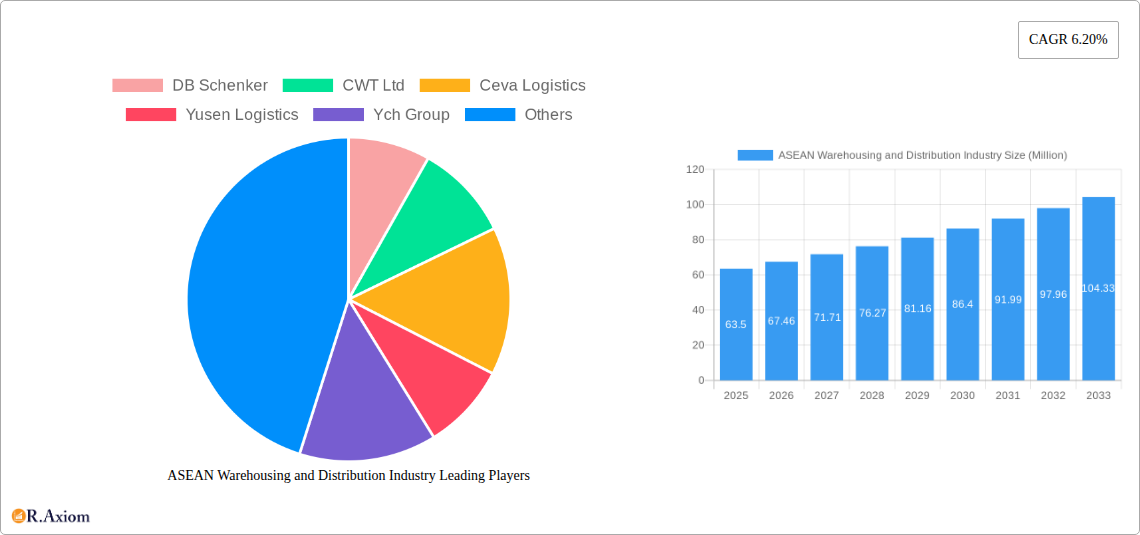

Key Insights

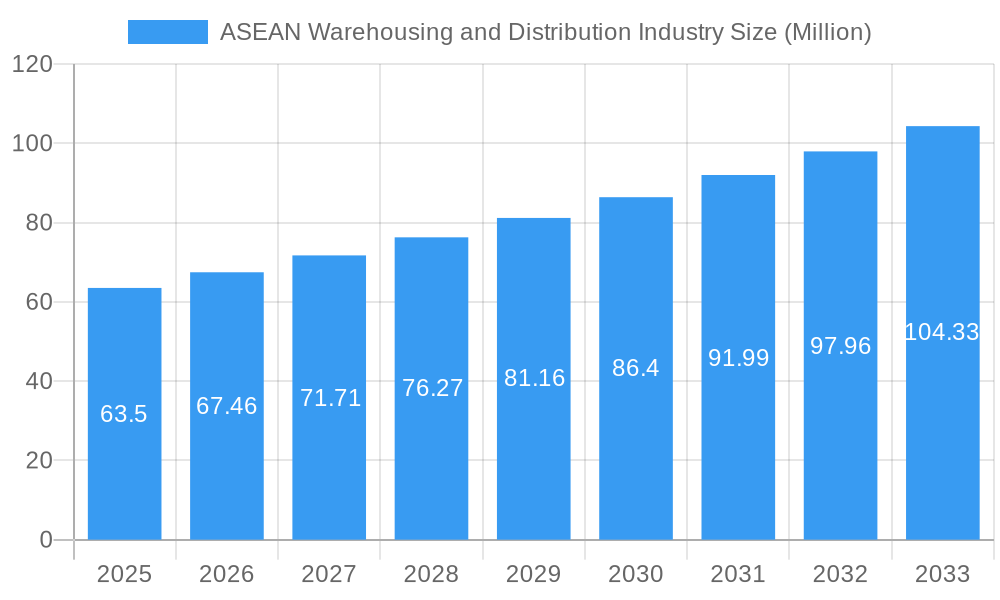

The ASEAN warehousing and distribution industry is experiencing robust growth, fueled by the region's expanding e-commerce sector, rising consumer spending, and increasing manufacturing activity. The market, currently valued at approximately $63.50 million in 2025, is projected to maintain a Compound Annual Growth Rate (CAGR) of 6.20% from 2025 to 2033. This growth is driven by several key factors. The rise of e-commerce necessitates efficient warehousing and distribution networks to handle the surge in online orders and deliveries. Furthermore, the increasing complexity of supply chains, particularly within the automotive, pharmaceutical, and FMCG sectors, is driving demand for sophisticated value-added services such as inventory management, packaging, and labeling. Growth is also spurred by advancements in technology, including warehouse management systems (WMS) and automated guided vehicles (AGVs), improving efficiency and reducing operational costs. However, challenges remain, including infrastructure limitations in certain areas, a potential shortage of skilled labor, and increasing land and construction costs.

ASEAN Warehousing and Distribution Industry Market Size (In Million)

Despite these restraints, the industry's strong fundamentals suggest continued expansion. The segmentation by service type (warehousing, distribution, and value-added services) reveals a diversified market with significant potential across all segments. Similarly, the diverse end-user industries (retail & e-commerce, automotive, pharmaceutical & healthcare, FMCG, manufacturing, and electronics) contribute to the industry's resilience and growth trajectory. Leading players such as DB Schenker, Kuehne + Nagel, and others are strategically investing in infrastructure and technology to capitalize on these opportunities, further consolidating their market positions. The significant presence of major players from various regions indicates a competitive landscape that will drive innovation and efficiency improvements in the ASEAN warehousing and distribution market. This makes the ASEAN region an attractive investment destination for both existing and new entrants to the warehousing and distribution industry.

ASEAN Warehousing and Distribution Industry Company Market Share

ASEAN Warehousing and Distribution Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the ASEAN warehousing and distribution industry, offering invaluable insights for industry stakeholders, investors, and businesses seeking to navigate this dynamic market. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages historical data (2019-2024) to project future trends and opportunities. The report values are in Millions.

ASEAN Warehousing and Distribution Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the ASEAN warehousing and distribution market, examining market concentration, innovation drivers, regulatory frameworks, and recent M&A activity. The industry exhibits a moderately concentrated structure, with several large players holding significant market share. Key players include DB Schenker, CWT Ltd, Ceva Logistics, Yusen Logistics, YCH Group, Gemadept, WHA Corporation, Kuehne + Nagel, Singapore Post, Agility, Kerry Logistics, CJ Century Logistics, Tiong Nam Logistics, Keppel Logistics, DHL Supply Chain, and others. Market share data for 2024 suggests that the top 5 players hold approximately xx% of the total market, while the remaining players contribute to the remaining share.

- Market Concentration: The Herfindahl-Hirschman Index (HHI) for 2024 is estimated at xx, indicating a moderately concentrated market.

- Innovation Drivers: Automation, technological advancements in warehouse management systems (WMS), and the rise of e-commerce are key innovation drivers.

- Regulatory Frameworks: Varying regulations across ASEAN nations influence operational efficiency and compliance costs.

- M&A Activity: Significant M&A activity has reshaped the industry landscape, with notable deals impacting market share and service offerings. For instance, the Maersk acquisition of LF Logistics added 223 warehouses and 9.5 million square meters of space to its portfolio, significantly increasing its market presence. The Geodis acquisition of Keppel Logistics also marked a substantial expansion in Southeast Asia. Total M&A deal value in 2024 is estimated at $xx Million.

- End-User Trends: Growing e-commerce adoption and evolving consumer preferences drive demand for efficient and flexible warehousing and distribution solutions.

ASEAN Warehousing and Distribution Industry Industry Trends & Insights

This section delves into the key trends shaping the ASEAN warehousing and distribution industry. The market exhibits robust growth, fueled by several factors, including the expansion of e-commerce, increasing manufacturing activity, and improving infrastructure in several key ASEAN nations. The compound annual growth rate (CAGR) for the period 2025-2033 is projected at xx%. Market penetration of advanced warehousing technologies (like robotics and AI) is gradually increasing, though adoption rates vary across the region. Consumer preferences are shifting towards faster delivery times and greater transparency throughout the supply chain. Competitive dynamics are characterized by consolidation, strategic alliances, and a growing focus on value-added services.

Dominant Markets & Segments in ASEAN Warehousing and Distribution Industry

This section identifies the dominant regions, countries, and segments within the ASEAN warehousing and distribution industry.

By Service Type:

- Warehousing Services: This remains the largest segment, driven by the expanding e-commerce sector and rising demand for storage and order fulfillment.

- Distribution Services: Growth in this segment is closely tied to advancements in logistics and transportation infrastructure.

- Value-Added Services: This segment is experiencing rapid growth, with increasing demand for specialized services such as labeling, packaging, and inventory management.

By End-User Industry:

- Retail & E-commerce: This is the fastest-growing segment, fueled by the burgeoning e-commerce market in the region.

- Automotive: This sector's demand is driven by the growth in automotive manufacturing and sales within ASEAN.

- Pharmaceutical & Healthcare: This segment is characterized by stringent regulations and a focus on cold chain logistics.

- FMCG (Fast-Moving Consumer Goods): This is a significant segment, with high volume and fast turnaround times.

- Manufacturing: Manufacturing activities across various sectors contribute significantly to warehousing and distribution needs.

- Electronics: The electronics manufacturing sector in ASEAN creates a substantial demand for specialized warehousing solutions.

Dominant Markets: Singapore, Thailand, and Vietnam are identified as the leading markets, driven by strong economic growth, strategic locations, and advanced infrastructure. Key drivers include supportive government policies promoting logistics development, robust FDI, and the presence of large multinational corporations. These markets exhibit higher market penetration rates and greater technological adoption in comparison to other nations within the region.

ASEAN Warehousing and Distribution Industry Product Developments

Innovations within the ASEAN warehousing and distribution industry are significantly driven by the integration of cutting-edge technologies designed to revolutionize operational efficiency and supply chain management. Key advancements include the widespread adoption of AI-powered Warehouse Management Systems (WMS) for intelligent inventory control and predictive analytics, the deployment of Automated Guided Vehicles (AGVs) for seamless material handling, and the increasing use of robotics for tasks such as picking, packing, and sorting. These technological integrations are instrumental in boosting operational throughput, minimizing errors, and providing unparalleled supply chain visibility. While more developed economies within ASEAN are leading in the adoption of these technologies, a discernible trend towards broader implementation is evident across the region. These pioneering developments are critical for businesses aiming to establish and maintain a competitive edge in this rapidly evolving and highly competitive market.

Report Scope & Segmentation Analysis

This comprehensive report meticulously segments the ASEAN warehousing and distribution market to offer granular insights. The segmentation encompasses: Service Type (including warehousing, distribution, and value-added services) and End-User Industry (covering retail & e-commerce, automotive, pharmaceutical & healthcare, Fast-Moving Consumer Goods (FMCG), manufacturing, and electronics). For each segment, the analysis provides detailed growth projections, estimated market sizes (expressed in Millions USD), and an in-depth examination of competitive dynamics. The retail and e-commerce segment is identified as possessing the highest growth potential, driven by online retail expansion. Conversely, the pharmaceutical and healthcare segment stands out due to its high-value cargo and stringent regulatory and specialized handling requirements. The estimated market size for 2025 is approximately XX Million USD for warehousing, XX Million USD for distribution, and XX Million USD for value-added services. Market sizes for each end-user industry segment are also estimated accordingly, reflecting their respective contributions and growth trajectories.

Key Drivers of ASEAN Warehousing and Distribution Industry Growth

The growth of the ASEAN warehousing and distribution industry is propelled by several factors. Firstly, the burgeoning e-commerce sector necessitates efficient warehousing and fulfillment capabilities. Secondly, increased foreign direct investment (FDI) in manufacturing and logistics has boosted infrastructure development and capacity expansion. Thirdly, favorable government policies aimed at promoting trade and logistics have fostered a conducive business environment. Finally, technological advancements, such as automation and data analytics, are streamlining operations and improving efficiency.

Challenges in the ASEAN Warehousing and Distribution Industry Sector

The industry faces several challenges, including infrastructure gaps in some regions, regulatory inconsistencies across countries, and a skilled labor shortage. Supply chain disruptions, particularly during periods of economic uncertainty or global crises, also pose significant risks. These challenges, if not effectively addressed, could hinder the industry's growth trajectory. The estimated impact of these challenges on overall market growth in 2025 is approximately xx%.

Emerging Opportunities in ASEAN Warehousing and Distribution Industry

The ASEAN warehousing and distribution industry presents significant opportunities. The expansion of e-commerce across the region presents massive potential for growth. The adoption of innovative technologies like blockchain and the Internet of Things (IoT) offers opportunities for improved supply chain transparency and efficiency. The development of specialized warehousing solutions for specific industries, such as cold chain logistics for pharmaceuticals, also represents a significant opportunity.

Leading Players in the ASEAN Warehousing and Distribution Industry Market

- DB Schenker: A global logistics provider with a strong presence in ASEAN, offering integrated logistics solutions.

- CWT Ltd: A prominent integrated logistics service provider in Asia, with extensive warehousing and distribution networks.

- Ceva Logistics: A leading global supply chain company operating across the ASEAN region, specializing in freight management and contract logistics.

- Yusen Logistics: A global logistics company providing comprehensive supply chain solutions, including warehousing and distribution, within ASEAN.

- YCH Group: A leading end-to-end supply chain solutions provider in Asia, headquartered in Singapore, with significant operations across ASEAN.

- Gemadept: A major Vietnamese logistics and port operator with a growing warehousing and distribution network in the region.

- WHA Corporation: A leading industrial estate and logistics provider in Thailand, offering integrated solutions including warehousing.

- Kuehne + Nagel: A global transport and logistics company with a substantial footprint in ASEAN, providing warehousing and distribution services.

- Singapore Post (SingPost): A leading postal and logistics provider in Singapore and ASEAN, with a focus on e-commerce logistics.

- Agility: A global logistics provider with a strong presence in the Middle East and Asia, including comprehensive warehousing and distribution services in ASEAN.

- Kerry Logistics: A leading integrated logistics provider in Asia, with extensive operations and a robust network across ASEAN.

- CJ Century Logistics: A prominent logistics company in Malaysia and ASEAN, offering a wide range of warehousing and distribution services.

- Tiong Nam Logistics: One of the largest integrated logistics and warehousing providers in Malaysia, with a significant reach in ASEAN.

- Keppel Logistics: A key player in Singapore and ASEAN, offering integrated logistics and supply chain solutions.

- DHL Supply Chain: The contract logistics division of Deutsche Post DHL Group, a global leader with extensive operations and warehousing facilities across ASEAN.

- Peh-Shi Logistics: A dynamic and rapidly expanding logistics player in Southeast Asia, focusing on innovative warehousing solutions and last-mile delivery. Website: www.peh-shi.com

- Nava Logistics: A prominent third-party logistics (3PL) provider in Thailand, offering specialized warehousing and distribution services tailored to various industries. Website: www.navalogistics.com

- Ninja Van: A leading technology-enabled logistics company focused on e-commerce deliveries and warehousing solutions across Southeast Asia. Website: www.ninjavan.co

Key Developments in ASEAN Warehousing and Distribution Industry Industry

- August 2022: Maersk's acquisition of LF Logistics significantly expanded its warehousing capacity in ASEAN, adding 223 warehouses and 9.5 million square meters of space. This consolidation strengthened its market position and broadened its omnichannel fulfillment capabilities.

- April 2022: Geodis' acquisition of Keppel Logistics expanded its presence in Southeast Asia, enhancing its contract logistics and e-commerce fulfillment services.

Strategic Outlook for ASEAN Warehousing and Distribution Industry Market

The ASEAN warehousing and distribution industry is strategically positioned for sustained and accelerated growth, underpinned by the relentless expansion of the e-commerce ecosystem, increasing industrialization across the region, and proactive government initiatives aimed at fostering robust logistics infrastructure. The successful integration of advanced technologies and the cultivation of strategic partnerships will be paramount for companies aspiring to not only survive but also excel within this intensely competitive arena. The long-term outlook for the industry remains exceptionally promising, with expectations of significant expansion across all defined segments. Particular emphasis will be placed on rapidly developing economies within ASEAN, which are poised to become major hubs for logistics innovation and operational excellence.

ASEAN Warehousing and Distribution Industry Segmentation

-

1. Geography

- 1.1. Singapore

- 1.2. Thailand

- 1.3. Malaysia

- 1.4. Vietnam

- 1.5. Indonesia

- 1.6. Philippines

- 1.7. Rest of ASEAN

ASEAN Warehousing and Distribution Industry Segmentation By Geography

- 1. Singapore

- 2. Thailand

- 3. Malaysia

- 4. Vietnam

- 5. Indonesia

- 6. Philippines

- 7. Rest of ASEAN

ASEAN Warehousing and Distribution Industry Regional Market Share

Geographic Coverage of ASEAN Warehousing and Distribution Industry

ASEAN Warehousing and Distribution Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 5.1.1. Singapore

- 5.1.2. Thailand

- 5.1.3. Malaysia

- 5.1.4. Vietnam

- 5.1.5. Indonesia

- 5.1.6. Philippines

- 5.1.7. Rest of ASEAN

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Singapore

- 5.2.2. Thailand

- 5.2.3. Malaysia

- 5.2.4. Vietnam

- 5.2.5. Indonesia

- 5.2.6. Philippines

- 5.2.7. Rest of ASEAN

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 6. Global ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 6.1.1. Singapore

- 6.1.2. Thailand

- 6.1.3. Malaysia

- 6.1.4. Vietnam

- 6.1.5. Indonesia

- 6.1.6. Philippines

- 6.1.7. Rest of ASEAN

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 7. Singapore ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 7.1.1. Singapore

- 7.1.2. Thailand

- 7.1.3. Malaysia

- 7.1.4. Vietnam

- 7.1.5. Indonesia

- 7.1.6. Philippines

- 7.1.7. Rest of ASEAN

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 8. Thailand ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 8.1.1. Singapore

- 8.1.2. Thailand

- 8.1.3. Malaysia

- 8.1.4. Vietnam

- 8.1.5. Indonesia

- 8.1.6. Philippines

- 8.1.7. Rest of ASEAN

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 9. Malaysia ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 9.1.1. Singapore

- 9.1.2. Thailand

- 9.1.3. Malaysia

- 9.1.4. Vietnam

- 9.1.5. Indonesia

- 9.1.6. Philippines

- 9.1.7. Rest of ASEAN

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 10. Vietnam ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 10.1.1. Singapore

- 10.1.2. Thailand

- 10.1.3. Malaysia

- 10.1.4. Vietnam

- 10.1.5. Indonesia

- 10.1.6. Philippines

- 10.1.7. Rest of ASEAN

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 11. Indonesia ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 11.1.1. Singapore

- 11.1.2. Thailand

- 11.1.3. Malaysia

- 11.1.4. Vietnam

- 11.1.5. Indonesia

- 11.1.6. Philippines

- 11.1.7. Rest of ASEAN

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 12. Philippines ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Geography

- 12.1.1. Singapore

- 12.1.2. Thailand

- 12.1.3. Malaysia

- 12.1.4. Vietnam

- 12.1.5. Indonesia

- 12.1.6. Philippines

- 12.1.7. Rest of ASEAN

- 12.1. Market Analysis, Insights and Forecast - by Geography

- 13. Rest of ASEAN ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Geography

- 13.1.1. Singapore

- 13.1.2. Thailand

- 13.1.3. Malaysia

- 13.1.4. Vietnam

- 13.1.5. Indonesia

- 13.1.6. Philippines

- 13.1.7. Rest of ASEAN

- 13.1. Market Analysis, Insights and Forecast - by Geography

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 DB Schenker

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 CWT Ltd

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Ceva Logistics

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Yusen Logistics

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Ych Group

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Gemadept

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 WHA Corporation

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Kuehne + Nagel

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Singapore Post

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 Agility

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Kerry Logistics

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 CJ Century Logistics

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 Tiong Nam Logistics

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.14 Keppel Logistics**List Not Exhaustive 6 3 Other Companies (Key Information/Overview

- 14.1.14.1. Company Overview

- 14.1.14.2. Products

- 14.1.14.3. Company Financials

- 14.1.14.4. SWOT Analysis

- 14.1.15 DHL Supply Chain

- 14.1.15.1. Company Overview

- 14.1.15.2. Products

- 14.1.15.3. Company Financials

- 14.1.15.4. SWOT Analysis

- 14.1.1 DB Schenker

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Global ASEAN Warehousing and Distribution Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Singapore ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 3: Singapore ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 4: Singapore ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: Singapore ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Thailand ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 7: Thailand ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: Thailand ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Thailand ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Malaysia ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 11: Malaysia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 12: Malaysia ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Malaysia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Vietnam ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 15: Vietnam ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: Vietnam ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Vietnam ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Indonesia ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 19: Indonesia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 20: Indonesia ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Indonesia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Philippines ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 23: Philippines ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Philippines ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Philippines ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 27: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 28: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 29: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 2: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the ASEAN Warehousing and Distribution Industry?

The projected CAGR is approximately 6.20%.

2. Which companies are prominent players in the ASEAN Warehousing and Distribution Industry?

Key companies in the market include DB Schenker, CWT Ltd, Ceva Logistics, Yusen Logistics, Ych Group, Gemadept, WHA Corporation, Kuehne + Nagel, Singapore Post, Agility, Kerry Logistics, CJ Century Logistics, Tiong Nam Logistics, Keppel Logistics**List Not Exhaustive 6 3 Other Companies (Key Information/Overview, DHL Supply Chain.

3. What are the main segments of the ASEAN Warehousing and Distribution Industry?

The market segments include Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.50 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in the demand for the Air Cargo Capacity; The Rise of E-commerce.

6. What are the notable trends driving market growth?

Increase in Warehousing Space in Thailand.

7. Are there any restraints impacting market growth?

Cargo Restrictions.

8. Can you provide examples of recent developments in the market?

August 2022: A.P. Moller - Maersk (Maersk) announced the successful completion of its acquisition of LF Logistics, a logistics firm with premium capabilities in omnichannel fulfillment services, e-commerce, and inland shipping in the ASEAN region. Following the acquisition, Maersk will expand its warehouse network by adding 223 warehouses to its current network and increasing the total number of facilities, spread across 9.5 million square meters, to 549.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "ASEAN Warehousing and Distribution Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the ASEAN Warehousing and Distribution Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the ASEAN Warehousing and Distribution Industry?

To stay informed about further developments, trends, and reports in the ASEAN Warehousing and Distribution Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence