Key Insights

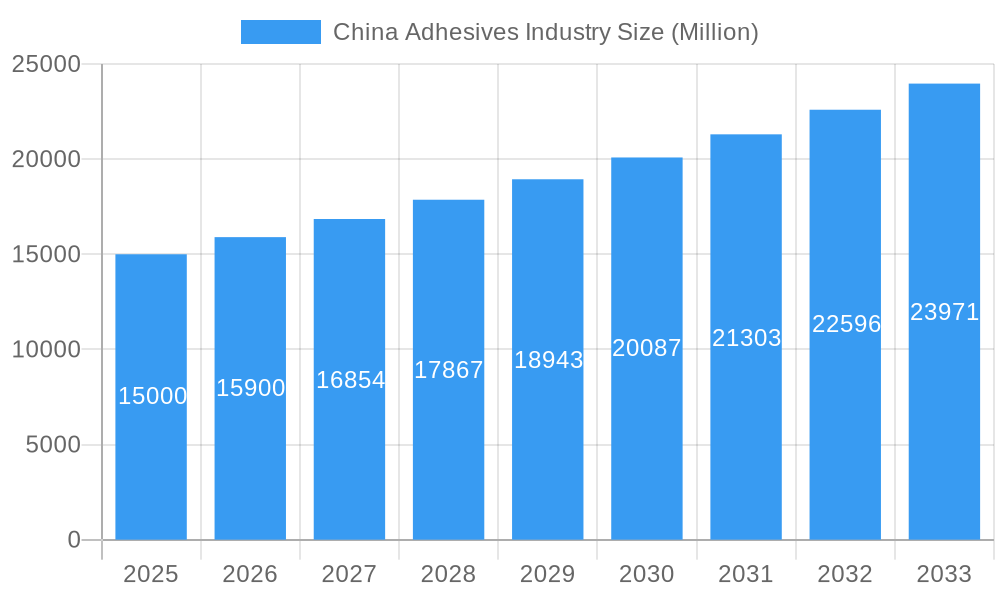

The China adhesives market, valued at approximately $6.68 billion in 2025, is experiencing robust growth with a projected Compound Annual Growth Rate (CAGR) of 6.5% from 2025 to 2033. Key drivers include the burgeoning automotive and construction sectors, increasing adoption of advanced manufacturing techniques, and the rise of e-commerce necessitating efficient packaging solutions. Trends such as the shift towards eco-friendly, water-borne adhesives and growing demand for specialized formulations in aerospace and healthcare are also stimulating market expansion. While supply chain disruptions and raw material price fluctuations present potential restraints, China's continuous industrialization and infrastructure development support a positive outlook. Hot melt and reactive adhesives dominate market share due to their versatility. Major global and domestic manufacturers are actively competing, driving innovation.

China Adhesives Industry Market Size (In Billion)

The forecast period (2025-2033) anticipates continued growth, propelled by government initiatives promoting sustainable development and technological advancements. The automotive and construction sectors are expected to maintain their dominance, with evolving adhesive types and chemistries adapting to technological innovations and application needs. Emphasis on product quality and regulatory compliance will drive formulation and manufacturing improvements, creating opportunities for market participants. The market's geographical concentration in China highlights its reliance on the country's economic trajectory and industrial expansion. Sustained growth is anticipated due to ongoing investment in infrastructure, manufacturing, and key end-use industries.

China Adhesives Industry Company Market Share

China Adhesives Industry: Market Analysis & Forecast (2025-2033)

This comprehensive report analyzes the China adhesives industry, detailing market size, segmentation, key players, growth drivers, challenges, and future outlook. The study utilizes historical data (2019-2024) and projections to 2033, with 2025 serving as the base year. It offers actionable insights for stakeholders, investors, and businesses operating within the dynamic Chinese adhesives market. Market size is presented in billions of USD.

China Adhesives Industry Market Concentration & Innovation

The Chinese adhesives market exhibits a moderately concentrated landscape, with both global giants and domestic players vying for market share. While precise market share figures for individual companies are proprietary, Henkel AG & Co KGaA, 3M, and Kangda New Materials (Group) Co Ltd are considered major players, holding a significant portion of the market. The industry is driven by innovation in adhesive technologies, responding to demands for higher performance, sustainability, and specialized applications across diverse end-user industries. Stringent environmental regulations in China are prompting a shift towards water-borne and bio-based adhesives, further fueling innovation. The regulatory framework, while evolving, presents both opportunities and challenges for companies adapting to stricter environmental standards and safety guidelines. Product substitution is a factor, particularly with the increasing availability of alternative fastening methods. End-user trends, such as the burgeoning e-commerce sector and construction boom, are influencing demand for specific adhesive types. Mergers and acquisitions (M&A) activity, as seen in Arkema's acquisition of Shanghai Zhiguan Polymer Materials in 2022, highlight strategic moves to expand market presence and technological capabilities. The total value of M&A deals in the sector from 2019-2024 is estimated at xx Million.

- Market Concentration: Moderately concentrated, with several dominant players.

- Innovation Drivers: Sustainability demands, performance requirements, and regulatory pressures.

- M&A Activity: Significant activity observed, indicating strategic consolidation.

- Regulatory Framework: Evolving, with focus on environmental standards and safety.

China Adhesives Industry Industry Trends & Insights

The China adhesives market is experiencing robust growth, driven by expanding end-user industries, particularly building and construction, packaging, and automotive. The compound annual growth rate (CAGR) for the period 2019-2024 is estimated at xx%, with projections for continued, albeit potentially moderated, growth through 2033. Technological disruptions, such as advancements in hot-melt and UV-cured adhesives, are enhancing product performance and application efficiency. Consumer preferences are shifting towards eco-friendly and high-performance adhesives, increasing demand for water-based and bio-based options. Competitive dynamics are characterized by both price competition and differentiation through technological innovation and specialized applications. Market penetration of advanced adhesive technologies remains relatively high in sectors like automotive and electronics. The market is further shaped by the rising demand for specialized adhesives in emerging sectors such as renewable energy and medical devices.

Dominant Markets & Segments in China Adhesives Industry

The building and construction sector constitutes the largest end-user segment in the China adhesives market, driven by substantial infrastructure development and urbanization. The packaging industry also exhibits significant growth due to the rise of e-commerce and consumer goods manufacturing. Within adhesive technologies, hot-melt adhesives maintain a dominant position due to their versatility and ease of application. Acrylic and polyurethane resins are the leading resin types, owing to their diverse applications and favorable cost-performance profile.

- End-User Industry Dominance: Building and Construction, Packaging

- Technology Dominance: Hot Melt Adhesives

- Resin Dominance: Acrylic, Polyurethane

- Key Drivers: Infrastructure development, urbanization, e-commerce growth, consumer goods manufacturing.

China Adhesives Industry Product Developments

Recent product innovations focus on sustainability, improved performance, and specialized applications. Examples include the introduction of bio-based adhesives and low-odor acrylic formulations. Companies are emphasizing competitive advantages through superior bonding strength, ease of use, and environmentally friendly attributes. This trend reflects the growing focus on eco-conscious manufacturing and consumer demand for sustainable products.

Report Scope & Segmentation Analysis

This report segments the China adhesives market by end-user industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, Other End-user Industries), technology (Hot Melt, Reactive, Solvent-borne, UV Cured Adhesives, Water-borne), and resin type (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Other Resins). Each segment's analysis includes growth projections, market size estimations, and competitive dynamics. For example, the building and construction segment is expected to exhibit strong growth, driven by ongoing infrastructure investments. The hot-melt adhesive technology segment benefits from its wide applicability across various end-user industries. The acrylic resin segment demonstrates high demand owing to its cost-effectiveness and diverse applications.

Key Drivers of China Adhesives Industry Growth

Key growth drivers include increasing industrialization and urbanization, leading to heightened construction activity and manufacturing output. The burgeoning e-commerce sector fuels demand for packaging adhesives. Government policies promoting sustainable development and technological advancements also contribute positively. The growing automotive industry, with its requirement for advanced adhesive solutions, further boosts market expansion.

Challenges in the China Adhesives Industry Sector

Challenges include volatile raw material prices, intense competition, and the need to comply with increasingly stringent environmental regulations. Supply chain disruptions can impact production and delivery timelines. Fluctuations in the global economy can affect demand, and maintaining a competitive edge requires ongoing investment in research and development.

Emerging Opportunities in China Adhesives Industry

Emerging opportunities include the expanding renewable energy sector, with its demand for specialized adhesives. The growing healthcare industry presents potential for advanced medical adhesive solutions. Moreover, the increasing focus on sustainability opens doors for bio-based and eco-friendly adhesives.

Leading Players in the China Adhesives Industry Market

- Henkel AG & Co KGaA

- 3M

- Kangda New Materials (Group) Co Ltd

- Beijing Comens New Materials Co Ltd

- Hubei Huitian New Materials Co Ltd

- NANPAO RESINS CHEMICAL GROUP

- Arkema Group

- Huntsman International LLC

- H B Fuller Company

- Sika A

Key Developments in China Adhesives Industry Industry

- October 2021: 3M introduced a new generation of acrylic adhesives, including 3M Scotch-Weld Low Odor Acrylic Adhesive 8700NS Series, 3M Scotch-Weld Flexible Acrylic Adhesive 8600NS Series, and 3M Scotch-Weld Nylon Bonder Structural Adhesive DP8910NS.

- December 2021: Arkema introduced a new range of disposable hygiene adhesive solutions under the Nuplaviva brand, formulated with bio-based renewable content.

- February 2022: Arkema acquired Shanghai Zhiguan Polymer Materials (PMP), specializing in hot-melt adhesives for the consumer electronics sector.

Strategic Outlook for China Adhesives Industry Market

The China adhesives market is poised for continued growth, driven by ongoing industrialization, urbanization, and technological advancements. The increasing focus on sustainability and the emergence of new applications across various sectors present significant opportunities for both established players and new entrants. Strategic investments in research and development, along with a focus on sustainable and high-performance products, will be crucial for success in this competitive and dynamic market.

China Adhesives Industry Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Footwear and Leather

- 1.5. Healthcare

- 1.6. Packaging

- 1.7. Woodworking and Joinery

- 1.8. Other End-user Industries

-

2. Technology

- 2.1. Hot Melt

- 2.2. Reactive

- 2.3. Solvent-borne

- 2.4. UV Cured Adhesives

- 2.5. Water-borne

-

3. Resin

- 3.1. Acrylic

- 3.2. Cyanoacrylate

- 3.3. Epoxy

- 3.4. Polyurethane

- 3.5. Silicone

- 3.6. VAE/EVA

- 3.7. Other Resins

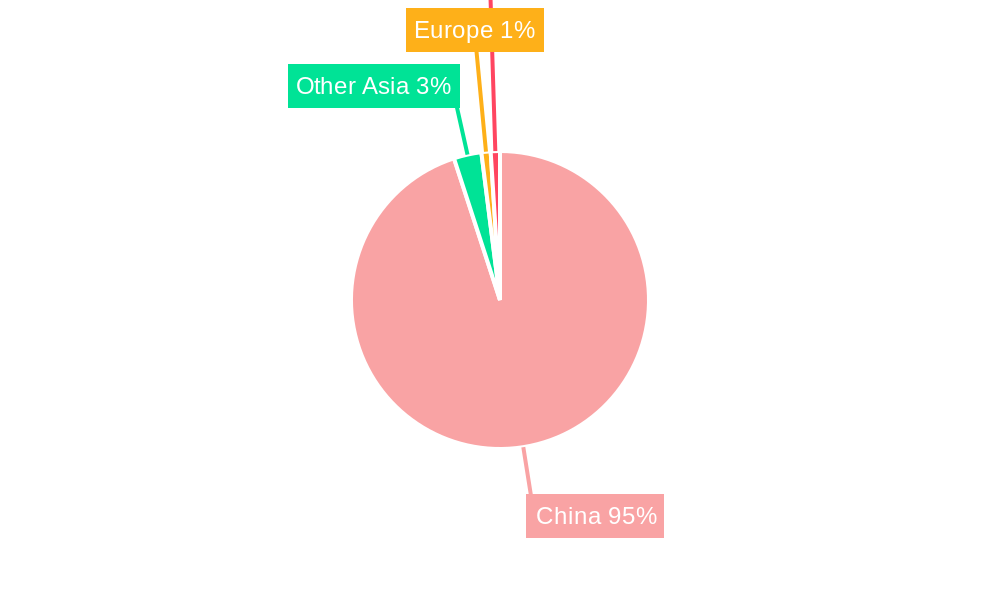

China Adhesives Industry Segmentation By Geography

- 1. China

China Adhesives Industry Regional Market Share

Geographic Coverage of China Adhesives Industry

China Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Footwear and Leather

- 5.1.5. Healthcare

- 5.1.6. Packaging

- 5.1.7. Woodworking and Joinery

- 5.1.8. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Hot Melt

- 5.2.2. Reactive

- 5.2.3. Solvent-borne

- 5.2.4. UV Cured Adhesives

- 5.2.5. Water-borne

- 5.3. Market Analysis, Insights and Forecast - by Resin

- 5.3.1. Acrylic

- 5.3.2. Cyanoacrylate

- 5.3.3. Epoxy

- 5.3.4. Polyurethane

- 5.3.5. Silicone

- 5.3.6. VAE/EVA

- 5.3.7. Other Resins

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. China Adhesives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Aerospace

- 6.1.2. Automotive

- 6.1.3. Building and Construction

- 6.1.4. Footwear and Leather

- 6.1.5. Healthcare

- 6.1.6. Packaging

- 6.1.7. Woodworking and Joinery

- 6.1.8. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Hot Melt

- 6.2.2. Reactive

- 6.2.3. Solvent-borne

- 6.2.4. UV Cured Adhesives

- 6.2.5. Water-borne

- 6.3. Market Analysis, Insights and Forecast - by Resin

- 6.3.1. Acrylic

- 6.3.2. Cyanoacrylate

- 6.3.3. Epoxy

- 6.3.4. Polyurethane

- 6.3.5. Silicone

- 6.3.6. VAE/EVA

- 6.3.7. Other Resins

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Henkel AG & Co KGaA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 3M

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Kangda New Materials (Group) Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Beijing Comens New Materials Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Hubei Huitian New Materials Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 NANPAO RESINS CHEMICAL GROUP

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Arkema Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Huntsman International LLC

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 H B Fuller Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sika A

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Henkel AG & Co KGaA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Adhesives Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Adhesives Industry Share (%) by Company 2025

List of Tables

- Table 1: China Adhesives Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: China Adhesives Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: China Adhesives Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 4: China Adhesives Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: China Adhesives Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 6: China Adhesives Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 7: China Adhesives Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 8: China Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Adhesives Industry?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the China Adhesives Industry?

Key companies in the market include Henkel AG & Co KGaA, 3M, Kangda New Materials (Group) Co Ltd, Beijing Comens New Materials Co Ltd, Hubei Huitian New Materials Co Ltd, NANPAO RESINS CHEMICAL GROUP, Arkema Group, Huntsman International LLC, H B Fuller Company, Sika A.

3. What are the main segments of the China Adhesives Industry?

The market segments include End User Industry, Technology, Resin.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.68 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Demand from the Packaging Industry; Other Drivers.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

; Impact of COVID-19 Pandemic on Global Economy.

8. Can you provide examples of recent developments in the market?

February 2022: Arkema acquired Shanghai Zhiguan Polymer Materials (PMP), specializing in hot-melt adhesives for the consumer electronics sector.December 2021: Under the Nuplaviva brand, Arkema introduced a new range of disposable hygiene adhesive solutions formulated with bio-based renewable content.October 2021: 3M introduced a new generation of acrylic adhesives, including 3M Scotch-Weld Low Odor Acrylic Adhesive 8700NS Series, 3M Scotch-Weld Flexible Acrylic Adhesive 8600NS Series, and 3M Scotch-Weld Nylon Bonder Structural Adhesive DP8910NS.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Adhesives Industry?

To stay informed about further developments, trends, and reports in the China Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence