Key Insights

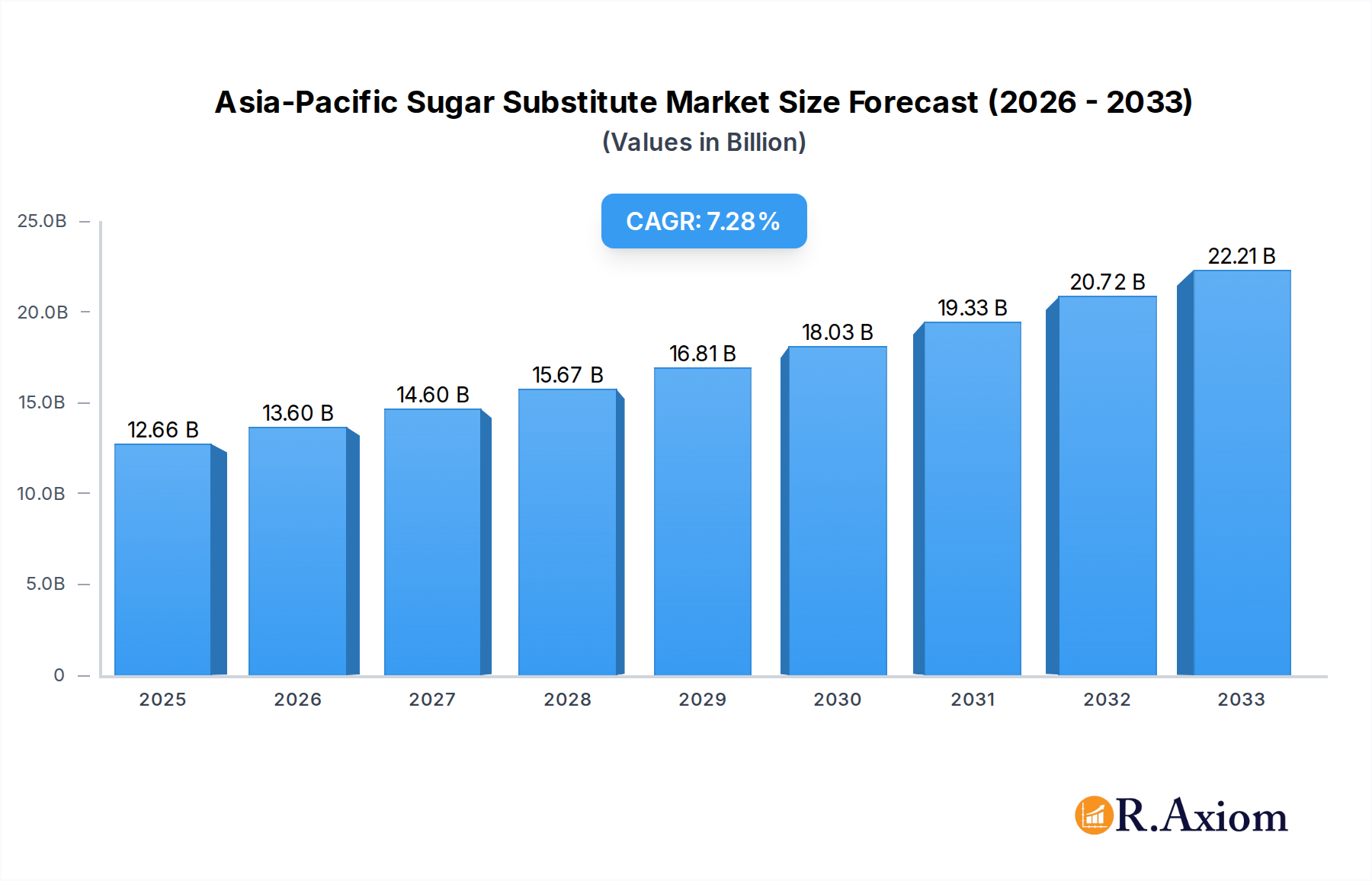

The Asia-Pacific Sugar Substitute Market is poised for significant expansion, projected to reach USD 12.66 billion in 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of 7.3% through 2033. This burgeoning market is primarily driven by a confluence of factors including increasing health consciousness among consumers, a rising prevalence of lifestyle diseases like diabetes and obesity, and a growing demand for reduced-calorie food and beverage options. Government initiatives promoting healthier lifestyles and stricter regulations on sugar content in food products further bolster market growth. The demand for both high-intensity and low-intensity sweeteners is expected to rise, catering to diverse consumer preferences and application needs across the food, beverage, pharmaceutical, and dietary supplement industries. Innovations in natural sweeteners and cleaner labeling are also playing a crucial role in shaping consumer choices and driving market penetration.

Asia-Pacific Sugar Substitute Market Market Size (In Billion)

Key trends fueling this growth include the escalating demand for natural and plant-based sugar alternatives like Stevia, alongside continued innovation in synthetic sweeteners offering improved taste profiles and cost-effectiveness. The market is witnessing a surge in product launches tailored for specific applications, from bakery and confectionery to beverages and dairy. While the market is largely optimistic, potential restraints such as fluctuating raw material prices, stringent regulatory approvals for new ingredients, and consumer perception regarding the safety and origin of certain artificial sweeteners could pose challenges. Nevertheless, the immense potential in emerging economies within the Asia-Pacific region, coupled with a growing middle class and increasing disposable incomes, positions this market for sustained and dynamic growth.

Asia-Pacific Sugar Substitute Market Company Market Share

Asia-Pacific Sugar Substitute Market Report Description

Unlock the immense potential of the Asia-Pacific sugar substitute market with our comprehensive, data-driven report. This in-depth analysis provides critical insights into market dynamics, growth trajectories, and competitive landscapes, empowering stakeholders to make informed strategic decisions. The Asia-Pacific sugar substitute market is projected to reach $15.7 billion by 2033, exhibiting a robust CAGR of 6.8% from 2025 to 2033, driven by escalating health consciousness, favorable government initiatives, and an expanding food and beverage industry.

This report meticulously examines market segmentation by product type, application, and geography, offering granular data on market sizes and growth forecasts. We delve into the evolving consumer preferences for healthier food options, the increasing prevalence of lifestyle diseases like diabetes, and the growing demand for natural and low-calorie sweeteners.

Key companies profiled include: Cargill Incorporated, DuPont de Nemours Inc, Archer Daniels Midland Company, Tate & Lyle PLC, Roquette Freres, Ajinomoto Inc, PureCircle, Ingredion Incorporated.

This report is an indispensable resource for:

- Manufacturers seeking to expand their product portfolios.

- Suppliers aiming to identify new market opportunities.

- Investors looking to capitalize on emerging trends.

- Researchers and analysts tracking the sugar substitute industry.

Study Period: 2019–2033 | Base Year: 2025 | Estimated Year: 2025 | Forecast Period: 2025–2033 | Historical Period: 2019–2024

Asia-Pacific Sugar Substitute Market Market Concentration & Innovation

The Asia-Pacific sugar substitute market is characterized by a moderate to high level of concentration, with a few major global players holding significant market share. However, the landscape is increasingly dynamic due to continuous innovation and the emergence of regional manufacturers. Innovation drivers are primarily centered around developing natural, plant-based sweeteners like stevia and monk fruit, catering to the growing consumer demand for clean labels and perceived health benefits. Furthermore, advancements in extraction and processing technologies are enhancing the taste profiles and cost-effectiveness of these substitutes. Regulatory frameworks across different Asia-Pacific countries vary, impacting the adoption and approval of various sugar substitutes. For instance, stringent regulations in some nations may slow down the introduction of new ingredients, while others are more progressive in their approval processes. The threat of product substitutes, including natural sweeteners not yet widely commercialized and evolving consumer dietary habits, poses a challenge. End-user trends highlight a shift towards reduced sugar intake across all demographics, with a particular focus on children's products and functional foods. Mergers and acquisitions (M&A) activities are strategically important for market consolidation and expansion. For example, acquisitions of smaller, innovative companies by larger players aim to secure intellectual property and market access. The total M&A deal value in the broader global sugar substitute market has seen significant investment, with projections indicating continued strategic moves within the Asia-Pacific region, potentially reaching several hundred million US dollars in key transactions over the forecast period.

Asia-Pacific Sugar Substitute Market Industry Trends & Insights

The Asia-Pacific sugar substitute market is poised for substantial growth, driven by a confluence of escalating health consciousness and an expanding food and beverage sector. Consumers across the region are increasingly aware of the detrimental health effects of excessive sugar consumption, leading to a significant shift in dietary preferences towards low-calorie and natural alternatives. This heightened health awareness is a primary catalyst for market expansion, as individuals actively seek sugar-free or reduced-sugar options in their daily diets. The market penetration of sugar substitutes is rapidly increasing, especially in emerging economies within Asia-Pacific where urbanization and disposable incomes are on the rise, facilitating greater access to processed foods and beverages that often incorporate these ingredients. The overall market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 6.8% during the forecast period of 2025-2033, underscoring its robust expansion trajectory. Technological disruptions are playing a pivotal role, with continuous advancements in the production and refinement of both natural and artificial sweeteners. Innovations in biotechnology and sustainable sourcing are improving the cost-effectiveness, taste, and functionality of sugar substitutes, making them more attractive to manufacturers. For instance, advancements in stevia extraction and purification have led to improved taste profiles, reducing the bitter aftertaste often associated with early iterations. Consumer preferences are evolving beyond simply reducing sugar; there is a growing demand for sweeteners that are perceived as natural, organic, and derived from sustainable sources. This trend is particularly evident in countries like Japan and Australia, where consumers are highly discerning about ingredient origins and health impacts. Competitive dynamics within the market are intensifying, with both established global players and emerging local manufacturers vying for market share. Strategic partnerships, product diversification, and aggressive marketing campaigns are key strategies employed by companies to gain a competitive edge. The influx of innovative product formulations and the increasing adoption of sugar substitutes in diverse applications, from beverages and dairy products to confectionery and pharmaceuticals, are further fueling market growth. The growing prevalence of diabetes and other lifestyle-related diseases across the Asia-Pacific region further amplifies the demand for sugar substitutes as a means to manage blood sugar levels and promote healthier lifestyles. This demographic shift presents a significant long-term growth opportunity for the sugar substitute industry.

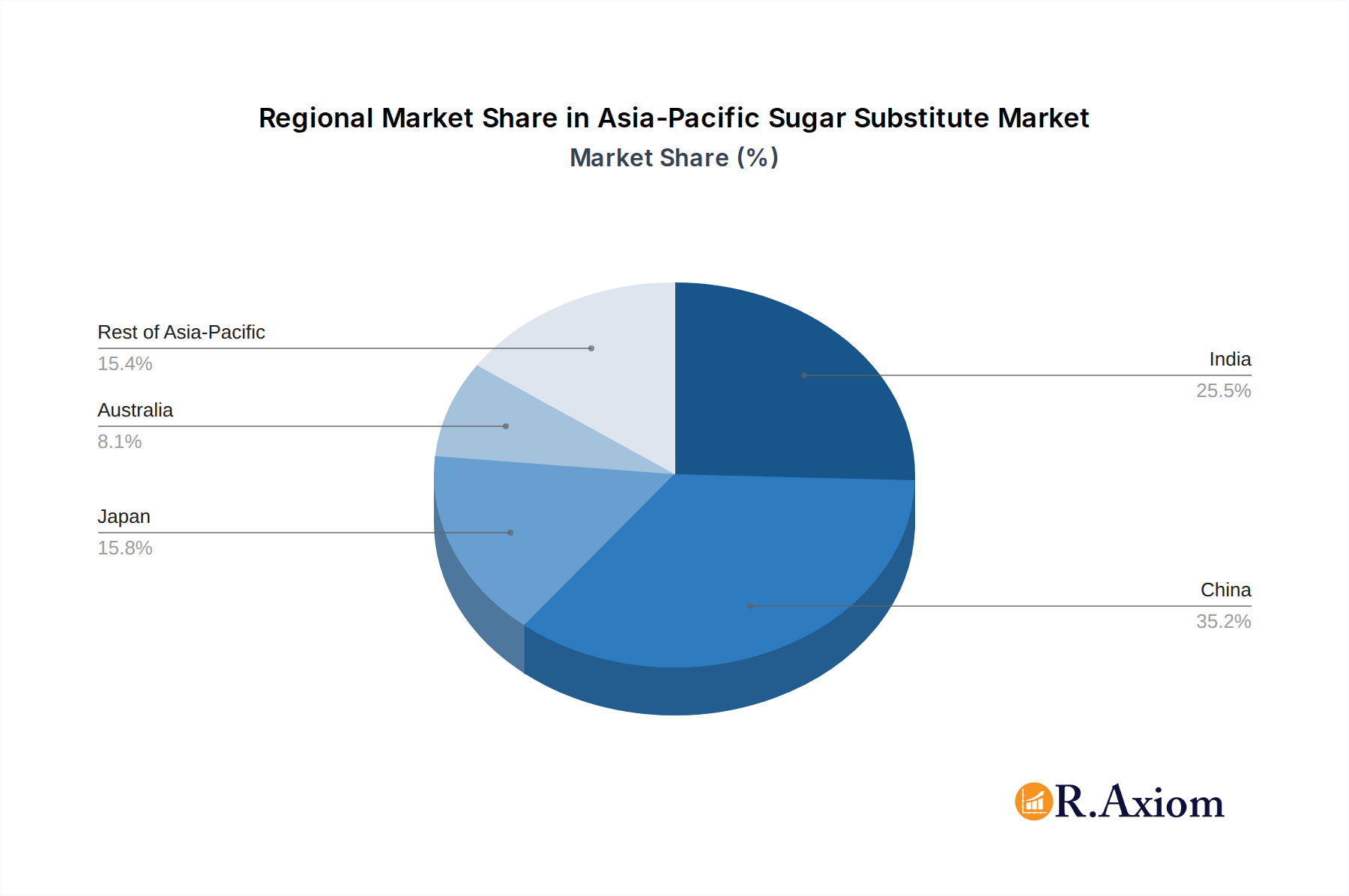

Dominant Markets & Segments in Asia-Pacific Sugar Substitute Market

China stands out as the dominant market within the Asia-Pacific sugar substitute landscape, driven by its massive population, rapidly expanding middle class, and a burgeoning food and beverage industry that is increasingly embracing healthier ingredient alternatives. The Chinese government's focus on public health initiatives and the growing awareness among consumers regarding the impact of sugar on health are significant growth drivers. Economic policies that support the food processing sector and investments in research and development for food ingredients further solidify China's leading position.

Product Type Dominance:

- High-Intensity Sweeteners (HIS) represent the most dominant segment in terms of market value and volume. Within HIS:

- Stevia is experiencing exceptional growth due to its natural origin and zero-calorie profile, making it a preferred choice for health-conscious consumers. Favorable agricultural conditions and increasing cultivation efforts in several Asian countries are contributing to its widespread availability and cost competitiveness. The market penetration of stevia is rapidly increasing across bakery, confectionery, and beverage applications.

- Sucralose also holds a significant market share due to its stability, intense sweetness, and wide application range. Its ability to withstand high temperatures makes it ideal for baked goods and processed foods.

- Low-Intensity Sweeteners (LIS), while smaller in market share compared to HIS, are also witnessing steady growth.

- Xylitol is gaining traction due to its oral health benefits and lower glycemic index, finding applications in confectionery, chewing gum, and toothpaste.

- Sorbitol and Maltitol are crucial for sugar-free confectionery and diabetic-friendly products.

Application Dominance:

- Food and Beverage is the largest application segment by a substantial margin, accounting for the lion's share of the market. Within this segment:

- Beverages (including carbonated drinks, fruit juices, and ready-to-drink teas) are the primary consumers of sugar substitutes, driven by the global trend towards reduced-sugar beverages.

- Confectionery and Bakery products follow closely, as manufacturers reformulate to offer healthier options to cater to consumer demand for guilt-free indulgence.

- Dairy products, such as yogurts and ice creams, are also increasingly incorporating sugar substitutes.

- Dietary Supplements and Pharmaceuticals represent niche but growing segments, where sugar substitutes are used for palatability enhancement and in sugar-free formulations.

Geographical Dominance:

- China is the undisputed leader in the Asia-Pacific sugar substitute market, driven by its large consumer base, growing disposable incomes, and increasing health awareness. The country's robust food processing industry and government support for healthier food options contribute significantly to its dominance.

- India is emerging as a significant growth market, fueled by a large diabetic population and increasing consumer demand for sugar-free products. Government initiatives promoting health and wellness are also playing a crucial role.

- Japan exhibits a mature market with a high consumer preference for natural and functional ingredients, leading to strong demand for stevia and other high-quality sugar substitutes.

Asia-Pacific Sugar Substitute Market Product Developments

Product development in the Asia-Pacific sugar substitute market is primarily focused on enhancing natural alternatives, improving taste profiles, and expanding applications. Innovations in stevia processing are yielding refined extracts with superior sweetness and reduced off-notes, making them highly competitive with artificial sweeteners. Companies are also investing in the research and development of new natural sweeteners derived from fruits and traditional botanicals, aiming to capture the growing demand for clean-label products. Competitive advantages are being gained through proprietary extraction technologies, sustainable sourcing practices, and the development of synergistic sweetener blends that offer optimal taste and functionality. The market fit is improving as these advancements address consumer concerns about health, naturalness, and ingredient transparency, driving wider adoption across food, beverage, and pharmaceutical sectors.

Report Scope & Segmentation Analysis

This comprehensive report offers an in-depth analysis of the Asia-Pacific sugar substitute market, meticulously segmented to provide actionable insights. The Product Type segmentation covers High-Intensity Sweeteners (Stevia, Aspartame, Cyclamate, Sucralose, Other High Intensity Sweeteners) and Low-Intensity Sweeteners (Sorbitol, Maltitol, Xylitol, Other Low Intensity Sweeteners), along with High Fructose Syrup. Growth projections for these categories highlight the accelerating demand for natural and calorie-free options, particularly for stevia and sucralose.

The Application segmentation breaks down the market into Food and Beverage (Bakery, Confectionery, Dairy, Beverages, Meat and Seafood, Other Food and Beverages), Dietary Supplements, and Pharmaceuticals. The Food and Beverage segment is expected to maintain its dominance, with beverages and confectionery leading the growth trajectory due to consumer-driven demand for healthier indulgence.

Geographically, the report analyzes the market across India, China, Japan, Australia, and the Rest of Asia-Pacific. China is anticipated to continue its market leadership, driven by its vast population and evolving consumer preferences. India and other emerging economies are projected to witness significant growth, fueled by increasing health awareness and rising disposable incomes, presenting considerable market opportunities.

Key Drivers of Asia-Pacific Sugar Substitute Market Growth

The Asia-Pacific sugar substitute market is propelled by several critical drivers. Foremost among these is the escalating global health consciousness, leading to a significant shift in consumer preferences towards reduced sugar intake and healthier dietary options. This trend is further amplified by the rising prevalence of lifestyle diseases such as diabetes, obesity, and cardiovascular conditions, creating a strong demand for sugar alternatives. Government initiatives and public health campaigns promoting healthier eating habits and stricter regulations on sugar content in food products also play a crucial role in market expansion. Technological advancements in the extraction, purification, and formulation of sugar substitutes, particularly natural sweeteners like stevia, have improved their taste profiles, cost-effectiveness, and functionality, making them more viable alternatives for manufacturers. The expanding middle class in many Asia-Pacific countries, coupled with increasing disposable incomes, allows consumers to opt for premium and healthier food and beverage products, further stimulating market growth.

Challenges in the Asia-Pacific Sugar Substitute Market Sector

Despite its robust growth, the Asia-Pacific sugar substitute market faces several challenges. Regulatory hurdles and varying approval processes across different countries can lead to delays in product launches and market penetration. Consumer perceptions regarding the safety and naturalness of certain artificial sweeteners can create resistance, impacting adoption rates. The cost of production for some natural sweeteners, while decreasing, can still be higher than that of traditional sugar, posing a barrier for price-sensitive markets. Supply chain complexities, particularly for agricultural-based sweeteners, and the potential for price volatility due to factors like weather conditions or geopolitical events, can disrupt availability and impact profitability. Furthermore, intense competition among a growing number of players, including both established global corporations and local manufacturers, puts pressure on profit margins and necessitates continuous innovation.

Emerging Opportunities in Asia-Pacific Sugar Substitute Market

The Asia-Pacific sugar substitute market presents numerous emerging opportunities. The burgeoning demand for natural and plant-based sweeteners, such as stevia, monk fruit, and erythritol, offers significant growth potential. Innovations in developing novel low-calorie sweeteners with improved taste and functional properties are opening new avenues. The expanding pharmaceutical and nutraceutical sectors are increasingly incorporating sugar substitutes into their formulations for healthier products, creating a substantial market for specialized sweeteners. Untapped rural markets in developing Asia-Pacific economies represent a significant opportunity for market expansion as awareness about health and wellness grows. Furthermore, the trend towards clean-label products and increasing consumer interest in sustainable sourcing practices create opportunities for companies focusing on transparent and ethical production methods. The development of sugar substitutes specifically tailored for different cuisines and local dietary habits can also unlock new market niches.

Leading Players in the Asia-Pacific Sugar Substitute Market Market

- Cargill Incorporated

- DuPont de Nemours Inc

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Roquette Freres

- Ajinomoto Inc

- PureCircle

- Ingredion Incorporated

Key Developments in Asia-Pacific Sugar Substitute Market Industry

- 2023/11: Tate & Lyle PLC expands its stevia portfolio with a new formulation for beverages, enhancing taste and sweetness profiles.

- 2023/09: Ingredion Incorporated announces significant investment in expanding its stevia production capacity in Asia to meet growing regional demand.

- 2023/07: Roquette Freres launches a new range of plant-based sweeteners derived from fermentation, targeting the clean-label market in Asia.

- 2023/05: PureCircle strengthens its strategic partnerships with major beverage manufacturers in China to accelerate the adoption of stevia-based sweeteners.

- 2023/03: Archer Daniels Midland Company introduces a cost-effective sucralose solution for bakery applications, aiming to capture a larger market share.

- 2022/12: Cargill Incorporated invests in research to develop next-generation stevia cultivars with improved yield and reduced bitterness for the Asian market.

- 2022/10: DuPont de Nemours Inc receives regulatory approval for a new high-intensity sweetener in several key Asian countries, broadening its market reach.

Strategic Outlook for Asia-Pacific Sugar Substitute Market Market

The strategic outlook for the Asia-Pacific sugar substitute market is overwhelmingly positive, characterized by sustained growth driven by macro trends in health and wellness. Key growth catalysts include the burgeoning demand for natural ingredients, particularly stevia and other plant-based alternatives, which aligns with evolving consumer preferences for clean labels and perceived health benefits. Continued innovation in taste enhancement and cost reduction for these natural sweeteners will be crucial for wider market adoption. Furthermore, the increasing focus on preventative healthcare and the management of chronic diseases like diabetes will continue to fuel demand across the food, beverage, pharmaceutical, and nutraceutical sectors. Strategic partnerships, mergers, and acquisitions will likely play a significant role in market consolidation and the expansion of market players into emerging economies. Investments in R&D for novel sweetener technologies and sustainable sourcing practices will be vital for maintaining a competitive edge. The market is well-positioned to capitalize on the growing disposable incomes and urbanization across the region, further solidifying its promising future.

Asia-Pacific Sugar Substitute Market Segmentation

-

1. Product Type

-

1.1. High-Intensity Sweeteners

- 1.1.1. Stevia

- 1.1.2. Aspartame

- 1.1.3. Cyclamate

- 1.1.4. Sucralose

- 1.1.5. Other High Intensity Sweeteners

-

1.2. Low-Intensity Sweeteners

- 1.2.1. Sorbitol

- 1.2.2. Maltitol

- 1.2.3. Xylitol

- 1.2.4. Other Low Intensity Sweeteners

- 1.3. High Fructose Syrup

-

1.1. High-Intensity Sweeteners

-

2. Application

-

2.1. Food and Beverage

- 2.1.1. Bakery

- 2.1.2. Confectionery

- 2.1.3. Dairy

- 2.1.4. Beverages

- 2.1.5. Meat and Seafood

- 2.1.6. Other Food and Beverages

- 2.2. Dietary Supplements

- 2.3. Pharmaceuticals

-

2.1. Food and Beverage

-

3. Geography

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia-Pacific

Asia-Pacific Sugar Substitute Market Segmentation By Geography

- 1. India

- 2. China

- 3. Japan

- 4. Australia

- 5. Rest of Asia Pacific

Asia-Pacific Sugar Substitute Market Regional Market Share

Geographic Coverage of Asia-Pacific Sugar Substitute Market

Asia-Pacific Sugar Substitute Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. High-Intensity Sweeteners

- 5.1.1.1. Stevia

- 5.1.1.2. Aspartame

- 5.1.1.3. Cyclamate

- 5.1.1.4. Sucralose

- 5.1.1.5. Other High Intensity Sweeteners

- 5.1.2. Low-Intensity Sweeteners

- 5.1.2.1. Sorbitol

- 5.1.2.2. Maltitol

- 5.1.2.3. Xylitol

- 5.1.2.4. Other Low Intensity Sweeteners

- 5.1.3. High Fructose Syrup

- 5.1.1. High-Intensity Sweeteners

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Food and Beverage

- 5.2.1.1. Bakery

- 5.2.1.2. Confectionery

- 5.2.1.3. Dairy

- 5.2.1.4. Beverages

- 5.2.1.5. Meat and Seafood

- 5.2.1.6. Other Food and Beverages

- 5.2.2. Dietary Supplements

- 5.2.3. Pharmaceuticals

- 5.2.1. Food and Beverage

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. India

- 5.3.2. China

- 5.3.3. Japan

- 5.3.4. Australia

- 5.3.5. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.4.2. China

- 5.4.3. Japan

- 5.4.4. Australia

- 5.4.5. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Asia-Pacific Sugar Substitute Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. High-Intensity Sweeteners

- 6.1.1.1. Stevia

- 6.1.1.2. Aspartame

- 6.1.1.3. Cyclamate

- 6.1.1.4. Sucralose

- 6.1.1.5. Other High Intensity Sweeteners

- 6.1.2. Low-Intensity Sweeteners

- 6.1.2.1. Sorbitol

- 6.1.2.2. Maltitol

- 6.1.2.3. Xylitol

- 6.1.2.4. Other Low Intensity Sweeteners

- 6.1.3. High Fructose Syrup

- 6.1.1. High-Intensity Sweeteners

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Food and Beverage

- 6.2.1.1. Bakery

- 6.2.1.2. Confectionery

- 6.2.1.3. Dairy

- 6.2.1.4. Beverages

- 6.2.1.5. Meat and Seafood

- 6.2.1.6. Other Food and Beverages

- 6.2.2. Dietary Supplements

- 6.2.3. Pharmaceuticals

- 6.2.1. Food and Beverage

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. India

- 6.3.2. China

- 6.3.3. Japan

- 6.3.4. Australia

- 6.3.5. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. India Asia-Pacific Sugar Substitute Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. High-Intensity Sweeteners

- 7.1.1.1. Stevia

- 7.1.1.2. Aspartame

- 7.1.1.3. Cyclamate

- 7.1.1.4. Sucralose

- 7.1.1.5. Other High Intensity Sweeteners

- 7.1.2. Low-Intensity Sweeteners

- 7.1.2.1. Sorbitol

- 7.1.2.2. Maltitol

- 7.1.2.3. Xylitol

- 7.1.2.4. Other Low Intensity Sweeteners

- 7.1.3. High Fructose Syrup

- 7.1.1. High-Intensity Sweeteners

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Food and Beverage

- 7.2.1.1. Bakery

- 7.2.1.2. Confectionery

- 7.2.1.3. Dairy

- 7.2.1.4. Beverages

- 7.2.1.5. Meat and Seafood

- 7.2.1.6. Other Food and Beverages

- 7.2.2. Dietary Supplements

- 7.2.3. Pharmaceuticals

- 7.2.1. Food and Beverage

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. India

- 7.3.2. China

- 7.3.3. Japan

- 7.3.4. Australia

- 7.3.5. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. China Asia-Pacific Sugar Substitute Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. High-Intensity Sweeteners

- 8.1.1.1. Stevia

- 8.1.1.2. Aspartame

- 8.1.1.3. Cyclamate

- 8.1.1.4. Sucralose

- 8.1.1.5. Other High Intensity Sweeteners

- 8.1.2. Low-Intensity Sweeteners

- 8.1.2.1. Sorbitol

- 8.1.2.2. Maltitol

- 8.1.2.3. Xylitol

- 8.1.2.4. Other Low Intensity Sweeteners

- 8.1.3. High Fructose Syrup

- 8.1.1. High-Intensity Sweeteners

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Food and Beverage

- 8.2.1.1. Bakery

- 8.2.1.2. Confectionery

- 8.2.1.3. Dairy

- 8.2.1.4. Beverages

- 8.2.1.5. Meat and Seafood

- 8.2.1.6. Other Food and Beverages

- 8.2.2. Dietary Supplements

- 8.2.3. Pharmaceuticals

- 8.2.1. Food and Beverage

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. India

- 8.3.2. China

- 8.3.3. Japan

- 8.3.4. Australia

- 8.3.5. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Japan Asia-Pacific Sugar Substitute Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. High-Intensity Sweeteners

- 9.1.1.1. Stevia

- 9.1.1.2. Aspartame

- 9.1.1.3. Cyclamate

- 9.1.1.4. Sucralose

- 9.1.1.5. Other High Intensity Sweeteners

- 9.1.2. Low-Intensity Sweeteners

- 9.1.2.1. Sorbitol

- 9.1.2.2. Maltitol

- 9.1.2.3. Xylitol

- 9.1.2.4. Other Low Intensity Sweeteners

- 9.1.3. High Fructose Syrup

- 9.1.1. High-Intensity Sweeteners

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Food and Beverage

- 9.2.1.1. Bakery

- 9.2.1.2. Confectionery

- 9.2.1.3. Dairy

- 9.2.1.4. Beverages

- 9.2.1.5. Meat and Seafood

- 9.2.1.6. Other Food and Beverages

- 9.2.2. Dietary Supplements

- 9.2.3. Pharmaceuticals

- 9.2.1. Food and Beverage

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. India

- 9.3.2. China

- 9.3.3. Japan

- 9.3.4. Australia

- 9.3.5. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Australia Asia-Pacific Sugar Substitute Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. High-Intensity Sweeteners

- 10.1.1.1. Stevia

- 10.1.1.2. Aspartame

- 10.1.1.3. Cyclamate

- 10.1.1.4. Sucralose

- 10.1.1.5. Other High Intensity Sweeteners

- 10.1.2. Low-Intensity Sweeteners

- 10.1.2.1. Sorbitol

- 10.1.2.2. Maltitol

- 10.1.2.3. Xylitol

- 10.1.2.4. Other Low Intensity Sweeteners

- 10.1.3. High Fructose Syrup

- 10.1.1. High-Intensity Sweeteners

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Food and Beverage

- 10.2.1.1. Bakery

- 10.2.1.2. Confectionery

- 10.2.1.3. Dairy

- 10.2.1.4. Beverages

- 10.2.1.5. Meat and Seafood

- 10.2.1.6. Other Food and Beverages

- 10.2.2. Dietary Supplements

- 10.2.3. Pharmaceuticals

- 10.2.1. Food and Beverage

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. India

- 10.3.2. China

- 10.3.3. Japan

- 10.3.4. Australia

- 10.3.5. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Rest of Asia Pacific Asia-Pacific Sugar Substitute Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. High-Intensity Sweeteners

- 11.1.1.1. Stevia

- 11.1.1.2. Aspartame

- 11.1.1.3. Cyclamate

- 11.1.1.4. Sucralose

- 11.1.1.5. Other High Intensity Sweeteners

- 11.1.2. Low-Intensity Sweeteners

- 11.1.2.1. Sorbitol

- 11.1.2.2. Maltitol

- 11.1.2.3. Xylitol

- 11.1.2.4. Other Low Intensity Sweeteners

- 11.1.3. High Fructose Syrup

- 11.1.1. High-Intensity Sweeteners

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Food and Beverage

- 11.2.1.1. Bakery

- 11.2.1.2. Confectionery

- 11.2.1.3. Dairy

- 11.2.1.4. Beverages

- 11.2.1.5. Meat and Seafood

- 11.2.1.6. Other Food and Beverages

- 11.2.2. Dietary Supplements

- 11.2.3. Pharmaceuticals

- 11.2.1. Food and Beverage

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. India

- 11.3.2. China

- 11.3.3. Japan

- 11.3.4. Australia

- 11.3.5. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Cargill Incorporated

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 DuPont de Nemours Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Archer Daniels Midland Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Tate & Lyle PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Roquette Freres*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Ajinomoto Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 PureCircle

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Ingredion Incorporated

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Cargill Incorporated

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Sugar Substitute Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Sugar Substitute Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 10: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 18: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 22: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: Asia-Pacific Sugar Substitute Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Sugar Substitute Market?

The projected CAGR is approximately 8.98%.

2. Which companies are prominent players in the Asia-Pacific Sugar Substitute Market?

Key companies in the market include Cargill Incorporated, DuPont de Nemours Inc, Archer Daniels Midland Company, Tate & Lyle PLC, Roquette Freres*List Not Exhaustive, Ajinomoto Inc, PureCircle, Ingredion Incorporated.

3. What are the main segments of the Asia-Pacific Sugar Substitute Market?

The market segments include Product Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Low-Fat and Low-Calorie Food; Increasing Product Innovation.

6. What are the notable trends driving market growth?

Stevia Held the Largest Market Share.

7. Are there any restraints impacting market growth?

; Threat of New Entrants; Bargaining Power of Buyers/Consumers; Bargaining Power of Suppliers; Threat of Substitute Products; Degree Of Competition.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Sugar Substitute Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Sugar Substitute Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Sugar Substitute Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Sugar Substitute Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence