Key Insights

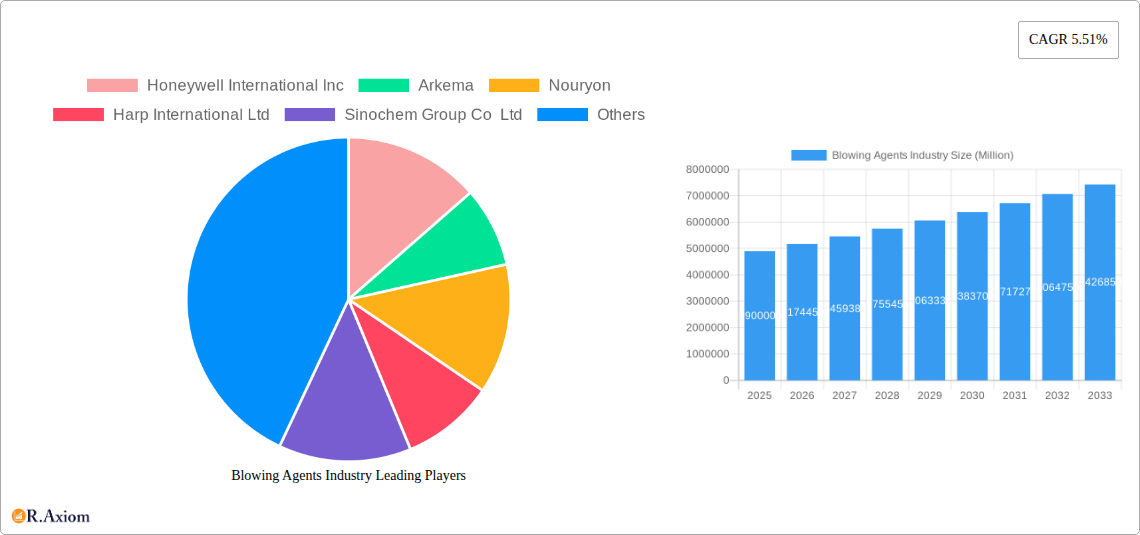

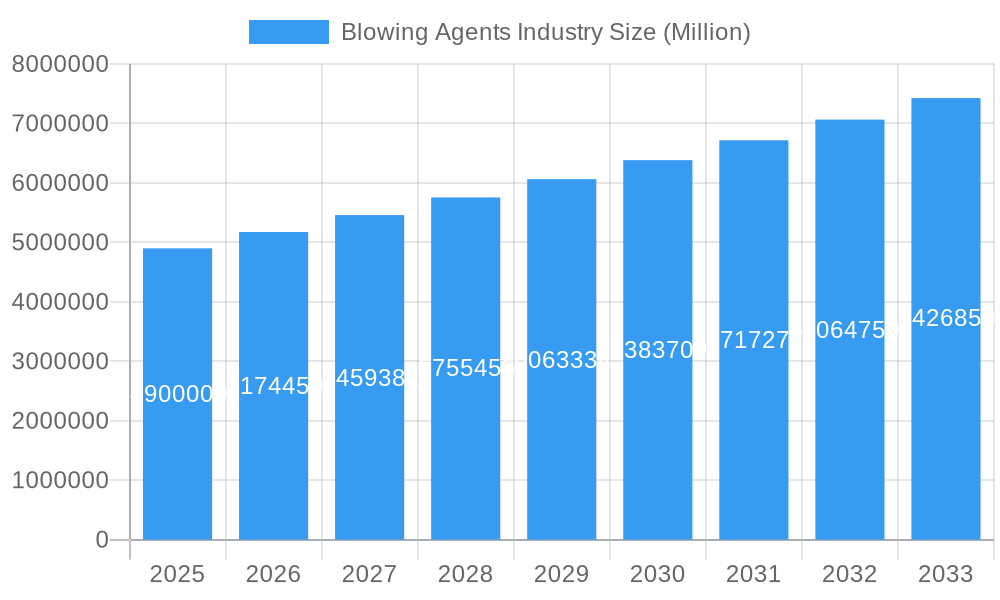

The global Blowing Agents market is poised for robust growth, projected to reach a valuation of $4.90 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 5.51% through 2033. This expansion is primarily fueled by the escalating demand for energy-efficient insulation materials across diverse sectors, particularly building and construction, and a growing preference for sustainable and environmentally friendly blowing agents. The stringent regulatory landscape, phasing out ozone-depleting substances like HCFCs, is a significant driver, pushing manufacturers towards innovative alternatives such as HFOs and HCs. The automotive industry's increasing adoption of lightweight foam materials for enhanced fuel efficiency also contributes to market momentum. Furthermore, the burgeoning furniture, bedding, and appliance sectors, which rely heavily on polyurethane and other foam types for comfort and performance, represent substantial growth avenues.

Blowing Agents Industry Market Size (In Million)

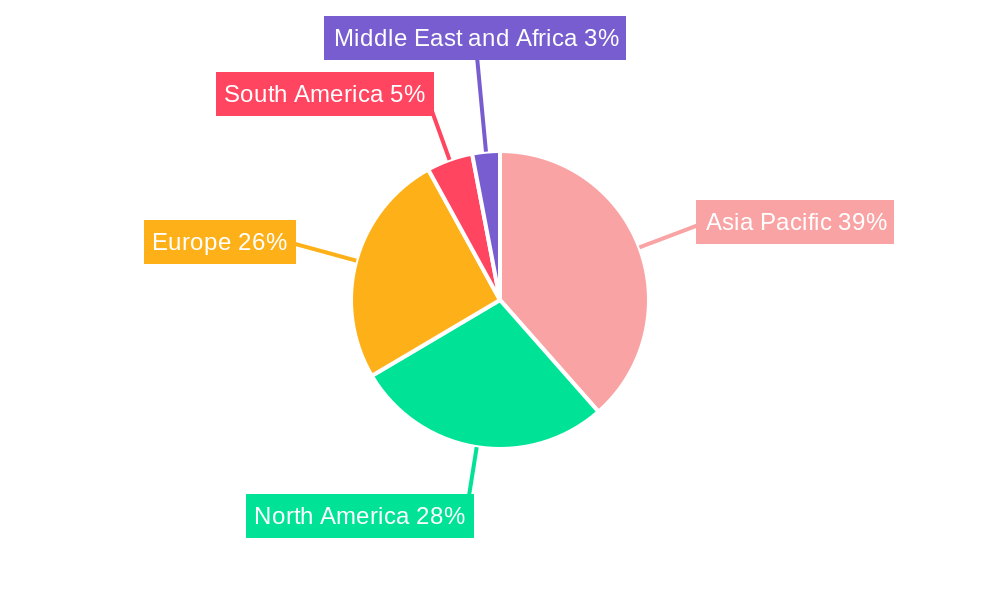

The market's trajectory is characterized by a significant shift towards lower Global Warming Potential (GWP) blowing agents, with HFOs emerging as a frontrunner due to their superior environmental profiles and comparable performance to traditional HFCs. While the transition away from HCFCs and the development of novel HFO formulations present opportunities, challenges such as the higher cost of some advanced blowing agents and the need for retooling manufacturing processes for certain applications could temper growth in specific segments. However, ongoing research and development efforts aimed at optimizing cost-effectiveness and expanding application portfolios are expected to mitigate these restraints. Geographically, Asia Pacific, led by China and India, is anticipated to dominate the market, driven by rapid industrialization, urbanization, and a growing middle class with increasing disposable incomes. North America and Europe will also remain significant markets, propelled by mature construction industries and stringent environmental regulations.

Blowing Agents Industry Company Market Share

Here is an SEO-optimized, detailed report description for the Blowing Agents Industry:

Blowing Agents Industry Market Concentration & Innovation

The global blowing agents market exhibits a moderate to high level of concentration, with key players like Honeywell International Inc., Arkema, Nouryon, and The Chemours Company holding significant market share. Innovation is a primary driver, fueled by the continuous demand for more sustainable and efficient blowing agents that comply with stringent environmental regulations. The transition from HCFCs and HFCs to HFOs and other low-GWP alternatives is a major innovation trend. Regulatory frameworks, such as the Kigali Amendment to the Montreal Protocol and various regional environmental policies, are pivotal in shaping market dynamics and pushing for greener solutions. Product substitutes, including physical blowing agents and alternative insulation materials, pose a competitive challenge, necessitating ongoing research and development into next-generation blowing agents with enhanced performance and reduced environmental impact. End-user trends, particularly the growing demand for energy-efficient insulation in the building and construction sector and lightweighting solutions in the automotive industry, are stimulating innovation. Mergers and acquisitions (M&A) activities, while not pervasive, are strategic moves by major companies to consolidate market position, acquire advanced technologies, and expand their product portfolios. For instance, recent M&A deals in the specialty chemicals sector, with estimated values in the hundreds of millions of USD, indicate a focus on acquiring expertise in HFO production and sustainable blowing agent technologies.

Blowing Agents Industry Industry Trends & Insights

The blowing agents industry is experiencing robust growth, projected to witness a significant Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period of 2025–2033. This expansion is primarily driven by the escalating demand for high-performance insulation materials across diverse end-use industries, particularly building and construction, which accounts for a substantial portion of market penetration. Technological disruptions are reshaping the industry landscape, with a pronounced shift towards Hydrofluoroolefins (HFOs) due to their superior environmental profiles, boasting near-zero Global Warming Potential (GWP) and ozone depletion potential. This transition is overcoming historical market dominance of Hydrochlorofluorocarbons (HCFCs) and Hydrofluorocarbons (HFCs), which are facing increasing regulatory scrutiny and phase-out mandates globally. Consumer preferences are increasingly aligned with sustainability and energy efficiency. In the building sector, the demand for energy-efficient homes and commercial spaces directly translates into a higher need for effective insulation foams, thus boosting the consumption of blowing agents. Similarly, in the automotive industry, lightweighting initiatives to improve fuel efficiency are driving the adoption of foam-based components, requiring advanced blowing agents. The competitive dynamics are characterized by intense research and development efforts, strategic partnerships, and capacity expansions by major players to cater to the evolving market needs. Companies are investing heavily in R&D to develop novel blowing agent formulations that offer improved fire retardancy, thermal conductivity, and processing characteristics, while simultaneously meeting strict environmental compliance. The market penetration of HFOs is steadily increasing, replacing older generation blowing agents and setting new benchmarks for performance and sustainability. The historical period of 2019–2024 has seen a foundational shift, with the base year of 2025 marking a significant inflection point for the widespread adoption of next-generation blowing agents.

Dominant Markets & Segments in Blowing Agents Industry

The Building and Construction application segment stands as the dominant force in the blowing agents market, driven by escalating global construction activities and a strong emphasis on energy efficiency. Within this segment, Polyurethane Foam (PUF) is the most widely utilized foam type, favored for its excellent insulation properties and versatility in applications like rigid boards, spray foams, and insulated panels. The demand for PUF is closely linked to stringent building codes requiring enhanced thermal performance, directly boosting the consumption of blowing agents.

- Key Drivers for Building and Construction Dominance:

- Global Infrastructure Development: Significant investments in residential, commercial, and industrial construction projects worldwide.

- Energy Efficiency Regulations: Increasingly strict building codes mandating lower energy consumption, driving the demand for superior insulation materials.

- Urbanization: Rapid growth of cities and the need for modern, energy-efficient buildings.

- Retrofitting Initiatives: Government programs and private sector efforts to improve the energy performance of existing buildings.

In terms of Product Type, Hydrocarbons (HCs), particularly pentanes, currently hold a substantial market share due to their cost-effectiveness and low GWP, making them a preferred choice in many regions for PUF applications. However, Hydrofluoroolefins (HFOs) are rapidly gaining traction and are projected to witness the highest growth rate in the forecast period (2025–2033). This surge is propelled by their ultra-low GWP and zero ODP, positioning them as the future standard for environmentally conscious insulation. The transition from HFCs, driven by regulatory phase-downs, is directly fueling HFO adoption.

- Key Drivers for HFO Growth:

- Kigali Amendment and Global Phase-Downs: International agreements mandating the reduction of HFC consumption.

- Technological Advancements: Improved performance and cost-competitiveness of HFO formulations.

- Corporate Sustainability Goals: Companies seeking to reduce their environmental footprint by adopting low-GWP blowing agents.

Regionally, Asia Pacific is emerging as a dominant market, fueled by rapid industrialization, a growing middle class, and substantial investments in infrastructure and construction. Countries like China and India are major contributors to this growth. The region's expanding manufacturing base for appliances and automotive components also contributes to the overall demand for blowing agents.

Blowing Agents Industry Product Developments

The blowing agents industry is witnessing a flurry of product developments focused on sustainability, performance, and regulatory compliance. Companies are heavily investing in the research and development of Hydrofluoroolefins (HFOs), such as HFO-1233zd, offering near-zero Global Warming Potential (GWP) and zero Ozone Depletion Potential (ODP). These next-generation blowing agents are gaining significant market traction, especially in rigid polyurethane foam applications for insulation in construction and appliances. Furthermore, advancements are being made in formulating blowing agent blends that optimize thermal conductivity, fire retardancy, and processing efficiency, providing competitive advantages to manufacturers. The emphasis is on creating solutions that facilitate lightweighting in automotive and packaging sectors while adhering to evolving environmental standards.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the blowing agents market from 2019 to 2033, with a base year of 2025. The market is segmented by Product Type, including Hydrochlorofluorocarbons (HCFCs), Hydrofluorocarbons (HFCs), Hydrocarbons (HCs), Hydrofluoroolefin (HFO), and Other Product Types. It further categorizes the market by Foam Type: Polyurethane Foam, Polystyrene Foam, Phenolic Foam, Polypropylene Foam, Polyethylene Foam, and Other Foam Types. The Application segmentation covers Building and Construction, Automotive, Bedding and Furniture, Appliances, Packaging, and Other Applications. Market sizes, growth projections, and competitive dynamics are analyzed for each segment.

- Product Type: HFOs are projected for significant growth due to environmental regulations.

- Foam Type: Polyurethane Foam remains dominant due to its versatile insulation properties.

- Application: Building and Construction leads due to energy efficiency demands.

Key Drivers of Blowing Agents Industry Growth

The blowing agents industry is propelled by several key growth drivers. Foremost is the increasing global demand for energy-efficient insulation materials, driven by stringent environmental regulations and a rising awareness of climate change, particularly in the building and construction sector. The automotive industry's pursuit of lightweighting solutions to enhance fuel efficiency and reduce emissions is another significant catalyst. Technological advancements leading to the development of low-GWP blowing agents, such as HFOs, are crucial, offering environmentally superior alternatives to traditional HCFCs and HFCs. Furthermore, the expanding manufacturing base for appliances and consumer goods, especially in emerging economies, contributes to the sustained demand for blowing agents used in foam production.

Challenges in the Blowing Agents Industry Sector

The blowing agents industry faces several challenges that can impede its growth trajectory. Stringent and evolving environmental regulations, while driving innovation, can also create compliance hurdles and increase production costs, particularly for manufacturers transitioning to new technologies. The volatile pricing of raw materials, especially hydrocarbons, can impact profit margins. Supply chain disruptions, as witnessed in recent years, can affect the availability and cost of key ingredients. Moreover, the development of alternative insulation technologies and materials, though not yet posing a widespread threat, represents a potential long-term challenge. Intense competition among established players and the emergence of new market entrants also exert pressure on pricing and market share.

Emerging Opportunities in Blowing Agents Industry

Emerging opportunities within the blowing agents industry are abundant, driven by innovation and sustainability imperatives. The widespread adoption of Hydrofluoroolefins (HFOs) presents a significant growth avenue, with ongoing research focused on optimizing their performance and expanding their application range. The circular economy model is also creating opportunities for developing recyclable blowing agents and foam solutions. The increasing demand for sustainable packaging solutions, particularly in the e-commerce sector, is opening new markets for specialized blowing agents. Furthermore, the growing emphasis on smart buildings and energy-efficient infrastructure in developing nations offers substantial untapped potential. Strategic collaborations and partnerships for technology development and market access are also key opportunities for stakeholders.

Leading Players in the Blowing Agents Industry Market

- Honeywell International Inc.

- Arkema

- Nouryon

- Harp International Ltd

- Sinochem Group Co Ltd

- Zeon Corporation

- Solvay

- Form Supplies Inc (FSI)

- HCS Group GmbH

- Huntsman International LLC

- The Chemours Company

- A-Gas

- The Linde Group

- Americhem

- Lanxess

Key Developments in Blowing Agents Industry Industry

- June 2021: Arkema announced an increase in the production capacity of the insulation foam-blowing agent hydro-fluoro olefin 1233zd (HFO-1233zd) in China and the United States. The company planned to invest USD 60 million to add 15 kilotons per year of HFO capacity at its plant in Calvert City, Kentucky, United States. Additionally, Arkema will contract with Aofan to produce 5 kilotons per year in China by 2022. This development signifies a strategic move to meet the growing demand for low-GWP blowing agents in key global markets.

- November 2020: Nouryon launched a new version of its Expancel expandable microspheres, which act as a filler and blowing agent to make products lighter and reduce overall costs. This product finds major applications in specialty thin coatings, primarily for improving the printability of thermal paper labels, tickets, and other similar items. This innovation highlights the diversification of blowing agent functionalities beyond traditional foam applications.

Strategic Outlook for Blowing Agents Industry Market

The blowing agents industry is poised for sustained growth, driven by a confluence of regulatory tailwinds and evolving market demands for sustainable and high-performance materials. The ongoing global phase-down of HFCs will continue to propel the adoption of HFOs and other low-GWP alternatives, creating significant opportunities for innovation and market expansion. The building and construction sector, with its continuous focus on energy efficiency, will remain a primary growth engine. Similarly, the automotive industry's commitment to lightweighting and emissions reduction will fuel demand for advanced blowing agents. Strategic investments in R&D, capacity expansion, and geographical penetration will be crucial for market leaders to capitalize on emerging trends, such as the development of next-generation blowing agents with enhanced fire retardancy and improved thermal conductivity, ensuring long-term competitive advantage.

Blowing Agents Industry Segmentation

-

1. Product Type

- 1.1. Hydrochlorofluorocarbons (HCFCs)

- 1.2. Hydrofluorocarbons (HFCs)

- 1.3. Hydrocarbons (HCs)

- 1.4. Hydrofluoroolefin (HFO)

- 1.5. Other Product Types

-

2. Foam Type

- 2.1. Polyurethane Foam

- 2.2. Polystyrene Foam

- 2.3. Phenolic Foam

- 2.4. Polypropylene Foam

- 2.5. Polyethylene Foam

- 2.6. Other Foam Types

-

3. Application

- 3.1. Building and Construction

- 3.2. Automotive

- 3.3. Bedding and Furniture

- 3.4. Appliances

- 3.5. Packaging

- 3.6. Other Applications

Blowing Agents Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Rest of North America

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Blowing Agents Industry Regional Market Share

Geographic Coverage of Blowing Agents Industry

Blowing Agents Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Hydrochlorofluorocarbons (HCFCs)

- 5.1.2. Hydrofluorocarbons (HFCs)

- 5.1.3. Hydrocarbons (HCs)

- 5.1.4. Hydrofluoroolefin (HFO)

- 5.1.5. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Foam Type

- 5.2.1. Polyurethane Foam

- 5.2.2. Polystyrene Foam

- 5.2.3. Phenolic Foam

- 5.2.4. Polypropylene Foam

- 5.2.5. Polyethylene Foam

- 5.2.6. Other Foam Types

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Building and Construction

- 5.3.2. Automotive

- 5.3.3. Bedding and Furniture

- 5.3.4. Appliances

- 5.3.5. Packaging

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Blowing Agents Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Hydrochlorofluorocarbons (HCFCs)

- 6.1.2. Hydrofluorocarbons (HFCs)

- 6.1.3. Hydrocarbons (HCs)

- 6.1.4. Hydrofluoroolefin (HFO)

- 6.1.5. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Foam Type

- 6.2.1. Polyurethane Foam

- 6.2.2. Polystyrene Foam

- 6.2.3. Phenolic Foam

- 6.2.4. Polypropylene Foam

- 6.2.5. Polyethylene Foam

- 6.2.6. Other Foam Types

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Building and Construction

- 6.3.2. Automotive

- 6.3.3. Bedding and Furniture

- 6.3.4. Appliances

- 6.3.5. Packaging

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Asia Pacific Blowing Agents Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Hydrochlorofluorocarbons (HCFCs)

- 7.1.2. Hydrofluorocarbons (HFCs)

- 7.1.3. Hydrocarbons (HCs)

- 7.1.4. Hydrofluoroolefin (HFO)

- 7.1.5. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Foam Type

- 7.2.1. Polyurethane Foam

- 7.2.2. Polystyrene Foam

- 7.2.3. Phenolic Foam

- 7.2.4. Polypropylene Foam

- 7.2.5. Polyethylene Foam

- 7.2.6. Other Foam Types

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Building and Construction

- 7.3.2. Automotive

- 7.3.3. Bedding and Furniture

- 7.3.4. Appliances

- 7.3.5. Packaging

- 7.3.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. North America Blowing Agents Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Hydrochlorofluorocarbons (HCFCs)

- 8.1.2. Hydrofluorocarbons (HFCs)

- 8.1.3. Hydrocarbons (HCs)

- 8.1.4. Hydrofluoroolefin (HFO)

- 8.1.5. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Foam Type

- 8.2.1. Polyurethane Foam

- 8.2.2. Polystyrene Foam

- 8.2.3. Phenolic Foam

- 8.2.4. Polypropylene Foam

- 8.2.5. Polyethylene Foam

- 8.2.6. Other Foam Types

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Building and Construction

- 8.3.2. Automotive

- 8.3.3. Bedding and Furniture

- 8.3.4. Appliances

- 8.3.5. Packaging

- 8.3.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Blowing Agents Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Hydrochlorofluorocarbons (HCFCs)

- 9.1.2. Hydrofluorocarbons (HFCs)

- 9.1.3. Hydrocarbons (HCs)

- 9.1.4. Hydrofluoroolefin (HFO)

- 9.1.5. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Foam Type

- 9.2.1. Polyurethane Foam

- 9.2.2. Polystyrene Foam

- 9.2.3. Phenolic Foam

- 9.2.4. Polypropylene Foam

- 9.2.5. Polyethylene Foam

- 9.2.6. Other Foam Types

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Building and Construction

- 9.3.2. Automotive

- 9.3.3. Bedding and Furniture

- 9.3.4. Appliances

- 9.3.5. Packaging

- 9.3.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Blowing Agents Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Hydrochlorofluorocarbons (HCFCs)

- 10.1.2. Hydrofluorocarbons (HFCs)

- 10.1.3. Hydrocarbons (HCs)

- 10.1.4. Hydrofluoroolefin (HFO)

- 10.1.5. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Foam Type

- 10.2.1. Polyurethane Foam

- 10.2.2. Polystyrene Foam

- 10.2.3. Phenolic Foam

- 10.2.4. Polypropylene Foam

- 10.2.5. Polyethylene Foam

- 10.2.6. Other Foam Types

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Building and Construction

- 10.3.2. Automotive

- 10.3.3. Bedding and Furniture

- 10.3.4. Appliances

- 10.3.5. Packaging

- 10.3.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Blowing Agents Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Hydrochlorofluorocarbons (HCFCs)

- 11.1.2. Hydrofluorocarbons (HFCs)

- 11.1.3. Hydrocarbons (HCs)

- 11.1.4. Hydrofluoroolefin (HFO)

- 11.1.5. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Foam Type

- 11.2.1. Polyurethane Foam

- 11.2.2. Polystyrene Foam

- 11.2.3. Phenolic Foam

- 11.2.4. Polypropylene Foam

- 11.2.5. Polyethylene Foam

- 11.2.6. Other Foam Types

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Building and Construction

- 11.3.2. Automotive

- 11.3.3. Bedding and Furniture

- 11.3.4. Appliances

- 11.3.5. Packaging

- 11.3.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Honeywell International Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Arkema

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Nouryon

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Harp International Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sinochem Group Co Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Zeon Corporation*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Solvay

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Form Supplies Inc (FSI)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 HCS Group GmbH

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Huntsman International LLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 The Chemours Company

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 A-Gas

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 The Linde Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Americhem

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Lanxess

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Honeywell International Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Blowing Agents Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Blowing Agents Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 3: Asia Pacific Blowing Agents Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: Asia Pacific Blowing Agents Industry Revenue (Million), by Foam Type 2025 & 2033

- Figure 5: Asia Pacific Blowing Agents Industry Revenue Share (%), by Foam Type 2025 & 2033

- Figure 6: Asia Pacific Blowing Agents Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: Asia Pacific Blowing Agents Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Asia Pacific Blowing Agents Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Asia Pacific Blowing Agents Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Blowing Agents Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 11: North America Blowing Agents Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: North America Blowing Agents Industry Revenue (Million), by Foam Type 2025 & 2033

- Figure 13: North America Blowing Agents Industry Revenue Share (%), by Foam Type 2025 & 2033

- Figure 14: North America Blowing Agents Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: North America Blowing Agents Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: North America Blowing Agents Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: North America Blowing Agents Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Blowing Agents Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 19: Europe Blowing Agents Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: Europe Blowing Agents Industry Revenue (Million), by Foam Type 2025 & 2033

- Figure 21: Europe Blowing Agents Industry Revenue Share (%), by Foam Type 2025 & 2033

- Figure 22: Europe Blowing Agents Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Europe Blowing Agents Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Europe Blowing Agents Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Blowing Agents Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Blowing Agents Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 27: South America Blowing Agents Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: South America Blowing Agents Industry Revenue (Million), by Foam Type 2025 & 2033

- Figure 29: South America Blowing Agents Industry Revenue Share (%), by Foam Type 2025 & 2033

- Figure 30: South America Blowing Agents Industry Revenue (Million), by Application 2025 & 2033

- Figure 31: South America Blowing Agents Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: South America Blowing Agents Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: South America Blowing Agents Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Blowing Agents Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 35: Middle East and Africa Blowing Agents Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: Middle East and Africa Blowing Agents Industry Revenue (Million), by Foam Type 2025 & 2033

- Figure 37: Middle East and Africa Blowing Agents Industry Revenue Share (%), by Foam Type 2025 & 2033

- Figure 38: Middle East and Africa Blowing Agents Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Middle East and Africa Blowing Agents Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East and Africa Blowing Agents Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Blowing Agents Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Blowing Agents Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Blowing Agents Industry Revenue Million Forecast, by Foam Type 2020 & 2033

- Table 3: Global Blowing Agents Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Blowing Agents Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Blowing Agents Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 6: Global Blowing Agents Industry Revenue Million Forecast, by Foam Type 2020 & 2033

- Table 7: Global Blowing Agents Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Blowing Agents Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: China Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: India Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Japan Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: South Korea Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Asia Pacific Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Blowing Agents Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 15: Global Blowing Agents Industry Revenue Million Forecast, by Foam Type 2020 & 2033

- Table 16: Global Blowing Agents Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 17: Global Blowing Agents Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: United States Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Canada Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of North America Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Blowing Agents Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 22: Global Blowing Agents Industry Revenue Million Forecast, by Foam Type 2020 & 2033

- Table 23: Global Blowing Agents Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Blowing Agents Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Germany Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: United Kingdom Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: France Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Italy Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Blowing Agents Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 31: Global Blowing Agents Industry Revenue Million Forecast, by Foam Type 2020 & 2033

- Table 32: Global Blowing Agents Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 33: Global Blowing Agents Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: Brazil Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Argentina Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of South America Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Blowing Agents Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 38: Global Blowing Agents Industry Revenue Million Forecast, by Foam Type 2020 & 2033

- Table 39: Global Blowing Agents Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Blowing Agents Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: Saudi Arabia Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: South Africa Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: Rest of Middle East and Africa Blowing Agents Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Blowing Agents Industry?

The projected CAGR is approximately 5.51%.

2. Which companies are prominent players in the Blowing Agents Industry?

Key companies in the market include Honeywell International Inc, Arkema, Nouryon, Harp International Ltd, Sinochem Group Co Ltd, Zeon Corporation*List Not Exhaustive, Solvay, Form Supplies Inc (FSI), HCS Group GmbH, Huntsman International LLC, The Chemours Company, A-Gas, The Linde Group, Americhem, Lanxess.

3. What are the main segments of the Blowing Agents Industry?

The market segments include Product Type, Foam Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.90 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Demand for Polymeric Insulation Foams for Buildings. Automotive. and Appliances; Increasing Demand for Foam Blowing Agents in the Manufacturing of Polyurethane Foams.

6. What are the notable trends driving market growth?

Increasing Demand from the Building and Construction Industry.

7. Are there any restraints impacting market growth?

Stringent Environmental Regulations Regarding Blowing Agents; Impact of COVID-; Other Restraints.

8. Can you provide examples of recent developments in the market?

In June 2021, Arkema has announced to increase in the production capacity of the insulation foam-blowing agent hydro-fluoro olefin 1233zd (HFO-1233zd) in the China and United States. Specifically, the company has planned to spend USD 60 million to add 15 kilotons per year of capacity for the HFO at its plant in Calvert City, Kentucky of United States. Moreover, the company will contract with Aofan to produce 5 kilotons per year in China by 2022.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Blowing Agents Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Blowing Agents Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Blowing Agents Industry?

To stay informed about further developments, trends, and reports in the Blowing Agents Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence