Key Insights

The global Anti-Submarine Warfare (ASW) market is poised for significant expansion, projected to reach USD 17.98 million with a compelling Compound Annual Growth Rate (CAGR) of 5.02% during the forecast period of 2025-2033. This robust growth is fueled by a confluence of escalating geopolitical tensions, the increasing stealth capabilities of modern submarines, and a heightened emphasis on maritime security by nations worldwide. Navies are investing heavily in advanced ASW systems and platforms to counter potential threats from an evolving submarine force. Key drivers include the modernization of naval fleets, the development of sophisticated sensor technologies for improved detection, and the integration of artificial intelligence and machine learning for faster threat assessment and response. The demand for enhanced electronic warfare capabilities and advanced armament systems designed to neutralize underwater threats further underpins this market's upward trajectory.

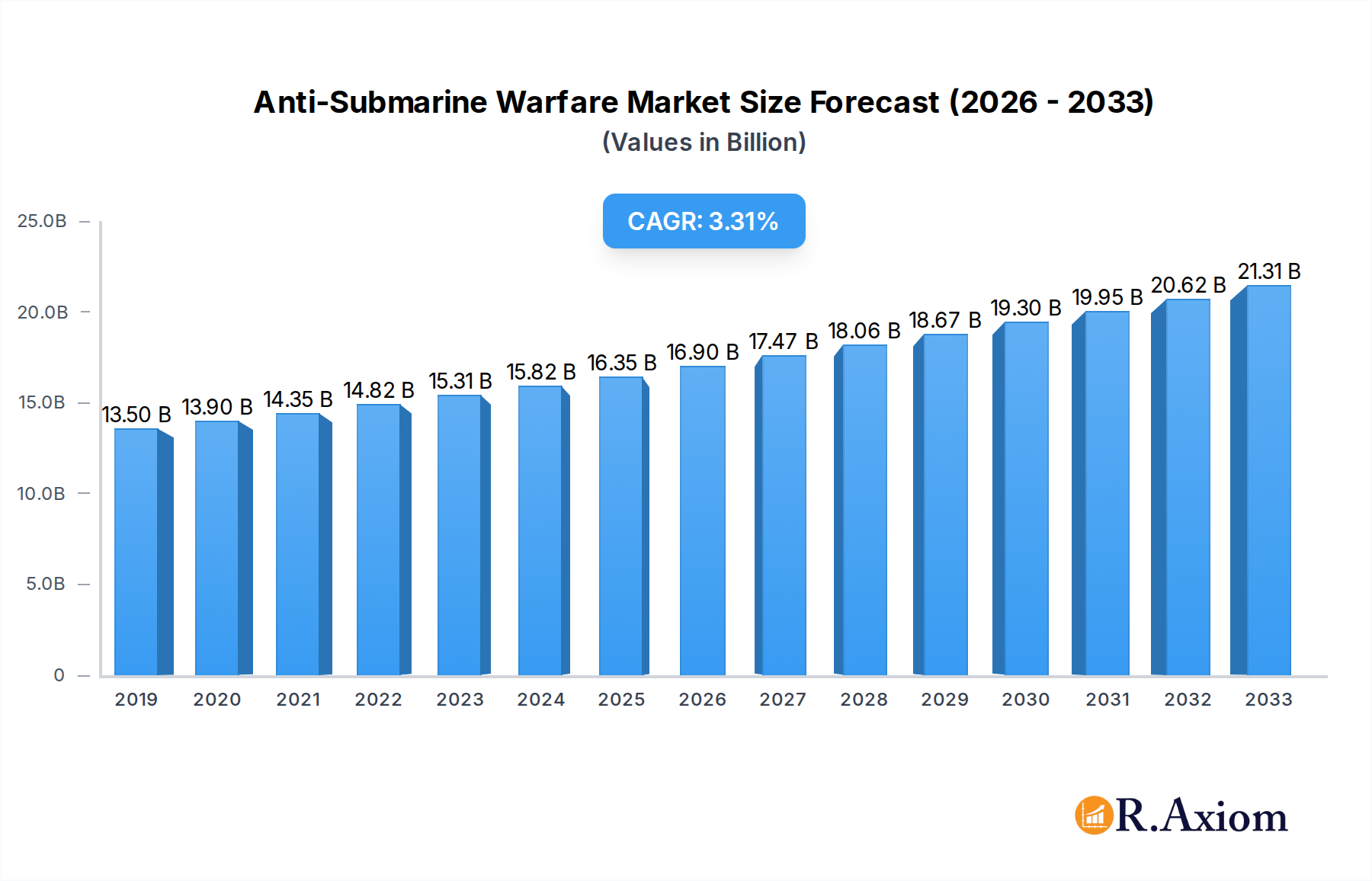

Anti-Submarine Warfare Market Market Size (In Billion)

The ASW market is characterized by a dynamic landscape with continuous innovation in both system components and platform integration. The "Sensors" segment is expected to witness substantial growth, driven by advancements in sonar technology, acoustic processing, and non-acoustic detection methods. Electronic Support Measures (ESM) are also crucial for identifying and tracking submarines through their electromagnetic emissions. On the platform front, submarines themselves are becoming increasingly integral to ASW operations, alongside traditional assets like surface ships, helicopters, and maritime patrol aircraft. The burgeoning role of Unmanned Systems (UxS), including Unmanned Underwater Vehicles (UUVs) and Unmanned Surface Vehicles (USVs), is a transformative trend, offering persistent surveillance and operational flexibility in a cost-effective manner. Despite the promising outlook, the market faces certain restraints, including the high cost of developing and deploying advanced ASW technologies, and the complexity of achieving full interoperability across diverse naval platforms and international collaborations. Nevertheless, the strategic imperative of maintaining undersea dominance ensures sustained investment and innovation within the ASW sector.

Anti-Submarine Warfare Market Company Market Share

This in-depth market research report provides an exhaustive analysis of the global Anti-Submarine Warfare (ASW) market, spanning from 2019 to 2033, with a detailed focus on the Base Year 2025 and a comprehensive Forecast Period of 2025–2033. Delving into historical trends from 2019–2024, this report is an indispensable resource for defense contractors, naval strategists, technology providers, and government agencies seeking to understand the evolving landscape of ASW capabilities. Our analysis covers critical segments including Sensors, Electronic Support Measures, and Armament, across Platforms like Submarines, Surface Ships, Helicopters, Maritime Patrol Aircraft, and Unmanned Systems. With an estimated market size poised for significant growth, this report illuminates key market concentration, innovation drivers, industry trends, dominant markets, product developments, growth drivers, challenges, emerging opportunities, leading players, and crucial industry developments.

Anti-Submarine Warfare Market Market Concentration & Innovation

The Anti-Submarine Warfare (ASW) market exhibits a moderate to high level of concentration, characterized by the presence of established defense giants alongside specialized technology providers. Key players like Lockheed Martin Corporation, Northrop Grumman Corporation, and BAE Systems plc command significant market share, driven by extensive R&D investments and long-standing government contracts. Innovation within the ASW market is primarily fueled by the escalating threat posed by increasingly stealthy and capable submarines, necessitating the development of advanced detection, tracking, and neutralization technologies. This includes advancements in sonar systems, artificial intelligence for signal processing, and the integration of unmanned systems for persistent surveillance. Regulatory frameworks, particularly those governing defense procurement and international arms sales, play a crucial role in shaping market dynamics. Product substitutes, such as enhanced electronic warfare capabilities or increased reliance on intelligence gathering, are present but do not fully negate the need for dedicated ASW platforms and systems. End-user trends are heavily influenced by geopolitical tensions and the need for robust maritime domain awareness, pushing for greater interoperability and network-centric warfare capabilities. Mergers and Acquisitions (M&A) activities are strategic in nature, aimed at consolidating capabilities, acquiring new technologies, or expanding market reach. For instance, strategic acquisitions of smaller technology firms specializing in AI-driven analytics or advanced sensor development are becoming more prevalent. The overall M&A deal value is projected to reach hundreds of millions, reflecting the strategic importance of ASW technologies.

Anti-Submarine Warfare Market Industry Trends & Insights

The global Anti-Submarine Warfare (ASW) market is experiencing robust growth, driven by a confluence of escalating geopolitical tensions, the modernization of naval fleets worldwide, and rapid advancements in technological capabilities. The increasing assertiveness of certain nations in maritime territories and the development of more sophisticated and stealthy submarine technologies by potential adversaries are primary catalysts for increased investment in ASW systems. This heightened threat perception necessitates the continuous enhancement of naval forces' ability to detect, track, and neutralize submarines, both conventional and nuclear-powered. The market penetration of advanced ASW solutions is steadily increasing as navies across the globe prioritize acquiring state-of-the-art equipment to maintain their operational edge.

Technological disruptions are a defining feature of the ASW market. Innovations in artificial intelligence (AI) and machine learning (ML) are revolutionizing acoustic signal processing, enabling more accurate detection and classification of submarines in complex acoustic environments. The development of persistent, multi-domain surveillance platforms, including advanced maritime patrol aircraft (MPAs), unmanned aerial vehicles (UAVs), and unmanned underwater vehicles (UUVs), is expanding the reach and effectiveness of ASW operations. Furthermore, the integration of sophisticated sensor networks, encompassing passive and active sonar arrays, magnetic anomaly detectors (MAD), and electronic support measures (ESM), is creating a more comprehensive and layered ASW defense capability.

Consumer preferences, dictated by military end-users, are shifting towards integrated, network-centric solutions that offer enhanced situational awareness and interoperability across different platforms and systems. There is a growing demand for modular and adaptable ASW systems that can be readily integrated into existing naval architectures and upgraded to meet future threats. The emphasis is on reducing the human-in-the-loop for initial detection and classification, thereby increasing response times and reducing operator workload.

Competitive dynamics within the ASW market are intense, with a mix of large, established defense conglomerates and agile, niche technology providers vying for market share. Companies are investing heavily in research and development to maintain a technological advantage, often forming strategic partnerships and alliances to leverage specialized expertise. The market is characterized by long procurement cycles and significant upfront investment requirements, favoring companies with strong relationships with defense ministries and a proven track record of delivering complex military systems. The compound annual growth rate (CAGR) for the ASW market is projected to be robust, estimated to be between 5.5% and 7.0% over the forecast period, reflecting the sustained demand for advanced ASW capabilities. The market is estimated to reach a valuation of over $25,000 million by 2030.

Dominant Markets & Segments in Anti-Submarine Warfare Market

The global Anti-Submarine Warfare (ASW) market's dominance is sculpted by a complex interplay of geopolitical imperatives, technological advancements, and strategic naval investments. Geographically, North America and Europe currently represent the most dominant markets, driven by robust defense budgets, the presence of major naval powers like the United States and key European nations, and ongoing modernization programs for their submarine and surface fleets. The Asia-Pacific region is emerging as a significant growth engine, fueled by increasing naval power projection, territorial disputes, and substantial investments in naval modernization by countries such as China, Japan, and India. Economic policies in these regions, such as sustained defense spending and strategic trade agreements, directly contribute to the demand for advanced ASW solutions.

Within the System segmentation, Sensors hold a commanding position. This is primarily due to the foundational role of sonar technology (both passive and active) in detecting and tracking submarines. Advancements in towed arrays, conformal arrays, and deployable sonar systems are critical for enhancing detection ranges and accuracy in diverse oceanic conditions. The increasing sophistication of submarine stealth capabilities necessitates continuous innovation in sensor technology, driving significant market share. Electronic Support Measures (ESM) are also gaining prominence as they provide vital passive intelligence on enemy submarine activities by detecting their electronic emissions. Armament, while crucial for the final neutralization of a submarine threat, follows closely behind sensors in terms of market dominance, as the deployment of torpedoes and depth charges is contingent on accurate detection and targeting information.

In terms of Platform dominance, Submarines themselves are key platforms, both as ASW hunters and as targets, driving demand for their own ASW systems. However, Surface Ships, particularly frigates and destroyers equipped with advanced ASW suites, represent a substantial and growing segment. These vessels form the backbone of many naval ASW operations, offering a versatile and deployable force. Helicopters equipped with dipping sonar and sonobuoys play a crucial role in rapidly deploying ASW capabilities over wide areas, making them indispensable assets. Maritime Patrol Aircraft (MPAs) are critical for long-range surveillance and the deployment of sonobuoys and air-launched torpedoes, extending the ASW "kill chain." The market for Unmanned Systems, including UUVs and unmanned surface vehicles (USVs) equipped with ASW sensors, is experiencing exponential growth. These platforms offer persistent, cost-effective, and low-risk solutions for reconnaissance, surveillance, and even engagement in hostile environments, positioning them as a future dominant platform. The strategic importance of maintaining oceanic control and deterring submarine threats ensures sustained investment across all these platforms, with a notable upward trend in the integration of advanced ASW systems into multi-role vessels and unmanned platforms.

Anti-Submarine Warfare Market Product Developments

The Anti-Submarine Warfare (ASW) market is witnessing a surge in product innovation driven by the need for enhanced detection, tracking, and engagement capabilities against increasingly stealthy submarines. Key developments include the integration of artificial intelligence and machine learning into sonar processing algorithms to improve signal-to-noise ratios and reduce false positives. Advances in sensor technology, such as multi-static sonar and novel acoustic materials, are expanding detection ranges and effectiveness. Furthermore, the proliferation of unmanned systems, including autonomous underwater vehicles (AUVs) and unmanned surface vessels (USVs) equipped with ASW payloads, offers persistent surveillance and cost-effective operational capabilities. These innovations provide significant competitive advantages by enabling faster response times, improved situational awareness, and the ability to operate in contested or denied environments.

Report Scope & Segmentation Analysis

This comprehensive report segments the Anti-Submarine Warfare (ASW) market across critical dimensions to provide granular insights. The System segmentation includes Sensors, which encompass sonar systems (hull-mounted, towed, dipping, and sonobuoys), magnetic anomaly detectors (MAD), and acoustic processors. The Electronic Support Measures (ESM) segment focuses on systems designed to detect, identify, and locate hostile electronic emissions. The Armament segment covers torpedoes, depth charges, and anti-submarine rockets. The Platform segmentation analyzes the ASW market across Submarines, Surface Ships (frigates, destroyers, cruisers), Helicopters, Maritime Patrol Aircraft (MPA), and Unmanned Systems (UUVs, USVs, UAVs). Each segment is analyzed for its market size, growth projections, and competitive dynamics, offering a detailed understanding of market penetration and future potential within each category.

Key Drivers of Anti-Submarine Warfare Market Growth

The Anti-Submarine Warfare (ASW) market growth is propelled by several critical drivers. Geopolitical instability and rising maritime tensions are compelling nations to invest heavily in ASW capabilities to counter potential submarine threats and secure vital sea lanes. Technological advancements, particularly in AI-powered sonar processing, advanced sensor fusion, and the integration of unmanned systems, are driving demand for modernized ASW platforms and equipment. The ongoing modernization of naval fleets worldwide, with a focus on acquiring next-generation submarines and surface combatants, directly translates into increased procurement of ASW systems. Furthermore, the development of more stealthy and advanced submarine technologies by potential adversaries necessitates a continuous evolutionary response in ASW capabilities, ensuring sustained market growth.

Challenges in the Anti-Submarine Warfare Market Sector

Despite the robust growth, the Anti-Submarine Warfare (ASW) market faces significant challenges. The high cost of developing and acquiring advanced ASW systems and platforms presents a substantial barrier for many nations, leading to protracted procurement cycles and potential budget constraints. Regulatory hurdles and complex export control regulations can impede the international transfer of critical ASW technologies, impacting market expansion for certain players. Supply chain disruptions, particularly for specialized electronic components and raw materials, can affect production timelines and costs. Intense competition among established defense contractors and emerging technology firms also pressures profit margins and necessitates continuous innovation to maintain market relevance.

Emerging Opportunities in Anti-Submarine Warfare Market

Emerging opportunities in the Anti-Submarine Warfare (ASW) market are centered around technological innovation and evolving operational paradigms. The increasing adoption of artificial intelligence and machine learning for enhanced acoustic signal processing and predictive maintenance presents a significant growth area. The rapid development and integration of unmanned systems, including UUVs and USVs equipped with ASW payloads, offer cost-effective and persistent surveillance solutions, opening new market avenues. The growing emphasis on network-centric warfare and data fusion creates demand for interoperable ASW systems that can seamlessly integrate with broader maritime domain awareness architectures. Furthermore, the expansion of ASW capabilities to address new types of underwater threats, such as unmanned underwater vehicles (UUVs) operated by state or non-state actors, presents a novel and growing opportunity.

Leading Players in the Anti-Submarine Warfare Market Market

- L3Harris Technologies Inc

- THALES

- TERM

- General Dynamics Corporation

- Elbit Systems Ltd

- Lockheed Martin Corporation

- Kongsberg Defense & Aerospace (Kongsberg Gruppen ASA)

- Safran SA

- RTX Corporation

- BAE Systems plc

- Northrop Grumman Corporation

- Saab AB

Key Developments in Anti-Submarine Warfare Market Industry

- September 2023: BAE Systems plc awarded contracts to A&P, and Cammell Laird awarded contracts to build units for the Royal Navy's Type 26 Frigates. The advanced anti-submarine warfare vessels are being constructed at BAE Systems' site in Scotland.

- July 2023: Damen Naval signed a contract with RH Marine for the new Anti-Submarine Warfare (ASW) Frigates. RH Marine will supply the Integrated Mission Management System (IMMS), the Integrated Navigation Bridge System (INBS), and the Integrated Platform Management System (IPMS) for each of the four frigates for the Dutch and Belgian Navies.

Strategic Outlook for Anti-Submarine Warfare Market Market

The strategic outlook for the Anti-Submarine Warfare (ASW) market is exceptionally positive, underpinned by persistent global security challenges and relentless technological progress. The ongoing modernization of naval forces worldwide, coupled with a heightened awareness of submarine threats, ensures sustained demand for advanced ASW systems and platforms. Key growth catalysts include the continued integration of artificial intelligence and machine learning for enhanced detection and tracking, the expansion of unmanned ASW capabilities for persistent surveillance, and the development of more sophisticated and adaptable sensor technologies. Strategic investments in R&D, coupled with agile adaptation to evolving threats, will be crucial for market players to capitalize on future opportunities and maintain a competitive edge in this critical domain of maritime security. The market is poised for significant expansion as nations prioritize the safeguarding of their maritime interests.

Anti-Submarine Warfare Market Segmentation

-

1. System

- 1.1. Sensors

- 1.2. Electronic Support Measures

- 1.3. Armament

-

2. Platform

- 2.1. Submarines

- 2.2. Surface Ships

- 2.3. Helicopters

- 2.4. Maritime Patrol Aircraft

- 2.5. Unmanned Systems

Anti-Submarine Warfare Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

- 4. Rest of the World

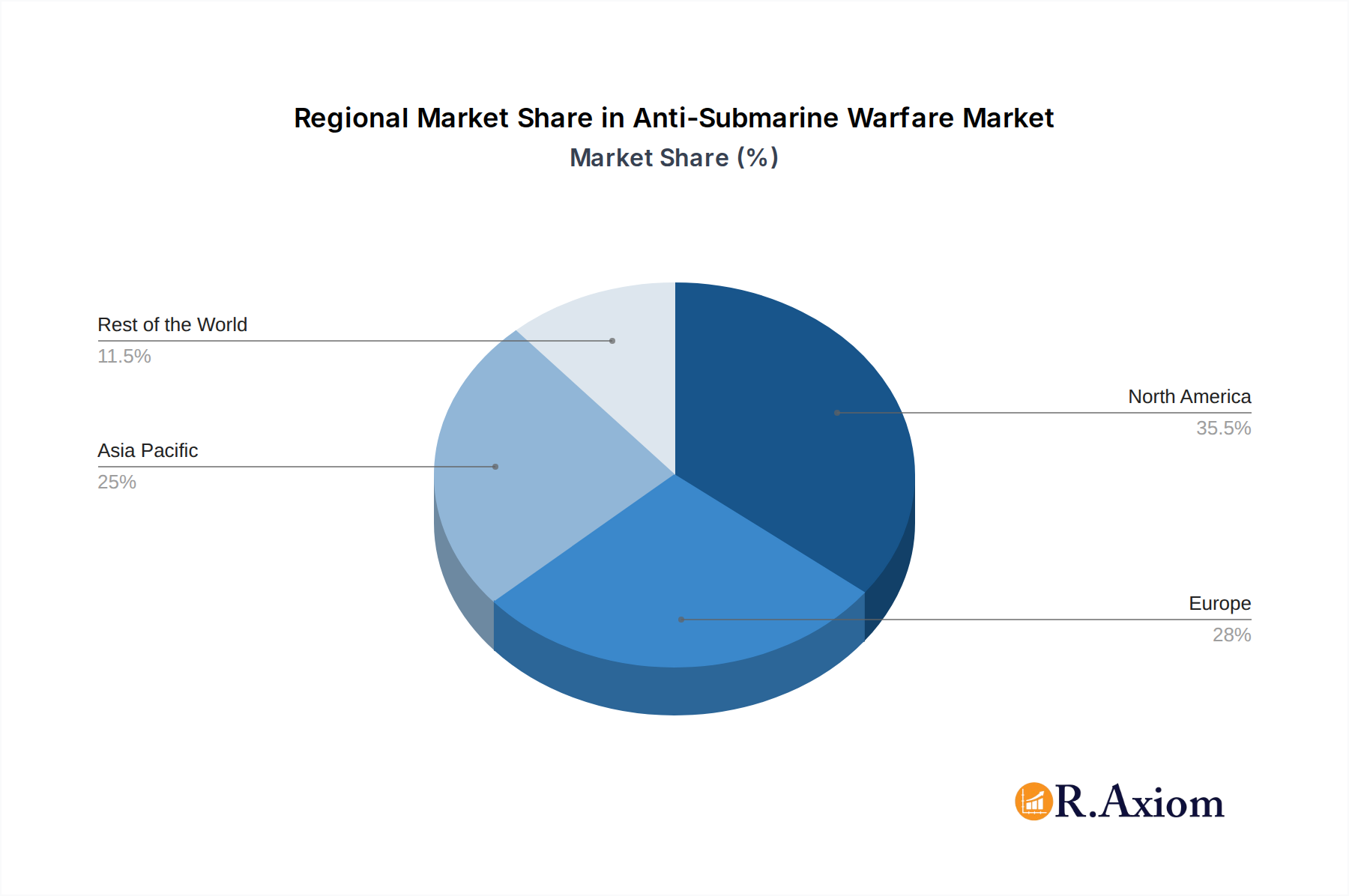

Anti-Submarine Warfare Market Regional Market Share

Geographic Coverage of Anti-Submarine Warfare Market

Anti-Submarine Warfare Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by System

- 5.1.1. Sensors

- 5.1.2. Electronic Support Measures

- 5.1.3. Armament

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Submarines

- 5.2.2. Surface Ships

- 5.2.3. Helicopters

- 5.2.4. Maritime Patrol Aircraft

- 5.2.5. Unmanned Systems

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by System

- 6. Global Anti-Submarine Warfare Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by System

- 6.1.1. Sensors

- 6.1.2. Electronic Support Measures

- 6.1.3. Armament

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Submarines

- 6.2.2. Surface Ships

- 6.2.3. Helicopters

- 6.2.4. Maritime Patrol Aircraft

- 6.2.5. Unmanned Systems

- 6.1. Market Analysis, Insights and Forecast - by System

- 7. North America Anti-Submarine Warfare Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by System

- 7.1.1. Sensors

- 7.1.2. Electronic Support Measures

- 7.1.3. Armament

- 7.2. Market Analysis, Insights and Forecast - by Platform

- 7.2.1. Submarines

- 7.2.2. Surface Ships

- 7.2.3. Helicopters

- 7.2.4. Maritime Patrol Aircraft

- 7.2.5. Unmanned Systems

- 7.1. Market Analysis, Insights and Forecast - by System

- 8. Europe Anti-Submarine Warfare Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by System

- 8.1.1. Sensors

- 8.1.2. Electronic Support Measures

- 8.1.3. Armament

- 8.2. Market Analysis, Insights and Forecast - by Platform

- 8.2.1. Submarines

- 8.2.2. Surface Ships

- 8.2.3. Helicopters

- 8.2.4. Maritime Patrol Aircraft

- 8.2.5. Unmanned Systems

- 8.1. Market Analysis, Insights and Forecast - by System

- 9. Asia Pacific Anti-Submarine Warfare Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by System

- 9.1.1. Sensors

- 9.1.2. Electronic Support Measures

- 9.1.3. Armament

- 9.2. Market Analysis, Insights and Forecast - by Platform

- 9.2.1. Submarines

- 9.2.2. Surface Ships

- 9.2.3. Helicopters

- 9.2.4. Maritime Patrol Aircraft

- 9.2.5. Unmanned Systems

- 9.1. Market Analysis, Insights and Forecast - by System

- 10. Rest of the World Anti-Submarine Warfare Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by System

- 10.1.1. Sensors

- 10.1.2. Electronic Support Measures

- 10.1.3. Armament

- 10.2. Market Analysis, Insights and Forecast - by Platform

- 10.2.1. Submarines

- 10.2.2. Surface Ships

- 10.2.3. Helicopters

- 10.2.4. Maritime Patrol Aircraft

- 10.2.5. Unmanned Systems

- 10.1. Market Analysis, Insights and Forecast - by System

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 L3Harris Technologies Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 THALES

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 TERM

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 General Dynamics Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Elbit Systems Ltd

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Lockheed Martin Corporation

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Kongsberg Defense & Aerospace (Kongsberg Gruppen ASA)

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Safran SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 RTX Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 BAE Systems plc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Northrop Grumman Corporation

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Saab AB

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 L3Harris Technologies Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Anti-Submarine Warfare Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Anti-Submarine Warfare Market Revenue (billion), by System 2025 & 2033

- Figure 3: North America Anti-Submarine Warfare Market Revenue Share (%), by System 2025 & 2033

- Figure 4: North America Anti-Submarine Warfare Market Revenue (billion), by Platform 2025 & 2033

- Figure 5: North America Anti-Submarine Warfare Market Revenue Share (%), by Platform 2025 & 2033

- Figure 6: North America Anti-Submarine Warfare Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Anti-Submarine Warfare Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Anti-Submarine Warfare Market Revenue (billion), by System 2025 & 2033

- Figure 9: Europe Anti-Submarine Warfare Market Revenue Share (%), by System 2025 & 2033

- Figure 10: Europe Anti-Submarine Warfare Market Revenue (billion), by Platform 2025 & 2033

- Figure 11: Europe Anti-Submarine Warfare Market Revenue Share (%), by Platform 2025 & 2033

- Figure 12: Europe Anti-Submarine Warfare Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Anti-Submarine Warfare Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Anti-Submarine Warfare Market Revenue (billion), by System 2025 & 2033

- Figure 15: Asia Pacific Anti-Submarine Warfare Market Revenue Share (%), by System 2025 & 2033

- Figure 16: Asia Pacific Anti-Submarine Warfare Market Revenue (billion), by Platform 2025 & 2033

- Figure 17: Asia Pacific Anti-Submarine Warfare Market Revenue Share (%), by Platform 2025 & 2033

- Figure 18: Asia Pacific Anti-Submarine Warfare Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Anti-Submarine Warfare Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Anti-Submarine Warfare Market Revenue (billion), by System 2025 & 2033

- Figure 21: Rest of the World Anti-Submarine Warfare Market Revenue Share (%), by System 2025 & 2033

- Figure 22: Rest of the World Anti-Submarine Warfare Market Revenue (billion), by Platform 2025 & 2033

- Figure 23: Rest of the World Anti-Submarine Warfare Market Revenue Share (%), by Platform 2025 & 2033

- Figure 24: Rest of the World Anti-Submarine Warfare Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Anti-Submarine Warfare Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Anti-Submarine Warfare Market Revenue billion Forecast, by System 2020 & 2033

- Table 2: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 3: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Anti-Submarine Warfare Market Revenue billion Forecast, by System 2020 & 2033

- Table 5: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 6: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Anti-Submarine Warfare Market Revenue billion Forecast, by System 2020 & 2033

- Table 10: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 11: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: France Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Germany Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Russia Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Global Anti-Submarine Warfare Market Revenue billion Forecast, by System 2020 & 2033

- Table 18: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 19: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Country 2020 & 2033

- Table 20: China Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: India Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Japan Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Australia Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: South Korea Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Anti-Submarine Warfare Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Anti-Submarine Warfare Market Revenue billion Forecast, by System 2020 & 2033

- Table 27: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 28: Global Anti-Submarine Warfare Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Anti-Submarine Warfare Market?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Anti-Submarine Warfare Market?

Key companies in the market include L3Harris Technologies Inc, THALES, TERM, General Dynamics Corporation, Elbit Systems Ltd, Lockheed Martin Corporation, Kongsberg Defense & Aerospace (Kongsberg Gruppen ASA), Safran SA, RTX Corporation, BAE Systems plc, Northrop Grumman Corporation, Saab AB.

3. What are the main segments of the Anti-Submarine Warfare Market?

The market segments include System, Platform.

4. Can you provide details about the market size?

The market size is estimated to be USD 18.6 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Submarines to WItness Highest Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

September 2023: BAE Systems plc awarded contracts to A&P, and Cammell Laird awarded contracts to build units for the Royal Navy's Type 26 Frigates. The advanced anti-submarine warfare vessels are being constructed at BAE Systems' site in Scotland.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Anti-Submarine Warfare Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Anti-Submarine Warfare Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Anti-Submarine Warfare Market?

To stay informed about further developments, trends, and reports in the Anti-Submarine Warfare Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence