Key Insights

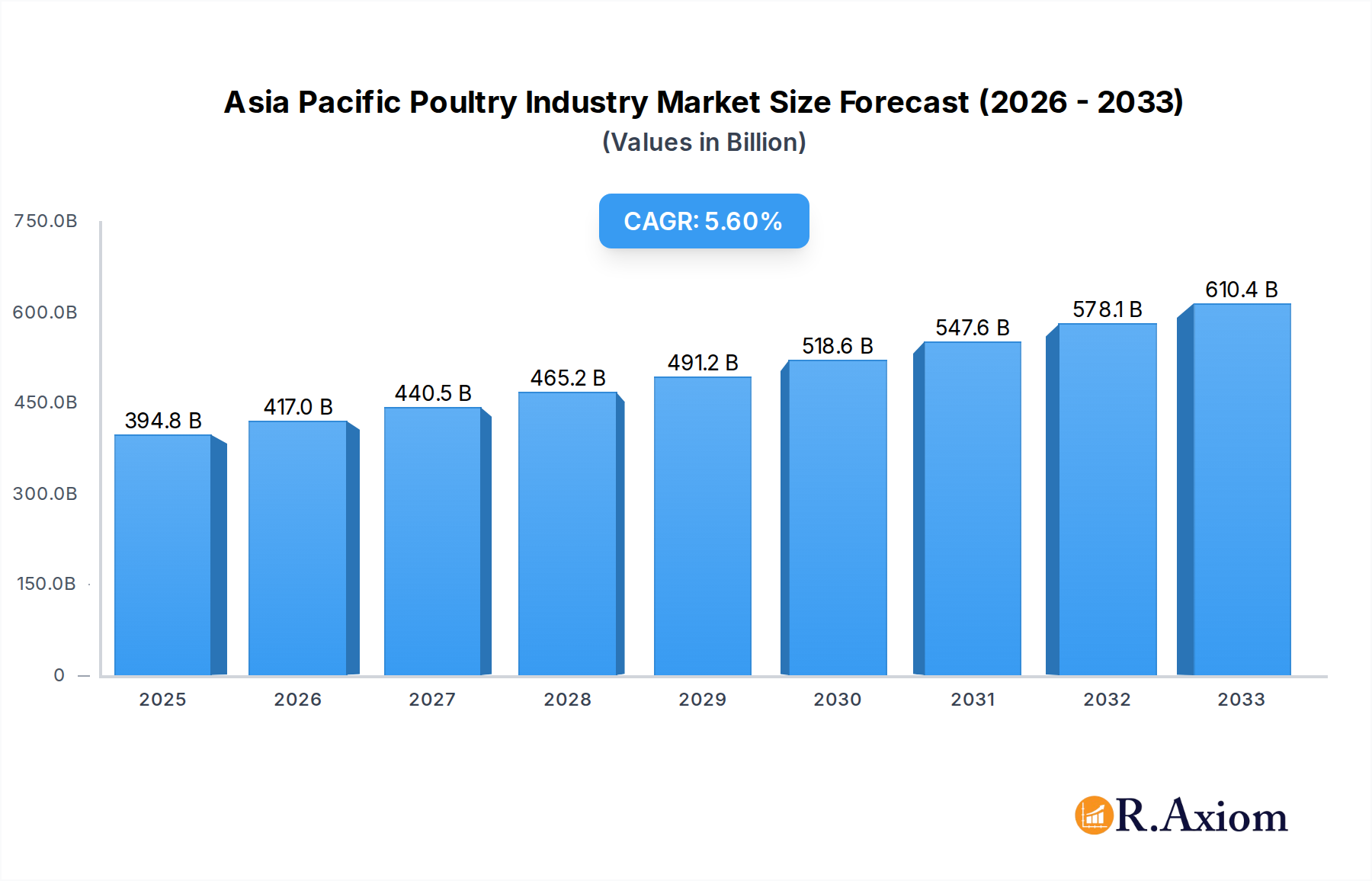

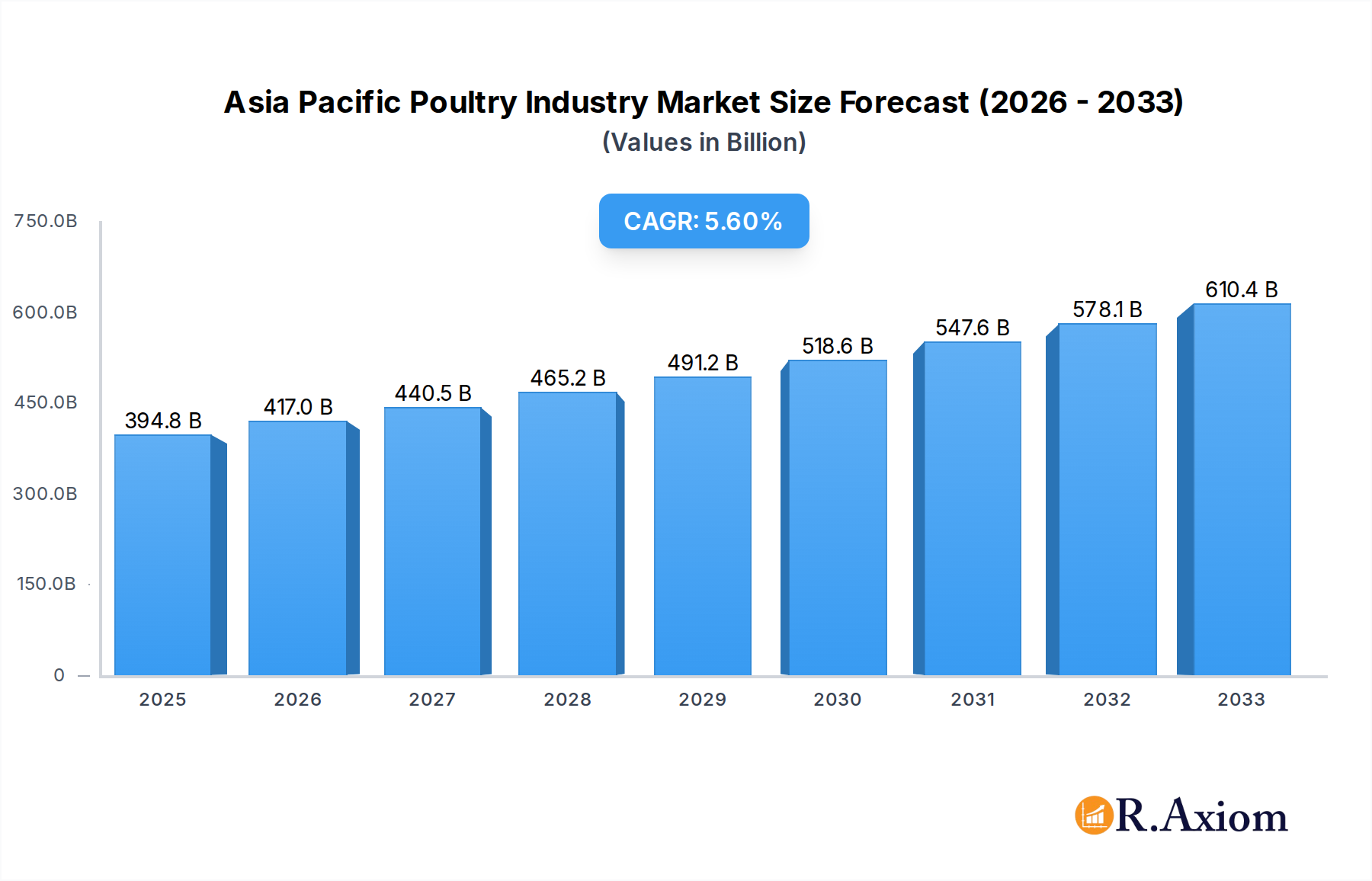

The Asia Pacific Poultry Industry is poised for robust growth, projected to reach a market size of $394.75 billion in 2025. Driven by a burgeoning population, increasing disposable incomes, and a growing preference for protein-rich diets, the demand for chicken meat and table eggs is expected to surge. The region's CAGR of 5.7% signifies a sustained expansion over the forecast period (2025-2033). Key drivers include the rising adoption of modern farming techniques, advancements in poultry genetics, and improved disease management practices, all contributing to enhanced production efficiency and quality. The growing middle class across nations like China, India, and Southeast Asian countries is a significant catalyst, with consumers increasingly opting for convenient and processed poultry products. Furthermore, the expanding on-trade and off-trade distribution channels, particularly the rapid growth of online retail and modern supermarkets, are making poultry products more accessible to a wider consumer base.

Asia Pacific Poultry Industry Market Size (In Billion)

The industry's trajectory is shaped by several influential trends, including the increasing demand for value-added poultry products such as ready-to-eat meals and marinated chicken, as well as a heightened focus on food safety and traceability. Technological innovations in animal husbandry and feed management are also playing a crucial role in optimizing production and reducing costs. While the market exhibits strong growth potential, certain restraints, such as fluctuating feed prices, the prevalence of avian influenza outbreaks, and stringent environmental regulations, need to be proactively managed by industry players. The competitive landscape is dominated by large, integrated players like Suguna Foods and Charoen Pokphand Group, who are strategically expanding their operations and product portfolios to cater to evolving consumer preferences and capitalize on the market's dynamism.

Asia Pacific Poultry Industry Company Market Share

Asia Pacific Poultry Industry Market Concentration & Innovation

The Asia Pacific poultry market, projected to reach hundreds of billions in value by 2033, exhibits a dynamic blend of concentrated major players and a burgeoning landscape of innovative startups. Market concentration is evident with global giants like Charoen Pokphand Group, Tyson Foods Inc., and Cargill Inc. holding significant market shares, particularly in large-scale production and processing. These entities leverage economies of scale, extensive distribution networks, and established brand recognition. However, innovation is a key differentiator, with a growing emphasis on sustainability, cultured meat alternatives, and advanced processing technologies. Regulatory frameworks across different Asia Pacific nations play a crucial role, influencing production standards, food safety, and market access, thereby shaping competitive dynamics. Product substitutes, such as plant-based proteins, pose an evolving challenge, driving the industry to enhance the appeal and perceived health benefits of poultry. End-user trends lean towards convenience, premium quality, and ethically sourced products, compelling companies to adapt their offerings. Mergers and acquisitions (M&A) activities, while not always disclosed in full billion-dollar figures, are strategic moves by leading companies to expand their geographical reach, acquire new technologies, or consolidate market share. For instance, understanding the M&A landscape is crucial to grasping the evolving competitive structure.

- Market Share: Dominated by a few key players in bulk production, with increasing fragmentation in niche and value-added segments.

- Innovation Drivers: Sustainable farming, cultured meat, processed food innovation, and traceability.

- Regulatory Frameworks: Varied across countries, impacting imports/exports, safety standards, and subsidies.

- Product Substitutes: Growing threat from plant-based alternatives.

- End-User Trends: Demand for convenience, health-conscious options, and ethical sourcing.

- M&A Activities: Strategic acquisitions to gain market access and technological advantages.

Asia Pacific Poultry Industry Industry Trends & Insights

The Asia Pacific poultry industry is poised for substantial growth, driven by a confluence of favorable market trends and transformative technological advancements. A compound annual growth rate (CAGR) of over XX% is anticipated throughout the forecast period, underpinned by a burgeoning population and a rising middle class with increasing disposable incomes. This demographic shift directly translates to higher per capita consumption of protein, with chicken emerging as a preferred choice due to its affordability, versatility, and perceived health benefits compared to other meat sources. Technological disruptions are revolutionizing every stage of the poultry value chain. Automation in farming operations, including advanced feeding systems and climate control, enhances efficiency and animal welfare. Furthermore, innovative processing technologies are enabling the production of a wider range of value-added products, catering to diverse consumer preferences. The penetration of processed poultry products, including ready-to-eat meals and marinated options, is steadily increasing, reflecting busy lifestyles and a demand for convenience.

Consumer preferences are evolving rapidly. There is a growing awareness and demand for poultry products that are not only safe and affordable but also produced sustainably and ethically. This includes a focus on antibiotic-free production, improved animal welfare standards, and reduced environmental impact. Traceability from farm to fork is becoming increasingly important, fostering consumer trust and brand loyalty. The competitive landscape is characterized by intense competition among both established global players and agile local enterprises. Companies are investing heavily in research and development to differentiate their products, optimize supply chains, and expand their market reach. E-commerce platforms are also playing a significant role, providing new distribution channels and direct access to consumers, especially in urban centers. The industry is witnessing a strategic pivot towards product diversification, moving beyond basic chicken meat and table eggs to include a wider array of processed and specialty poultry items. This strategic imperative is crucial for capturing higher profit margins and catering to the nuanced demands of the modern consumer.

- Market Growth Drivers: Rising population, increasing disposable income, and favorable protein consumption trends.

- Technological Disruptions: Automation in farming, advanced processing, and supply chain optimization.

- Consumer Preferences: Demand for convenience, health-conscious, sustainable, and ethically sourced poultry.

- Competitive Dynamics: Intense competition, strategic partnerships, and investment in R&D.

- Market Penetration: Increasing penetration of processed and value-added poultry products.

Dominant Markets & Segments in Asia Pacific Poultry Industry

The Asia Pacific poultry industry is a multifaceted market, with significant dominance observed across various regions and product segments. China and India stand out as dominant markets, driven by their massive populations, rapid economic growth, and expanding middle class. These nations represent the largest consumers and producers of poultry products, influencing global market dynamics. Within product types, Chicken Meat is the most dominant segment, accounting for a substantial portion of the market value.

Chicken Meat Dominance:

- Fresh / Chilled: This sub-segment holds a leading position due to consumer preference for freshness and the burgeoning modern retail infrastructure in urban areas of countries like China, Japan, and South Korea. Supermarkets and hypermarkets are key distribution channels, offering a wide variety of fresh poultry cuts.

- Frozen / Canned: Significant for its longer shelf life and affordability, this sub-segment is crucial for catering to a broader consumer base, including rural populations and for use in food service industries. Emerging economies with developing cold chain infrastructure are seeing accelerated growth here.

- Processed: This is a rapidly expanding segment, driven by the demand for convenience and ready-to-eat meals. Products like chicken nuggets, sausages, and marinated chicken cuts are gaining immense popularity across all distribution channels, especially in urban centers of Southeast Asia.

Table Eggs: While a fundamental part of the poultry industry, table eggs, though substantial in volume, represent a smaller market value compared to chicken meat. The segment is characterized by widespread production and consumption, with both traditional and modernized farming practices coexisting. Growth is steady, driven by nutritional value and affordability.

Distribution Channel Dominance:

- Off-Trade: This channel, particularly Supermarkets/Hypermarkets, is the most dominant and fastest-growing. These outlets provide a convenient one-stop shopping experience, displaying a wide array of poultry products under controlled temperature conditions, ensuring quality and safety. Their extensive reach in urban and semi-urban areas makes them pivotal for market penetration.

- Online Retail: Witnessing exponential growth, online retail is rapidly becoming a significant distribution channel. This is especially true for pre-packaged and value-added products, offering consumers convenience and wider choices delivered to their doorstep. The COVID-19 pandemic accelerated this trend, and it continues to be a key growth area.

- On-Trade: This includes restaurants, hotels, and catering services. While significant for consumption volume, its market share is generally smaller than the off-trade segment, but it plays a vital role in the demand for specific types of poultry, particularly processed and premium cuts.

Key Drivers of Dominance:

- Economic Policies: Government support for the poultry sector, trade agreements, and investment in infrastructure.

- Infrastructure Development: Growth of cold chain logistics, modern retail outlets, and e-commerce platforms.

- Consumer Demographics: Large and growing populations, urbanization, and increasing disposable incomes.

- Cultural Preferences: Poultry as a preferred protein source across many Asian cultures.

Asia Pacific Poultry Industry Product Developments

Product innovation in the Asia Pacific poultry industry is accelerating, focusing on enhanced convenience, improved nutritional profiles, and sustainable production methods. Companies are investing in the development of value-added processed products, such as ready-to-cook marinated chicken, gourmet chicken sausages, and plant-based poultry alternatives, catering to the growing demand for convenient and healthy meal solutions. Technological advancements in processing, including advanced cooking and preservation techniques, are enabling the creation of products with longer shelf lives and superior textures. Furthermore, there's a notable trend towards developing specialized poultry products, such as antibiotic-free or free-range chicken, appealing to health-conscious consumers. Competitive advantages are being carved out through unique flavor profiles, innovative packaging, and transparent sourcing information, building consumer trust and market differentiation.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Asia Pacific poultry industry, covering a study period from 2019 to 2033, with a base and estimated year of 2025, and a forecast period from 2025 to 2033. The historical period spans from 2019 to 2024. The market is segmented by Product Type and Distribution Channel.

Product Type:

- Table Eggs: This segment includes various types of eggs consumed directly, with growth projections driven by steady demand and nutritional value. Market size is significant, with competitive dynamics shaped by local production capabilities and price sensitivity.

- Chicken Meat: This forms the largest segment and is further divided into Fresh / Chilled, Frozen / Canned, and Processed. Fresh/chilled meat is expected to see robust growth due to modern retail expansion. Frozen/canned meat offers scalability and affordability. Processed chicken meat is projected for high growth due to convenience trends.

Distribution Channel:

- On-Trade: Encompassing hotels, restaurants, and catering services, this segment's growth is tied to the hospitality sector's performance.

- Off-Trade: This is the dominant channel, comprising Supermarkets/Hypermarkets, Specialty Stores, Online Retail, and Others. Supermarkets/Hypermarkets are expected to maintain strong growth due to convenience and product variety. Online Retail is poised for exponential growth, driven by e-commerce adoption.

Key Drivers of Asia Pacific Poultry Industry Growth

The Asia Pacific poultry industry's growth is propelled by several pivotal factors. A burgeoning population, particularly in emerging economies, directly fuels an increased demand for protein sources like poultry. Rising disposable incomes empower consumers to opt for more diverse and often more expensive protein options. Furthermore, cultural preferences across many Asian nations favor poultry as a primary meat source due to its affordability, versatility, and perceived health benefits compared to red meats. Technological advancements in poultry farming, processing, and logistics are enhancing efficiency, reducing costs, and improving product quality. Government initiatives, including subsidies and favorable trade policies, also play a crucial role in fostering industry expansion and market access.

Challenges in the Asia Pacific Poultry Industry Sector

Despite robust growth prospects, the Asia Pacific poultry industry faces several significant challenges. Stringent and often varied regulatory frameworks across different countries can create complexities in market access and compliance. Avian influenza outbreaks and other disease concerns pose a constant threat to biosecurity, leading to significant economic losses and impacting consumer confidence. Supply chain disruptions, particularly in developing regions with inadequate cold chain infrastructure, can lead to product spoilage and increased costs. Intense price competition, especially in the commodity segments of chicken meat and eggs, can limit profit margins. The growing consumer demand for ethically sourced and sustainably produced poultry also presents a challenge, requiring significant investment in farm management practices and transparency.

Emerging Opportunities in Asia Pacific Poultry Industry

The Asia Pacific poultry industry is brimming with emerging opportunities. The increasing consumer demand for value-added and convenient poultry products, such as ready-to-eat meals and marinated cuts, presents a significant avenue for growth. The expansion of online retail and direct-to-consumer sales models offers new channels for market penetration and brand building. Innovations in alternative protein, including cultured meat, while still nascent, represent a long-term opportunity for diversification and meeting evolving consumer preferences. Furthermore, the growing focus on sustainable and antibiotic-free poultry production creates a niche market for premium products, allowing companies to command higher prices. Investing in improved cold chain infrastructure and advanced processing technologies can unlock significant potential in previously underserved markets.

Leading Players in the Asia Pacific Poultry Industry Market

- Suguna Foods

- Charoen Pokphand Group

- NH Foods Ltd

- Doyoo Group

- Tyson Foods Inc

- VH Group

- New Hope Liuhe

- Cargill Inc

- Wen's Food Group

- Sunner Development Co

Key Developments in Asia Pacific Poultry Industry Industry

- October 2022: Vow, an Australian cultured meat start-up, opened Factory 1, a facility capable of producing 30 tonnes of cultured meat annually, making it the largest of its kind in the Southern Hemisphere. Plans for Factory 2 are progressing, with the initial stage of production slated for the second half of FY24, envisioned to be approximately 100 times the scale of Factory 1.

- October 2022: Tyson launched its namesake processed meat products in Malaysia, introducing seven halal-certified products including chicken nuggets, classic fried chicken, BBQ roasted chicken drumsticks, chicken kara-age, crispy chicken stripes, and grilled tender chicken.

- September 2022: Tyson Foods introduced fully-cooked frozen chicken products in Malaysia, utilizing their signature triple coating technology for maximum crunch and a vacuum marination method for tender, juicy bites.

Strategic Outlook for Asia Pacific Poultry Industry Market

The strategic outlook for the Asia Pacific poultry industry is exceptionally promising, driven by sustained growth catalysts. The increasing demand for affordable and high-quality protein, coupled with a rapidly expanding middle class, will continue to be a primary growth engine. Innovation in product development, focusing on convenience, health, and sustainability, will be key to capturing market share and commanding premium pricing. Strategic investments in advanced processing technologies and efficient cold chain logistics will be crucial for operational excellence and market expansion. Furthermore, the burgeoning e-commerce landscape presents a significant opportunity for direct consumer engagement and diversified distribution. Companies that adapt to evolving consumer preferences for ethically sourced and environmentally conscious products will likely lead the market. The industry is poised for continued expansion, with significant potential for both consolidation among major players and growth for specialized niche providers.

Asia Pacific Poultry Industry Segmentation

-

1. Product Type

- 1.1. Table Eggs

-

1.2. Chicken Meat

- 1.2.1. Fresh / Chilled

- 1.2.2. Frozen / Canned

- 1.2.3. Processed

-

2. Distribution Channel

- 2.1. On-Trade

-

2.2. Off-Trade

- 2.2.1. Supermarkets/Hypermarkets

- 2.2.2. Specialty Stores

- 2.2.3. Online Retail

- 2.2.4. Others

Asia Pacific Poultry Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

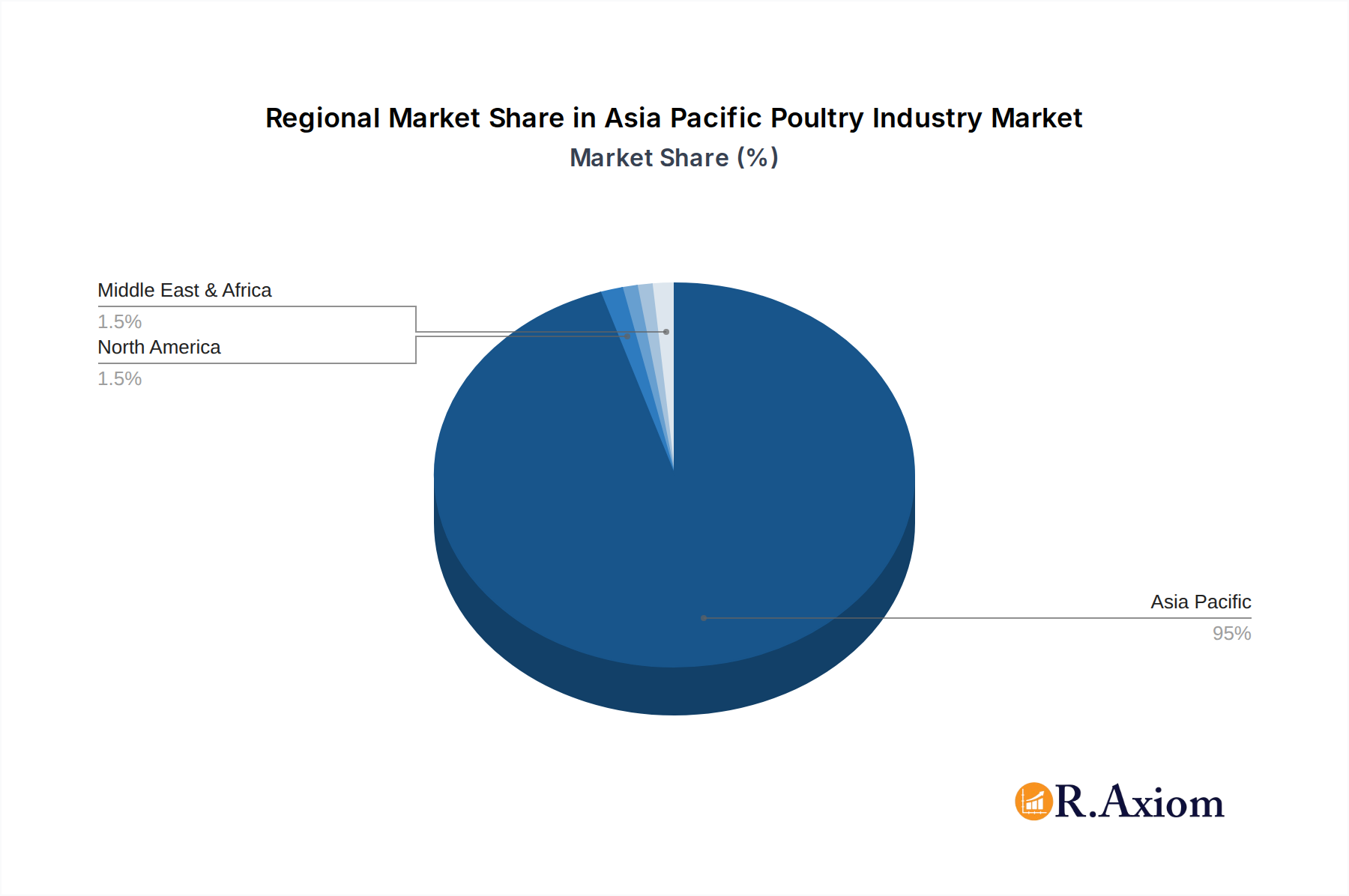

Asia Pacific Poultry Industry Regional Market Share

Geographic Coverage of Asia Pacific Poultry Industry

Asia Pacific Poultry Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Table Eggs

- 5.1.2. Chicken Meat

- 5.1.2.1. Fresh / Chilled

- 5.1.2.2. Frozen / Canned

- 5.1.2.3. Processed

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-Trade

- 5.2.2. Off-Trade

- 5.2.2.1. Supermarkets/Hypermarkets

- 5.2.2.2. Specialty Stores

- 5.2.2.3. Online Retail

- 5.2.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Asia Pacific Poultry Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Table Eggs

- 6.1.2. Chicken Meat

- 6.1.2.1. Fresh / Chilled

- 6.1.2.2. Frozen / Canned

- 6.1.2.3. Processed

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On-Trade

- 6.2.2. Off-Trade

- 6.2.2.1. Supermarkets/Hypermarkets

- 6.2.2.2. Specialty Stores

- 6.2.2.3. Online Retail

- 6.2.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Suguna Foods

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Charoen Pokphand Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 NH Foods Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Doyoo Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Tyson Foods Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 VH Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 New Hope Liuhe

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cargill Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Wen's Food Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sunner Development Co*List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Suguna Foods

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Poultry Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Poultry Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Poultry Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Asia Pacific Poultry Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: Asia Pacific Poultry Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Asia Pacific Poultry Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: Asia Pacific Poultry Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Asia Pacific Poultry Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Asia Pacific Poultry Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Asia Pacific Poultry Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 9: Asia Pacific Poultry Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Asia Pacific Poultry Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 11: Asia Pacific Poultry Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Asia Pacific Poultry Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: China Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: China Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: Japan Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Japan Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: South Korea Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: South Korea Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: India Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: India Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Australia Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Australia Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: New Zealand Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: New Zealand Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Indonesia Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Indonesia Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Malaysia Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Malaysia Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Singapore Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Singapore Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Thailand Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Thailand Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 33: Vietnam Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Vietnam Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 35: Philippines Asia Pacific Poultry Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Philippines Asia Pacific Poultry Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Poultry Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Asia Pacific Poultry Industry?

Key companies in the market include Suguna Foods, Charoen Pokphand Group, NH Foods Ltd, Doyoo Group, Tyson Foods Inc, VH Group, New Hope Liuhe, Cargill Inc, Wen's Food Group, Sunner Development Co*List Not Exhaustive.

3. What are the main segments of the Asia Pacific Poultry Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 394.75 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Protein-Rich Food; Increasing Demand for Plant-Based and Organic Ingredients.

6. What are the notable trends driving market growth?

Increasing Demand for Poultry Products.

7. Are there any restraints impacting market growth?

Presence of Alternative Proteins.

8. Can you provide examples of recent developments in the market?

In October 2022, Vow, an Australian cultured meat start-up opened the first of two planned cultured meat facilities. The facility, Factory 1, can produce 30 tonnes of cultured meat a year, making it the largest plant in the Southern Hemisphere. Plans for Factory 2 were advanced, with the first stage of production scheduled for 2H FY24. It would be roughly 100 times the scale of Factory 1.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Poultry Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Poultry Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Poultry Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Poultry Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence