Key Insights

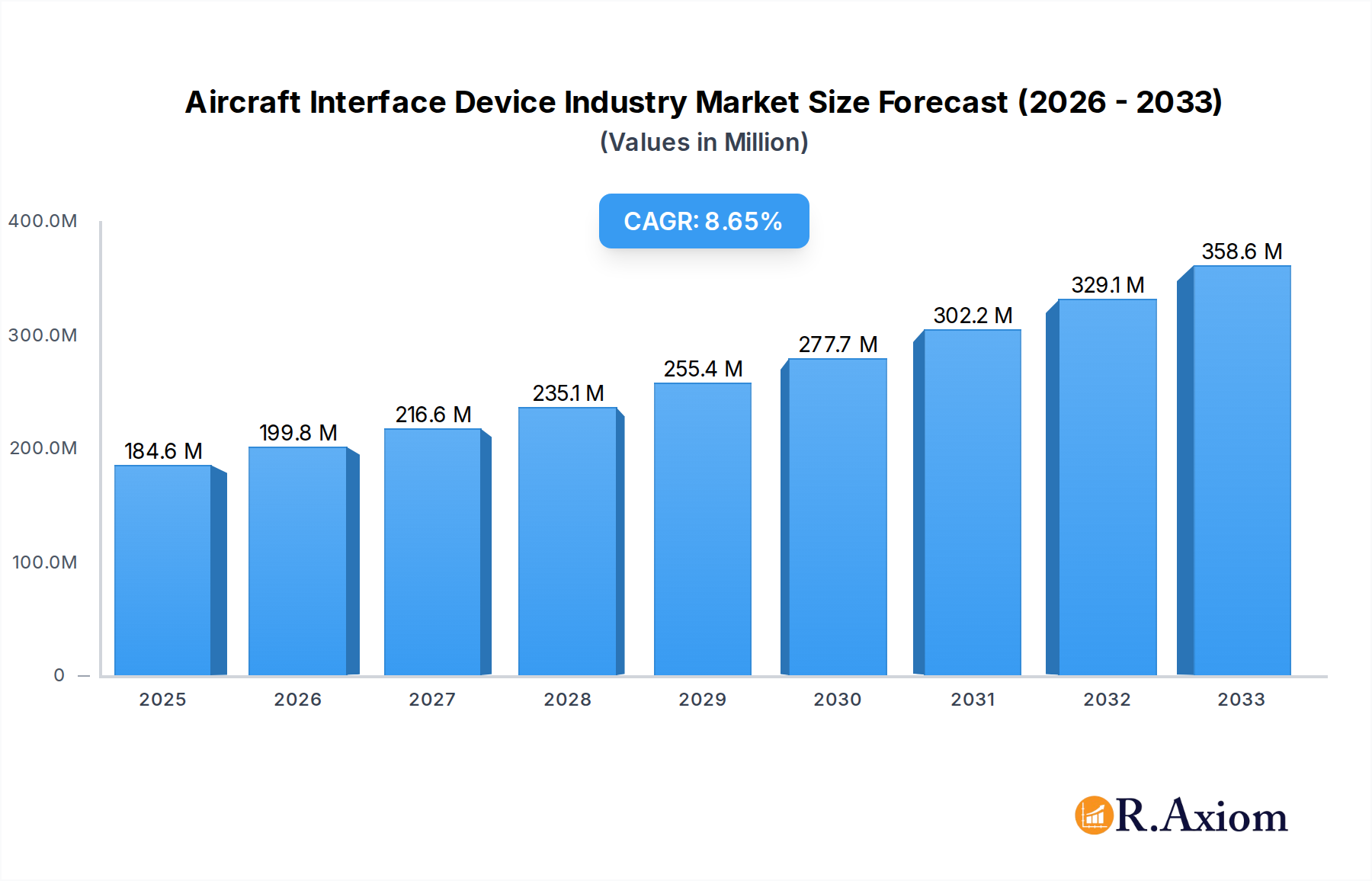

The global Aircraft Interface Device (AID) market is poised for substantial expansion, projected to reach $184.60 million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 8.38% through 2033. This robust growth is fueled by a confluence of factors including the increasing demand for advanced avionics systems, the growing complexity of aircraft operations, and the imperative for enhanced data connectivity and management. The military segment is a significant contributor, driven by the need for sophisticated communication, navigation, and surveillance capabilities in modern defense platforms. General aviation is also witnessing a surge in demand for AIDs as manufacturers integrate more sophisticated electronic systems to improve safety and operational efficiency. The commercial aviation sector, characterized by its large fleet size and continuous technological upgrades, represents another key driver, with airlines investing in AIDs to optimize flight operations, improve passenger experience through enhanced connectivity, and meet stringent regulatory requirements for data logging and transmission.

Aircraft Interface Device Industry Market Size (In Million)

Several key trends are shaping the AID market. The miniaturization of components and the development of lighter, more powerful interface devices are enabling greater integration within aircraft systems. Furthermore, the increasing adoption of advanced networking technologies, such as Ethernet and Wi-Fi, within cockpits and cabin environments is creating new opportunities for AID manufacturers. The focus on cybersecurity for flight data is also paramount, leading to the development of more secure and resilient AID solutions. While the market benefits from strong demand, some restraints exist, including the high cost of research and development for cutting-edge technologies and the lengthy certification processes for aerospace components. However, the continuous innovation by leading companies like Astronics Corporation, Honeywell International Inc., THALES, and Collins Aerospace (RTX Corporation), coupled with the strategic expansion into emerging markets within the Asia Pacific and Middle East regions, is expected to overcome these challenges and drive sustained market growth.

Aircraft Interface Device Industry Company Market Share

Here is an SEO-optimized, detailed report description for the Aircraft Interface Device Industry:

Aircraft Interface Device Industry Market Concentration & Innovation

The Aircraft Interface Device (AID) industry exhibits a moderate to high market concentration, with key players like Collins Aerospace (RTX Corporation), Honeywell International Inc, and THALES dominating significant market shares, estimated to be upwards of 60% collectively. Innovation is a critical driver, fueled by the relentless demand for enhanced aircraft connectivity, data analytics, and operational efficiency. Regulatory frameworks, including those set by the FAA and EASA, play a crucial role in shaping product development and adoption, often necessitating stringent safety and data security standards. Product substitutes are limited, primarily revolving around legacy data logging systems, but the increasing sophistication of AIDs renders them increasingly less competitive. End-user trends highlight a strong preference for solutions that offer real-time data transmission, predictive maintenance capabilities, and seamless integration with existing airline IT infrastructure. Mergers and acquisitions (M&A) are moderately active, with strategic acquisitions by larger players aimed at consolidating market presence and acquiring specialized technological capabilities. M&A deal values in this sector are projected to reach several hundred million dollars annually, driven by the strategic importance of data-driven aviation solutions.

Aircraft Interface Device Industry Industry Trends & Insights

The global Aircraft Interface Device (AID) industry is poised for robust growth, driven by an increasing demand for advanced data acquisition, transmission, and analysis capabilities across commercial, military, and general aviation sectors. The market is experiencing a Compound Annual Growth Rate (CAGR) of approximately 7-9% during the forecast period of 2025–2033. This growth is underpinned by several key trends. Firstly, the escalating need for real-time aircraft performance monitoring and predictive maintenance is a significant catalyst. Airlines are increasingly investing in AID solutions that can collect vast amounts of data, enabling them to identify potential issues before they lead to costly disruptions or safety concerns. This trend is particularly pronounced in the commercial aviation segment, where operational efficiency and passenger safety are paramount. Secondly, the evolution of the "connected aircraft" concept is a major technological disruption. AIDs are central to this evolution, acting as the crucial link between aircraft systems and ground-based networks. The ability to transmit flight data, maintenance logs, and operational parameters wirelessly and in real-time empowers airlines with unprecedented operational insights and agility. This facilitates proactive service scheduling, optimized flight planning, and enhanced passenger experience.

Furthermore, evolving consumer preferences for seamless and efficient air travel are indirectly influencing AID adoption. Airlines that leverage data effectively to improve aircraft availability and reduce delays gain a competitive edge. The competitive landscape is characterized by a blend of established aerospace giants and specialized technology providers. Companies are investing heavily in research and development to offer advanced features such as AI-powered analytics, cybersecurity enhancements, and lightweight, power-efficient hardware. Market penetration is deepening across all aviation segments, with new aircraft models increasingly featuring integrated AID systems as standard. The military sector is also a significant contributor, demanding robust and secure AID solutions for mission-critical data collection and operational awareness. The general aviation sector, while smaller in market size, represents a growing segment with an increasing adoption of sophisticated AID technologies for flight tracking, performance monitoring, and safety enhancement. The market penetration for advanced AID systems is projected to exceed 70% within the commercial aviation segment by 2030.

Dominant Markets & Segments in Aircraft Interface Device Industry

The Aircraft Interface Device (AID) industry's dominance is multifaceted, with the Commercial Aviation segment standing out as the largest and most influential market. This segment is driven by several key factors:

- Economic Policies: Global economic growth and increased travel demand directly translate into higher aircraft utilization and a subsequent need for advanced AID systems to optimize operations and reduce costs. Favorable trade agreements and government initiatives supporting the aviation sector further bolster this segment.

- Infrastructure Development: The continuous expansion of airline fleets, both for new aircraft orders and fleet upgrades, necessitates the integration of modern AID technologies. Investment in new airports and air traffic control modernization also indirectly supports the demand for data-driven aviation solutions.

- Technological Adoption Rate: Commercial airlines are typically early adopters of new technologies that promise significant return on investment through operational efficiency, fuel savings, and enhanced safety. The pressure to remain competitive in a global market compels airlines to leverage data analytics powered by sophisticated AIDs.

Within the commercial aviation segment, the demand for AIDs is particularly high for long-haul fleets operating on extensive international routes. These aircraft generate substantial data volumes, making advanced AID capabilities for real-time monitoring and analysis indispensable. The focus here is on maximizing aircraft availability, minimizing downtime, and optimizing fuel consumption. For example, the integration of AIDs with predictive maintenance platforms allows airlines to schedule maintenance proactively, preventing costly in-flight failures and schedule disruptions, thereby ensuring higher aircraft utilization rates.

The Military Aviation segment, while smaller in terms of the sheer number of aircraft compared to commercial aviation, represents a critical and high-value market. This segment is characterized by:

- Stringent Security and Reliability Requirements: Military operations demand highly robust and secure AID systems capable of withstanding extreme conditions and protecting sensitive data. The emphasis is on mission success, operational readiness, and intelligence gathering.

- Advanced Mission Data Collection: AIDs in military applications are crucial for collecting data related to mission performance, system diagnostics, and environmental factors, which are vital for post-mission analysis, training, and future platform development.

- Long Lifespan and Lifecycle Support: Military aircraft often have very long operational lifespans, leading to sustained demand for AID systems and ongoing support and upgrades throughout their service life.

The General Aviation segment, encompassing private jets, turboprops, and smaller aircraft, is a growing market for AID technologies. Key drivers include:

- Increasing Safety Consciousness: Owners and operators are increasingly recognizing the safety benefits offered by AIDs, such as flight data recording and real-time tracking.

- Emerging Affordability: As AID technology matures, more cost-effective solutions are becoming available for the general aviation market, making them more accessible to a broader range of users.

- Value-Added Services: Demand for services like flight tracking, performance optimization, and remote diagnostics is growing among general aviation users.

Overall, the commercial segment holds the largest market share due to the sheer volume of aircraft and the continuous drive for operational efficiency. However, the military segment represents a crucial market due to its high-value contracts and specialized requirements, while general aviation presents a significant growth opportunity as technology becomes more accessible.

Aircraft Interface Device Industry Product Developments

The Aircraft Interface Device (AID) industry is witnessing rapid product innovations focused on enhanced connectivity, advanced data processing, and improved cybersecurity. Companies are developing next-generation AIDs that offer higher bandwidth for real-time data streaming, enabling sophisticated applications like predictive maintenance and in-flight diagnostics. Integration with cloud-based platforms is a key trend, allowing for seamless data access and analysis by airlines and maintenance crews. Furthermore, miniaturization and power efficiency are critical design considerations for new AIDs, reducing installation complexity and aircraft weight. The competitive advantage lies in offering robust, secure, and scalable solutions that can adapt to evolving aviation needs and integrate with a wide array of aircraft systems.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Aircraft Interface Device (AID) industry. The market is segmented based on application, with a detailed examination of the following categories:

- Commercial Aviation: This segment focuses on AIDs used in airliners operated by passenger and cargo carriers. It includes analysis of market size, projected growth rates, and key competitive dynamics driven by operational efficiency and passenger safety. The market for commercial aviation AIDs is estimated to be approximately $4,000 Million in 2025, with a projected CAGR of 8.5%.

- Military Aviation: This segment covers AIDs deployed on military aircraft for defense and security operations. It assesses growth drivers related to advanced data collection and stringent security requirements. The military aviation AID market is projected to reach $1,500 Million by 2025, with a CAGR of 6.2%.

- General Aviation: This segment includes AIDs for private jets, helicopters, and other non-commercial aircraft. It highlights the growing adoption of these devices for safety and performance monitoring. The general aviation AID market is estimated at $500 Million in 2025, with a projected CAGR of 7.8%.

Key Drivers of Aircraft Interface Device Industry Growth

Several key factors are propelling the growth of the Aircraft Interface Device (AID) industry. The escalating demand for enhanced operational efficiency and fuel management in commercial aviation is a primary driver, as AIDs facilitate the collection of crucial flight data for optimization. The increasing emphasis on proactive and predictive maintenance by airlines, aiming to reduce downtime and operational costs, is another significant growth catalyst. Furthermore, the advancement of connectivity technologies, such as 5G and satellite communications, enables real-time data transmission, unlocking new possibilities for aircraft monitoring and management. Stringent aviation safety regulations worldwide also mandate the use of sophisticated data recording devices, indirectly driving AID market expansion. Lastly, the growing adoption of the "connected aircraft" concept, transforming aviation through data-driven insights, is fundamentally reshaping the demand for advanced AID solutions.

Challenges in the Aircraft Interface Device Industry Sector

Despite robust growth, the Aircraft Interface Device (AID) industry faces several challenges. High initial investment costs for advanced AID systems can be a barrier, particularly for smaller operators and in the general aviation segment. Complex integration with legacy aircraft systems presents technical hurdles and can increase installation time and costs. Evolving cybersecurity threats necessitate continuous investment in robust security features to protect sensitive flight data, adding to development and maintenance expenses. Furthermore, the long certification processes for aviation hardware can slow down the market entry of new products. Global supply chain disruptions, as experienced in recent years, can also impact the availability of critical components and lead to increased lead times.

Emerging Opportunities in Aircraft Interface Device Industry

The Aircraft Interface Device (AID) industry is ripe with emerging opportunities. The expansion of AI and machine learning capabilities for analyzing vast amounts of flight data presents a significant opportunity for developing more sophisticated predictive maintenance and operational optimization tools. The growing trend towards sustainable aviation is creating demand for AIDs that can monitor and optimize fuel efficiency more effectively, supporting eco-friendly flight operations. The increasing development of urban air mobility (UAM) and eVTOL aircraft will require new generations of specialized AIDs, offering a nascent but high-growth market. Furthermore, enhanced in-flight connectivity services are creating opportunities for AIDs that can seamlessly manage and transmit data for passenger entertainment and business applications. The increasing focus on fleet-wide data management platforms by airlines presents opportunities for AID providers to offer integrated solutions.

Leading Players in the Aircraft Interface Device Industry Market

- Astronics Corporation

- Honeywell International Inc

- THALES

- Collins Aerospace (RTX Corporation)

- Elbit Systems Ltd

- SCI Technology Inc

- Teledyne Technologies Incorporated

- Anuvu

- SKYTRAC Systems Ltd

- ViaSat Inc

- Avionics Interface Technologies

Key Developments in Aircraft Interface Device Industry Industry

- August 2023: FLYHT Aerospace Solutions LLC announced a five-year contract extension with a long-term aircraft lease customer for ongoing software services across their entire Boeing B777 and B767 fleets, highlighting the importance of continued software support for AID-related functionalities.

- May 2023: RTX Corporation announced the successful installation of Collins Aerospace's InteliSight aircraft interface device on over 200 JetBlue Airways Airbus A320 aircraft. This development underscores the trend towards secure, real-time data collection and transmission to cloud platforms like Collins' Global Connect, enabling airlines to optimize service schedules and improve aircraft durability.

Strategic Outlook for Aircraft Interface Device Industry Market

The strategic outlook for the Aircraft Interface Device (AID) industry remains exceptionally positive, driven by the fundamental shift towards data-centric aviation. Continued innovation in AI and machine learning will unlock deeper insights from flight data, further enhancing predictive maintenance and operational efficiency, projected to grow by xx%. The increasing emphasis on sustainability will fuel demand for AIDs that optimize fuel consumption and reduce emissions. The nascent but rapidly growing urban air mobility sector presents a significant new market for specialized AID solutions. As airlines and MRO (Maintenance, Repair, and Overhaul) providers continue to invest in digital transformation, the demand for integrated, secure, and real-time data solutions powered by advanced AIDs will only intensify, creating sustained growth opportunities estimated at over $10,000 Million by 2033.

Aircraft Interface Device Industry Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Military

- 1.3. General Aviation

Aircraft Interface Device Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Egypt

- 5.4. Qatar

- 5.5. Rest of Middle East and Africa

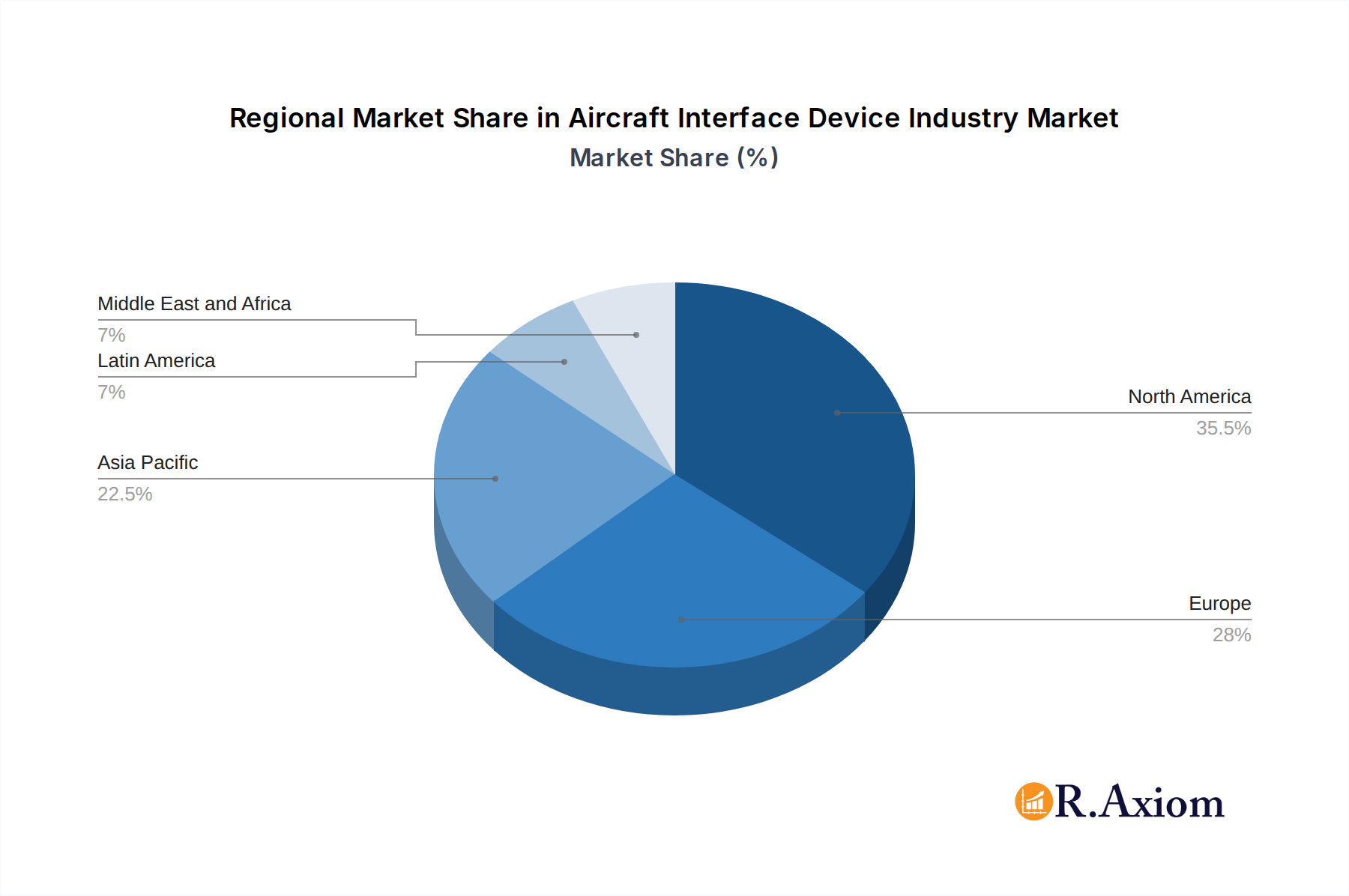

Aircraft Interface Device Industry Regional Market Share

Geographic Coverage of Aircraft Interface Device Industry

Aircraft Interface Device Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Military

- 5.1.3. General Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Aircraft Interface Device Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Military

- 6.1.3. General Aviation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Aircraft Interface Device Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Military

- 7.1.3. General Aviation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Aircraft Interface Device Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Military

- 8.1.3. General Aviation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia Pacific Aircraft Interface Device Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Military

- 9.1.3. General Aviation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Latin America Aircraft Interface Device Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Military

- 10.1.3. General Aviation

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Middle East and Africa Aircraft Interface Device Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Commercial

- 11.1.2. Military

- 11.1.3. General Aviation

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Astronics Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Honeywell International Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 THALES

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Collins Aerospace (RTX Corporation)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Elbit Systems Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SCI Technology Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Teledyne Technologies Incorporated

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Anuvu

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SKYTRAC Systems Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ViaSat Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Avionics Interface Technologies

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Astronics Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aircraft Interface Device Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Aircraft Interface Device Industry Revenue (Million), by Application 2025 & 2033

- Figure 3: North America Aircraft Interface Device Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aircraft Interface Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Aircraft Interface Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Aircraft Interface Device Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: Europe Aircraft Interface Device Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Europe Aircraft Interface Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Aircraft Interface Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Aircraft Interface Device Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: Asia Pacific Aircraft Interface Device Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Asia Pacific Aircraft Interface Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Aircraft Interface Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Aircraft Interface Device Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Latin America Aircraft Interface Device Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Latin America Aircraft Interface Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Latin America Aircraft Interface Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Aircraft Interface Device Industry Revenue (Million), by Application 2025 & 2033

- Figure 19: Middle East and Africa Aircraft Interface Device Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Middle East and Africa Aircraft Interface Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Middle East and Africa Aircraft Interface Device Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aircraft Interface Device Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global Aircraft Interface Device Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Aircraft Interface Device Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Aircraft Interface Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Global Aircraft Interface Device Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Aircraft Interface Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Germany Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: France Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Italy Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Europe Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Aircraft Interface Device Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 15: Global Aircraft Interface Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: China Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Japan Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: India Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: South Korea Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Asia Pacific Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Aircraft Interface Device Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Global Aircraft Interface Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: Brazil Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Mexico Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Latin America Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Aircraft Interface Device Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 27: Global Aircraft Interface Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: United Arab Emirates Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Saudi Arabia Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Egypt Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Qatar Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Rest of Middle East and Africa Aircraft Interface Device Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aircraft Interface Device Industry?

The projected CAGR is approximately 8.38%.

2. Which companies are prominent players in the Aircraft Interface Device Industry?

Key companies in the market include Astronics Corporation, Honeywell International Inc, THALES, Collins Aerospace (RTX Corporation), Elbit Systems Ltd, SCI Technology Inc, Teledyne Technologies Incorporated, Anuvu, SKYTRAC Systems Ltd, ViaSat Inc, Avionics Interface Technologies.

3. What are the main segments of the Aircraft Interface Device Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 184.60 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Commercial Aircraft Segment to have the Largest Market Share During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

August 2023: FLYHT Aerospace Solutions LLC announced that it had signed a five-year contract extension with one of its long-term aircraft lease customers to provide ongoing software services for its entire Boeing B777 and B767 fleets

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aircraft Interface Device Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aircraft Interface Device Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aircraft Interface Device Industry?

To stay informed about further developments, trends, and reports in the Aircraft Interface Device Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence