Key Insights

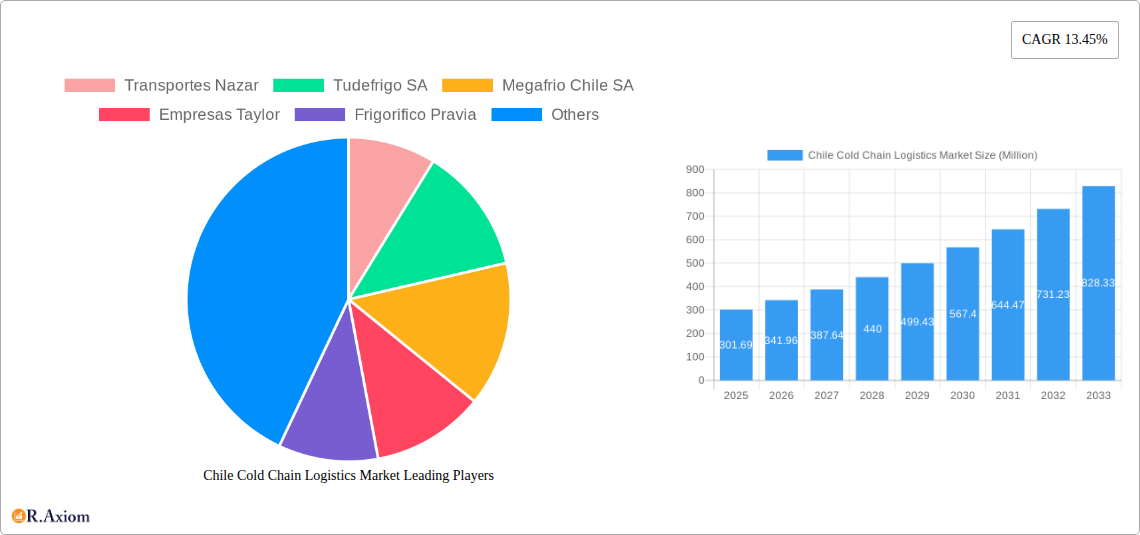

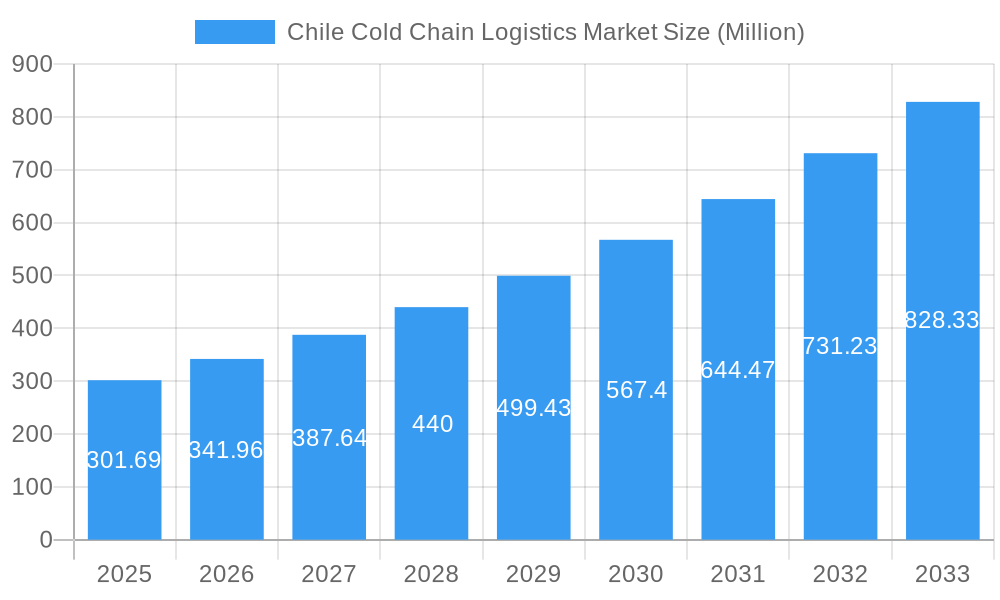

The Chilean cold chain logistics market, valued at $301.69 million in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 13.45% from 2025 to 2033. This expansion is driven by several key factors. The increasing demand for fresh produce, dairy, meat, and processed foods, fueled by a growing population and rising disposable incomes, is a significant driver. Furthermore, the burgeoning e-commerce sector in Chile is creating a heightened need for efficient and reliable cold chain solutions to ensure the quality and safety of temperature-sensitive goods during delivery. The expansion of the pharmaceutical and life sciences industries further contributes to market growth, as these sectors require stringent temperature-controlled storage and transportation for sensitive products. Specific service segments like value-added services (blast freezing, labeling, inventory management) are experiencing particularly strong growth, reflecting a trend toward greater supply chain sophistication and efficiency. However, challenges remain, including the need for improved infrastructure in certain regions and the high cost of maintaining cold chain equipment and operations. Major players like Transportes Nazar, Tudefrigo SA, and Megafrio Chile SA are actively shaping the market landscape through strategic investments and expansion initiatives. The market's segmentation across service types (storage, transportation, value-added services), temperature requirements (chilled, frozen, ambient), and end-user industries (horticulture, dairy, meat, pharmaceuticals) offers diverse opportunities for growth and specialization within the Chilean cold chain logistics sector.

Chile Cold Chain Logistics Market Market Size (In Million)

The competitive landscape is marked by a mix of established players and emerging companies. While established companies like Transportes Nazar and Tudefrigo SA benefit from existing infrastructure and customer relationships, emerging players are innovating with technology and services to gain market share. This competitive dynamic fosters innovation and efficiency improvements within the industry, ultimately benefiting consumers and businesses alike. The forecast period (2025-2033) is expected to witness continued expansion, driven by sustained economic growth, evolving consumer preferences, and the ongoing modernization of the Chilean cold chain logistics infrastructure. However, the market will need to address ongoing challenges related to sustainability, regulatory compliance, and workforce development to achieve its full potential.

Chile Cold Chain Logistics Market Company Market Share

Chile Cold Chain Logistics Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Chile Cold Chain Logistics market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report unveils the market's dynamics, growth drivers, challenges, and emerging opportunities. The market size is projected to reach xx Million by 2033, presenting significant investment potential.

Chile Cold Chain Logistics Market Concentration & Innovation

The Chilean cold chain logistics market exhibits a moderately concentrated landscape, with a few key players commanding significant market share. Transportes Nazar, Tudefrigo SA, Megafrio Chile SA, Empresas Taylor, Frigorifico Pravia, Friofort SA, Frigorificos Puerto Montt, and Ceva Logistics are prominent examples, alongside 63 other companies, including Emergent Cold LatAm and TIBA Chile. However, the market also features a substantial number of smaller, regional players. Market share data reveals that the top 5 players hold approximately xx% of the market share in 2025, indicating opportunities for both consolidation and niche market penetration.

Innovation is driven by the increasing demand for efficient and reliable cold chain solutions, particularly within the perishable goods sector. Technological advancements, such as IoT-enabled monitoring systems and automated warehousing, are transforming the industry. Stringent regulatory frameworks focusing on food safety and hygiene standards are also influencing innovation, fostering the adoption of advanced technologies to ensure product quality and traceability. Furthermore, the growing popularity of value-added services like blast freezing and labeling drives further innovation within the sector. M&A activity has been moderate, with a few notable deals totaling approximately xx Million in the last five years, primarily focused on expanding geographical reach and service offerings. This consolidation trend is expected to continue, further shaping the market landscape. Product substitution is limited, primarily driven by technological improvements within existing services rather than entirely new offerings. End-user trends towards higher quality standards and traceability are also prompting significant innovation across the entire cold chain ecosystem.

Chile Cold Chain Logistics Market Industry Trends & Insights

The Chilean cold chain logistics market is experiencing robust growth, driven by several key factors. The expanding horticulture sector, particularly the export of fresh fruits and vegetables, significantly contributes to the market's expansion. Increased consumer demand for fresh and high-quality food products fuels the need for efficient cold chain solutions. Technological disruptions, specifically the implementation of advanced tracking and monitoring systems, improve efficiency, reduce waste, and enhance traceability. A compound annual growth rate (CAGR) of xx% is projected for the forecast period (2025-2033), driven by increased investments in infrastructure and a growing focus on sustainability. Market penetration of advanced technologies like IoT and blockchain is increasing steadily, reaching approximately xx% in 2025. Competitive dynamics are characterized by a mix of intense competition among established players and the emergence of innovative startups. The focus on value-added services, customization of cold chain solutions to specific client needs, and strategic partnerships are shaping the competitive landscape.

Dominant Markets & Segments in Chile Cold Chain Logistics Market

The central and southern regions of Chile are dominant due to the concentration of agricultural production and export activities. Within the service segments, storage and transportation account for the largest market share, although value-added services are showing significant growth.

Key Drivers for Storage Dominance: Increasing demand for warehousing space, especially near ports and airports, alongside government investments in cold storage infrastructure.

Key Drivers for Transportation Dominance: The high volume of perishable goods exports and imports, necessitating efficient and reliable transportation networks.

Key Drivers for Value-Added Services Growth: Growing consumer awareness of food safety and quality, leading to an increased demand for specialized services like blast freezing and labeling.

Among temperature segments, frozen and chilled products are the leading segments, driven by the export of fruits, vegetables, and seafood. The horticulture sector, specifically fresh fruits and vegetables, is the largest end-user segment, benefiting from the robust export market. The dairy and processed food sectors also show substantial demand for cold chain solutions. The pharmaceuticals and life sciences sectors represent a niche but fast-growing segment, requiring stringent temperature control and traceability. Economic policies promoting agricultural exports, strategic infrastructure development (e.g., improved port facilities and refrigerated transportation networks), and government initiatives to enhance food safety are key drivers behind the dominance of these segments.

Chile Cold Chain Logistics Market Product Developments

Recent product innovations focus on improving temperature control, reducing waste, and enhancing traceability. Smart containers, utilizing IoT sensors and real-time data tracking, are gaining traction, providing better visibility and control throughout the supply chain. The development of more sustainable cold chain solutions, emphasizing reduced carbon emissions and environmentally friendly refrigerants, is also driving innovation. These developments provide significant competitive advantages by enhancing operational efficiency, reducing costs, and improving customer satisfaction. The market is driven by a strong fit between these innovations and the growing demand for higher quality, more sustainable, and traceable cold chain solutions.

Report Scope & Segmentation Analysis

This report segments the Chilean cold chain logistics market across various parameters:

Service: Storage, Transportation, Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) Storage is projected to maintain the largest market share, with Transportation second, followed by rapidly expanding value-added services.

Temperature: Chilled, Frozen, Ambient. Frozen and chilled segments dominate due to the nature of Chilean exports.

End-User: Horticulture (Fresh Fruits and Vegetables), Dairy Products (Milk, Ice Cream, Butter, etc.), Meat, Fish, and Poultry, Processed Food Products, Pharma, Life Sciences, and Chemicals, Other End Users. Horticulture is the largest end-user, followed by dairy and processed food segments.

Each segment shows varying growth projections, influenced by market-specific factors such as export trends and technological advancements. Competitive dynamics within each segment vary depending on the level of market concentration and the presence of niche players.

Key Drivers of Chile Cold Chain Logistics Market Growth

Several factors are driving the growth of the Chilean cold chain logistics market:

Export-Oriented Agriculture: Chile's strong agricultural exports necessitate robust cold chain infrastructure.

Technological Advancements: The adoption of IoT, AI, and other technologies improves efficiency and traceability.

Government Initiatives: Government support for infrastructure development and food safety regulations boosts the market.

Rising Consumer Demand: Increasing consumer preference for fresh and high-quality food products fuels market growth.

Challenges in the Chile Cold Chain Logistics Market Sector

The Chilean cold chain logistics market faces certain challenges:

Infrastructure Gaps: Uneven infrastructure development in certain regions can hamper efficient logistics.

High Operational Costs: Fuel costs and energy consumption can impact profitability.

Regulatory Compliance: Maintaining strict compliance with food safety and environmental regulations presents challenges.

These challenges can result in increased operational costs, potential supply chain disruptions, and a need for efficient logistics optimization to mitigate impacts.

Emerging Opportunities in Chile Cold Chain Logistics Market

The Chilean cold chain logistics market presents exciting opportunities:

Sustainable Cold Chain Solutions: Growing emphasis on environmental sustainability opens opportunities for eco-friendly technologies.

Value-Added Services: Demand for specialized services like packaging and labeling creates lucrative opportunities.

Technological Integration: Integrating advanced technologies like blockchain enhances traceability and efficiency.

These factors contribute to the overall growth potential of the market.

Leading Players in the Chile Cold Chain Logistics Market Market

- Transportes Nazar

- Tudefrigo SA

- Megafrio Chile SA

- Empresas Taylor

- Frigorifico Pravia

- Friofort SA

- Frigorificos Puerto Montt

- Ceva Logistics

- 63 Other Companies

- Emergent Cold LatAm

- TIBA Chile

Key Developments in Chile Cold Chain Logistics Market Industry

- 2022-Q4: Megafrio Chile SA invests in a new automated warehouse facility.

- 2023-Q1: Ceva Logistics launches a new temperature-controlled transportation service.

- 2023-Q3: Transportes Nazar implements a new IoT-based tracking system.

- (Further specific development examples would be included here)

Strategic Outlook for Chile Cold Chain Logistics Market Market

The Chilean cold chain logistics market exhibits significant growth potential driven by continuous expansion of the agricultural sector, increasing investments in infrastructure, and the adoption of advanced technologies. Opportunities in value-added services, sustainable cold chain solutions, and technological integration are expected to drive future growth, creating a favorable environment for both established players and new entrants. The market's trajectory suggests a promising outlook, with significant potential for expansion and innovation over the forecast period.

Chile Cold Chain Logistics Market Segmentation

-

1. Service

- 1.1. Storage

- 1.2. Transportation

- 1.3. Value-ad

-

2. Temperature

- 2.1. Chilled

- 2.2. Frozen

- 2.3. Ambient

-

3. End User

- 3.1. Horticulture (Fresh Fruits and Vegetables)

- 3.2. Dairy Products (Milk, Ice Cream, Butter, etc.)

- 3.3. Meat, Fish, and Poultry

- 3.4. Processed Food Products

- 3.5. Pharma, Life Sciences, and Chemicals

- 3.6. Other End Users

Chile Cold Chain Logistics Market Segmentation By Geography

- 1. Chile

Chile Cold Chain Logistics Market Regional Market Share

Geographic Coverage of Chile Cold Chain Logistics Market

Chile Cold Chain Logistics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.45% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Storage

- 5.1.2. Transportation

- 5.1.3. Value-ad

- 5.2. Market Analysis, Insights and Forecast - by Temperature

- 5.2.1. Chilled

- 5.2.2. Frozen

- 5.2.3. Ambient

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Horticulture (Fresh Fruits and Vegetables)

- 5.3.2. Dairy Products (Milk, Ice Cream, Butter, etc.)

- 5.3.3. Meat, Fish, and Poultry

- 5.3.4. Processed Food Products

- 5.3.5. Pharma, Life Sciences, and Chemicals

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Chile

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Chile Cold Chain Logistics Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Storage

- 6.1.2. Transportation

- 6.1.3. Value-ad

- 6.2. Market Analysis, Insights and Forecast - by Temperature

- 6.2.1. Chilled

- 6.2.2. Frozen

- 6.2.3. Ambient

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Horticulture (Fresh Fruits and Vegetables)

- 6.3.2. Dairy Products (Milk, Ice Cream, Butter, etc.)

- 6.3.3. Meat, Fish, and Poultry

- 6.3.4. Processed Food Products

- 6.3.5. Pharma, Life Sciences, and Chemicals

- 6.3.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Transportes Nazar

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Tudefrigo SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Megafrio Chile SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Empresas Taylor

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Frigorifico Pravia

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Friofort SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Frigorificos Puerto Montt

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ceva Logistics**List Not Exhaustive 6 3 Other Companie

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Emergent Cold LatAm

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 TIBA Chile

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Transportes Nazar

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Chile Cold Chain Logistics Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Chile Cold Chain Logistics Market Share (%) by Company 2025

List of Tables

- Table 1: Chile Cold Chain Logistics Market Revenue Million Forecast, by Service 2020 & 2033

- Table 2: Chile Cold Chain Logistics Market Revenue Million Forecast, by Temperature 2020 & 2033

- Table 3: Chile Cold Chain Logistics Market Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Chile Cold Chain Logistics Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Chile Cold Chain Logistics Market Revenue Million Forecast, by Service 2020 & 2033

- Table 6: Chile Cold Chain Logistics Market Revenue Million Forecast, by Temperature 2020 & 2033

- Table 7: Chile Cold Chain Logistics Market Revenue Million Forecast, by End User 2020 & 2033

- Table 8: Chile Cold Chain Logistics Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Chile Cold Chain Logistics Market?

The projected CAGR is approximately 13.45%.

2. Which companies are prominent players in the Chile Cold Chain Logistics Market?

Key companies in the market include Transportes Nazar, Tudefrigo SA, Megafrio Chile SA, Empresas Taylor, Frigorifico Pravia, Friofort SA, Frigorificos Puerto Montt, Ceva Logistics**List Not Exhaustive 6 3 Other Companie, Emergent Cold LatAm, TIBA Chile.

3. What are the main segments of the Chile Cold Chain Logistics Market?

The market segments include Service, Temperature, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 301.69 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Fruit Exports.

6. What are the notable trends driving market growth?

Growth Of E-commerce Driving The Market.

7. Are there any restraints impacting market growth?

4.; Challenges of First Mile Distribution in Chile.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Chile Cold Chain Logistics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Chile Cold Chain Logistics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Chile Cold Chain Logistics Market?

To stay informed about further developments, trends, and reports in the Chile Cold Chain Logistics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence