Key Insights

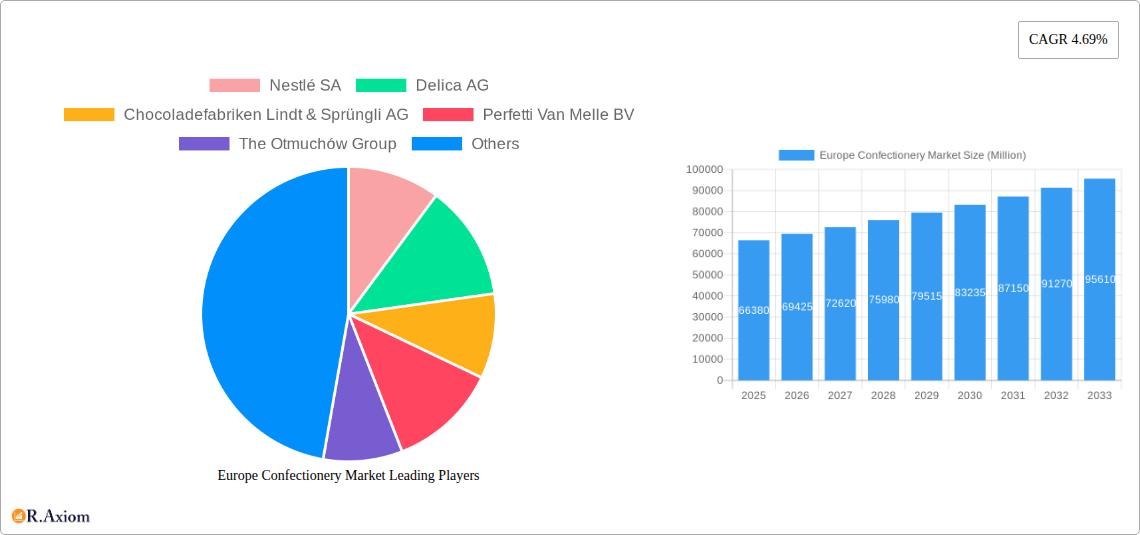

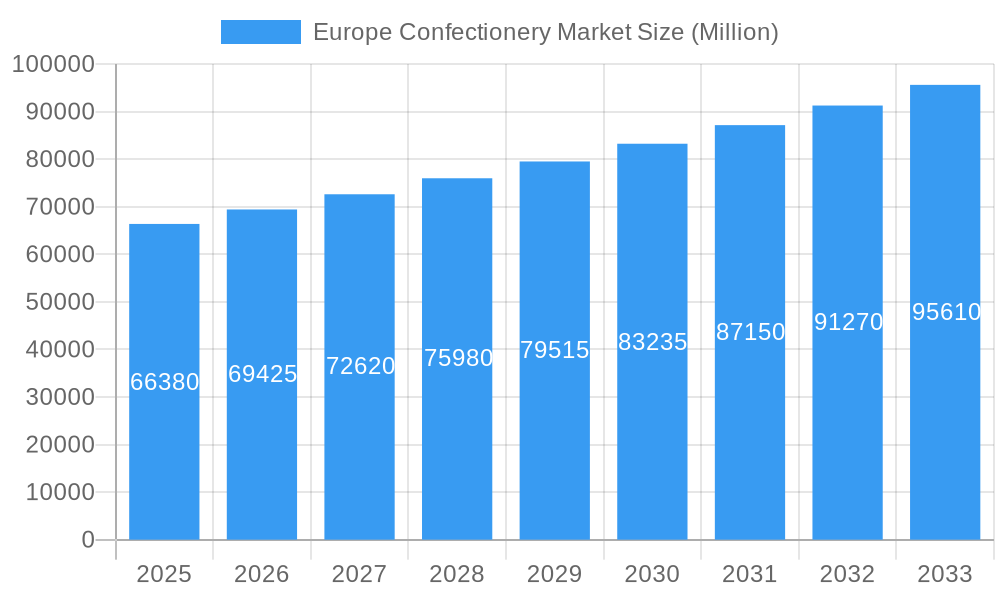

The European confectionery market is forecast for substantial growth, projected to reach $72.38 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.69% between 2025 and 2033. Key growth drivers include increasing demand for premium and artisanal chocolates, a rising preference for sugar-free and healthier options due to growing health consciousness, and continuous product innovation in flavors and formats by leading manufacturers. Online retail, supermarkets, and hypermarkets are pivotal distribution channels. Emerging trends like ethical sourcing and sustainable production are also shaping consumer preferences and product development.

Europe Confectionery Market Market Size (In Billion)

The market is segmented into Confections (especially chocolate – dark, milk, white), Gums (bubble gum, chewing gum – sugared and sugar-free), Snack Bars (cereal, fruit & nut, protein bars), and Sugar Confectionery (hard candies, lollipops, mints, gummies, toffees, nougats). Major players including Nestlé SA, Ferrero International SA, Mars Incorporated, and Mondelēz International Inc. are actively influencing the market through strategic launches, acquisitions, and marketing. Europe, with high disposable incomes, remains a dominant consumption region, led by Germany, the United Kingdom, and France.

Europe Confectionery Market Company Market Share

This report provides an in-depth analysis of the Europe Confectionery Market, offering critical insights into dynamics, growth drivers, and future trends. Covering the period from 2019 to 2033, with 2025 as the base year, this report is essential for confectionery manufacturers, distributors, investors, and stakeholders. We examine chocolate, gums, snack bars, and sugar confectionery, analyzing consumption patterns and evolving preferences across online retail, convenience stores, and supermarkets.

With a projected market size of $72.38 billion in 2025 and an estimated CAGR of 4.69% during the forecast period, the Europe confectionery market is poised for significant expansion. Our analysis details market concentration, innovation strategies, and the impact of regulatory frameworks, providing a clear roadmap for strategic decision-making in the competitive European confectionery sector.

Europe Confectionery Market Market Concentration & Innovation

The Europe confectionery market exhibits a moderate to high level of market concentration, with a few major players holding significant market share. Leading companies like Mondelēz International Inc., Ferrero International SA, and Nestlé SA consistently drive innovation and dominate distribution channels. Innovation is a key differentiator, fueled by evolving consumer demand for healthier options, unique flavor profiles, and sustainable sourcing. The market actively witnesses advancements in product formulations, such as reduced sugar content, plant-based ingredients, and functional confectionery offerings.

- Innovation Drivers:

- Health & Wellness Trends: Growing consumer focus on sugar-free, low-calorie, and plant-based confectionery.

- Premiumization: Demand for artisanal chocolates and gourmet confectionery with unique ingredients and sophisticated packaging.

- Sustainability: Increasing emphasis on ethically sourced cocoa, eco-friendly packaging, and reduced environmental impact.

- Novel Flavors and Textures: Exploration of exotic fruits, savory notes, and multi-sensory experiences.

- Regulatory Frameworks: Strict regulations regarding food safety, labeling, and nutritional content significantly influence product development and market entry.

- Product Substitutes: Competition from other snack categories, such as bakery goods and healthy snacks, necessitates continuous product differentiation.

- End-User Trends: Consumers are increasingly seeking convenience, indulgence, and personalized confectionery experiences.

- Mergers & Acquisitions (M&A): Strategic acquisitions and partnerships are prevalent, allowing companies to expand their product portfolios, geographical reach, and technological capabilities. M&A deal values are projected to reach USD XXX Million by 2025, reflecting the consolidation trend.

Europe Confectionery Market Industry Trends & Insights

The Europe confectionery market is characterized by robust growth, driven by a confluence of factors including rising disposable incomes, changing lifestyles, and an enduring cultural appreciation for confectionery products. The market is dynamic, with technological disruptions constantly reshaping production and distribution. Consumer preferences are evolving at an unprecedented pace, leaning towards healthier indulgence, ethical sourcing, and personalized experiences. This necessitates a keen understanding of competitive dynamics and the ability to adapt swiftly to market shifts.

The demand for chocolate confectionery, particularly dark and milk chocolate variants, continues to be a cornerstone of the market, accounting for an estimated XX% of the total market value. This segment is bolstered by premiumization trends, with consumers willing to pay more for high-quality, ethically sourced cocoa. Sugar confectionery, while facing scrutiny due to health concerns, remains popular due to its affordability and wide variety of forms, including hard candies, gummies, and pastilles. The sugar-free and reduced-sugar variants are witnessing significant growth within this segment.

Gums, encompassing bubble gum and chewing gum, represent another substantial segment, with a notable shift towards sugar-free options driven by oral health consciousness. Snack bars, including cereal bars, fruit & nut bars, and protein bars, are experiencing rapid expansion as consumers seek convenient and nutritious on-the-go options. This segment is attracting new entrants and fostering innovation in ingredient formulations and functional benefits.

Technological advancements in manufacturing processes are enhancing efficiency, reducing costs, and enabling greater product customization. Automation in production lines and advanced packaging solutions are becoming increasingly commonplace. Furthermore, the digital transformation is profoundly impacting distribution channels, with online retail stores witnessing exponential growth. This shift requires confectionery companies to invest in robust e-commerce strategies and digital marketing to reach a wider consumer base.

The competitive landscape is intense, with both global giants and regional players vying for market share. Companies are investing heavily in research and development to launch innovative products that cater to niche markets and emerging consumer demands. Strategic partnerships and collaborations are also key to expanding market reach and leveraging complementary expertise. The overall market penetration of confectionery products in Europe remains high, indicating a mature yet continuously evolving industry. The projected market size of USD XXX Million in 2025 underscores the sector's economic significance and its resilience to economic fluctuations. The compounded annual growth rate (CAGR) is estimated at XX% for the forecast period, highlighting a healthy and sustained growth trajectory.

Dominant Markets & Segments in Europe Confectionery Market

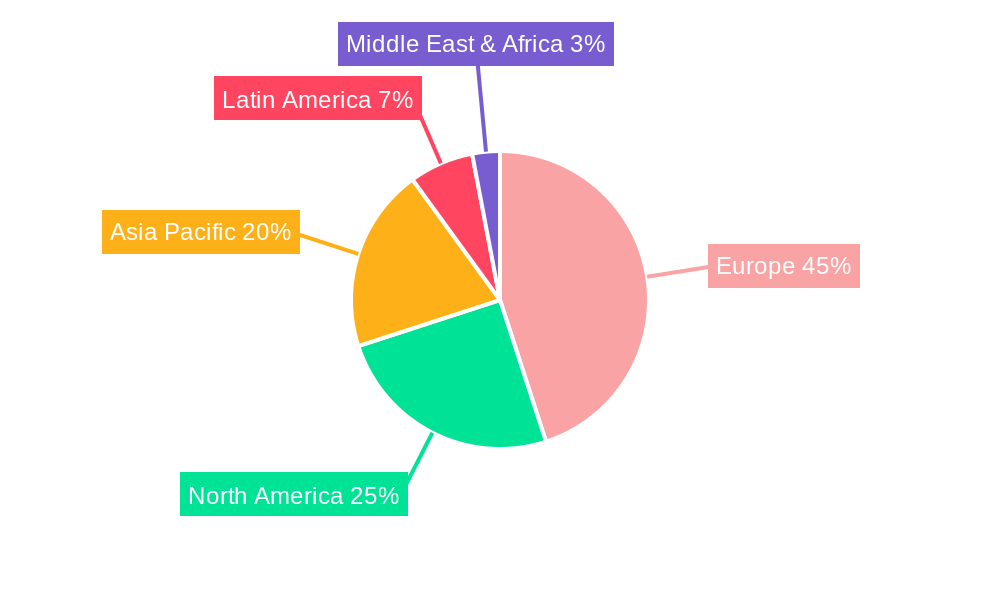

The European confectionery market is a vibrant and diverse landscape, with significant variations in dominance across regions and product categories. Germany, the United Kingdom, and France consistently emerge as the leading national markets, owing to their large consumer bases, high disposable incomes, and established confectionery manufacturing sectors. The economic policies in these nations, focusing on consumer spending and international trade, further bolster their dominance. Infrastructure development, including robust logistics networks, ensures efficient distribution of confectionery products across the continent.

Dominant Confections Segment: Chocolate Chocolate remains the undisputed leader within the European confectionery market, representing a substantial portion of overall sales. Within the chocolate segment, several variants command significant market share:

- Milk Chocolate: This variant continues to be the most popular choice across Europe, catering to a broad consumer base with its familiar and comforting taste. Its dominance is driven by widespread availability, attractive price points, and its appeal to both children and adults.

- Dark Chocolate: Experiencing robust growth, dark chocolate is increasingly favored by health-conscious consumers and connoisseurs seeking richer, more complex flavor profiles. The demand for dark chocolate with higher cocoa content and ethically sourced ingredients is a key driver.

- White Chocolate: While holding a smaller market share, white chocolate maintains its appeal, particularly for specific applications in desserts and as a complementary flavor in various confectionery products.

Dominant Distribution Channel: Supermarket/Hypermarket Supermarkets and hypermarkets continue to be the most significant distribution channels for confectionery products in Europe. Their broad reach, extensive product assortments, and strategic placement of impulse-buy items at checkout counters contribute to their dominance.

- Key Drivers for Supermarket/Hypermarket Dominance:

- Convenience: Consumers can purchase a wide range of confectionery alongside other grocery essentials.

- Visibility and Accessibility: Extensive store networks ensure products are readily available to a vast majority of the population.

- Promotional Activities: Supermarkets frequently host promotions, discounts, and bundled offers, driving impulse purchases.

- Product Variety: A single location offers access to a multitude of brands and confectionery types.

Other Significant Segments and Their Dominance Drivers:

- Sugar Confectionery: This broad category, encompassing hard candies, lollipops, mints, pastilles, gummies, and jellies, holds a significant market share due to its affordability and broad appeal.

- Dominance Drivers: Price sensitivity, impulse buying, variety of flavors and shapes, and appeal to younger demographics.

- Gums: Chewing gum, especially sugar-free variants, is popular for its convenience and perceived oral health benefits.

- Dominance Drivers: Growing health consciousness, portability, and marketing by major gum manufacturers.

- Snack Bars: This segment is rapidly growing, driven by the demand for convenient, nutritious, and on-the-go snacking options.

- Dominance Drivers: Evolving lifestyle trends, increasing awareness of health and fitness, and product innovation in terms of ingredients and functionality.

The dominance of these segments is further influenced by factors such as marketing campaigns, seasonal demand, and the strategic placement of products by manufacturers. The online retail store segment is also witnessing rapid growth, challenging traditional distribution models and offering new avenues for market penetration.

Europe Confectionery Market Product Developments

Product development in the Europe confectionery market is sharply focused on innovation driven by evolving consumer preferences. Manufacturers are increasingly launching products that cater to health and wellness trends, featuring reduced sugar, plant-based ingredients, and functional benefits such as added vitamins or probiotics. Premiumization is another key trend, with a rise in artisanal chocolates and gourmet confectionery with unique flavor combinations and high-quality ingredients. Technological advancements are enabling the creation of novel textures and forms, enhancing the sensory experience for consumers. Competitive advantages are being built through sustainable sourcing, eco-friendly packaging, and transparent labeling, resonating with ethically conscious consumers.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Europe confectionery market, segmented across key product categories and distribution channels. The Confections segment is further divided into Chocolate (including Dark Chocolate, Milk Chocolate, and White Chocolate), Gums (comprising Bubble Gum and Chewing Gum, further broken down by Sugar Content into Sugar Chewing Gum and Sugar-free Chewing Gum), Snack Bar (encompassing Cereal Bar, Fruit & Nut Bar, and Protein Bar), and Sugar Confectionery (including Hard Candy, Lollipops, Mints, Pastilles, Gummies and Jellies, Toffees and Nougats, and Others). The Distribution Channel segmentation includes Convenience Store, Online Retail Store, Supermarket/Hypermarket, and Others. Each segment is analyzed for its market size, growth projections, and competitive dynamics, offering detailed insights into specific market niches.

Key Drivers of Europe Confectionery Market Growth

The growth of the Europe confectionery market is propelled by several key drivers. Rising disposable incomes across European nations contribute significantly to increased consumer spending on premium and indulgence products. Evolving lifestyle trends, characterized by busier schedules, fuel the demand for convenient on-the-go snacking options, boosting the snack bar and single-serving confectionery segments. Technological advancements in manufacturing processes enhance efficiency and allow for greater product customization, leading to innovative offerings that cater to niche consumer preferences. Furthermore, a growing consumer awareness of health and wellness is driving the demand for sugar-free, low-calorie, and plant-based confectionery options, creating new market opportunities. Regulatory support for fair trade practices and sustainable sourcing is also influencing product development and consumer choice.

Challenges in the Europe Confectionery Market Sector

Despite robust growth, the Europe confectionery market faces several challenges. Increasing health consciousness among consumers, particularly concerning sugar intake, poses a significant restraint, leading to a potential decline in demand for traditional high-sugar products. Stringent regulatory frameworks regarding food labeling, nutritional content, and ingredient sourcing add complexity to product development and market entry. Supply chain disruptions, influenced by geopolitical events and climate change impacting cocoa production, can lead to price volatility and availability issues. Intense competition from both established global players and emerging regional brands necessitates continuous innovation and aggressive marketing strategies, impacting profit margins. Furthermore, the rising cost of raw materials, including cocoa, sugar, and dairy, poses a continuous challenge to maintaining competitive pricing.

Emerging Opportunities in Europe Confectionery Market

Emerging opportunities in the Europe confectionery market are primarily driven by evolving consumer preferences and technological advancements. The demand for plant-based and vegan confectionery products is rapidly expanding, presenting a significant opportunity for manufacturers to develop and market innovative alternatives. The trend towards personalized nutrition and functional confectionery, offering added health benefits beyond mere indulgence, is gaining traction. This includes products fortified with vitamins, minerals, or probiotics. The burgeoning online retail sector offers a direct-to-consumer channel for niche and artisanal confectionery brands to reach a wider audience. Furthermore, sustainable sourcing and ethical production practices are becoming key purchasing drivers, creating opportunities for brands that prioritize transparency and environmental responsibility in their supply chains. The exploration of novel flavor profiles and international culinary influences also presents avenues for product differentiation.

Leading Players in the Europe Confectionery Market Market

- Nestlé SA

- Delica AG

- Chocoladefabriken Lindt & Sprüngli AG

- Perfetti Van Melle BV

- The Otmuchów Group

- Valrhona Chocolate

- August Storck KG

- Ferrero International SA

- Mars Incorporated

- Yıldız Holding A

- HARIBO Holding GmbH & Co KG

- Sirio Pharma Co Ltd

- Mondelēz International Inc

- Meiji Holdings Company Ltd

- Confiserie Leonidas SA

Key Developments in Europe Confectionery Market Industry

- March 2023: Nestlé launched a new chocolate bar fused with two flavors, i.e., the Purple One and Green Triangle, available in supermarkets across the United Kingdom.

- October 2022: Sirio Pharma launched two new gummies in Europe, available in various fruit flavors and shapes.

- August 2022: The German brand Haribo opened its first brand store in Poland.

Strategic Outlook for Europe Confectionery Market Market

The strategic outlook for the Europe confectionery market is one of sustained growth and continuous evolution. Key growth catalysts include the ongoing demand for premium and artisanal products, driven by increasing consumer sophistication and a willingness to indulge in high-quality confectionery. The persistent focus on health and wellness will continue to fuel innovation in sugar-free, low-calorie, and plant-based offerings, creating significant market penetration opportunities. Furthermore, the expansion of e-commerce platforms provides a robust channel for direct-to-consumer sales and niche market access. Companies that prioritize sustainable sourcing, transparent ingredient labeling, and innovative product development will be well-positioned to capture market share. The strategic integration of new technologies in production and distribution, alongside agile responses to shifting consumer preferences, will be crucial for long-term success.

Europe Confectionery Market Segmentation

-

1. Confections

-

1.1. Chocolate

-

1.1.1. By Confectionery Variant

- 1.1.1.1. Dark Chocolate

- 1.1.1.2. Milk and White Chocolate

-

1.1.1. By Confectionery Variant

-

1.2. Gums

- 1.2.1. Bubble Gum

-

1.2.2. Chewing Gum

-

1.2.2.1. By Sugar Content

- 1.2.2.1.1. Sugar Chewing Gum

- 1.2.2.1.2. Sugar-free Chewing Gum

-

1.2.2.1. By Sugar Content

-

1.3. Snack Bar

- 1.3.1. Cereal Bar

- 1.3.2. Fruit & Nut Bar

- 1.3.3. Protein Bar

-

1.4. Sugar Confectionery

- 1.4.1. Hard Candy

- 1.4.2. Lollipops

- 1.4.3. Mints

- 1.4.4. Pastilles, Gummies, and Jellies

- 1.4.5. Toffees and Nougats

- 1.4.6. Others

-

1.1. Chocolate

-

2. Distribution Channel

- 2.1. Convenience Store

- 2.2. Online Retail Store

- 2.3. Supermarket/Hypermarket

- 2.4. Others

Europe Confectionery Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Confectionery Market Regional Market Share

Geographic Coverage of Europe Confectionery Market

Europe Confectionery Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.69% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Confections

- 5.1.1. Chocolate

- 5.1.1.1. By Confectionery Variant

- 5.1.1.1.1. Dark Chocolate

- 5.1.1.1.2. Milk and White Chocolate

- 5.1.1.1. By Confectionery Variant

- 5.1.2. Gums

- 5.1.2.1. Bubble Gum

- 5.1.2.2. Chewing Gum

- 5.1.2.2.1. By Sugar Content

- 5.1.2.2.1.1. Sugar Chewing Gum

- 5.1.2.2.1.2. Sugar-free Chewing Gum

- 5.1.2.2.1. By Sugar Content

- 5.1.3. Snack Bar

- 5.1.3.1. Cereal Bar

- 5.1.3.2. Fruit & Nut Bar

- 5.1.3.3. Protein Bar

- 5.1.4. Sugar Confectionery

- 5.1.4.1. Hard Candy

- 5.1.4.2. Lollipops

- 5.1.4.3. Mints

- 5.1.4.4. Pastilles, Gummies, and Jellies

- 5.1.4.5. Toffees and Nougats

- 5.1.4.6. Others

- 5.1.1. Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Store

- 5.2.2. Online Retail Store

- 5.2.3. Supermarket/Hypermarket

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Confections

- 6. Europe Confectionery Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Confections

- 6.1.1. Chocolate

- 6.1.1.1. By Confectionery Variant

- 6.1.1.1.1. Dark Chocolate

- 6.1.1.1.2. Milk and White Chocolate

- 6.1.1.1. By Confectionery Variant

- 6.1.2. Gums

- 6.1.2.1. Bubble Gum

- 6.1.2.2. Chewing Gum

- 6.1.2.2.1. By Sugar Content

- 6.1.2.2.1.1. Sugar Chewing Gum

- 6.1.2.2.1.2. Sugar-free Chewing Gum

- 6.1.2.2.1. By Sugar Content

- 6.1.3. Snack Bar

- 6.1.3.1. Cereal Bar

- 6.1.3.2. Fruit & Nut Bar

- 6.1.3.3. Protein Bar

- 6.1.4. Sugar Confectionery

- 6.1.4.1. Hard Candy

- 6.1.4.2. Lollipops

- 6.1.4.3. Mints

- 6.1.4.4. Pastilles, Gummies, and Jellies

- 6.1.4.5. Toffees and Nougats

- 6.1.4.6. Others

- 6.1.1. Chocolate

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Convenience Store

- 6.2.2. Online Retail Store

- 6.2.3. Supermarket/Hypermarket

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Confections

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Nestlé SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Delica AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Chocoladefabriken Lindt & Sprüngli AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Perfetti Van Melle BV

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 The Otmuchów Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Valrhona Chocolate

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 August Storck KG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ferrero International SA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mars Incorporated

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Yıldız Holding A

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 HARIBO Holding GmbH & Co KG

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Sirio Pharma Co Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Mondelēz International Inc

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Meiji Holdings Company Ltd

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Confiserie Leonidas SA

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Nestlé SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Confectionery Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Confectionery Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 2: Europe Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 3: Europe Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Europe Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: Europe Confectionery Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Europe Confectionery Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Europe Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 8: Europe Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 9: Europe Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Europe Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 11: Europe Confectionery Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Europe Confectionery Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: Germany Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: France Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: Italy Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Italy Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Spain Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Spain Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: Netherlands Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Netherlands Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Belgium Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Belgium Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Sweden Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Sweden Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Norway Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Norway Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Poland Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Poland Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 33: Denmark Europe Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Denmark Europe Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Confectionery Market?

The projected CAGR is approximately 4.69%.

2. Which companies are prominent players in the Europe Confectionery Market?

Key companies in the market include Nestlé SA, Delica AG, Chocoladefabriken Lindt & Sprüngli AG, Perfetti Van Melle BV, The Otmuchów Group, Valrhona Chocolate, August Storck KG, Ferrero International SA, Mars Incorporated, Yıldız Holding A, HARIBO Holding GmbH & Co KG, Sirio Pharma Co Ltd, Mondelēz International Inc, Meiji Holdings Company Ltd, Confiserie Leonidas SA.

3. What are the main segments of the Europe Confectionery Market?

The market segments include Confections, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 72.38 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Consumption of Baked Goods; Demand for Indigenous Fermented Foods.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Potential Side-effects of Yeast.

8. Can you provide examples of recent developments in the market?

March 2023: Nestlé launched a new chocolate bar fused with two flavors, i.e., the Purple One and Green Triangle. These chocolate bars are available in supermarkets across the United Kingdom.October 2022: Sirio Pharma launched two new gummies in Europe. The gummies are available in various fruit flavors and shapes.August 2022: The German brand Haribo opened its first brand store in Poland.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Confectionery Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Confectionery Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Confectionery Market?

To stay informed about further developments, trends, and reports in the Europe Confectionery Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence