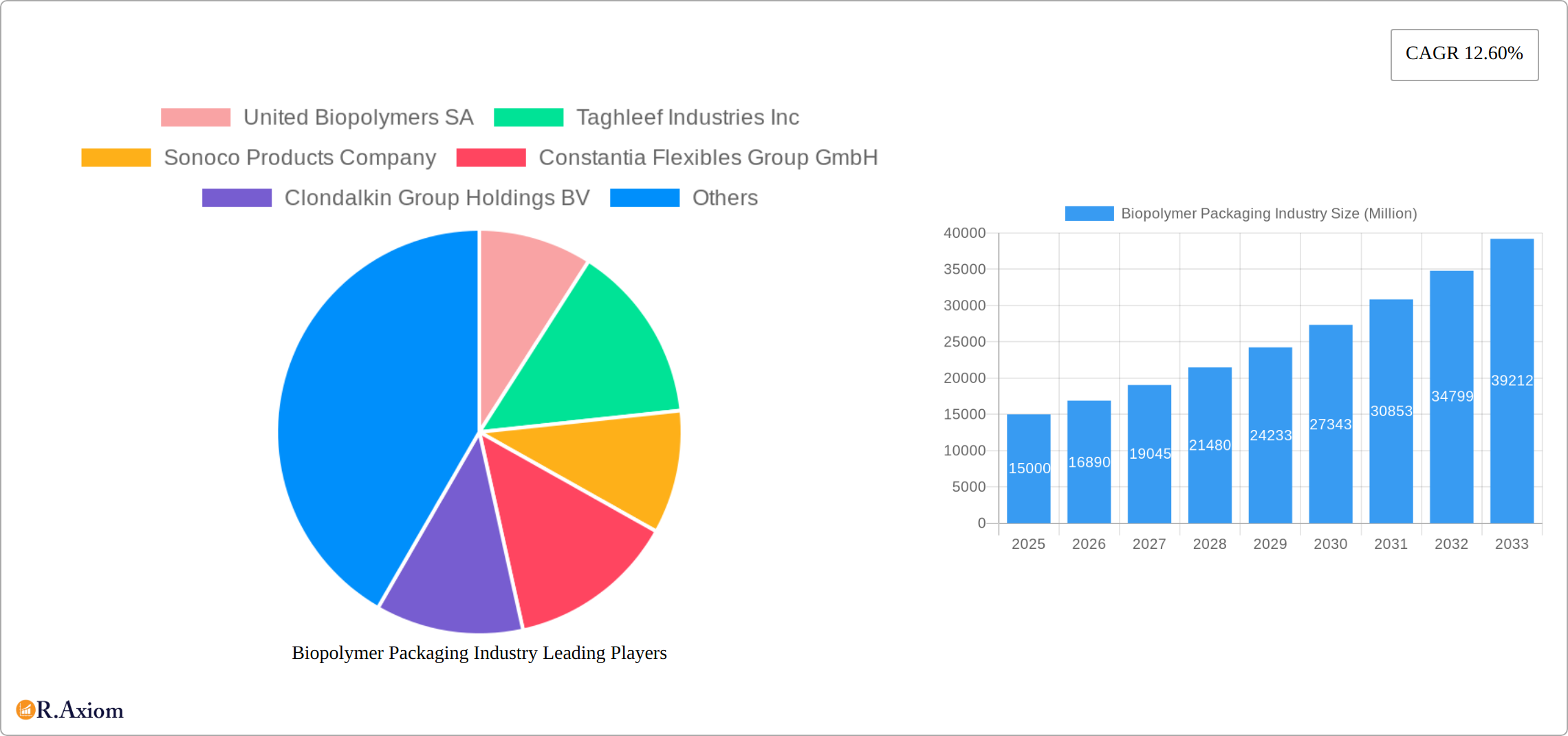

Key Insights

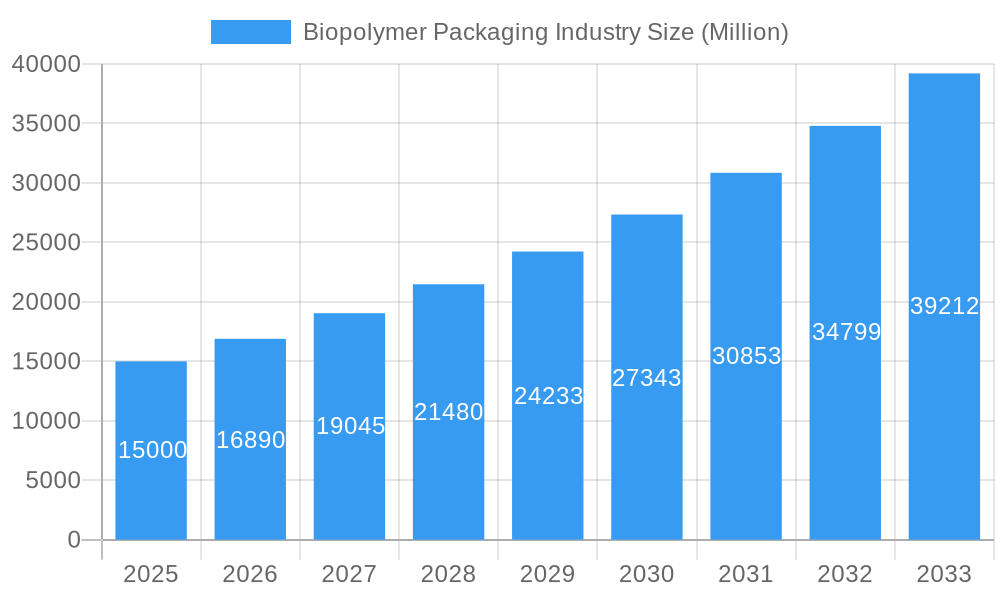

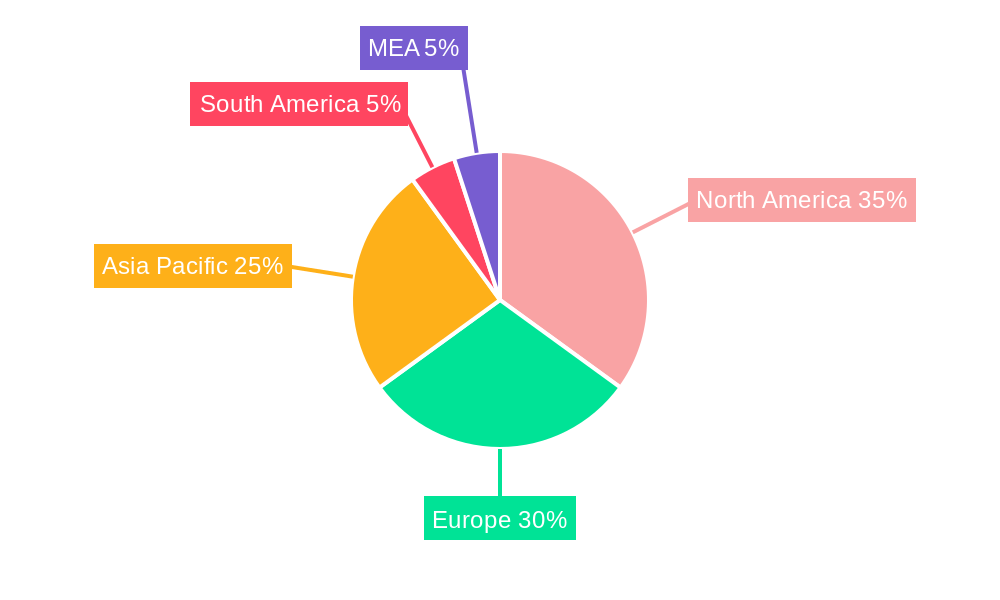

The biopolymer packaging market is experiencing robust growth, driven by increasing consumer demand for eco-friendly and sustainable alternatives to traditional petroleum-based packaging. A compound annual growth rate (CAGR) of 12.60% from 2019 to 2024 suggests a significant market expansion, projected to continue into the forecast period (2025-2033). This growth is fueled by several key factors: rising environmental concerns and stringent regulations regarding plastic waste, coupled with the increasing adoption of bio-based materials across various end-user industries. The food and beverage sector, followed by retail and healthcare, represent the largest market segments, reflecting the widespread need for sustainable packaging solutions in these sectors. The shift towards biodegradable and compostable packaging options, like those made from polylactic acid (PLA) and polyhydroxyalkanoates (PHAs), is a major trend driving market expansion. However, challenges such as higher production costs compared to conventional packaging and limitations in material performance in certain applications remain as restraints. Technological advancements aiming to address these limitations, particularly in terms of improving the barrier properties and durability of biopolymers, are crucial for sustaining market growth. The geographic distribution reveals strong growth across North America, Europe, and the Asia-Pacific region, driven by increasing consumer awareness and government initiatives promoting sustainable packaging.

Biopolymer Packaging Industry Market Size (In Billion)

The competitive landscape is characterized by a mix of large multinational corporations and specialized biopolymer producers. Key players like United Biopolymers SA, Taghleef Industries Inc., and Amcor PLC are actively investing in research and development, expanding their product portfolios, and adopting strategic partnerships to capitalize on the growing market demand. Regional variations in growth rates are expected, reflecting differences in regulatory landscapes, consumer preferences, and the availability of raw materials. The market's future trajectory hinges on continuous innovation in biopolymer technology, the development of more cost-effective production methods, and the expansion of collection and composting infrastructure to facilitate the full lifecycle benefits of biodegradable packaging. Further market growth will also depend on effective communication strategies to educate consumers about the benefits of biopolymer packaging and dispel misconceptions about its performance and viability.

Biopolymer Packaging Industry Company Market Share

Biopolymer Packaging Industry: A Comprehensive Market Analysis (2019-2033)

This comprehensive report provides a detailed analysis of the Biopolymer Packaging industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. The study period covers 2019-2033, with a base year of 2025 and a forecast period spanning 2025-2033. The report leverages rigorous research methodologies to provide accurate market sizing, segmentation, and growth projections, enabling informed decision-making. The report incorporates analysis of key players, emerging trends, and significant challenges to provide a holistic view of the industry landscape. The market value is expressed in Millions throughout the report.

Biopolymer Packaging Industry Market Concentration & Innovation

The biopolymer packaging market exhibits a moderately concentrated structure, with a handful of multinational corporations commanding significant market share. Key players like Amcor PLC, Sonoco Products Company, and Sealed Air Corporation leverage their established distribution networks and technological capabilities to maintain their leadership positions. However, the market also witnesses the emergence of specialized biopolymer producers and innovative packaging solutions providers, leading to increased competition. The estimated market share of the top five players in 2025 is xx%.

Innovation Drivers:

- Sustainable packaging regulations and consumer demand for eco-friendly alternatives are driving innovation in biodegradable and compostable biopolymer materials.

- Advancements in bio-based polymer technology are leading to improved barrier properties, strength, and processability of biopolymer packaging.

- The exploration of novel bio-based feedstocks and efficient production processes is contributing to cost reduction and improved sustainability.

Regulatory Frameworks:

Stringent environmental regulations in several regions are pushing the adoption of biopolymer packaging, particularly in the EU and North America. These regulations impose limitations on the use of conventional plastics and incentivize the use of eco-friendly alternatives.

Product Substitutes:

Biopolymer packaging faces competition from traditional petroleum-based plastics and other sustainable packaging materials like paper and glass. However, the increasing awareness of plastic pollution and the limitations of other sustainable alternatives are creating a favorable environment for biopolymer adoption.

M&A Activities:

The biopolymer packaging industry has witnessed several mergers and acquisitions in recent years, driven by the consolidation of market share and the pursuit of technological synergies. The total value of M&A deals in the industry during 2019-2024 was estimated at $xx Million.

Biopolymer Packaging Industry Industry Trends & Insights

The global biopolymer packaging market is experiencing robust growth, propelled by a confluence of factors. The estimated Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033) is projected at xx%. This expansion is largely driven by rising consumer awareness of environmental concerns, coupled with stricter governmental regulations aimed at reducing plastic waste. The increasing demand for sustainable and eco-friendly packaging solutions across various end-use industries is a significant contributor to market expansion. Technological advancements, leading to improved material properties and production efficiencies, are also playing a crucial role.

Consumer preferences are shifting towards products with sustainable packaging, creating significant opportunities for biopolymer packaging manufacturers. This trend is particularly pronounced in developed countries with high environmental awareness. However, the high initial cost of biopolymer packaging remains a challenge. Market penetration of biopolymer packaging is gradually increasing, with estimates suggesting xx% market share in 2025, projected to increase to xx% by 2033. Competitive dynamics are characterized by both intense rivalry among established players and the entry of new players specializing in innovative biopolymer solutions.

Dominant Markets & Segments in Biopolymer Packaging Industry

Leading Regions and Countries:

North America and Europe are currently the dominant markets for biopolymer packaging, driven by stringent environmental regulations and high consumer demand for sustainable products. However, Asia-Pacific is expected to witness the fastest growth during the forecast period, fueled by rapid economic development and increasing disposable incomes.

Dominant Segments:

Material Type: Biodegradable biopolymers, owing to their environmental benefits, are experiencing higher growth compared to non-biodegradable alternatives. However, non-biodegradable biopolymers still hold a significant market share due to their cost-effectiveness and specific application requirements.

End-user Industry: The food and beverage sector accounts for the largest share of biopolymer packaging consumption due to the increasing demand for sustainable packaging solutions for food products. The healthcare and personal care/homecare segments are also showing promising growth potential.

Key Drivers:

- Economic Policies: Government incentives, tax breaks, and subsidies for biopolymer production are driving market growth in several regions.

- Infrastructure: Investments in advanced bio-refineries and efficient waste management systems are contributing to the expansion of the biopolymer packaging industry.

Biopolymer Packaging Industry Product Developments

Recent product developments focus on enhancing the barrier properties, strength, and processability of biopolymer packaging. Innovations include the development of advanced bio-based polymers with improved oxygen and moisture barriers, enabling their application in a wider range of products. These advancements also address concerns regarding the cost and performance limitations of biopolymer packaging compared to traditional plastics, increasing their market competitiveness. The integration of smart packaging technologies, such as sensors for monitoring product freshness, is also gaining traction.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation analysis of the biopolymer packaging market, considering various crucial factors. The market is segmented by material type (biodegradable and non-biodegradable), offering a detailed examination of each segment's growth trajectory, market size, and competitive landscape. Further granularity is achieved through end-user industry segmentation, encompassing food and beverages, retail, healthcare, personal care/homecare, and other sectors. Detailed analysis reveals that the biodegradable segment is projected to demonstrate a higher compound annual growth rate (CAGR) than its non-biodegradable counterpart, primarily driven by escalating global environmental awareness and stringent regulations. The food and beverage sector is anticipated to maintain its position as the largest end-user segment, exhibiting substantial growth potential, particularly within developing economies. The report also explores regional variations in market dynamics, highlighting key opportunities and challenges in different geographic regions.

Key Drivers of Biopolymer Packaging Industry Growth

The remarkable growth witnessed in the biopolymer packaging industry is fueled by a confluence of significant factors:

- Stringent Environmental Regulations: A global surge in regulations aimed at curbing plastic waste is significantly accelerating the adoption of bio-based alternatives. These regulations often include bans on specific plastics, extended producer responsibility (EPR) schemes, and taxes on non-recyclable materials.

- Growing Consumer Awareness: Increasing consumer consciousness regarding environmental sustainability is driving a strong demand for eco-friendly packaging solutions. Consumers are actively seeking out products with sustainable packaging, influencing purchasing decisions and prompting brands to adopt greener options.

- Technological Advancements: Continuous technological advancements are resulting in the development of biopolymers with enhanced performance characteristics, including improved barrier properties, strength, and durability. Simultaneously, innovations are reducing production costs, making biopolymer packaging a more economically viable option.

- Government Support and Incentives: Governments worldwide are actively promoting the production and adoption of biopolymer packaging through various initiatives, including subsidies, tax breaks, and research funding. These supportive policies are further accelerating market growth.

- Brand Reputation and Sustainability Initiatives: Companies are increasingly recognizing the importance of incorporating sustainable practices into their operations. The adoption of biopolymer packaging enhances brand image and appeals to environmentally conscious consumers, contributing to a positive brand reputation.

Challenges in the Biopolymer Packaging Industry Sector

Several factors impede the growth of the biopolymer packaging industry:

- The higher cost of biopolymers compared to traditional plastics remains a barrier to wider adoption.

- The lack of well-established collection and composting infrastructure for biodegradable biopolymers limits their sustainability benefits.

- Performance limitations of some biopolymers, such as limited barrier properties and heat resistance, restrict their applications.

- Competition from other sustainable packaging materials, such as paper and glass, poses a challenge to biopolymer packaging. The estimated impact of these challenges on market growth in 2025 is xx%.

Emerging Opportunities in Biopolymer Packaging Industry

The biopolymer packaging industry presents several emerging opportunities:

- The development of new bio-based polymers with improved properties and reduced costs opens new market avenues.

- Expanding into new applications, such as medical devices and electronics packaging, provides growth potential.

- The increasing demand for customized and functional biopolymer packaging solutions offers opportunities for innovation.

- The development of efficient waste management systems for biopolymer packaging enhances their environmental benefits.

Leading Players in the Biopolymer Packaging Industry Market

- Amcor PLC

- Sonoco Products Company

- Sealed Air Corporation

- United Biopolymers SA

- Taghleef Industries Inc

- Constantia Flexibles Group GmbH

- Clondalkin Group Holdings BV

- Berry Plastics Group Inc

- Mondi Group

- Tetra Pak International SA

- This list is not exhaustive and represents a selection of key players. The full report contains a more comprehensive list.

Key Developments in Biopolymer Packaging Industry Industry

- January 2023: Amcor PLC launched a new range of biodegradable and compostable packaging solutions for food applications.

- June 2022: Sonoco Products Company invested in a new biopolymer production facility to expand its manufacturing capacity.

- October 2021: A significant merger between two leading biopolymer producers resulted in the creation of a larger market player.

- Further developments will be detailed in the full report.

Strategic Outlook for Biopolymer Packaging Industry Market

The biopolymer packaging market presents a compelling growth opportunity in the coming years. Several factors contribute to this positive outlook, including intensifying environmental concerns, supportive government policies, and ongoing technological innovations. The market's future hinges on developing cost-effective and high-performance bio-based polymers capable of effectively competing with traditional petroleum-based plastics. Expansion into new applications, such as flexible films and rigid containers, and geographical markets, particularly in emerging economies, will be crucial for driving future growth. A strategic focus on sustainability, research and development, and fostering collaboration across the entire value chain—from raw material suppliers to end-users—will be essential for success in this rapidly evolving market. The report delves deeper into specific strategic recommendations for companies operating within this sector.

Biopolymer Packaging Industry Segmentation

-

1. Material Type

-

1.1. Non-biodegradable

- 1.1.1. PET

- 1.1.2. PA

- 1.1.3. PTT

- 1.1.4. Other Material Types

-

1.2. Biodegradability

- 1.2.1. PLA

- 1.2.2. Starch Blends

- 1.2.3. PBAT

- 1.2.4. Other Biodegradability Types

-

1.1. Non-biodegradable

-

2. End-user Industry

- 2.1. Food and Beverages

- 2.2. Retail

- 2.3. Healthcare

- 2.4. Personal Care/Homecare

- 2.5. Other End-user Industries

Biopolymer Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Biopolymer Packaging Industry Regional Market Share

Geographic Coverage of Biopolymer Packaging Industry

Biopolymer Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Non-biodegradable

- 5.1.1.1. PET

- 5.1.1.2. PA

- 5.1.1.3. PTT

- 5.1.1.4. Other Material Types

- 5.1.2. Biodegradability

- 5.1.2.1. PLA

- 5.1.2.2. Starch Blends

- 5.1.2.3. PBAT

- 5.1.2.4. Other Biodegradability Types

- 5.1.1. Non-biodegradable

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food and Beverages

- 5.2.2. Retail

- 5.2.3. Healthcare

- 5.2.4. Personal Care/Homecare

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Biopolymer Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Non-biodegradable

- 6.1.1.1. PET

- 6.1.1.2. PA

- 6.1.1.3. PTT

- 6.1.1.4. Other Material Types

- 6.1.2. Biodegradability

- 6.1.2.1. PLA

- 6.1.2.2. Starch Blends

- 6.1.2.3. PBAT

- 6.1.2.4. Other Biodegradability Types

- 6.1.1. Non-biodegradable

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Food and Beverages

- 6.2.2. Retail

- 6.2.3. Healthcare

- 6.2.4. Personal Care/Homecare

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Non-biodegradable

- 7.1.1.1. PET

- 7.1.1.2. PA

- 7.1.1.3. PTT

- 7.1.1.4. Other Material Types

- 7.1.2. Biodegradability

- 7.1.2.1. PLA

- 7.1.2.2. Starch Blends

- 7.1.2.3. PBAT

- 7.1.2.4. Other Biodegradability Types

- 7.1.1. Non-biodegradable

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Food and Beverages

- 7.2.2. Retail

- 7.2.3. Healthcare

- 7.2.4. Personal Care/Homecare

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Europe Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Non-biodegradable

- 8.1.1.1. PET

- 8.1.1.2. PA

- 8.1.1.3. PTT

- 8.1.1.4. Other Material Types

- 8.1.2. Biodegradability

- 8.1.2.1. PLA

- 8.1.2.2. Starch Blends

- 8.1.2.3. PBAT

- 8.1.2.4. Other Biodegradability Types

- 8.1.1. Non-biodegradable

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Food and Beverages

- 8.2.2. Retail

- 8.2.3. Healthcare

- 8.2.4. Personal Care/Homecare

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Asia Pacific Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Non-biodegradable

- 9.1.1.1. PET

- 9.1.1.2. PA

- 9.1.1.3. PTT

- 9.1.1.4. Other Material Types

- 9.1.2. Biodegradability

- 9.1.2.1. PLA

- 9.1.2.2. Starch Blends

- 9.1.2.3. PBAT

- 9.1.2.4. Other Biodegradability Types

- 9.1.1. Non-biodegradable

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Food and Beverages

- 9.2.2. Retail

- 9.2.3. Healthcare

- 9.2.4. Personal Care/Homecare

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Latin America Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Non-biodegradable

- 10.1.1.1. PET

- 10.1.1.2. PA

- 10.1.1.3. PTT

- 10.1.1.4. Other Material Types

- 10.1.2. Biodegradability

- 10.1.2.1. PLA

- 10.1.2.2. Starch Blends

- 10.1.2.3. PBAT

- 10.1.2.4. Other Biodegradability Types

- 10.1.1. Non-biodegradable

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Food and Beverages

- 10.2.2. Retail

- 10.2.3. Healthcare

- 10.2.4. Personal Care/Homecare

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Middle East and Africa Biopolymer Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Non-biodegradable

- 11.1.1.1. PET

- 11.1.1.2. PA

- 11.1.1.3. PTT

- 11.1.1.4. Other Material Types

- 11.1.2. Biodegradability

- 11.1.2.1. PLA

- 11.1.2.2. Starch Blends

- 11.1.2.3. PBAT

- 11.1.2.4. Other Biodegradability Types

- 11.1.1. Non-biodegradable

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Food and Beverages

- 11.2.2. Retail

- 11.2.3. Healthcare

- 11.2.4. Personal Care/Homecare

- 11.2.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 United Biopolymers SA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Taghleef Industries Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sonoco Products Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Constantia Flexibles Group GmbH

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Clondalkin Group Holdings BV

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Berry Plastics Group Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mondi Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Tetra Pak International SA

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sealed Air Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Amcor PLC*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 United Biopolymers SA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Biopolymer Packaging Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 3: North America Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 5: North America Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 9: Europe Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 10: Europe Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 11: Europe Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 15: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 16: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Pacific Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 21: Latin America Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 22: Latin America Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Latin America Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Biopolymer Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 27: Middle East and Africa Biopolymer Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Middle East and Africa Biopolymer Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Biopolymer Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Biopolymer Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Biopolymer Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Biopolymer Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 5: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 8: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 9: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 11: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 12: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 14: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Biopolymer Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 17: Global Biopolymer Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Biopolymer Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Biopolymer Packaging Industry?

The projected CAGR is approximately 12.60%.

2. Which companies are prominent players in the Biopolymer Packaging Industry?

Key companies in the market include United Biopolymers SA, Taghleef Industries Inc, Sonoco Products Company, Constantia Flexibles Group GmbH, Clondalkin Group Holdings BV, Berry Plastics Group Inc, Mondi Group, Tetra Pak International SA, Sealed Air Corporation, Amcor PLC*List Not Exhaustive.

3. What are the main segments of the Biopolymer Packaging Industry?

The market segments include Material Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; The Growing Government Regulations for Bio-based Packaging; Increasing Awareness for Human Well Being and Eco-friendly Products.

6. What are the notable trends driving market growth?

Food and Beverages Industry is Expected to Witness a Significant Growth during the Forecast Period.

7. Are there any restraints impacting market growth?

; Performance Issues with Bio-based Materials; High Cost of Bio-packaging Materials.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Biopolymer Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Biopolymer Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Biopolymer Packaging Industry?

To stay informed about further developments, trends, and reports in the Biopolymer Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence