Key Insights

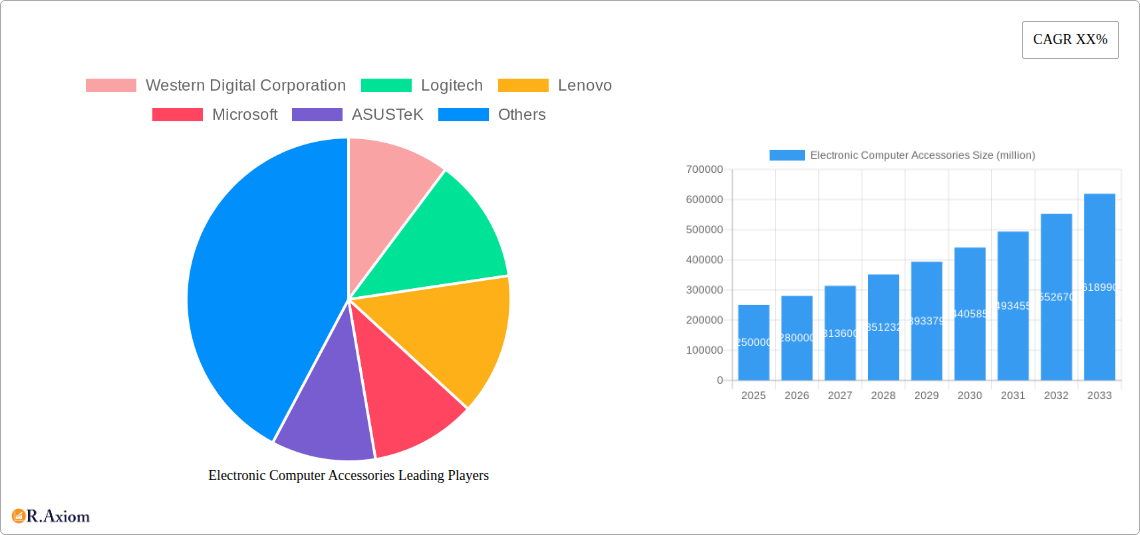

The global Electronic Computer Accessories market is poised for substantial growth, projected to reach approximately $250,000 million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 12% from 2019 to 2033. This expansion is fueled by a confluence of powerful drivers, including the burgeoning demand for high-performance computing in commercial enterprises and the increasing adoption of advanced accessories by individual consumers. The proliferation of remote work and hybrid employment models has significantly boosted the need for reliable and efficient computer peripherals such as external hard drives for data storage, advanced displays for enhanced productivity, and powerful graphics cards for demanding professional applications. Furthermore, the continuous evolution of technology, leading to upgrades and replacements of existing components, particularly in memory and mainboards, further propels market growth.

Key trends shaping the Electronic Computer Accessories landscape include the increasing miniaturization and portability of devices, alongside a growing emphasis on ergonomic designs that enhance user comfort and reduce strain. The integration of smart features and IoT capabilities into computer accessories is another significant trend, offering users more seamless and intuitive control over their digital environments. However, the market also faces certain restraints, such as the fluctuating prices of raw materials, which can impact manufacturing costs and, consequently, consumer prices. Additionally, the rapid pace of technological obsolescence necessitates continuous innovation and investment in research and development, posing a challenge for some market players. Despite these challenges, the market's diverse application segments, ranging from commercial enterprises to individual users, and its comprehensive product types, including hard disk drives, displays, and memory modules, indicate a robust and dynamic market with sustained upward momentum.

The electronic computer accessories market is characterized by a moderate to high degree of concentration, with key players like Western Digital Corporation, Logitech, Lenovo, Microsoft, ASUSTeK, AOC, GIGABYTE Technology, Intel, Advanced Micro Devices, NVIDIA, Kingston Technology Corporation, Ramaxel, Adata, Seagate Technology, and Toshiba holding significant market share. The study period, 2019–2033, with a base year of 2025, encompasses substantial shifts driven by technological advancements and evolving consumer needs. Innovation remains a critical differentiator, particularly in areas such as high-capacity storage solutions (Hard Disk Drives, SSDs), advanced display technologies (Monitors, VR headsets), and powerful graphics cards for gaming and professional workloads. Regulatory frameworks, while generally supportive of technological progress, can influence product standards and environmental compliance. The presence of readily available product substitutes, such as integrated system components, poses a continuous challenge, necessitating consistent innovation. End-user trends are increasingly leaning towards personalized computing experiences, remote work enablement, and high-performance gaming setups, directly impacting demand for specific accessory types. Mergers and acquisitions (M&A) activities are projected to play a role, with estimated M&A deal values in the range of hundreds of millions of dollars, as larger entities seek to consolidate market position or acquire cutting-edge technologies. For instance, a hypothetical M&A of a specialized memory module manufacturer by a major PC component provider could occur within the forecast period.

Electronic Computer Accessories Industry Trends & Insights

The electronic computer accessories market is poised for robust growth, driven by a confluence of accelerating technological disruptions, evolving consumer preferences, and increasing market penetration across various applications. The compound annual growth rate (CAGR) is projected to be approximately 7.5% over the forecast period of 2025–2033, fueled by the relentless demand for enhanced computing performance and user experience. The widespread adoption of remote work policies and the burgeoning gaming industry are significant growth drivers, boosting the demand for high-quality displays, ergonomic peripherals, and powerful graphics cards. Technological advancements, such as the continuous innovation in Solid-State Drive (SSD) technology offering faster data access, and the development of more energy-efficient and high-resolution displays, are creating new market opportunities. Furthermore, the integration of AI and machine learning capabilities into accessories, enhancing their functionality and user interaction, is a key disruptive trend. Consumer preferences are shifting towards personalized and customizable accessories that cater to specific needs, be it for professional productivity or immersive entertainment. This includes a growing demand for customizable RGB lighting on keyboards and mice, and specialized gaming chairs. The competitive landscape is intense, with established players like Intel, NVIDIA, and AMD continually pushing the boundaries of performance in processors and graphics, while companies like Logitech and Kingston Technology Corporation focus on peripherals and memory solutions respectively. Market penetration is expected to deepen in emerging economies as digital infrastructure improves and disposable incomes rise. The increasing reliance on cloud computing also indirectly drives demand for high-speed networking accessories and reliable storage solutions. The overall market penetration is expected to reach over 70% by 2033 for essential accessories.

Dominant Markets & Segments in Electronic Computer Accessories

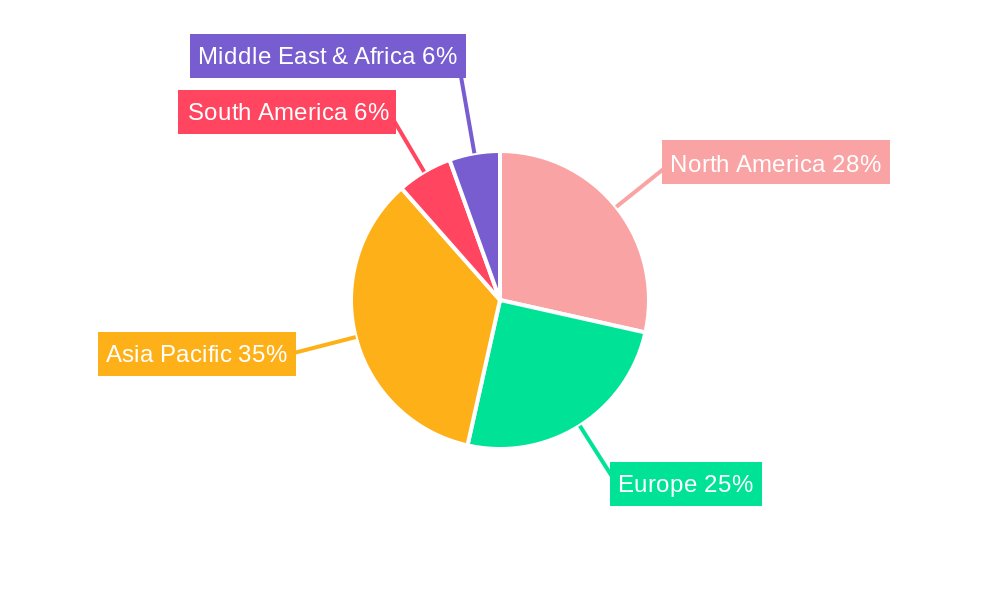

The electronic computer accessories market exhibits distinct regional and segmental dominance, shaped by economic policies, infrastructure development, and evolving technological adoption rates. Commercial Enterprises represent a substantial segment, driven by the continuous need for reliable and high-performance computing solutions to support business operations, data management, and employee productivity. Key drivers within this segment include the expansion of corporate IT infrastructure, the increasing adoption of cloud computing services, and the demand for cybersecurity-enhanced accessories. Countries with strong economic foundations and robust IT sectors, such as the United States, China, and Germany, are expected to lead in terms of market value for commercial enterprise accessories.

Within the Types of electronic computer accessories, Hard Disk Drive (HDD) and its Solid-State Drive (SSD) counterparts, along with Memory modules (RAM), consistently command significant market share due to their foundational role in any computing system. The increasing data generation across all sectors necessitates constant upgrades and expansion of storage capacities. Furthermore, the demand for faster data access fuels the transition towards SSDs, which are becoming more mainstream. The Graphics Card segment is experiencing explosive growth, propelled by the booming gaming industry, the increasing complexity of graphical workloads in professional fields like design and AI, and the rise of cryptocurrency mining (though this is a fluctuating driver). Countries with a strong gaming culture and advanced technological manufacturing capabilities, such as South Korea and Taiwan, are prominent in this segment.

The Personal segment, while smaller in terms of per-unit value compared to enterprise solutions, represents a vast and diverse consumer base. This segment is driven by individual upgrading cycles, the demand for enhanced gaming experiences, and the growing popularity of home offices. Economic policies promoting consumer spending and access to technology are crucial here. Countries with a large young population and high internet penetration are key markets.

Commercial Enterprises:

- Key Drivers: IT infrastructure upgrades, cloud adoption, remote work enablement, cybersecurity mandates.

- Dominance Analysis: This segment is characterized by bulk purchases and a focus on reliability, performance, and scalability. Corporate purchasing decisions are often influenced by Total Cost of Ownership (TCO) and long-term support. The demand for enterprise-grade SSDs, high-capacity HDDs, and robust networking accessories is particularly strong. Market value is estimated to be over one hundred million dollars by 2025.

Personals:

- Key Drivers: Gaming, content creation, home office setup, personal customization.

- Dominance Analysis: This segment is driven by individual consumer choices, brand loyalty, and the pursuit of the latest technology for entertainment and personal productivity. Demand for high-performance gaming peripherals, VR headsets, and aesthetically pleasing computer builds is prominent. Market value is estimated to be over eighty million dollars by 2025.

Hard Disk Drive (HDD):

- Key Drivers: Bulk data storage needs, cost-effectiveness for large capacities, surveillance systems.

- Dominance Analysis: Despite the rise of SSDs, HDDs remain crucial for mass storage solutions due to their lower cost per gigabyte. Market share is significant, with an estimated market value of over seventy million dollars by 2025.

Display:

- Key Drivers: Gaming monitors with high refresh rates, 4K and 8K resolutions, curved displays, portable monitors.

- Dominance Analysis: The display market is continuously evolving with new technologies enhancing visual immersion. Gaming and professional visual content creation are significant drivers. Market value is estimated to be over sixty million dollars by 2025.

Mainboard:

- Key Drivers: Supporting next-generation processors, integrated advanced features, overclocking capabilities.

- Dominance Analysis: Mainboards are critical for system compatibility and future upgrades, driving demand for advanced chipsets and connectivity. Market value is estimated to be over fifty million dollars by 2025.

Graphics Card:

- Key Drivers: Gaming, AI/ML, professional visualization, cryptocurrency mining.

- Dominance Analysis: This segment is experiencing rapid growth due to its essential role in visually intensive applications. High-end GPUs are in high demand. Market value is estimated to be over ninety million dollars by 2025.

Memory:

- Key Drivers: Multitasking capabilities, faster application loading, RAM capacity demands of modern software.

- Dominance Analysis: Sufficient RAM is crucial for overall system performance, driving consistent demand for memory modules. Market value is estimated to be over forty million dollars by 2025.

Others:

- Key Drivers: Peripherals (keyboards, mice, webcams), networking equipment, power supplies, cooling solutions.

- Dominance Analysis: This broad category captures essential accessories that enhance user experience and system functionality. Market value is estimated to be over fifty million dollars by 2025.

Electronic Computer Accessories Product Developments

Recent product developments in electronic computer accessories are heavily influenced by trends in miniaturization, increased power efficiency, and enhanced user interactivity. Innovations in Solid-State Drive (SSD) technology have led to faster read/write speeds and more compact form factors, catering to the demand for quicker boot times and application loading. High-refresh-rate and ultra-wide gaming monitors, featuring technologies like Quantum Dot and Mini-LED, are offering unparalleled visual fidelity and responsiveness. Furthermore, ergonomic peripherals, including programmable keyboards with tactile switches and advanced optical mice, are designed to improve user comfort and precision during extended use. The integration of AI into webcams for improved image processing and the development of smart home integration capabilities in peripherals are also key technological trends shaping the market.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global electronic computer accessories market, segmented by Application and Type. The Application segmentation includes Commercial Enterprises and Personals, analyzing their distinct purchasing behaviors and demand drivers. The Type segmentation encompasses Hard Disk Drive (HDD), Display, Mainboard, Graphics Card, Memory, and Others (including peripherals, networking, etc.). Growth projections and market sizes are detailed for each segment, with an emphasis on the competitive dynamics shaping their evolution throughout the forecast period. For instance, the Commercial Enterprises segment, projected to grow at a CAGR of 6.8%, is expected to reach a market size of approximately one hundred and fifty million dollars by 2033. Conversely, the Personal segment, driven by gaming and content creation, is projected to grow at a CAGR of 8.2% and reach a market size of over one hundred and twenty million dollars by 2033.

Key Drivers of Electronic Computer Accessories Growth

The growth of the electronic computer accessories market is propelled by several interconnected factors. Technologically, the continuous innovation in processing power, storage density (e.g., advancements in NVMe SSDs), and display resolutions (e.g., 8K monitors) fuels upgrades and new purchases. Economically, rising disposable incomes, particularly in emerging markets, and the sustained trend of remote and hybrid work arrangements are significant catalysts. Regulatory factors, such as government initiatives to promote digitalization and technological adoption, also contribute to market expansion. For example, increased investment in digital infrastructure in developing nations drives demand for all types of computer accessories. The escalating popularity of PC gaming and the increasing complexity of professional software applications necessitate higher-performance accessories.

Challenges in the Electronic Computer Accessories Sector

Despite robust growth, the electronic computer accessories sector faces several challenges. Supply chain disruptions, as evidenced by global chip shortages and logistics bottlenecks, can lead to increased costs and delayed product availability, impacting both manufacturers and consumers. Intense competition among a multitude of players, ranging from established giants to agile startups, puts pressure on profit margins and necessitates continuous innovation. Evolving cybersecurity threats require accessories with enhanced security features, adding to development costs. Moreover, the increasing electronic waste generated by rapid upgrade cycles presents environmental concerns and regulatory scrutiny regarding disposal and recycling. Market saturation in developed regions for certain basic accessories also limits organic growth.

Emerging Opportunities in Electronic Computer Accessories

Emerging opportunities in the electronic computer accessories market lie in the growing demand for specialized and niche products. The expansion of the Metaverse and augmented reality (AR)/virtual reality (VR) technologies presents a significant opportunity for advanced VR headsets, haptic feedback devices, and high-resolution displays. The increasing adoption of artificial intelligence (AI) in consumer electronics is creating avenues for AI-powered accessories that offer predictive capabilities, personalized experiences, and enhanced automation. The growing awareness of digital well-being and ergonomics is driving demand for smart accessories that monitor posture, eye strain, and promote healthier usage habits. Furthermore, the increasing demand for sustainable and eco-friendly accessories, manufactured with recycled materials and designed for longevity, represents a significant untapped market.

Leading Players in the Electronic Computer Accessories Market

- Western Digital Corporation

- Logitech

- Lenovo

- Microsoft

- ASUSTeK

- AOC

- GIGABYTE Technology

- Intel

- Advanced Micro Devices

- NVIDIA

- Kingston Technology Corporation

- Ramaxel

- Adata

- Seagate Technology

- Toshiba

Key Developments in Electronic Computer Accessories Industry

- 2023/09: NVIDIA announces the GeForce RTX 40 series graphics cards, pushing performance boundaries for gaming and professional applications.

- 2023/10: Western Digital Corporation launches new high-capacity WD Red Pro HDDs tailored for NAS environments.

- 2024/01: Logitech introduces new ergonomic wireless keyboards and mice designed for extended work sessions.

- 2024/03: Kingston Technology Corporation expands its NV2 NVMe SSD line with increased capacities and improved performance.

- 2024/05: ASUSTeK unveils new series of OLED gaming monitors with ultra-fast refresh rates.

- 2024/07: Microsoft releases Surface accessories emphasizing productivity and portability for its Surface device ecosystem.

- 2025/XX: Anticipated launch of next-generation AMD Ryzen processors with integrated RDNA graphics, impacting the demand for standalone graphics cards.

- 2025/XX: Expected release of new display technologies with enhanced color accuracy and energy efficiency.

Strategic Outlook for Electronic Computer Accessories Market

- 2023/09: NVIDIA announces the GeForce RTX 40 series graphics cards, pushing performance boundaries for gaming and professional applications.

- 2023/10: Western Digital Corporation launches new high-capacity WD Red Pro HDDs tailored for NAS environments.

- 2024/01: Logitech introduces new ergonomic wireless keyboards and mice designed for extended work sessions.

- 2024/03: Kingston Technology Corporation expands its NV2 NVMe SSD line with increased capacities and improved performance.

- 2024/05: ASUSTeK unveils new series of OLED gaming monitors with ultra-fast refresh rates.

- 2024/07: Microsoft releases Surface accessories emphasizing productivity and portability for its Surface device ecosystem.

- 2025/XX: Anticipated launch of next-generation AMD Ryzen processors with integrated RDNA graphics, impacting the demand for standalone graphics cards.

- 2025/XX: Expected release of new display technologies with enhanced color accuracy and energy efficiency.

Strategic Outlook for Electronic Computer Accessories Market

The strategic outlook for the electronic computer accessories market is exceptionally positive, driven by ongoing technological innovation and evolving consumer and enterprise needs. Key growth catalysts include the sustained demand for higher performance computing, the expansion of the gaming and esports industries, and the persistent trend of remote and hybrid work. Strategic focus for market players will involve investing in R&D for AI-integrated accessories, exploring sustainable manufacturing practices, and expanding market reach in emerging economies. Furthermore, companies that can offer integrated solutions, combining hardware and software to deliver unique user experiences, will likely gain a competitive advantage. The market's adaptability to new technological paradigms, such as the Metaverse, will be crucial for long-term success.

Electronic Computer Accessories Segmentation

-

1. Application

- 1.1. Commercial Enterprises

- 1.2. Personals

-

2. Types

- 2.1. Hard Disk Drive

- 2.2. Display

- 2.3. Mainboard

- 2.4. Graphics Card

- 2.5. Memory

- 2.6. Others

Electronic Computer Accessories Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electronic Computer Accessories REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electronic Computer Accessories Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Enterprises

- 5.1.2. Personals

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Hard Disk Drive

- 5.2.2. Display

- 5.2.3. Mainboard

- 5.2.4. Graphics Card

- 5.2.5. Memory

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Electronic Computer Accessories Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Enterprises

- 6.1.2. Personals

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Hard Disk Drive

- 6.2.2. Display

- 6.2.3. Mainboard

- 6.2.4. Graphics Card

- 6.2.5. Memory

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Electronic Computer Accessories Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Enterprises

- 7.1.2. Personals

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Hard Disk Drive

- 7.2.2. Display

- 7.2.3. Mainboard

- 7.2.4. Graphics Card

- 7.2.5. Memory

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Electronic Computer Accessories Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Enterprises

- 8.1.2. Personals

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Hard Disk Drive

- 8.2.2. Display

- 8.2.3. Mainboard

- 8.2.4. Graphics Card

- 8.2.5. Memory

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Electronic Computer Accessories Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Enterprises

- 9.1.2. Personals

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Hard Disk Drive

- 9.2.2. Display

- 9.2.3. Mainboard

- 9.2.4. Graphics Card

- 9.2.5. Memory

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Electronic Computer Accessories Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Enterprises

- 10.1.2. Personals

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Hard Disk Drive

- 10.2.2. Display

- 10.2.3. Mainboard

- 10.2.4. Graphics Card

- 10.2.5. Memory

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Western Digital Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Logitech

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Lenovo

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Microsoft

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ASUSTeK

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 AOC

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 GIGABYTE Technology

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Intel

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Advanced Micro Devices

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 NVIDIA

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Kingston Technology Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ramaxel

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Adata

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Seagate Technology

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Toshiba

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Western Digital Corporation

List of Figures

- Figure 1: Global Electronic Computer Accessories Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Electronic Computer Accessories Revenue (million), by Application 2024 & 2032

- Figure 3: North America Electronic Computer Accessories Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Electronic Computer Accessories Revenue (million), by Types 2024 & 2032

- Figure 5: North America Electronic Computer Accessories Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Electronic Computer Accessories Revenue (million), by Country 2024 & 2032

- Figure 7: North America Electronic Computer Accessories Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Electronic Computer Accessories Revenue (million), by Application 2024 & 2032

- Figure 9: South America Electronic Computer Accessories Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Electronic Computer Accessories Revenue (million), by Types 2024 & 2032

- Figure 11: South America Electronic Computer Accessories Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Electronic Computer Accessories Revenue (million), by Country 2024 & 2032

- Figure 13: South America Electronic Computer Accessories Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Electronic Computer Accessories Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Electronic Computer Accessories Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Electronic Computer Accessories Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Electronic Computer Accessories Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Electronic Computer Accessories Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Electronic Computer Accessories Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Electronic Computer Accessories Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Electronic Computer Accessories Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Electronic Computer Accessories Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Electronic Computer Accessories Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Electronic Computer Accessories Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Electronic Computer Accessories Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Electronic Computer Accessories Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Electronic Computer Accessories Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Electronic Computer Accessories Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Electronic Computer Accessories Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Electronic Computer Accessories Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Electronic Computer Accessories Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Electronic Computer Accessories Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Electronic Computer Accessories Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Electronic Computer Accessories Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Electronic Computer Accessories Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Electronic Computer Accessories Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Electronic Computer Accessories Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Electronic Computer Accessories Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Electronic Computer Accessories Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Electronic Computer Accessories Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Electronic Computer Accessories Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Electronic Computer Accessories Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Electronic Computer Accessories Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Electronic Computer Accessories Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Electronic Computer Accessories Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Electronic Computer Accessories Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Electronic Computer Accessories Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Electronic Computer Accessories Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Electronic Computer Accessories Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Electronic Computer Accessories Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Electronic Computer Accessories Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Computer Accessories?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Electronic Computer Accessories?

Key companies in the market include Western Digital Corporation, Logitech, Lenovo, Microsoft, ASUSTeK, AOC, GIGABYTE Technology, Intel, Advanced Micro Devices, NVIDIA, Kingston Technology Corporation, Ramaxel, Adata, Seagate Technology, Toshiba.

3. What are the main segments of the Electronic Computer Accessories?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electronic Computer Accessories," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electronic Computer Accessories report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electronic Computer Accessories?

To stay informed about further developments, trends, and reports in the Electronic Computer Accessories, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence