Key Insights

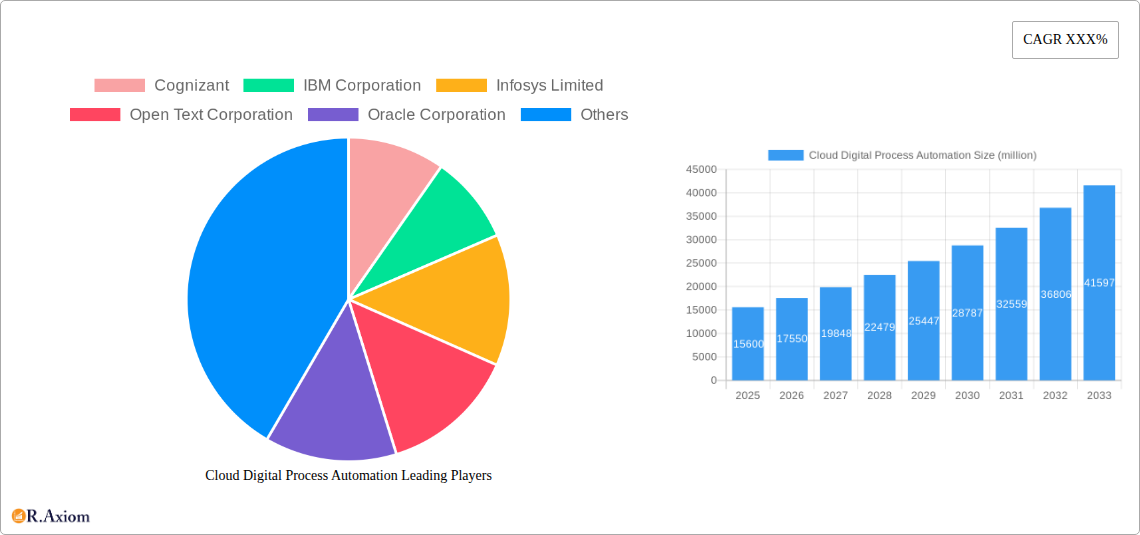

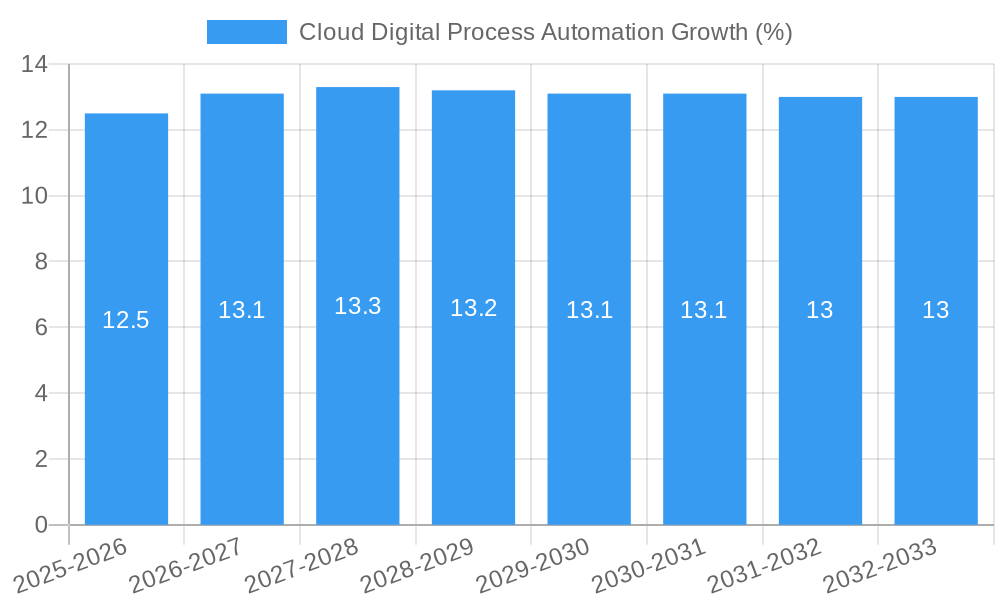

The Cloud Digital Process Automation (DPA) market is experiencing robust expansion, projected to reach a significant valuation of approximately USD 15,600 million by 2025. This growth is fueled by a compound annual growth rate (CAGR) of around 12.5% over the forecast period of 2025-2033. The primary drivers behind this surge include the escalating need for enhanced operational efficiency, a growing demand for streamlined customer experiences, and the imperative for organizations to accelerate their digital transformation initiatives. Industries such as BFSI, IT and Telecom, and Healthcare are leading the adoption of cloud DPA solutions, leveraging them to automate complex workflows, reduce manual intervention, and gain a competitive edge. The scalability, flexibility, and cost-effectiveness offered by cloud-based DPA platforms are further accelerating market penetration.

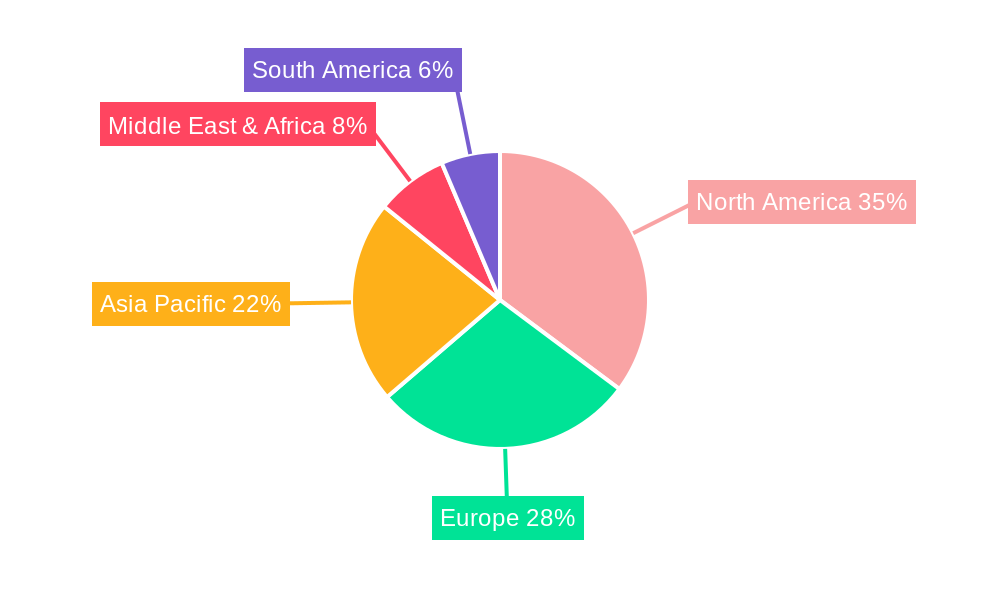

The market is segmented into Solutions and Services, with both experiencing substantial growth, reflecting the comprehensive nature of DPA offerings. The Solutions segment likely captures a larger share due to the foundational technology, while the Services segment, encompassing implementation, consulting, and support, is growing rapidly to ensure successful adoption and ROI. Geographically, North America is anticipated to lead the market, driven by early adoption of advanced technologies and a strong presence of key players like IBM Corporation, Oracle Corporation, and Pegasystems. The Asia Pacific region is expected to witness the fastest growth, propelled by the digitalization efforts in emerging economies like China and India, and increasing investments in cloud infrastructure. Key challenges include data security concerns and the complexity of integrating DPA with legacy systems, though these are being addressed by advancements in security protocols and integration capabilities.

Cloud Digital Process Automation Market Concentration & Innovation

The Cloud Digital Process Automation market is characterized by a moderate to high concentration, with a few key players like IBM Corporation, Oracle Corporation, and Pegasystems holding substantial market shares, estimated collectively at over 60% in the base year 2025. Innovation is a critical differentiator, fueled by advancements in AI, machine learning, and low-code/no-code development platforms. These technologies are enabling more sophisticated automation of complex workflows across diverse industries. Regulatory frameworks, particularly data privacy laws like GDPR and CCPA, are increasingly shaping the development and deployment of cloud-based automation solutions, demanding robust security and compliance features. Product substitutes, such as on-premises process automation solutions and manual process management, continue to exist but are steadily losing ground to the scalability, flexibility, and cost-efficiency of cloud-native offerings. End-user trends indicate a strong demand for seamless integration, user-friendly interfaces, and demonstrable ROI, with businesses prioritizing solutions that can adapt to evolving operational needs. Mergers and acquisitions (M&A) are a significant factor in market dynamics, with deal values expected to reach over 500 million in the historical period 2019-2024, further consolidating the market and driving innovation through the integration of complementary technologies and capabilities. For instance, acquisitions aimed at bolstering AI capabilities and expanding vertical-specific solutions are anticipated to remain prevalent.

Cloud Digital Process Automation Industry Trends & Insights

The Cloud Digital Process Automation (DPA) market is poised for robust expansion, projected to witness a Compound Annual Growth Rate (CAGR) of over 15% throughout the forecast period of 2025–2033. This significant growth is propelled by a confluence of factors, including the accelerating digital transformation initiatives across global enterprises, the increasing need for operational efficiency, and the growing adoption of automation across various business functions. The ability of cloud DPA solutions to offer scalability, flexibility, and cost-effectiveness compared to traditional on-premises systems is a primary driver. Technological disruptions are at the forefront of this evolution. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into DPA platforms is revolutionizing how processes are automated, enabling intelligent decision-making, predictive analytics, and autonomous operations. Robotic Process Automation (RPA) continues to mature, with cloud-native RPA solutions offering enhanced capabilities for automating repetitive tasks at scale. Furthermore, the rise of low-code and no-code development platforms is democratizing automation, allowing business users to build and deploy automated workflows without extensive coding knowledge, thus driving wider adoption and market penetration. Consumer preferences are increasingly leaning towards solutions that provide end-to-end process visibility, real-time analytics, and seamless integration with existing enterprise systems like ERP and CRM. Businesses are demanding greater agility to respond to market changes, and cloud DPA offers the agility to adapt and scale automation strategies rapidly. Competitive dynamics are intensifying, with established players and emerging startups vying for market share. Key strategies include developing specialized industry solutions, enhancing AI/ML capabilities, and focusing on user experience and ease of implementation. The market penetration of cloud DPA solutions is expected to surge from approximately 25% in the base year 2025 to over 60% by 2033, reflecting the widespread adoption and strategic importance of these technologies in modern business operations. The shift towards hybrid and multi-cloud environments also presents opportunities for vendors to offer flexible deployment options.

Dominant Markets & Segments in Cloud Digital Process Automation

The Cloud Digital Process Automation market exhibits distinct dominance across various regions and industry segments, driven by a combination of economic policies, technological infrastructure, and specific industry needs.

Leading Region: North America

North America, particularly the United States, is currently the dominant market for Cloud Digital Process Automation. This leadership is underpinned by several key drivers:

- Technological Adoption: The region boasts a high adoption rate of advanced technologies, including cloud computing, AI, and ML, which are foundational to sophisticated DPA solutions.

- Strong Economic Policies: Favorable government policies supporting digital transformation and innovation, coupled with significant private sector investment in technology, create a fertile ground for DPA market growth.

- Mature IT Infrastructure: A well-developed IT infrastructure ensures seamless implementation and scalability of cloud-based solutions.

- Presence of Key Players: Many leading Cloud DPA vendors are headquartered in North America, fostering innovation and market development.

Dominant Application Segment: BFSI (Banking, Financial Services, and Insurance)

The BFSI sector stands out as the most significant application segment for Cloud Digital Process Automation. Its dominance is driven by:

- High Transaction Volumes: The sheer volume of daily transactions and data processing in BFSI necessitates efficient automation for speed, accuracy, and compliance.

- Stringent Regulatory Compliance: The sector is heavily regulated, and DPA solutions play a crucial role in ensuring adherence to complex compliance mandates, risk management, and fraud detection. Automation helps in streamlining Know Your Customer (KYC) processes, loan origination, claims processing, and regulatory reporting.

- Customer Experience Demands: BFSI institutions are under pressure to enhance customer experience through faster service delivery, personalized offerings, and seamless digital interactions. Cloud DPA enables automation of customer onboarding, query resolution, and personalized communication.

- Operational Efficiency Focus: Automation helps reduce operational costs, minimize errors, and improve the overall efficiency of back-office operations, which are critical in a highly competitive landscape.

Dominant Type Segment: Solution

While both solutions and services are crucial, the "Solution" segment, encompassing the software platforms and tools for DPA, is currently dominant. This is because:

- Core Enabler: The DPA solution is the core technology that enables process automation. Its features, capabilities, and integration potential are primary determinants of adoption.

- Scalability and Customization: Cloud DPA solutions offer the flexibility to scale automation capabilities as per business needs and can be customized to address specific process requirements.

- Innovation Hub: Leading vendors are continuously innovating within their DPA platforms, introducing advanced AI/ML features, analytics, and user interface improvements, driving demand for these sophisticated tools.

Other Significant Segments:

- IT and Telecom: This segment is a significant adopter due to the complex and data-intensive nature of their operations, requiring automation for service provisioning, network management, and customer support.

- Healthcare: Driven by the need for improved patient care, streamlined administrative processes, and compliance with regulations like HIPAA, healthcare is a rapidly growing segment.

- Manufacturing: Automation is crucial for optimizing supply chains, production processes, and quality control.

- Retail: Cloud DPA is utilized for inventory management, order fulfillment, customer service, and personalized marketing campaigns.

The interplay of these factors continues to shape the market, with ongoing developments expected to further solidify the dominance of North America and the BFSI sector, while also fostering growth in other segments.

Cloud Digital Process Automation Product Developments

Recent product developments in Cloud Digital Process Automation are heavily influenced by the integration of advanced AI/ML capabilities, robust low-code/no-code platforms, and enhanced analytics. Innovations are focused on enabling hyperautomation, where multiple automation technologies are combined to automate as many business and IT processes as possible. Key advancements include intelligent document processing, natural language processing for understanding unstructured data, and predictive automation for proactive issue resolution. Competitive advantages are being gained through platforms offering seamless integration with existing enterprise systems, intuitive user interfaces, and strong governance and security features. These developments cater to the growing demand for end-to-end process visibility and agile workflow management across diverse industries.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Cloud Digital Process Automation market, segmenting it across key application and type categories. The Application segmentation includes BFSI, IT and Telecom, Healthcare, Retail, Manufacturing, and Others. Within the BFSI segment, growth is driven by regulatory compliance and transaction volumes. IT and Telecom's adoption is fueled by the need for efficient service delivery and network management. The Healthcare sector sees demand for streamlined patient care and administrative processes. Retail leverages DPA for supply chain optimization and customer experience enhancement. Manufacturing benefits from process optimization and quality control. The "Others" segment encompasses a diverse range of industries experiencing significant growth.

The Type segmentation focuses on Solution and Services. The Solution segment, encompassing DPA platforms and software, is currently dominant due to its role as the core enabler of automation. The Services segment, including implementation, consulting, and managed services, is also crucial for realizing the full potential of DPA and is expected to grow in parallel. Competitive dynamics within each segment are analyzed to understand market share, growth projections, and key market trends.

Key Drivers of Cloud Digital Process Automation Growth

The growth of the Cloud Digital Process Automation market is primarily driven by several interconnected factors. Technologically, the increasing maturity and accessibility of Artificial Intelligence (AI) and Machine Learning (ML) are enabling more sophisticated automation of complex tasks and decision-making. The widespread adoption of cloud computing provides the scalable and flexible infrastructure necessary for deploying DPA solutions globally. Economically, the persistent drive for operational efficiency and cost reduction across all industries is a major catalyst, as DPA solutions offer significant improvements in productivity and resource utilization. Regulatory frameworks, particularly in highly regulated sectors like BFSI and Healthcare, are also pushing for greater automation to ensure compliance and mitigate risks. The increasing demand for enhanced customer experience, requiring faster response times and personalized interactions, further fuels the adoption of DPA.

Challenges in the Cloud Digital Process Automation Sector

Despite its strong growth trajectory, the Cloud Digital Process Automation sector faces several challenges. Regulatory hurdles, especially concerning data privacy and security across different jurisdictions, can create complexities in implementation and require continuous adaptation. Supply chain issues, though less direct, can impact the availability of underlying hardware and specialized software components, potentially delaying deployments. Competitive pressures are intensifying, with a crowded market of vendors offering overlapping functionalities, leading to price wars and the need for continuous differentiation. Furthermore, the initial investment in DPA solutions and the need for skilled personnel to manage and maintain them can act as a barrier for smaller organizations. Overcoming these challenges requires robust compliance strategies, strategic partnerships, and a focus on delivering tangible business value to clients.

Emerging Opportunities in Cloud Digital Process Automation

Emerging opportunities in the Cloud Digital Process Automation market are ripe with potential. The increasing focus on hyperautomation, which combines various automation technologies like RPA, AI, and business process management (BPM), presents a significant avenue for growth. The expansion of DPA into emerging markets in Asia-Pacific and Latin America, driven by their accelerating digital transformation journeys, offers new customer bases. Furthermore, the development of industry-specific DPA solutions tailored to the unique needs of sectors like renewable energy and advanced manufacturing is creating niche markets. The growing demand for intelligent automation in areas such as customer service chatbots, predictive maintenance, and personalized marketing also opens up new avenues for innovation and revenue generation.

Leading Players in the Cloud Digital Process Automation Market

- Cognizant

- IBM Corporation

- Infosys Limited

- Open Text Corporation

- Oracle Corporation

- Pegasystems

- Appian

- SS&C Technologies

- LTIMindtree Limited

- Software AG

Key Developments in Cloud Digital Process Automation Industry

- 2023: Major vendors enhance AI/ML capabilities within their DPA platforms, focusing on intelligent document processing and natural language understanding.

- 2023: Increased adoption of low-code/no-code platforms for citizen developers to build and deploy automated workflows, democratizing automation.

- 2024: Strategic partnerships emerge between DPA vendors and cloud service providers to offer integrated, scalable automation solutions.

- 2024: Mergers and acquisitions continue as larger players acquire specialized DPA technology providers to expand their portfolios.

- 2024: Focus on sustainability through automation, with DPA solutions aiding in optimizing resource usage and reducing waste in manufacturing and logistics.

- 2025 (Projected): Further integration of robotic process automation (RPA) with broader DPA suites for end-to-end process automation.

- 2025 (Projected): Advancements in AI-driven analytics to provide deeper insights into process performance and identify new automation opportunities.

Strategic Outlook for Cloud Digital Process Automation Market

The strategic outlook for the Cloud Digital Process Automation market remains exceptionally strong, driven by its integral role in enabling digital transformation and operational excellence. The continued evolution of AI and ML will empower more sophisticated automation, leading to hyperautomation becoming a standard practice. As businesses increasingly prioritize agility, efficiency, and customer satisfaction, Cloud DPA will be a cornerstone of their strategies. Emerging markets represent significant growth potential, while ongoing innovation in specialized industry solutions will cater to specific business needs. The market is expected to see further consolidation and strategic alliances as vendors strive to offer comprehensive, end-to-end automation capabilities.

Cloud Digital Process Automation Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. IT and Telecom

- 1.3. Healthcare

- 1.4. Retail

- 1.5. Manufacturing

- 1.6. Others

-

2. Type

- 2.1. Solution

- 2.2. Services

Cloud Digital Process Automation Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Digital Process Automation REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cloud Digital Process Automation Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. IT and Telecom

- 5.1.3. Healthcare

- 5.1.4. Retail

- 5.1.5. Manufacturing

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Solution

- 5.2.2. Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cloud Digital Process Automation Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. IT and Telecom

- 6.1.3. Healthcare

- 6.1.4. Retail

- 6.1.5. Manufacturing

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Solution

- 6.2.2. Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cloud Digital Process Automation Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. BFSI

- 7.1.2. IT and Telecom

- 7.1.3. Healthcare

- 7.1.4. Retail

- 7.1.5. Manufacturing

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Solution

- 7.2.2. Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cloud Digital Process Automation Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. BFSI

- 8.1.2. IT and Telecom

- 8.1.3. Healthcare

- 8.1.4. Retail

- 8.1.5. Manufacturing

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Solution

- 8.2.2. Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cloud Digital Process Automation Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. BFSI

- 9.1.2. IT and Telecom

- 9.1.3. Healthcare

- 9.1.4. Retail

- 9.1.5. Manufacturing

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Solution

- 9.2.2. Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cloud Digital Process Automation Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. BFSI

- 10.1.2. IT and Telecom

- 10.1.3. Healthcare

- 10.1.4. Retail

- 10.1.5. Manufacturing

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Solution

- 10.2.2. Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Cognizant

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 IBM Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Infosys Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Open Text Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Oracle Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Pegasystems

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Appian

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 SS&C Technologies

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 LTIMindtree Limited

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Software AG

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Cognizant

List of Figures

- Figure 1: Global Cloud Digital Process Automation Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Cloud Digital Process Automation Revenue (million), by Application 2024 & 2032

- Figure 3: North America Cloud Digital Process Automation Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Cloud Digital Process Automation Revenue (million), by Type 2024 & 2032

- Figure 5: North America Cloud Digital Process Automation Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Cloud Digital Process Automation Revenue (million), by Country 2024 & 2032

- Figure 7: North America Cloud Digital Process Automation Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Cloud Digital Process Automation Revenue (million), by Application 2024 & 2032

- Figure 9: South America Cloud Digital Process Automation Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Cloud Digital Process Automation Revenue (million), by Type 2024 & 2032

- Figure 11: South America Cloud Digital Process Automation Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Cloud Digital Process Automation Revenue (million), by Country 2024 & 2032

- Figure 13: South America Cloud Digital Process Automation Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Cloud Digital Process Automation Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Cloud Digital Process Automation Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Cloud Digital Process Automation Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Cloud Digital Process Automation Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Cloud Digital Process Automation Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Cloud Digital Process Automation Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Cloud Digital Process Automation Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Cloud Digital Process Automation Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Cloud Digital Process Automation Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Cloud Digital Process Automation Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Cloud Digital Process Automation Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Cloud Digital Process Automation Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Cloud Digital Process Automation Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Cloud Digital Process Automation Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Cloud Digital Process Automation Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Cloud Digital Process Automation Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Cloud Digital Process Automation Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Cloud Digital Process Automation Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Cloud Digital Process Automation Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Cloud Digital Process Automation Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Cloud Digital Process Automation Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Cloud Digital Process Automation Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Cloud Digital Process Automation Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Cloud Digital Process Automation Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Cloud Digital Process Automation Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Cloud Digital Process Automation Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Cloud Digital Process Automation Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Cloud Digital Process Automation Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Cloud Digital Process Automation Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Cloud Digital Process Automation Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Cloud Digital Process Automation Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Cloud Digital Process Automation Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Cloud Digital Process Automation Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Cloud Digital Process Automation Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Cloud Digital Process Automation Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Cloud Digital Process Automation Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Cloud Digital Process Automation Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Cloud Digital Process Automation Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Digital Process Automation?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Cloud Digital Process Automation?

Key companies in the market include Cognizant, IBM Corporation, Infosys Limited, Open Text Corporation, Oracle Corporation, Pegasystems, Appian, SS&C Technologies, LTIMindtree Limited, Software AG.

3. What are the main segments of the Cloud Digital Process Automation?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud Digital Process Automation," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud Digital Process Automation report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud Digital Process Automation?

To stay informed about further developments, trends, and reports in the Cloud Digital Process Automation, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence