Key Insights

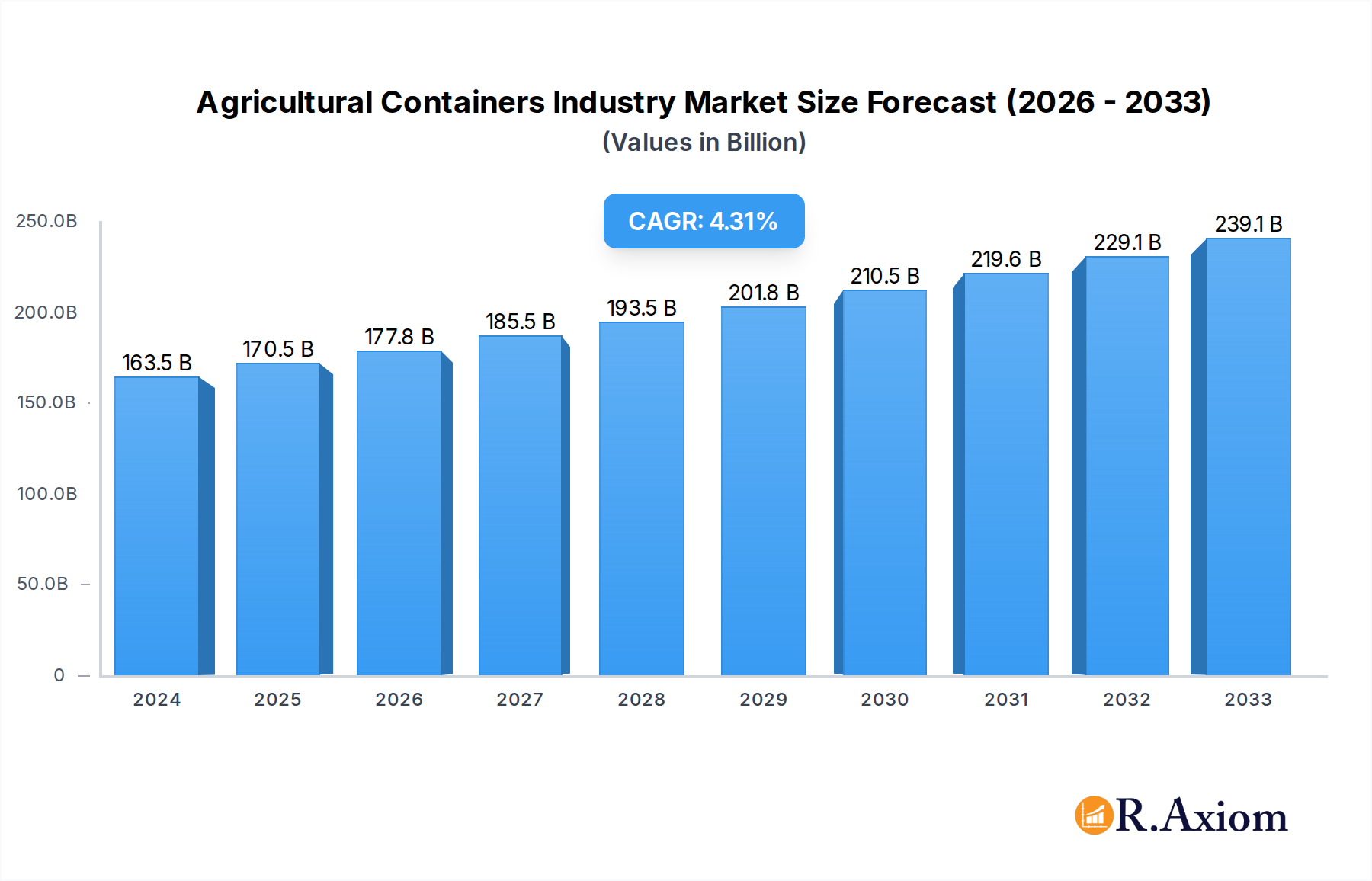

The global Agricultural Containers Market is poised for significant expansion, projected to reach a substantial USD 163.5 billion in 2024. This growth trajectory is underpinned by a robust CAGR of 4.5% anticipated throughout the forecast period of 2025-2033. The increasing global population, coupled with the imperative to enhance food production efficiency, serves as a primary catalyst for this market's development. Furthermore, the growing adoption of advanced farming techniques and the escalating demand for crop protection solutions are expected to drive the need for specialized and secure agricultural packaging. Innovations in material science, leading to the development of more sustainable and durable container options, will also play a crucial role in shaping market dynamics. The industry is witnessing a pronounced trend towards eco-friendly packaging solutions, driven by both regulatory pressures and consumer consciousness, encouraging manufacturers to invest in recyclable and biodegradable materials.

Agricultural Containers Industry Market Size (In Billion)

The market's expansion is further fueled by the diverse applications of agricultural containers, spanning pesticides, fertilizers, and seeds, among others. This broad utility ensures consistent demand across various agricultural segments. Key growth drivers include the rising emphasis on food safety and traceability, necessitating high-quality packaging that preserves product integrity. Conversely, challenges such as fluctuating raw material prices and the stringent regulatory landscape surrounding chemical packaging could pose moderate restraints. However, the ongoing technological advancements in container design, such as improved barrier properties and enhanced handling capabilities, alongside the strategic expansions and mergers of key market players like Amcor plc and Sonoco Products Company, are expected to mitigate these challenges and propel the market forward. The Asia Pacific region, in particular, is anticipated to emerge as a dominant force due to its vast agricultural landmass and increasing investments in modern farming practices.

Agricultural Containers Industry Company Market Share

Agricultural Containers Industry Market Concentration & Innovation

The agricultural containers industry, a critical component of global food production and distribution, exhibits a moderate level of market concentration. While several large, established players dominate significant portions of the market, the presence of regional and specialized manufacturers ensures a degree of competition. Innovation is a key driver, with a strong focus on developing sustainable packaging solutions, enhancing product protection, and improving logistical efficiency. Regulatory frameworks, particularly those concerning food safety, environmental impact, and the transportation of hazardous materials like pesticides, significantly influence product development and market entry. Product substitutes, such as alternative packaging materials or bulk transport methods, are continuously evaluated for cost-effectiveness and performance. End-user trends are shifting towards eco-friendly options, reduced plastic usage, and smart packaging technologies that provide real-time data on product condition. Mergers and acquisitions (M&A) activity, while not at peak levels, remains a strategic tool for consolidation and market expansion. For instance, the acquisition of Agri-Flex by Zeus for an estimated EUR 35 million (USD 36.88 million) signifies strategic investment in expanding global reach. The total M&A deal value in the sector is estimated to be in the billions, reflecting significant capital deployment. Market share for leading companies like Amcor plc and Sonoco Products Company is estimated to be in the double-digit percentage range, underscoring their substantial influence.

Agricultural Containers Industry Industry Trends & Insights

The agricultural containers industry is experiencing robust growth, propelled by a confluence of factors shaping the global agricultural landscape. The estimated Compound Annual Growth Rate (CAGR) for the forecast period 2025–2033 is projected to be between 5.5% and 6.5%, signifying sustained expansion. This upward trajectory is primarily driven by the increasing global population, which necessitates enhanced food production and, consequently, more sophisticated packaging solutions to preserve quality and reduce spoilage. The growing demand for efficient and safe transportation of agricultural produce, including fertilizers, pesticides, and seeds, further fuels market penetration. Technological advancements are playing a pivotal role, with innovations focusing on lightweight yet durable materials, improved barrier properties to extend shelf life, and the integration of smart technologies for traceability and inventory management. Consumer preferences are increasingly leaning towards sustainable and recyclable packaging, compelling manufacturers to invest in eco-friendly alternatives and circular economy initiatives. The competitive dynamics within the industry are characterized by strategic partnerships, product differentiation, and a focus on cost optimization. Key players are investing in research and development to create specialized containers tailored to specific crop types and farming practices. The global market penetration of advanced agricultural packaging solutions is on the rise, as farmers and distributors recognize the economic and environmental benefits. The transition towards more advanced packaging, like high-barrier films and reusable intermediate bulk containers (IBCs), is a significant trend. The overall market size for agricultural containers is projected to exceed USD 60 billion by 2025, with substantial growth anticipated through 2033.

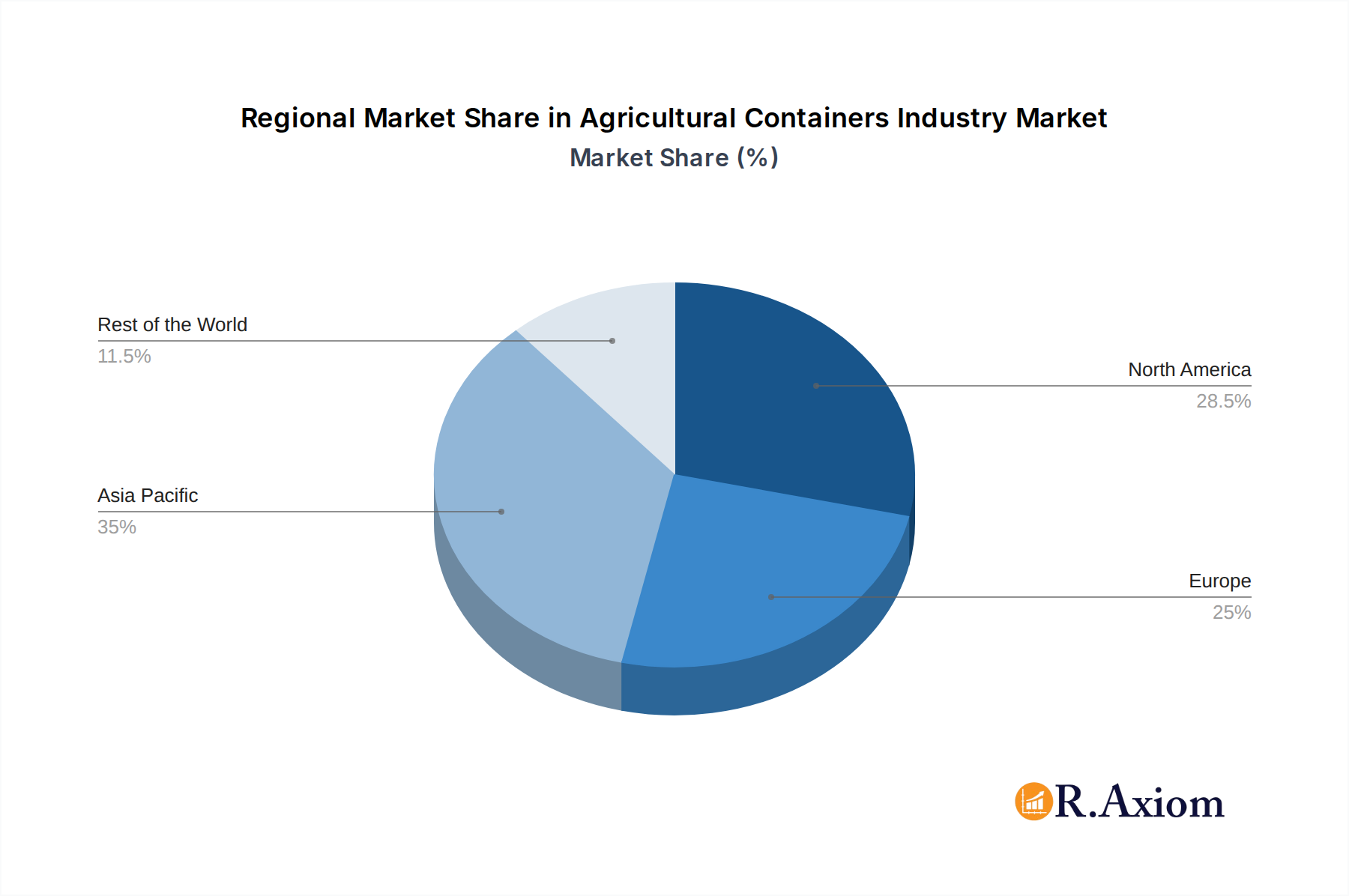

Dominant Markets & Segments in Agricultural Containers Industry

The agricultural containers industry is characterized by distinct regional dominance and segment leadership, driven by economic policies, infrastructure development, and agricultural output.

Dominant Regions and Countries

- North America and Europe currently represent the largest markets, owing to established agricultural sectors, advanced infrastructure, and strong regulatory frameworks that promote quality and safety.

- The Asia-Pacific region is emerging as a significant growth engine, driven by increasing agricultural output, a growing population, and rising demand for processed food, leading to a surge in the need for efficient packaging. Countries like China and India are key contributors to this growth.

- Latin America also presents substantial opportunities, fueled by its significant agricultural exports and expanding food processing industries.

Material Type Dominance

- Plastic containers, particularly high-density polyethylene (HDPE) and polyethylene (PE) variants used in bags, sacks, drums, and IBCs, hold the largest market share. Their durability, versatility, and cost-effectiveness make them indispensable across various applications. The market share for plastic containers is estimated to be over 40% of the total market.

- Paper and Paperboard containers, including sacks and boxes, are also significant, especially for dry goods like grains and animal feed, driven by their biodegradability and recyclability.

- Composite Materials are gaining traction due to their ability to offer enhanced barrier properties and structural integrity, often combining the benefits of plastic and paper.

Application Type Dominance

- Fertilizers and Pesticides represent the largest application segments due to their critical role in modern agriculture and the stringent packaging requirements for safety and containment. The market share for fertilizer and pesticide packaging is estimated to be around 30% and 25% respectively.

- Seeds packaging is another substantial segment, requiring specialized containers to maintain viability and protect against environmental factors.

- Other Types, including packaging for animal feed, soil amendments, and harvested produce, constitute a growing portion of the market.

Product Type Dominance

- Bags & Sacks (Plastic & Paper) are the most widely used product type, accounting for a significant portion of the market due to their cost-effectiveness and versatility for various agricultural inputs and outputs. This segment is estimated to hold approximately 35% of the market share.

- Bulk Containers (Drums & IBCs) are crucial for the transportation and storage of liquid and granular agricultural products, especially fertilizers and chemicals, experiencing strong demand. Their market share is estimated to be around 25%.

- Containers (Metal & Plastic), including smaller pails and tubs, cater to specific product needs.

- Pouches and Other Products (Boxes, Caps & Lids) are also important, particularly for specialized applications and smaller retail packaging.

Agricultural Containers Industry Product Developments

Product developments in the agricultural containers industry are significantly influenced by the pursuit of enhanced sustainability, improved product protection, and greater logistical efficiency. Innovations include the development of biodegradable and compostable plastic alternatives, such as PLA and PHA-based materials, to address environmental concerns. Advancements in multi-layer barrier films for bags and pouches are extending the shelf life of perishable agricultural products by minimizing oxygen and moisture ingress. The integration of smart packaging technologies, such as RFID tags and QR codes, offers improved traceability and inventory management throughout the supply chain. Furthermore, the design of lighter yet stronger composite containers and reusable Intermediate Bulk Containers (IBCs) is enhancing durability and reducing transportation costs. These developments aim to provide competitive advantages by meeting evolving regulatory standards and consumer demands for eco-friendly and high-performance packaging solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global agricultural containers market, segmented across key parameters to offer detailed insights. The segmentation includes:

- Material Type: Plastic, Metal, Paper and Paperboard, Composite Materials, and Other Materials. The plastic segment is projected to maintain its dominance with a market size exceeding USD 25 billion by 2025.

- Application Type: Pesticides, Fertilizers, Seeds, and Other Types. The fertilizer segment is expected to witness a CAGR of over 6% during the forecast period.

- Product Type: Bags & Sacks (Plastic & Paper), Bulk Containers (Drums & IBC), Pouches, Containers (Metal & Plastic), and Other Products (Boxes, Caps & Lids, etc.). Bags & Sacks are anticipated to retain the largest market share, with the bulk containers segment showing robust growth.

The analysis delves into the market size, growth projections, and competitive dynamics within each of these segments, offering a granular understanding of the industry's landscape through the study period 2019–2033.

Key Drivers of Agricultural Containers Industry Growth

The agricultural containers industry's growth is primarily propelled by several key factors:

- Growing Global Population: An increasing world population necessitates higher food production, driving demand for efficient packaging to preserve harvests and inputs.

- Technological Advancements: Innovations in material science and manufacturing processes are leading to more sustainable, durable, and specialized containers.

- Increasing Demand for Processed Foods: The rise of the processed food industry requires sophisticated packaging solutions for a wider variety of agricultural products.

- Stringent Food Safety and Environmental Regulations: These regulations mandate the use of high-quality, safe, and increasingly eco-friendly packaging materials.

- E-commerce Growth in Agriculture: The expansion of online agricultural product sales drives the need for robust and easily transportable packaging.

Challenges in the Agricultural Containers Industry Sector

Despite significant growth, the agricultural containers industry faces several challenges:

- Volatility in Raw Material Prices: Fluctuations in the cost of petroleum-based plastics and paper pulp can impact profitability and pricing strategies.

- Environmental Concerns and Regulatory Pressures: Increasing scrutiny over plastic waste and the demand for sustainable alternatives necessitate significant investment in research and development for eco-friendly solutions.

- Supply Chain Disruptions: Global events and logistical complexities can lead to delays in raw material procurement and product delivery.

- Intense Competition: The presence of numerous global and regional players leads to price pressures and the need for continuous innovation to maintain market share.

- Grape-like agricultural practices: Over-reliance on traditional, less sustainable materials and practices can hinder the adoption of advanced solutions.

Emerging Opportunities in Agricultural Containers Industry

The agricultural containers industry is ripe with emerging opportunities:

- Sustainable Packaging Solutions: The growing demand for biodegradable, compostable, and recyclable containers presents a significant avenue for growth and innovation.

- Smart Packaging Technologies: Integration of IoT sensors, QR codes, and RFID tags for enhanced traceability, temperature monitoring, and inventory management.

- Growth in Developing Economies: Expanding agricultural sectors in regions like Asia-Pacific and Latin America offer substantial untapped market potential.

- Specialized Packaging for Niche Crops: Development of tailored containers for high-value or sensitive agricultural products like organic produce and specialty seeds.

- Circular Economy Initiatives: Collaboration across the value chain to develop robust collection, recycling, and reuse programs for agricultural packaging.

Leading Players in the Agricultural Containers Industry Market

- Proampac LLC

- Sonoco Products Company

- Anderson Packaging Inc

- LC Packaging International BV

- Greif Inc

- Amcor plc

- NNZ Group

- Mondi Group

- Pactiv LLC

- BAG Corporation

- Flexpack FIBC

- Western Packagin

Key Developments in Agricultural Containers Industry Industry

- May 2022: Zeus, a global packaging solutions firm, acquired Canadian agricultural supplies company Agri-Flex as part of its EUR 35 million (USD 36.88 million) investment strategy, positioning Zeus as a top global distributor of agricultural crop packaging products.

- March 2022: StenCo LLC, specializing in environmentally friendly and biodegradable packaging, announced a collaboration with Cargill Inc., facilitated by Plug and Play Topeka. This partnership aims to develop a biodegradable oxygen-excluding barrier for several Cargill products.

Strategic Outlook for Agricultural Containers Industry Market

The strategic outlook for the agricultural containers industry remains highly positive, fueled by an increasing global demand for food and a strong push towards sustainable and technologically advanced packaging solutions. Key growth catalysts include the ongoing innovation in biodegradable and recyclable materials, the adoption of smart packaging for enhanced traceability and efficiency, and the expanding agricultural sectors in emerging economies. Companies that prioritize investment in research and development, focus on circular economy principles, and forge strategic partnerships will be well-positioned to capitalize on these opportunities. The market is poised for continued expansion, driven by the imperative to optimize food production, minimize waste, and meet evolving consumer and regulatory expectations through innovative and responsible packaging.

Agricultural Containers Industry Segmentation

-

1. Material Type

- 1.1. Plastic

- 1.2. Metal

- 1.3. Paper and Paperboard

- 1.4. Composite Materials

- 1.5. Other Materials

-

2. Application Type

- 2.1. Pesticides

- 2.2. Fertilizers

- 2.3. Seeds

- 2.4. Other Types

-

3. Product Type

- 3.1. Bags & Sacks (Plastic & Paper)

- 3.2. Bulk Containers (Drums & IBC)

- 3.3. Pouches

- 3.4. Containers (Metal & Plastic)

- 3.5. Other Products (Boxes, Caps & Lids, etc.)

Agricultural Containers Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. France

- 2.2. Germany

- 2.3. United Kingdom

- 2.4. The Netherlands

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Indonesia

- 3.4. Rest of Asia Pacific

- 4. Rest of the World

Agricultural Containers Industry Regional Market Share

Geographic Coverage of Agricultural Containers Industry

Agricultural Containers Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Plastic

- 5.1.2. Metal

- 5.1.3. Paper and Paperboard

- 5.1.4. Composite Materials

- 5.1.5. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. Pesticides

- 5.2.2. Fertilizers

- 5.2.3. Seeds

- 5.2.4. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Bags & Sacks (Plastic & Paper)

- 5.3.2. Bulk Containers (Drums & IBC)

- 5.3.3. Pouches

- 5.3.4. Containers (Metal & Plastic)

- 5.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Agricultural Containers Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Plastic

- 6.1.2. Metal

- 6.1.3. Paper and Paperboard

- 6.1.4. Composite Materials

- 6.1.5. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. Pesticides

- 6.2.2. Fertilizers

- 6.2.3. Seeds

- 6.2.4. Other Types

- 6.3. Market Analysis, Insights and Forecast - by Product Type

- 6.3.1. Bags & Sacks (Plastic & Paper)

- 6.3.2. Bulk Containers (Drums & IBC)

- 6.3.3. Pouches

- 6.3.4. Containers (Metal & Plastic)

- 6.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Plastic

- 7.1.2. Metal

- 7.1.3. Paper and Paperboard

- 7.1.4. Composite Materials

- 7.1.5. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Application Type

- 7.2.1. Pesticides

- 7.2.2. Fertilizers

- 7.2.3. Seeds

- 7.2.4. Other Types

- 7.3. Market Analysis, Insights and Forecast - by Product Type

- 7.3.1. Bags & Sacks (Plastic & Paper)

- 7.3.2. Bulk Containers (Drums & IBC)

- 7.3.3. Pouches

- 7.3.4. Containers (Metal & Plastic)

- 7.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Europe Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Plastic

- 8.1.2. Metal

- 8.1.3. Paper and Paperboard

- 8.1.4. Composite Materials

- 8.1.5. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Application Type

- 8.2.1. Pesticides

- 8.2.2. Fertilizers

- 8.2.3. Seeds

- 8.2.4. Other Types

- 8.3. Market Analysis, Insights and Forecast - by Product Type

- 8.3.1. Bags & Sacks (Plastic & Paper)

- 8.3.2. Bulk Containers (Drums & IBC)

- 8.3.3. Pouches

- 8.3.4. Containers (Metal & Plastic)

- 8.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Asia Pacific Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Plastic

- 9.1.2. Metal

- 9.1.3. Paper and Paperboard

- 9.1.4. Composite Materials

- 9.1.5. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Application Type

- 9.2.1. Pesticides

- 9.2.2. Fertilizers

- 9.2.3. Seeds

- 9.2.4. Other Types

- 9.3. Market Analysis, Insights and Forecast - by Product Type

- 9.3.1. Bags & Sacks (Plastic & Paper)

- 9.3.2. Bulk Containers (Drums & IBC)

- 9.3.3. Pouches

- 9.3.4. Containers (Metal & Plastic)

- 9.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Rest of the World Agricultural Containers Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Plastic

- 10.1.2. Metal

- 10.1.3. Paper and Paperboard

- 10.1.4. Composite Materials

- 10.1.5. Other Materials

- 10.2. Market Analysis, Insights and Forecast - by Application Type

- 10.2.1. Pesticides

- 10.2.2. Fertilizers

- 10.2.3. Seeds

- 10.2.4. Other Types

- 10.3. Market Analysis, Insights and Forecast - by Product Type

- 10.3.1. Bags & Sacks (Plastic & Paper)

- 10.3.2. Bulk Containers (Drums & IBC)

- 10.3.3. Pouches

- 10.3.4. Containers (Metal & Plastic)

- 10.3.5. Other Products (Boxes, Caps & Lids, etc.)

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Proampac LLC

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Sonoco Products Company

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Anderson Packaging Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 LC Packaging International BV

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Greif Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Amcor plc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 NNZ Group

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Mondi Group

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Pactiv LLC

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 BAG Corporation

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Flexpack FIBC

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Western Packagin

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 Proampac LLC

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Agricultural Containers Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 3: North America Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 5: North America Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 6: North America Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 7: North America Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: North America Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 11: Europe Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 12: Europe Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 13: Europe Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 14: Europe Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Europe Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Europe Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 19: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 20: Asia Pacific Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 21: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 22: Asia Pacific Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 23: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 24: Asia Pacific Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Agricultural Containers Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 27: Rest of the World Agricultural Containers Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Rest of the World Agricultural Containers Industry Revenue (billion), by Application Type 2025 & 2033

- Figure 29: Rest of the World Agricultural Containers Industry Revenue Share (%), by Application Type 2025 & 2033

- Figure 30: Rest of the World Agricultural Containers Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 31: Rest of the World Agricultural Containers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 32: Rest of the World Agricultural Containers Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World Agricultural Containers Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 3: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 4: Global Agricultural Containers Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 7: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 12: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 13: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: France Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: The Netherlands Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Rest of Europe Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 21: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 22: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: China Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: India Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Indonesia Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Agricultural Containers Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Agricultural Containers Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 29: Global Agricultural Containers Industry Revenue billion Forecast, by Application Type 2020 & 2033

- Table 30: Global Agricultural Containers Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 31: Global Agricultural Containers Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Agricultural Containers Industry?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Agricultural Containers Industry?

Key companies in the market include Proampac LLC, Sonoco Products Company, Anderson Packaging Inc, LC Packaging International BV, Greif Inc, Amcor plc, NNZ Group, Mondi Group, Pactiv LLC, BAG Corporation, Flexpack FIBC, Western Packagin.

3. What are the main segments of the Agricultural Containers Industry?

The market segments include Material Type, Application Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 163.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from the Agro-chemical Segment; Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging.

6. What are the notable trends driving market growth?

Plastic Packaging to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

; High Inventory Costs and Premium Pricing.

8. Can you provide examples of recent developments in the market?

May 2022 - Zeus, a global packaging solutions firm with Irish ownership, announced the acquisition of Canadian agricultural supplies company Agri-Flex. This acquisition represents the next stage of the company's EUR 35 million (nearly USD 36.88 million) investment strategy. It positions Zeus as one of the top distributors of agricultural crop packaging products worldwide.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Agricultural Containers Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Agricultural Containers Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Agricultural Containers Industry?

To stay informed about further developments, trends, and reports in the Agricultural Containers Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence