Key Insights

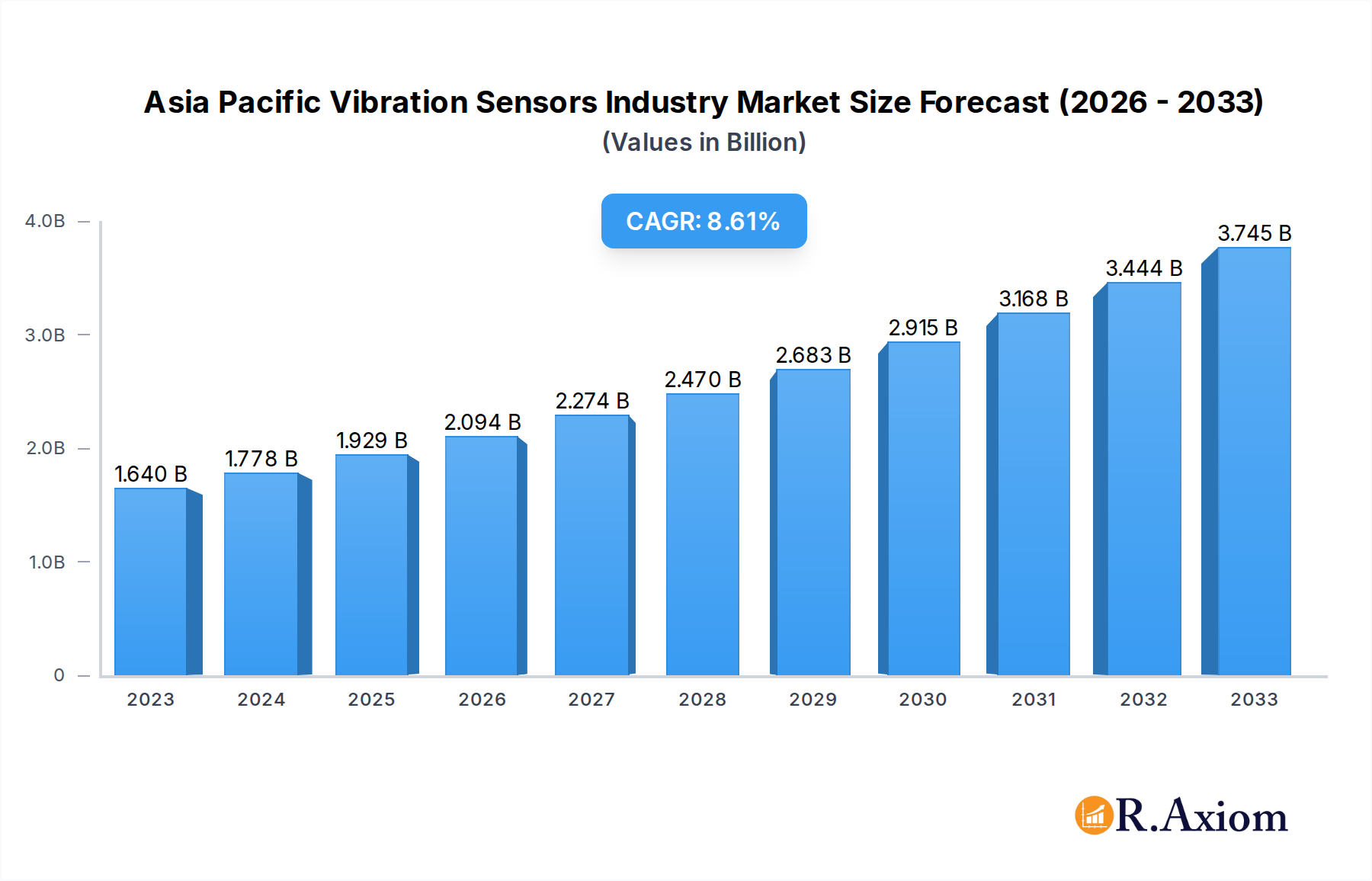

The Asia Pacific vibration sensors market is experiencing robust growth, driven by increasing industrial automation and the adoption of predictive maintenance strategies across diverse sectors. With an estimated market size of $1640 million in 2023 and a projected CAGR of 8.6%, the region is poised for significant expansion. Key product segments like accelerometers and proximity probes are witnessing high demand due to their crucial role in monitoring equipment health and ensuring operational efficiency in industries such as automotive, healthcare, aerospace and defense, and consumer electronics. The burgeoning oil and gas sector, alongside the metals and mining industries, also presents substantial opportunities as companies increasingly invest in advanced monitoring solutions to optimize production and mitigate potential failures. Furthermore, the growing emphasis on smart manufacturing and the proliferation of IoT devices are further fueling the adoption of sophisticated vibration sensing technologies throughout the region.

Asia Pacific Vibration Sensors Industry Market Size (In Billion)

The competitive landscape in the Asia Pacific vibration sensors market is dynamic, with prominent players like Honeywell International Inc., NXP Semiconductors N.V., SKF AB, and Bosch Sensortec GmbH leading innovation and market penetration. These companies are focusing on developing advanced, cost-effective, and integrated vibration sensing solutions to cater to the evolving needs of end-users. The region's robust manufacturing base, coupled with supportive government initiatives for technological advancement and industrial upgrades, provides a fertile ground for market expansion. Emerging economies within Asia Pacific, such as China, India, and Southeast Asian nations, are expected to be key growth engines, driven by rapid industrialization and increasing investments in infrastructure and high-tech manufacturing. The market is also benefiting from the growing integration of vibration sensors with cloud-based analytics platforms, enabling real-time data analysis and proactive decision-making for enhanced asset management and operational uptime.

Asia Pacific Vibration Sensors Industry Company Market Share

Asia Pacific Vibration Sensors Industry Market Concentration & Innovation

The Asia Pacific vibration sensors industry is characterized by a moderately consolidated market, with leading players like Honeywell International Inc., NXP Semiconductors N.V., SKF AB, National Instruments Corporation, Emerson Electric Co., and Bosch Sensortec GmbH (Robert Bosch GmbH) holding significant market share. The estimated market size for vibration sensors in the Asia Pacific region is expected to reach USD 3,500 million by 2025, with a projected CAGR of approximately 7.5% during the forecast period of 2025–2033. Innovation is a key driver, fueled by the increasing demand for advanced diagnostics and predictive maintenance solutions across diverse sectors.

- Market Concentration: The top 5-7 companies are estimated to account for over 60% of the market share.

- Innovation Drivers:

- Advancements in MEMS (Micro-Electro-Mechanical Systems) technology for miniaturized and cost-effective sensors.

- Integration of AI and machine learning for enhanced data analysis and anomaly detection.

- Development of wireless and IoT-enabled vibration monitoring systems.

- Regulatory Frameworks: While generally supportive, specific regional regulations regarding industrial safety and data privacy can influence product development and adoption.

- Product Substitutes: Mechanical condition monitoring techniques and traditional visual inspections represent limited substitutes in high-tech applications but are declining in relevance.

- End-User Trends: Growing adoption of Industry 4.0 initiatives, a focus on operational efficiency, and the need to minimize downtime are paramount.

- M&A Activities: Recent acquisitions, such as TE Connectivity Ltd.'s takeover of First Sensor AG, indicate a trend towards consolidation and portfolio expansion, with deal values in the tens to hundreds of millions of USD.

Asia Pacific Vibration Sensors Industry Industry Trends & Insights

The Asia Pacific vibration sensors industry is poised for robust growth, driven by a confluence of technological advancements, evolving industrial landscapes, and increasing awareness of the benefits of predictive maintenance. The market is projected to expand from an estimated USD 3,200 million in 2024 to over USD 5,500 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period. This growth is underpinned by the rapid industrialization and economic development witnessed across key Asia Pacific nations, including China, Japan, South Korea, and India. The increasing adoption of Industry 4.0 technologies, such as the Internet of Things (IoT), artificial intelligence (AI), and big data analytics, is a significant catalyst, enabling more sophisticated and real-time monitoring of machinery health.

Technological disruptions are at the forefront of this expansion. The continuous miniaturization and cost reduction of MEMS-based accelerometers are making vibration sensing more accessible and affordable for a wider range of applications, from consumer electronics to complex industrial machinery. Furthermore, the development of wireless sensor networks and cloud-based platforms is revolutionizing data collection and analysis. These solutions offer enhanced flexibility, scalability, and remote monitoring capabilities, allowing businesses to gain deeper insights into equipment performance and potential failures without extensive wiring or manual intervention. The demand for high-precision sensors capable of detecting subtle vibrations and anomalies is also on the rise, particularly in critical industries like aerospace, automotive, and healthcare.

Consumer preferences, while less direct in the industrial context, are indirectly influencing the market through the demand for higher quality and more reliable end products. Manufacturers across various sectors are investing in advanced condition monitoring to ensure product durability and performance, thereby reducing warranty claims and enhancing customer satisfaction. This translates into a greater need for sophisticated vibration sensing solutions to validate product quality during manufacturing and throughout their lifecycle.

The competitive dynamics within the Asia Pacific vibration sensors market are intensifying. Established global players are fiercely competing with emerging regional manufacturers, leading to price pressures and an accelerated pace of innovation. Companies are strategically investing in research and development to introduce novel sensor technologies, improve data processing algorithms, and expand their product portfolios to cater to niche applications. Strategic partnerships and acquisitions are also becoming increasingly common as companies seek to leverage complementary technologies and expand their market reach. The overall trend is towards integrated solutions that offer not just data but actionable insights for maintenance optimization and operational efficiency.

Dominant Markets & Segments in Asia Pacific Vibration Sensors Industry

The Asia Pacific vibration sensors industry is experiencing significant growth, with several key segments and regions demonstrating remarkable dominance. The market's trajectory is shaped by a combination of industrial policies, infrastructure development, and the adoption of advanced technologies.

Leading Regions and Countries:

- China stands as the dominant market within the Asia Pacific, fueled by its vast manufacturing base, extensive infrastructure projects, and rapid adoption of Industry 4.0 principles. Government initiatives promoting technological innovation and smart manufacturing have created a fertile ground for vibration sensor deployment across sectors like automotive, industrial automation, and consumer electronics.

- Japan and South Korea are key contributors, distinguished by their advanced technological capabilities and a strong focus on high-value manufacturing, particularly in the automotive, semiconductor, and aerospace sectors. These countries exhibit a mature market for sophisticated vibration sensing solutions.

- India is emerging as a significant growth engine, driven by its expanding industrial sector, government 'Make in India' initiatives, and increasing investments in infrastructure and manufacturing. The oil and gas and metals and mining industries are particularly driving demand.

Dominant Product Segments:

- Accelerometers: This segment holds the largest market share due to their versatility, wide range of applications, and declining costs, especially MEMS-based accelerometers.

- Key Drivers: Ubiquitous use in automotive (e.g., airbag deployment, engine monitoring), consumer electronics (e.g., smartphones, wearables), industrial machinery for condition monitoring, and aerospace for structural integrity.

- Technological Advancements: Miniaturization, improved sensitivity, and integration with wireless communication protocols are further bolstering their dominance.

- Proximity Probes: Crucial for high-speed rotating machinery, particularly in the oil and gas and power generation sectors.

- Key Drivers: Essential for continuous monitoring of shaft vibration and displacement in critical industrial equipment, ensuring operational safety and preventing catastrophic failures.

- Market Penetration: High in industries where asset integrity and uptime are paramount.

- Tachometers: Primarily used for measuring rotational speed, often integrated with vibration analysis systems.

- Key Drivers: Important for machinery diagnostics, performance optimization, and safety systems in industries like automotive, manufacturing, and power generation.

- Application Expansion: Increasingly used in renewable energy (wind turbines) and industrial automation for precise speed control and monitoring.

Dominant Industry Segments:

- Automotive: This sector is a major driver of vibration sensor demand, encompassing engine health monitoring, chassis vibration analysis, safety systems (e.g., ABS, ESC), and the growing electric vehicle (EV) market for battery and motor diagnostics.

- Key Drivers: Stringent safety regulations, increasing vehicle complexity, and the pursuit of enhanced driving comfort and performance.

- Aerospace and Defense: Characterized by high-value applications where precision and reliability are non-negotiable. Vibration sensors are critical for aircraft health monitoring, structural integrity assessment, and the performance of defense systems.

- Key Drivers: Extreme operating conditions, need for early fault detection in critical systems, and stringent safety standards.

- Oil and Gas: This industry relies heavily on vibration sensors for the continuous monitoring of pumps, compressors, turbines, and pipelines to prevent failures and ensure operational safety in harsh environments.

- Key Drivers: The need to maintain high uptime for exploration and production, safety regulations in potentially hazardous environments, and the integrity of aging infrastructure.

- Industrial Automation and Metals and Mining: These sectors are increasingly adopting vibration sensing for predictive maintenance of heavy machinery, robotics, and process control equipment to optimize efficiency and reduce downtime.

- Key Drivers: Focus on operational efficiency, cost reduction through minimized unplanned downtime, and the safe operation of heavy-duty equipment.

Asia Pacific Vibration Sensors Industry Product Developments

The Asia Pacific vibration sensors industry is witnessing a rapid evolution in product development, driven by technological innovation and the increasing demand for smarter, more connected monitoring solutions. MEMS technology continues to be a cornerstone, enabling the creation of smaller, more energy-efficient, and cost-effective accelerometers suitable for a broader spectrum of applications. Innovations are focused on enhancing sensor accuracy, expanding frequency response ranges, and improving resistance to harsh environmental conditions. The integration of these sensors with wireless communication modules and embedded processing capabilities is leading to the development of smart sensors that can perform local data analysis and transmit actionable insights. This trend is particularly evident in the development of IoT-enabled condition monitoring systems designed for predictive maintenance in industries such as automotive, manufacturing, and oil and gas, offering competitive advantages through early fault detection and optimized asset management.

Report Scope & Segmentation Analysis

The "Asia Pacific Vibration Sensors Industry" report provides a comprehensive analysis of the market from 2019 to 2033, with a base year of 2025. The study encompasses detailed segmentation across product types and end-use industries.

Product Segmentation:

- Accelerometers: This segment, expected to witness significant growth at a CAGR of approximately 7.8% from 2025-2033, is driven by widespread adoption in automotive and consumer electronics.

- Proximity Probes: Critical for high-speed rotating machinery, this segment is projected to grow at a CAGR of around 6.5%, with strong demand from the oil and gas and power generation sectors.

- Tachometers: Integral to machinery diagnostics, this segment is anticipated to expand at a CAGR of roughly 7.0%, finding applications in industrial automation and automotive.

- Others: This segment includes specialized vibration sensors and is expected to grow at a CAGR of approximately 6.8%, catering to niche industrial requirements.

Industry Segmentation:

- Automotive: The largest segment, projected to grow at a CAGR of 8.0% due to increasing vehicle sophistication and safety regulations.

- Healthcare: Experiencing steady growth at a CAGR of 7.2%, driven by demand for precision monitoring in medical equipment.

- Aerospace and Defense: A high-value segment with a projected CAGR of 7.5%, driven by stringent safety and performance requirements.

- Consumer Electronics: Demonstrating robust growth at a CAGR of 8.2%, fueled by the integration of sensors in smart devices.

- Oil and Gas: A critical sector for vibration sensing, expected to grow at a CAGR of 6.9%, focusing on asset integrity and operational safety.

- Metals and Mining: This segment is projected to grow at a CAGR of 7.1%, driven by the need for efficient operation of heavy machinery.

- Others: This segment, including power generation and general manufacturing, is expected to grow at a CAGR of 7.0%.

Key Drivers of Asia Pacific Vibration Sensors Industry Growth

The Asia Pacific vibration sensors industry's expansion is primarily propelled by several interconnected factors. The accelerating adoption of Industry 4.0 and smart manufacturing initiatives across the region is creating a substantial demand for real-time condition monitoring solutions. This includes the integration of IoT sensors for predictive maintenance, reducing unplanned downtime and optimizing operational efficiency in sectors like automotive, oil and gas, and manufacturing. Technological advancements, particularly in MEMS technology, are leading to smaller, more accurate, and cost-effective sensors, broadening their applicability. Furthermore, stringent regulatory mandates in industries like aerospace and automotive, emphasizing safety and reliability, necessitate the use of advanced vibration sensing for fault detection and performance validation. The increasing focus on asset lifecycle management and the need to extend the lifespan of expensive industrial equipment also contribute significantly to market growth.

Challenges in the Asia Pacific Vibration Sensors Industry Sector

Despite the promising growth trajectory, the Asia Pacific vibration sensors industry faces several challenges that could temper its expansion. The high initial investment cost for sophisticated sensor systems and the associated data analysis infrastructure can be a significant barrier for small and medium-sized enterprises (SMEs), particularly in developing economies within the region. Data security and privacy concerns, especially with the increasing reliance on cloud-based platforms and wireless transmission, pose a challenge, requiring robust cybersecurity measures. While market consolidation is occurring, the presence of numerous smaller players and intense price competition can lead to thinner profit margins for manufacturers. Furthermore, the availability of skilled personnel capable of installing, operating, and interpreting data from advanced vibration monitoring systems remains a bottleneck in certain sub-regions, hindering widespread adoption.

Emerging Opportunities in Asia Pacific Vibration Sensors Industry

The Asia Pacific vibration sensors industry is ripe with emerging opportunities, driven by technological evolution and shifting industrial demands. The burgeoning electric vehicle (EV) market presents a significant avenue, with vibration sensors crucial for monitoring EV powertrains, battery health, and structural integrity. The increasing application of AI and machine learning in conjunction with vibration data analysis is opening doors for more sophisticated predictive analytics and prescriptive maintenance, moving beyond mere fault detection to offering optimized solutions. Furthermore, the growing focus on renewable energy sources, such as wind and solar power, is creating a demand for robust vibration sensors to monitor the performance and health of associated machinery, like wind turbines. The development of smart cities and infrastructure projects across the region also presents opportunities for vibration monitoring in civil engineering applications and public transportation systems.

Leading Players in the Asia Pacific Vibration Sensors Industry Market

- Honeywell International Inc.

- NXP Semiconductors N V

- SKF AB

- National Instruments Corporation

- Emerson Electric Co.

- Bosch Sensortec GmbH (Robert Bosch GmbH)

- TE Connectivity Ltd.

- Hansford Sensors Ltd

- Texas Instruments Incorporated

- Rockwell Automation Inc.

- Analog Devices Inc.

Key Developments in Asia Pacific Vibration Sensors Industry Industry

- March 2020: SKF announced the SKF Enlight Collect IMx-1, a compact vibration and temperature sensor designed for automatic monitoring of rotating parts on heavy industrial machinery. This development aims to significantly reduce unplanned downtime and maintenance costs by enabling more frequent data collection from previously inaccessible locations with fewer technicians.

- March 2020: TE Connectivity Ltd. completed its public takeover of First Sensor AG, acquiring 71.87% of its shares. This strategic move allows TE Connectivity to broaden its product portfolio, integrating First Sensor's innovative sensors with TE's existing offerings, thereby strengthening its position in the sensors market and supporting its overall growth strategy.

Strategic Outlook for Asia Pacific Vibration Sensors Industry Market

The strategic outlook for the Asia Pacific vibration sensors industry is overwhelmingly positive, fueled by the relentless pursuit of operational excellence and technological advancement. The ongoing digital transformation across industries, coupled with the escalating adoption of Industry 4.0 principles, will continue to drive demand for sophisticated condition monitoring solutions. Key growth catalysts include the increasing integration of AI and machine learning for enhanced data analytics, the expansion of the electric vehicle market, and the growing need for predictive maintenance in critical infrastructure and industrial assets. Companies that focus on developing innovative, cost-effective, and integrated sensing solutions, while also addressing cybersecurity and data privacy concerns, are well-positioned to capitalize on the significant market potential and emerging opportunities within this dynamic region. Strategic partnerships and investments in R&D will be crucial for maintaining a competitive edge.

Asia Pacific Vibration Sensors Industry Segmentation

-

1. Product

- 1.1. Accelerometers

- 1.2. Proximity Probes

- 1.3. Tachometers

- 1.4. Others

-

2. Industry

- 2.1. Automotive

- 2.2. Healthcare

- 2.3. Aerospace and Defense

- 2.4. Consumer Electronics

- 2.5. Oil And Gas

- 2.6. Metals and Mining

- 2.7. Others

Asia Pacific Vibration Sensors Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Vibration Sensors Industry Regional Market Share

Geographic Coverage of Asia Pacific Vibration Sensors Industry

Asia Pacific Vibration Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Accelerometers

- 5.1.2. Proximity Probes

- 5.1.3. Tachometers

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Industry

- 5.2.1. Automotive

- 5.2.2. Healthcare

- 5.2.3. Aerospace and Defense

- 5.2.4. Consumer Electronics

- 5.2.5. Oil And Gas

- 5.2.6. Metals and Mining

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Asia Pacific Vibration Sensors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Accelerometers

- 6.1.2. Proximity Probes

- 6.1.3. Tachometers

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Industry

- 6.2.1. Automotive

- 6.2.2. Healthcare

- 6.2.3. Aerospace and Defense

- 6.2.4. Consumer Electronics

- 6.2.5. Oil And Gas

- 6.2.6. Metals and Mining

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 NXP Semiconductors N V

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SKF AB

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 National Instruments Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Emerson Electric Co

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bosch Sensortec GmbH (Robert Bosch GmbH)*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 TE Connectivity Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Hansford Sensors Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Texas Instruments Incorporated

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Rockwell Automation Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Analog Devices Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Vibration Sensors Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Vibration Sensors Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Vibration Sensors Industry Revenue million Forecast, by Product 2020 & 2033

- Table 2: Asia Pacific Vibration Sensors Industry Revenue million Forecast, by Industry 2020 & 2033

- Table 3: Asia Pacific Vibration Sensors Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Asia Pacific Vibration Sensors Industry Revenue million Forecast, by Product 2020 & 2033

- Table 5: Asia Pacific Vibration Sensors Industry Revenue million Forecast, by Industry 2020 & 2033

- Table 6: Asia Pacific Vibration Sensors Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: China Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Japan Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: South Korea Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: India Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Australia Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: New Zealand Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Indonesia Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Malaysia Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Singapore Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Thailand Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Vietnam Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Philippines Asia Pacific Vibration Sensors Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Vibration Sensors Industry?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Asia Pacific Vibration Sensors Industry?

Key companies in the market include Honeywell International Inc, NXP Semiconductors N V, SKF AB, National Instruments Corporation, Emerson Electric Co, Bosch Sensortec GmbH (Robert Bosch GmbH)*List Not Exhaustive, TE Connectivity Ltd, Hansford Sensors Ltd, Texas Instruments Incorporated, Rockwell Automation Inc, Analog Devices Inc.

3. What are the main segments of the Asia Pacific Vibration Sensors Industry?

The market segments include Product, Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1639.9 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Machine Monitoring and Maintenance; Longer Service Life. Self Generating Capability and Wide Range of Frequency of Vibration Sensors.

6. What are the notable trends driving market growth?

Aerospace & Defense End User to Hold Significant Share.

7. Are there any restraints impacting market growth?

Compatibility With Old Machinery; Critical and Hazardous Implication on the Environment.

8. Can you provide examples of recent developments in the market?

Mar 2020: SKF has announced a compact vibration and temperature sensor that monitors the condition of rotating parts on heavy industrial machinery automatically. The SKF Enlight Collect IMx-1 sensor will allow users to cut both unplanned downtime and maintenance costs. They will also be able to collect data more frequently over hours and days instead of weeks and months from locations that were previously inaccessible, using fewer technicians.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Vibration Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Vibration Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Vibration Sensors Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Vibration Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence