Key Insights

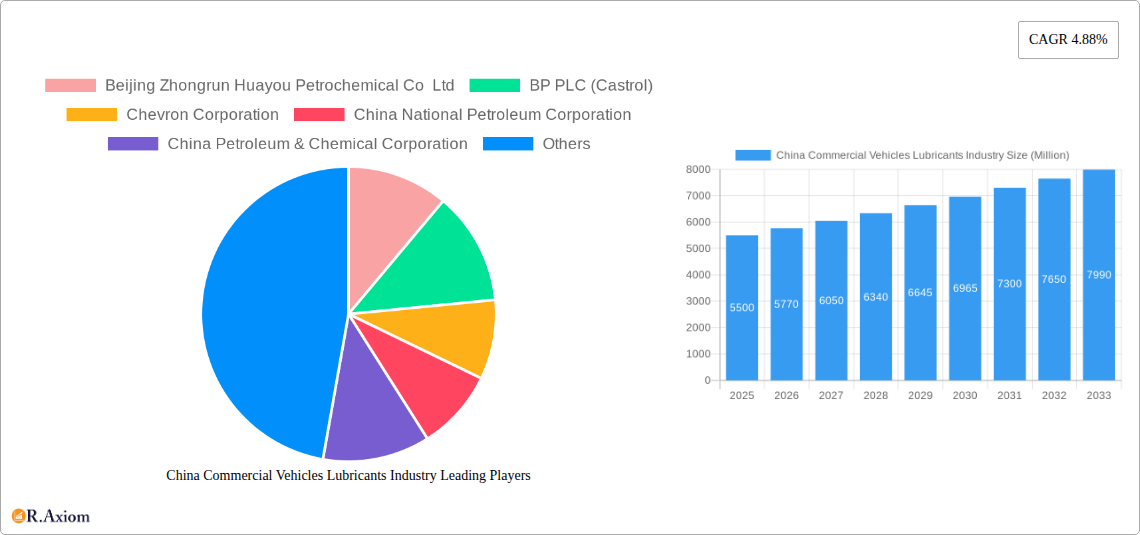

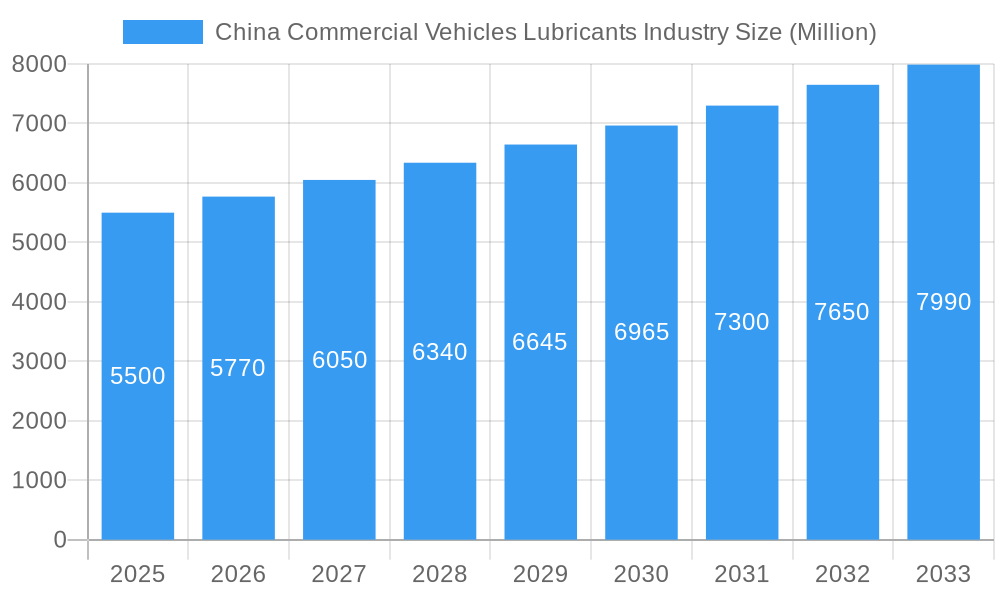

The China Commercial Vehicles Lubricants Industry is projected for significant expansion, with an estimated market size of USD 5.5 billion in the base year 2025. The market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.88%, reaching over USD 6.5 billion by 2033. This growth is fueled by the expanding logistics and transportation sector, driven by China's e-commerce boom and ongoing infrastructure development. An increasing commercial vehicle fleet, coupled with demand for enhanced performance and extended drain intervals, necessitates advanced lubricant solutions. Growing emphasis on fuel efficiency and emission reduction is accelerating the adoption of synthetic and semi-synthetic lubricants, offering superior protection and operational advantages. Key segments including Engine Oils, Greases, Hydraulic Fluids, and Transmission & Gear Oils are anticipated to experience rising demand with fleet expansion and evolving maintenance standards. Major industry players such as China National Petroleum Corporation, Sinopec, ExxonMobil, and Shell are actively investing in R&D to meet these dynamic market requirements.

China Commercial Vehicles Lubricants Industry Market Size (In Billion)

Favorable government policies supporting industrial modernization and efficient supply chains further bolster the growth of China's commercial vehicle lubricants market. However, the market faces challenges from fluctuating raw material prices, particularly for base oils and additives, which can affect profit margins. Intense competition from both established domestic and international companies, alongside a proliferation of smaller, unbranded suppliers, may exert downward price pressure. Despite these headwinds, the trend towards premium lubricants and specialized formulations for applications like long-haul trucking and heavy-duty construction equipment is expected to counterbalance these restraints. Advancements in engine technology and stricter environmental regulations will continue to drive innovation and market penetration of high-value lubricants. Strategic focus on key industrial hubs and logistics centers within China will remain crucial for market players to capitalize on demand.

China Commercial Vehicles Lubricants Industry Company Market Share

This comprehensive market research report provides an in-depth analysis of the China Commercial Vehicles Lubricants Industry, covering the period from 2019 to 2033, with 2025 as the base year and a forecast period of 2025–2033. Explore critical market dynamics, a CAGR of 4.88%, market penetration strategies, and innovation drivers impacting this vital sector. Gain actionable insights into engine oils, greases, hydraulic fluids, and transmission & gear oils segments. This report is essential for automotive lubricant manufacturers, petrochemical companies, component suppliers, and investment firms seeking to understand the evolving Chinese commercial vehicle market.

China Commercial Vehicles Lubricants Industry Market Concentration & Innovation

The China Commercial Vehicles Lubricants Industry exhibits a moderate to high market concentration, driven by a few dominant global and domestic players. Key innovation drivers include the increasing demand for higher performance lubricants, extended drain intervals, and enhanced fuel efficiency in commercial vehicles. Stringent environmental regulations and evolving emission standards are compelling manufacturers to develop advanced formulations. The regulatory framework, particularly concerning environmental protection and product safety, plays a significant role in shaping market entry and product development. Product substitutes are limited in the traditional lubricant space, but the rise of electric vehicles presents a nascent alternative in terms of fluid requirements. End-user trends are shifting towards premium, specialized lubricants that offer superior protection and reduced operational costs. Mergers and acquisitions (M&A) activities are expected to continue as companies seek to consolidate market share, acquire new technologies, and expand their geographical reach. Recent M&A deal values in the broader global lubricant market indicate significant strategic investments, reflecting the perceived growth potential in emerging economies like China. While specific deal values within China's commercial vehicle lubricant sector are closely guarded, industry consolidation is a clear trend. The market share of leading companies in China's commercial vehicle lubricants sector is estimated to be held by: China Petroleum & Chemical Corporation (Sinopec) with an estimated XX% share, China National Petroleum Corporation (CNPC) with an estimated XX% share, and international players like BP PLC (Castrol), ExxonMobil Corporation, and Chevron Corporation collectively holding significant portions.

China Commercial Vehicles Lubricants Industry Industry Trends & Insights

The China Commercial Vehicles Lubricants Industry is poised for substantial growth, driven by robust economic expansion, increasing industrialization, and a rapidly expanding logistics and transportation network. The CAGR of xx% projected for the forecast period underscores the market's dynamic nature. A key market growth driver is the continuous upgrade of commercial vehicle fleets, with a growing preference for advanced vehicles that necessitate high-performance lubricants. The market penetration of synthetic and semi-synthetic lubricants is steadily increasing, displacing conventional mineral oils due to their superior properties, such as better thermal stability, oxidation resistance, and wear protection. Technological disruptions, particularly in the realm of electric and hybrid commercial vehicles, are creating new opportunities and challenges. While the demand for traditional engine oils remains dominant, the emergence of specialized e-fluids, such as e-gear oils and e-coolants, is a significant technological shift. Consumer preferences are increasingly influenced by factors like total cost of ownership, lubricant longevity, and environmental sustainability. Fleet operators are actively seeking lubricants that reduce maintenance downtime and improve fuel economy, thereby lowering operational expenses. The competitive dynamics within the industry are characterized by intense price competition among domestic players and a strong emphasis on technological innovation and product differentiation by international brands. The expansion of road infrastructure and government initiatives to boost domestic manufacturing further contribute to the sustained demand for commercial vehicle lubricants. The increasing sophistication of manufacturing processes and stringent quality control measures by Original Equipment Manufacturers (OEMs) also push the demand for higher-grade lubricants.

Dominant Markets & Segments in China Commercial Vehicles Lubricants Industry

The China Commercial Vehicles Lubricants Industry is largely dominated by the Engine Oils segment, a direct consequence of the sheer volume of commercial vehicles operating across the country, including trucks, buses, and vans. The extensive road network and the burgeoning logistics sector, coupled with consistent vehicle sales, create an unyielding demand for reliable engine lubrication. Economic policies promoting the growth of the transportation and logistics sectors have been instrumental in this dominance. Infrastructure development, such as the expansion of highways and freight terminals, directly correlates with increased commercial vehicle usage, thus fueling the demand for Engine Oils.

- Engine Oils: This segment's dominance is underpinned by the vast number of internal combustion engines in operation. Key drivers include:

- Increasing fleet sizes of heavy-duty trucks and commercial vans.

- Stringent emission standards necessitating advanced, high-performance engine oils.

- The ongoing need for engine protection against wear, corrosion, and sludge formation in demanding operational environments.

- The shift towards longer oil drain intervals, which encourages the use of premium synthetic and semi-synthetic engine oils.

While Engine Oils hold the largest market share, Transmission & Gear Oils and Hydraulic Fluids are also critical segments, experiencing steady growth. The increasing complexity of modern transmissions and hydraulic systems in commercial vehicles requires specialized lubricants that can withstand extreme pressures and temperatures. The use of automated manual transmissions (AMTs) and advanced hydraulic steering systems further boosts the demand for high-quality transmission and hydraulic fluids.

Transmission & Gear Oils:

- Growing adoption of advanced transmission technologies in commercial vehicles.

- Demand for lubricants that offer superior load-carrying capacity and anti-wear properties.

- The need for consistent performance across a wide temperature range.

Hydraulic Fluids:

- Ubiquitous use in hydraulic systems for lifting, braking, and steering in various commercial vehicles.

- Requirement for high viscosity index and excellent thermal stability.

- The impact of construction and mining sectors, which heavily utilize hydraulically powered equipment.

The Greases segment, though smaller in volume compared to engine oils, is crucial for the lubrication of various moving parts, chassis components, and bearings. The demand for specialized greases with enhanced load-carrying capabilities and resistance to water wash-out is on the rise.

- Greases:

- Essential for lubricating wheel bearings, chassis components, and fifth wheels.

- Increasing demand for high-temperature and heavy-duty greases.

- The role of specialized greases in extending component life and reducing maintenance.

The overall market is significantly influenced by government initiatives supporting domestic manufacturing and logistics efficiency, which indirectly propels the demand across all lubricant segments. The market is segmented by Product Type: Engine Oils, Greases, Hydraulic Fluids, and Transmission & Gear Oils.

China Commercial Vehicles Lubricants Industry Product Developments

Product development in the China Commercial Vehicles Lubricants Industry is sharply focused on meeting evolving performance demands and environmental regulations. Manufacturers are continuously innovating to create lubricants offering extended drain intervals, superior wear protection, and enhanced fuel efficiency. A significant trend is the development of specialized lubricants tailored for the unique requirements of electric and hybrid commercial vehicles, such as the Castrol ON e-fluid range, including e-gear oils, e-coolants, and e-greases, designed to manage thermal loads and ensure the longevity of electric powertrain components. The expansion of grease production facilities by companies like FUCHS signifies a commitment to meeting the growing demand for high-performance greases in China. Advancements in additive technology are enabling the creation of lubricants that offer improved viscosity index, better detergency, and enhanced oxidation stability, providing a competitive advantage in a discerning market.

Report Scope & Segmentation Analysis

This report provides a detailed analysis of the China Commercial Vehicles Lubricants Industry, segmented by Product Type. The primary segments analyzed include:

Engine Oils: This segment is projected to maintain its dominant position due to the extensive fleet of internal combustion engine commercial vehicles. Growth will be driven by the demand for high-performance synthetic and semi-synthetic oils that meet stringent emission standards and offer extended drain intervals.

Greases: The greases segment is expected to witness steady growth, fueled by the need for specialized lubrication in bearings, chassis, and other components of commercial vehicles. Innovations in high-temperature and heavy-duty greases will be key drivers.

Hydraulic Fluids: Demand for hydraulic fluids is anticipated to remain robust, supported by the widespread use of hydraulic systems in construction, logistics, and various industrial applications involving commercial vehicles. Advanced formulations offering superior thermal stability and load-carrying capacity will be crucial.

Transmission & Gear Oils: This segment is set to experience significant growth as modern commercial vehicles incorporate more sophisticated transmission systems. The need for lubricants that can handle extreme pressures and temperatures in manual, automatic, and automated manual transmissions will drive market expansion.

Key Drivers of China Commercial Vehicles Lubricants Industry Growth

Several key factors are propelling the growth of the China Commercial Vehicles Lubricants Industry. The sustained expansion of China's logistics and transportation sector, driven by e-commerce growth and increasing inter-city trade, directly translates to higher demand for commercial vehicles and their associated lubricants. Government policies aimed at modernizing the fleet and enforcing stricter emission standards are encouraging the adoption of high-quality, performance-driven lubricants. Technological advancements in vehicle manufacturing, leading to more complex and high-performance engines and powertrains, necessitate the use of advanced lubricant formulations. Furthermore, the growing awareness among fleet operators regarding the benefits of using premium lubricants, such as extended service intervals, reduced maintenance costs, and improved fuel efficiency, is a significant growth catalyst. The increasing investment in research and development by lubricant manufacturers to create products that meet these evolving demands also fuels market expansion.

Challenges in the China Commercial Vehicles Lubricants Industry Sector

Despite the positive growth outlook, the China Commercial Vehicles Lubricants Industry faces several challenges. Intense price competition, particularly from domestic players, can squeeze profit margins for manufacturers. The increasing stringency of environmental regulations, while a driver for innovation, also necessitates significant investment in R&D and production upgrades, which can be a barrier for smaller companies. Supply chain disruptions, exacerbated by geopolitical factors and logistical complexities, can impact raw material availability and cost. The evolving landscape of electric vehicles presents a long-term challenge to the traditional lubricant market, although it simultaneously creates new opportunities for specialized EV fluids. Counterfeit products also remain a concern, potentially eroding brand trust and market share for genuine lubricant manufacturers. The need for continuous adaptation to new OEM specifications and evolving vehicle technologies requires ongoing investment and agility.

Emerging Opportunities in China Commercial Vehicles Lubricants Industry

The China Commercial Vehicles Lubricants Industry is brimming with emerging opportunities. The rapid electrification of commercial vehicle fleets presents a significant growth avenue for specialized electric vehicle (EV) fluids, including e-gear oils, e-coolants, and e-greases, as highlighted by the launch of Castrol's ON range. The continued development of advanced additive technologies offers opportunities to create lubricants with superior performance characteristics, such as enhanced wear protection and extreme temperature stability. Growing demand for sustainable and bio-based lubricants, driven by corporate environmental responsibility initiatives, presents a niche but expanding market. The increasing adoption of fleet management telematics provides valuable data that can inform lubricant selection and maintenance schedules, opening opportunities for service-oriented lubricant providers. Furthermore, the "Belt and Road Initiative" is expected to stimulate cross-border trade and infrastructure development, potentially increasing the demand for commercial vehicle lubricants in related regions.

Leading Players in the China Commercial Vehicles Lubricants Industry Market

- Beijing Zhongrun Huayou Petrochemical Co Ltd

- BP PLC (Castrol)

- Chevron Corporation

- China National Petroleum Corporation

- China Petroleum & Chemical Corporation

- ExxonMobil Corporation

- FUCHS

- Jiangsu Lopal Tech Co Ltd

- Royal Dutch Shell Plc

- Tongyi Petrochemical Co Lt

Key Developments in China Commercial Vehicles Lubricants Industry Industry

- January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions. This strategic restructuring aims to better align the company's operations with market demands and future growth areas, potentially impacting its lubricant offerings and market approach.

- August 2021: FUCHS has decided to expand its grease plant located in China named Yingkou Fox Oil Products Co. Ltd. This expansion may help the company produce more volumes of grease to cater to the demand in China, indicating a strategic move to bolster its presence and production capacity for a key lubricant segment.

- March 2021: Castrol announced the launch of Castrol ON (a Castrol e-fluid range that includes e-gear oils, e-coolants, and e-greases) to its product portfolio. This range is specially designed for electric vehicles, signaling a proactive approach to the emerging electric mobility market and its unique lubrication needs.

Strategic Outlook for China Commercial Vehicles Lubricants Industry Market

The strategic outlook for the China Commercial Vehicles Lubricants Industry is exceptionally positive, characterized by sustained growth driven by fleet expansion and technological advancements. The transition towards higher-performance, synthetic, and semi-synthetic lubricants will continue, as will the increasing demand for specialized fluids for electric and hybrid commercial vehicles. Manufacturers are expected to focus on innovation in additive technology and product formulations to meet stringent emission standards and enhance fuel efficiency. Strategic partnerships and potential M&A activities will likely shape the market landscape, as companies seek to consolidate their positions and expand their technological capabilities. The emphasis on sustainability and environmentally friendly products will also gain momentum, presenting opportunities for companies offering bio-based or recycled lubricant solutions. The industry's ability to adapt to the evolving powertrain technologies and meet the diverse needs of China's vast and dynamic commercial vehicle sector will be key to future success.

China Commercial Vehicles Lubricants Industry Segmentation

-

1. Product Type

- 1.1. Engine Oils

- 1.2. Greases

- 1.3. Hydraulic Fluids

- 1.4. Transmission & Gear Oils

China Commercial Vehicles Lubricants Industry Segmentation By Geography

- 1. China

China Commercial Vehicles Lubricants Industry Regional Market Share

Geographic Coverage of China Commercial Vehicles Lubricants Industry

China Commercial Vehicles Lubricants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Engine Oils

- 5.1.2. Greases

- 5.1.3. Hydraulic Fluids

- 5.1.4. Transmission & Gear Oils

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. China Commercial Vehicles Lubricants Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Engine Oils

- 6.1.2. Greases

- 6.1.3. Hydraulic Fluids

- 6.1.4. Transmission & Gear Oils

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Beijing Zhongrun Huayou Petrochemical Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 BP PLC (Castrol)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Chevron Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China National Petroleum Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 China Petroleum & Chemical Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ExxonMobil Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 FUCHS

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Jiangsu Lopal Tech Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Royal Dutch Shell Plc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tongyi Petrochemical Co Lt

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Beijing Zhongrun Huayou Petrochemical Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Commercial Vehicles Lubricants Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Commercial Vehicles Lubricants Industry Share (%) by Company 2025

List of Tables

- Table 1: China Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: China Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: China Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 4: China Commercial Vehicles Lubricants Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Commercial Vehicles Lubricants Industry?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the China Commercial Vehicles Lubricants Industry?

Key companies in the market include Beijing Zhongrun Huayou Petrochemical Co Ltd, BP PLC (Castrol), Chevron Corporation, China National Petroleum Corporation, China Petroleum & Chemical Corporation, ExxonMobil Corporation, FUCHS, Jiangsu Lopal Tech Co Ltd, Royal Dutch Shell Plc, Tongyi Petrochemical Co Lt.

3. What are the main segments of the China Commercial Vehicles Lubricants Industry?

The market segments include Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.9 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Largest Segment By Product Type : Engine Oils.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.August 2021: FUCHS has decided to expand its grease plant located in China named Yingkou Fox Oil Products Co. Ltd. This expansion may help the company produce more volumes of grease to cater to the demand in China.March 2021: Castrol announced the launch of Castrol ON (a Castrol e-fluid range that includes e-gear oils, e-coolants, and e-greases) to its product portfolio. This range is specially designed for electric vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Commercial Vehicles Lubricants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Commercial Vehicles Lubricants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Commercial Vehicles Lubricants Industry?

To stay informed about further developments, trends, and reports in the China Commercial Vehicles Lubricants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence