphshire Ball bearings

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kaman Speciality Bearings

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 National Precision Bearings

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AST Bearings

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 UmbraGroup

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Thomson Industries Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Aurora Bearings

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 August Steinmeyer GmbH

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aerospace Bearing Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Aerospace Bearing Industry Revenue (billion), by Platform 2025 & 2033

- Figure 3: North America Aerospace Bearing Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 4: North America Aerospace Bearing Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 5: North America Aerospace Bearing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Aerospace Bearing Industry Revenue (billion), by Application 2025 & 2033

- Figure 7: North America Aerospace Bearing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Aerospace Bearing Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Aerospace Bearing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Aerospace Bearing Industry Revenue (billion), by Platform 2025 & 2033

- Figure 11: Europe Aerospace Bearing Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 12: Europe Aerospace Bearing Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 13: Europe Aerospace Bearing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: Europe Aerospace Bearing Industry Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Aerospace Bearing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aerospace Bearing Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Aerospace Bearing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Aerospace Bearing Industry Revenue (billion), by Platform 2025 & 2033

- Figure 19: Asia Pacific Aerospace Bearing Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 20: Asia Pacific Aerospace Bearing Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 21: Asia Pacific Aerospace Bearing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Asia Pacific Aerospace Bearing Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Asia Pacific Aerospace Bearing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Asia Pacific Aerospace Bearing Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Aerospace Bearing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Aerospace Bearing Industry Revenue (billion), by Platform 2025 & 2033

- Figure 27: Latin America Aerospace Bearing Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 28: Latin America Aerospace Bearing Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 29: Latin America Aerospace Bearing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Latin America Aerospace Bearing Industry Revenue (billion), by Application 2025 & 2033

- Figure 31: Latin America Aerospace Bearing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: Latin America Aerospace Bearing Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Aerospace Bearing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Aerospace Bearing Industry Revenue (billion), by Platform 2025 & 2033

- Figure 35: Middle East and Africa Aerospace Bearing Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 36: Middle East and Africa Aerospace Bearing Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 37: Middle East and Africa Aerospace Bearing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Middle East and Africa Aerospace Bearing Industry Revenue (billion), by Application 2025 & 2033

- Figure 39: Middle East and Africa Aerospace Bearing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East and Africa Aerospace Bearing Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa Aerospace Bearing Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace Bearing Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 2: Global Aerospace Bearing Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Global Aerospace Bearing Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Aerospace Bearing Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Aerospace Bearing Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 6: Global Aerospace Bearing Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: Global Aerospace Bearing Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Aerospace Bearing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Aerospace Bearing Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 12: Global Aerospace Bearing Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 13: Global Aerospace Bearing Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Aerospace Bearing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: Germany Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: United Kingdom Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Aerospace Bearing Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 20: Global Aerospace Bearing Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 21: Global Aerospace Bearing Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: Global Aerospace Bearing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 23: China Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Japan Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Australia Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace Bearing Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 29: Global Aerospace Bearing Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 30: Global Aerospace Bearing Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 31: Global Aerospace Bearing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Mexico Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Brazil Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Aerospace Bearing Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 35: Global Aerospace Bearing Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 36: Global Aerospace Bearing Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 37: Global Aerospace Bearing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 38: United Arab Emirates Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Saudi Arabia Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: South Africa Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East and Africa Aerospace Bearing Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Bearing Industry?

The projected CAGR is approximately 9.8%.

2. Which companies are prominent players in the Aerospace Bearing Industry?

Key companies in the market include August Steinmeyer GmbH, JTEKT, Beaver Aerospace and Defense Inc, GGB Bearings Technology, Kugel Aerospace and Defense, New Hamphshire Ball bearings, Kaman Speciality Bearings, National Precision Bearings, AST Bearings, UmbraGroup, Thomson Industries Inc, Aurora Bearings.

3. What are the main segments of the Aerospace Bearing Industry?

The market segments include Platform, Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 143.21 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Ball Bearings Segment is Expected to Witness Significant Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

October 2022: the expertise of Marsh brothers Aviation has added to the low-weight appeal of dark aero composite kit craft. Conceived as a self-build solution similar to the kit car concept, the DarkAero 1 features a range of composite materials, with Marsh Brothers Aviation providing the Wisconsin-based aviators with composite bearings for three different applications for the soon-to-launch aircraft kit.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace Bearing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace Bearing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace Bearing Industry?

To stay informed about further developments, trends, and reports in the Aerospace Bearing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence