Key Insights

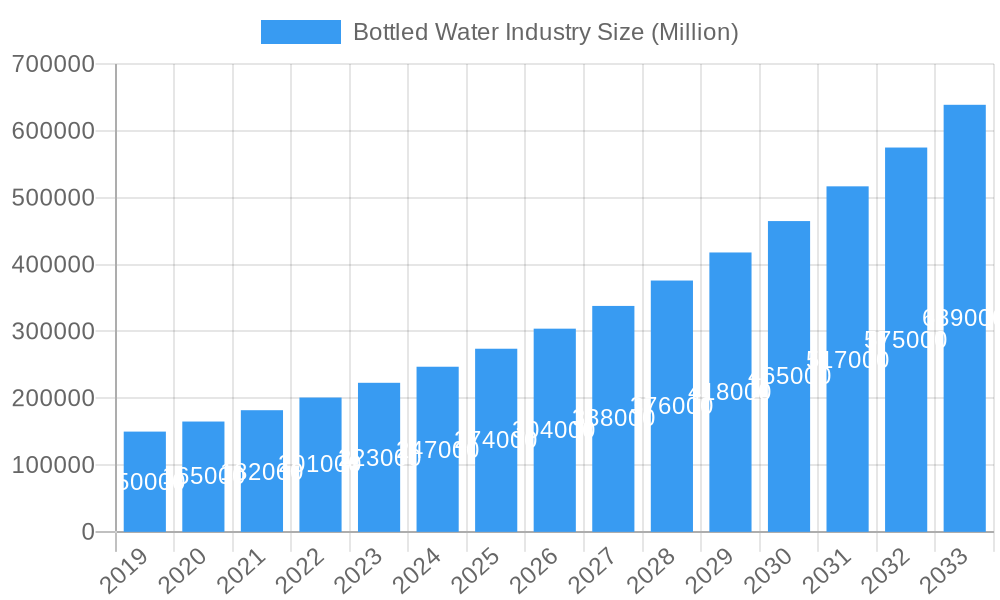

The global bottled water market is projected for substantial expansion, expected to reach $353.61 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 5.3% through 2033. This growth is driven by increasing consumer preference for healthier beverage options, heightened health consciousness, and the perceived safety of bottled water, particularly in areas with water quality concerns. Rising disposable incomes in emerging economies are also fueling demand. Key growth factors include escalating urbanization, a trend towards more active lifestyles, and product innovation, such as functional and flavored waters, catering to diverse consumer preferences and the demand for convenient hydration solutions.

Bottled Water Industry Market Size (In Billion)

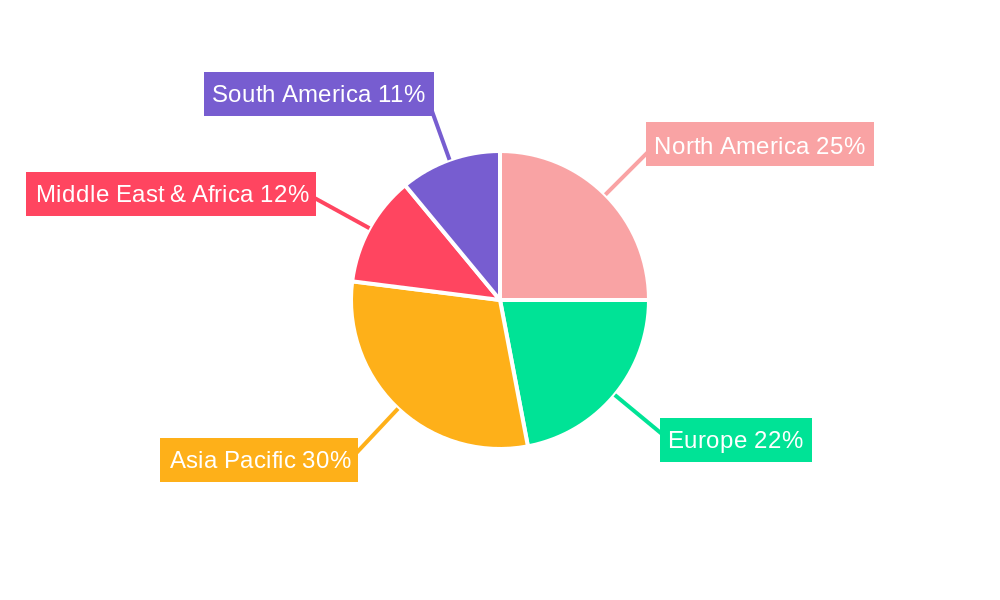

The market is segmented by product type, with "Still Water" leading, followed by the rapidly growing "Sparkling Water" segment. "Functional Water," enriched with vitamins and minerals, is a high-growth niche aligned with wellness trends. Distribution channels include "Supermarkets and Hypermarkets," alongside increasingly popular "Home and Office Delivery" services and the "On-trade" sector (restaurants, hotels). Geographically, Asia Pacific is anticipated to lead growth due to its large population and rising health awareness. North America and Europe are mature markets, while the Middle East & Africa and South America offer significant untapped potential. The competitive landscape features major players such as Nestlé S.A., PepsiCo Inc., and Agthia Group PJSC, alongside innovative brands like Spindrift and Hint Inc., all focused on product differentiation and strategic market expansion.

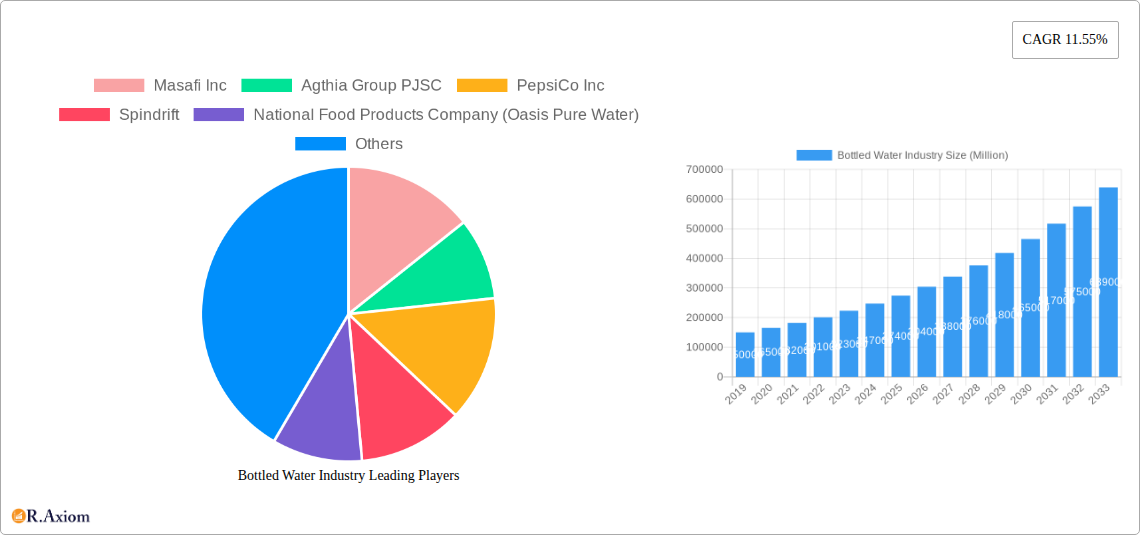

Bottled Water Industry Company Market Share

Bottled Water Industry Market Concentration & Innovation

The global bottled water market exhibits a moderate to high concentration, with major players like Nestlé S.A., PepsiCo Inc., and Agthia Group PJSC holding significant market shares, estimated to be in the range of tens of billions USD. Innovation is a key differentiator, driven by increasing consumer demand for healthier and sustainable options. Companies are investing heavily in advanced filtration technologies, eco-friendly packaging solutions, and functional water formulations. Regulatory frameworks are evolving to ensure product safety, quality, and environmental responsibility, influencing product development and market entry strategies. The threat of product substitutes, such as tap water purifiers and flavored beverages, remains a consideration, but the convenience and perceived quality of bottled water continue to drive demand. End-user trends lean towards premiumization, health and wellness, and sustainability, compelling companies to adapt their offerings. Merger and acquisition (M&A) activities are prevalent, with strategic acquisitions aimed at expanding product portfolios and geographical reach. For instance, Agthia Group PJSC's acquisition of Nabil Foods in May 2021, valued at several hundred million USD, exemplifies this trend, integrating diversified food and beverage businesses. The market share of key players fluctuates, with some estimated to hold between 5% and 15% of the global market.

Bottled Water Industry Industry Trends & Insights

The bottled water industry is experiencing robust growth, fueled by a confluence of factors that are reshaping consumer behavior and market dynamics. A significant driver of this expansion is the increasing global health consciousness, with consumers actively seeking healthier alternatives to sugary beverages. This trend is further amplified by growing concerns over the quality and safety of municipal tap water in many regions. The market penetration of bottled water continues to rise, particularly in emerging economies where access to clean drinking water is a persistent challenge. The Compound Annual Growth Rate (CAGR) for the bottled water market is projected to remain strong, estimated between 5% and 7% over the forecast period of 2025–2033. Technological disruptions are playing a pivotal role, with innovations in water purification, such as reverse osmosis and advanced filtration systems, enhancing the perceived purity and quality of bottled water. Furthermore, the development of smart packaging solutions that monitor water quality and provide traceability is gaining traction. Consumer preferences are evolving beyond basic hydration to include specialized functional waters fortified with vitamins, minerals, and other beneficial ingredients, catering to specific health and wellness needs. This segment is anticipated to witness above-average growth. The competitive landscape is intensifying, characterized by the strategic expansion of established brands and the emergence of niche players focusing on premium and sustainable offerings. Companies are actively engaging in product differentiation through unique sourcing, enhanced taste profiles, and compelling brand narratives. The overall market value is estimated to reach hundreds of billions USD by the end of the forecast period.

Dominant Markets & Segments in Bottled Water Industry

The bottled water industry's dominance is sculpted by a complex interplay of regional economic policies, robust infrastructure, and evolving consumer lifestyles, with Still Water emerging as the undisputed leader across most global markets.

Still Water: This segment commands the largest market share, estimated to be over 70% of the total bottled water market value, projected to exceed hundreds of billions USD in value by 2033. Its dominance is driven by its universal appeal as a primary source of hydration, its perceived health benefits, and its broad applicability in various consumption occasions. Economic policies in developing nations often prioritize access to safe drinking water, making still bottled water a critical commodity.

Supermarkets and Hypermarkets: This distribution channel is the most significant, accounting for an estimated 40-50% of total bottled water sales. The wide reach, high foot traffic, and diverse product offerings within these retail environments make them the primary point of purchase for the majority of consumers. The strategic placement and promotional activities within these channels significantly influence purchasing decisions.

North America and Asia Pacific: These regions are identified as the dominant markets in terms of consumption volume and value, with the North American market alone valued at tens of billions USD. North America's dominance is attributed to high disposable incomes, established consumer habits, and a strong preference for convenience and premium products. The Asia Pacific region, with its rapidly growing population and increasing urbanization, presents immense growth potential, driven by improving living standards and a heightened awareness of water quality issues.

Functional Water: While smaller in market share compared to still water, the functional water segment is experiencing the highest growth rate, with a projected CAGR of over 8% during the forecast period. This growth is fueled by increasing consumer interest in health and wellness, leading to a demand for beverages offering added benefits such as enhanced hydration, immunity support, or stress relief.

Home and Office Delivery: This channel is experiencing significant expansion, estimated to account for 15-20% of the market share, with a projected value in the tens of billions USD. The increasing demand for convenience and the growing number of remote work arrangements have propelled the popularity of subscription-based delivery services, offering a steady and reliable supply of bottled water directly to consumers' doorsteps.

Bottled Water Industry Product Developments

Product innovation in the bottled water industry is rapidly evolving, driven by sustainability and health trends. Companies are prioritizing the development of eco-friendly packaging, such as 100% plant-based bottles and biodegradable materials, to reduce environmental impact. The launch of "Source" by Masafi Inc. in September 2021, a premium and sustainable bottle produced via hydro panel technology, exemplifies this shift. Functional water formulations are also gaining prominence, with products fortified with vitamins, minerals, and natural flavors to cater to health-conscious consumers. These developments aim to enhance brand appeal, capture niche market segments, and provide competitive advantages in an increasingly discerning market.

Report Scope & Segmentation Analysis

This comprehensive report analyzes the bottled water industry across various key segments. The Type segmentation includes Still Water, which represents the largest market share due to its widespread appeal and primary use for hydration. Sparkling Water is a growing segment, driven by consumer preference for refreshing, low-calorie alternatives. Functional Water, while currently smaller, is poised for significant growth as consumers increasingly seek health benefits beyond basic hydration.

In terms of Distribution Channel, Supermarkets and Hypermarkets dominate sales due to their extensive reach and convenience. Convenience Stores cater to immediate consumption needs, while Home and Office Delivery services are rapidly expanding, offering enhanced convenience and subscription models. The On-trade segment, encompassing restaurants and hotels, also contributes significantly to market volume. Other Distribution Channels, including e-commerce and direct-to-consumer platforms, are emerging as vital avenues for market penetration and growth.

Key Drivers of Bottled Water Industry Growth

The bottled water industry's growth is propelled by several interconnected drivers. Increasing global awareness of health and wellness directly fuels demand for pure, safe hydration alternatives to sugary drinks. Economic development and rising disposable incomes in emerging markets are enhancing affordability and accessibility. Technological advancements in purification and packaging are improving product quality and sustainability, appealing to environmentally conscious consumers. Furthermore, stringent regulations regarding tap water safety in many regions indirectly boost bottled water consumption. The convenience and perceived premium quality associated with bottled water continue to make it a preferred choice for a significant consumer base.

Challenges in the Bottled Water Industry Sector

Despite its robust growth, the bottled water industry faces several challenges. Environmental concerns surrounding plastic waste and single-use packaging are leading to increased scrutiny and regulatory pressure for sustainable alternatives. Supply chain disruptions, influenced by geopolitical events and logistical complexities, can impact production and distribution costs. Intense competition from both established brands and private labels can lead to price wars and reduced profit margins. Furthermore, negative perceptions regarding the environmental impact of transporting bottled water and the availability of safe tap water in developed regions present ongoing hurdles that require strategic addressing.

Emerging Opportunities in Bottled Water Industry

The bottled water industry is ripe with emerging opportunities. The rapidly growing functional water segment, offering enhanced health benefits, presents substantial growth potential. Innovations in sustainable packaging, such as biodegradable materials and refillable systems, cater to growing eco-consciousness. The expansion of e-commerce and direct-to-consumer models allows for greater market reach and personalized customer experiences. Furthermore, emerging markets with increasing populations and developing infrastructure offer significant untapped potential for market penetration and growth, especially for affordable and accessible bottled water solutions.

Leading Players in the Bottled Water Industry Market

- Masafi Inc.

- Agthia Group PJSC

- PepsiCo Inc.

- Spindrift

- National Food Products Company (Oasis Pure Water)

- AL Ghadeer Drinking Water LLC

- Hint Inc.

- Mai Dubai

- Dubai Crystal Mineral Water & Refreshments L L C Co

- Nestlé S A

Key Developments in Bottled Water Industry Industry

- September 2021: Masafi Inc. launched "Source," a premium and sustainable water bottle in the UAE, produced by hydro panel technology, using solar energy to create premium drinking water.

- May 2021: Agthia Group PJSC announced the strategic acquisition of Nabil Foods to expand its product portfolio, including processed protein, bottled water, convenience foods, flour, and animal feed businesses.

- April 2020: The National Food Products Company (Oasis Pure Water) introduced the first boxed drinking water in Tetra Pak in the region in a 330-ml size, featuring completely biodegradable and recyclable packaging, with paper sourced from FSC-certified forests.

- February 2020: Agthia Group PJSC (Al Ain) introduced 100% plant-based water bottles (Al Ain Plant Bottle) in the United Arab Emirates, with the entire bottle and cap made of plant materials and fully compostable within 80 days.

Strategic Outlook for Bottled Water Industry Market

The strategic outlook for the bottled water industry remains highly positive, driven by persistent global trends in health consciousness and the demand for safe, convenient hydration. Future growth will be significantly influenced by continued innovation in functional water offerings, catering to specialized dietary and wellness needs. The industry's ability to embrace and implement truly sustainable packaging solutions will be paramount in navigating regulatory pressures and consumer expectations. Expansion into underserved emerging markets, coupled with the leveraging of e-commerce platforms for direct consumer engagement, presents substantial opportunities. Strategic partnerships and mergers will continue to shape the competitive landscape, enabling companies to achieve economies of scale and broaden their product portfolios, ensuring long-term market resilience and profitability.

Bottled Water Industry Segmentation

-

1. Type

- 1.1. Still Water

- 1.2. Sparkling Water

- 1.3. Functional Water

-

2. Distribution Channel

- 2.1. Supermarkets and Hypermarkets

- 2.2. Convenience Stores

- 2.3. Home and Office Delivery

- 2.4. On-trade

- 2.5. Other Distribution Channels

Bottled Water Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Bottled Water Industry Regional Market Share

Geographic Coverage of Bottled Water Industry

Bottled Water Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Still Water

- 5.1.2. Sparkling Water

- 5.1.3. Functional Water

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets and Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Home and Office Delivery

- 5.2.4. On-trade

- 5.2.5. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Bottled Water Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Still Water

- 6.1.2. Sparkling Water

- 6.1.3. Functional Water

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets and Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Home and Office Delivery

- 6.2.4. On-trade

- 6.2.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Bottled Water Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Still Water

- 7.1.2. Sparkling Water

- 7.1.3. Functional Water

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets and Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Home and Office Delivery

- 7.2.4. On-trade

- 7.2.5. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America Bottled Water Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Still Water

- 8.1.2. Sparkling Water

- 8.1.3. Functional Water

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets and Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Home and Office Delivery

- 8.2.4. On-trade

- 8.2.5. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Bottled Water Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Still Water

- 9.1.2. Sparkling Water

- 9.1.3. Functional Water

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets and Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Home and Office Delivery

- 9.2.4. On-trade

- 9.2.5. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa Bottled Water Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Still Water

- 10.1.2. Sparkling Water

- 10.1.3. Functional Water

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets and Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Home and Office Delivery

- 10.2.4. On-trade

- 10.2.5. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific Bottled Water Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Still Water

- 11.1.2. Sparkling Water

- 11.1.3. Functional Water

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets and Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Home and Office Delivery

- 11.2.4. On-trade

- 11.2.5. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Masafi Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Agthia Group PJSC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 PepsiCo Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Spindrift

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 National Food Products Company (Oasis Pure Water)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AL Ghadeer Drinking Water LLC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hint Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mai Dubai*List Not Exhaustive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Dubai Crystal Mineral Water & Refreshments L L C Co

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nestlé S A

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Masafi Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Bottled Water Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Bottled Water Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Bottled Water Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Bottled Water Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 5: North America Bottled Water Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America Bottled Water Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Bottled Water Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Bottled Water Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: South America Bottled Water Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America Bottled Water Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: South America Bottled Water Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: South America Bottled Water Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Bottled Water Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Bottled Water Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Bottled Water Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Bottled Water Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Europe Bottled Water Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Europe Bottled Water Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Bottled Water Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Bottled Water Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa Bottled Water Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa Bottled Water Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 23: Middle East & Africa Bottled Water Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Middle East & Africa Bottled Water Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Bottled Water Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Bottled Water Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific Bottled Water Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific Bottled Water Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific Bottled Water Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific Bottled Water Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Bottled Water Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Bottled Water Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Bottled Water Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global Bottled Water Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Bottled Water Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Bottled Water Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Bottled Water Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Bottled Water Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Bottled Water Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global Bottled Water Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Bottled Water Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Bottled Water Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global Bottled Water Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Bottled Water Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global Bottled Water Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global Bottled Water Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Bottled Water Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global Bottled Water Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 39: Global Bottled Water Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Bottled Water Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bottled Water Industry?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the Bottled Water Industry?

Key companies in the market include Masafi Inc, Agthia Group PJSC, PepsiCo Inc, Spindrift, National Food Products Company (Oasis Pure Water), AL Ghadeer Drinking Water LLC, Hint Inc, Mai Dubai*List Not Exhaustive, Dubai Crystal Mineral Water & Refreshments L L C Co, Nestlé S A.

3. What are the main segments of the Bottled Water Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 353.61 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Protein-Rich Food; Increasing Demand for Plant-Based and Organic Ingredients.

6. What are the notable trends driving market growth?

Surge in the Demand for Functional/Fortified and Flavored Water.

7. Are there any restraints impacting market growth?

Presence of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

September 2021: Masafi Inc. launched "Source", the premium and sustainable water bottle in the UAE, produced by hydro panel technology, which uses the energy and heat of the sun to create premium drinking water.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Bottled Water Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Bottled Water Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Bottled Water Industry?

To stay informed about further developments, trends, and reports in the Bottled Water Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence