Key Insights

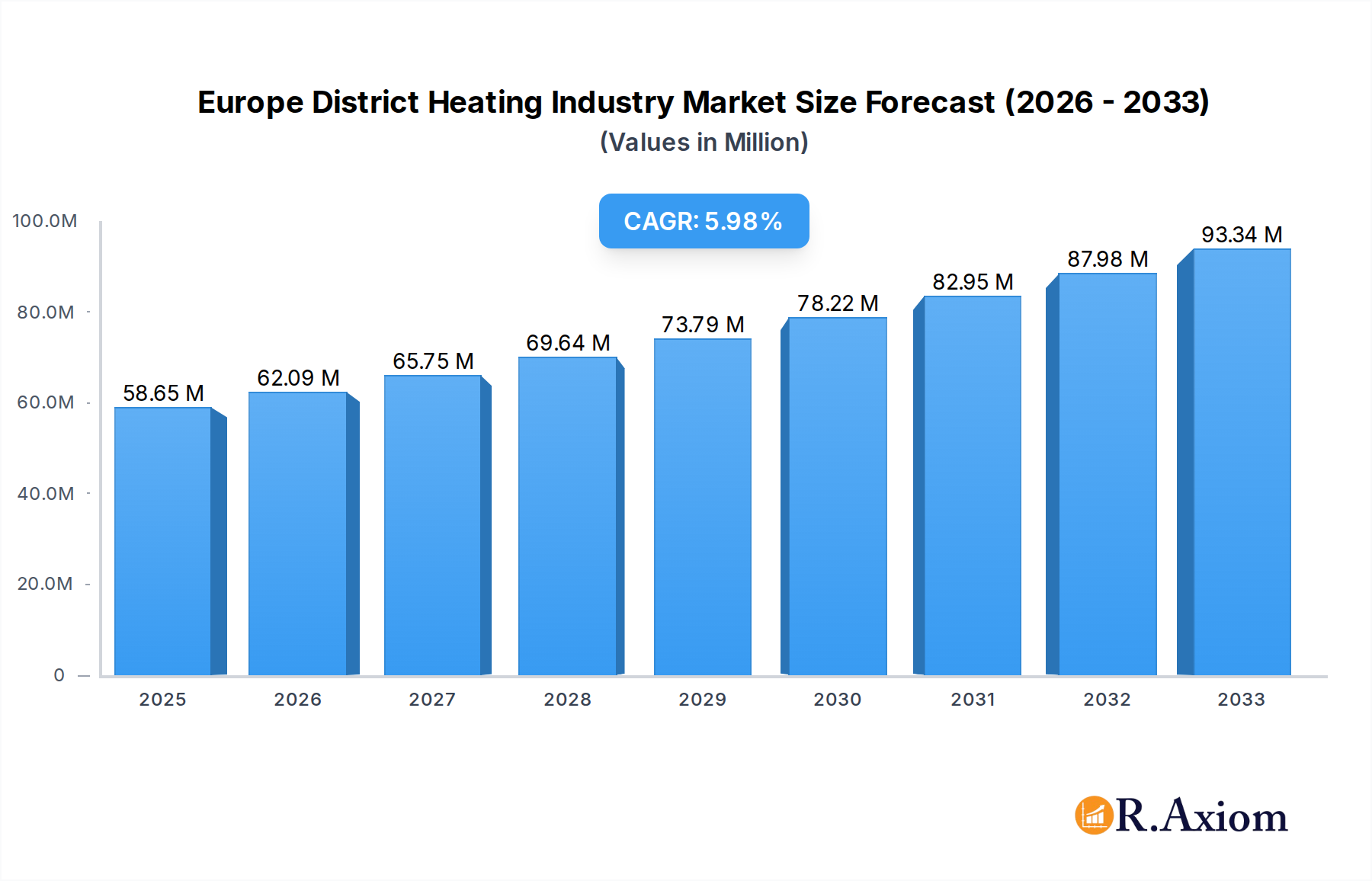

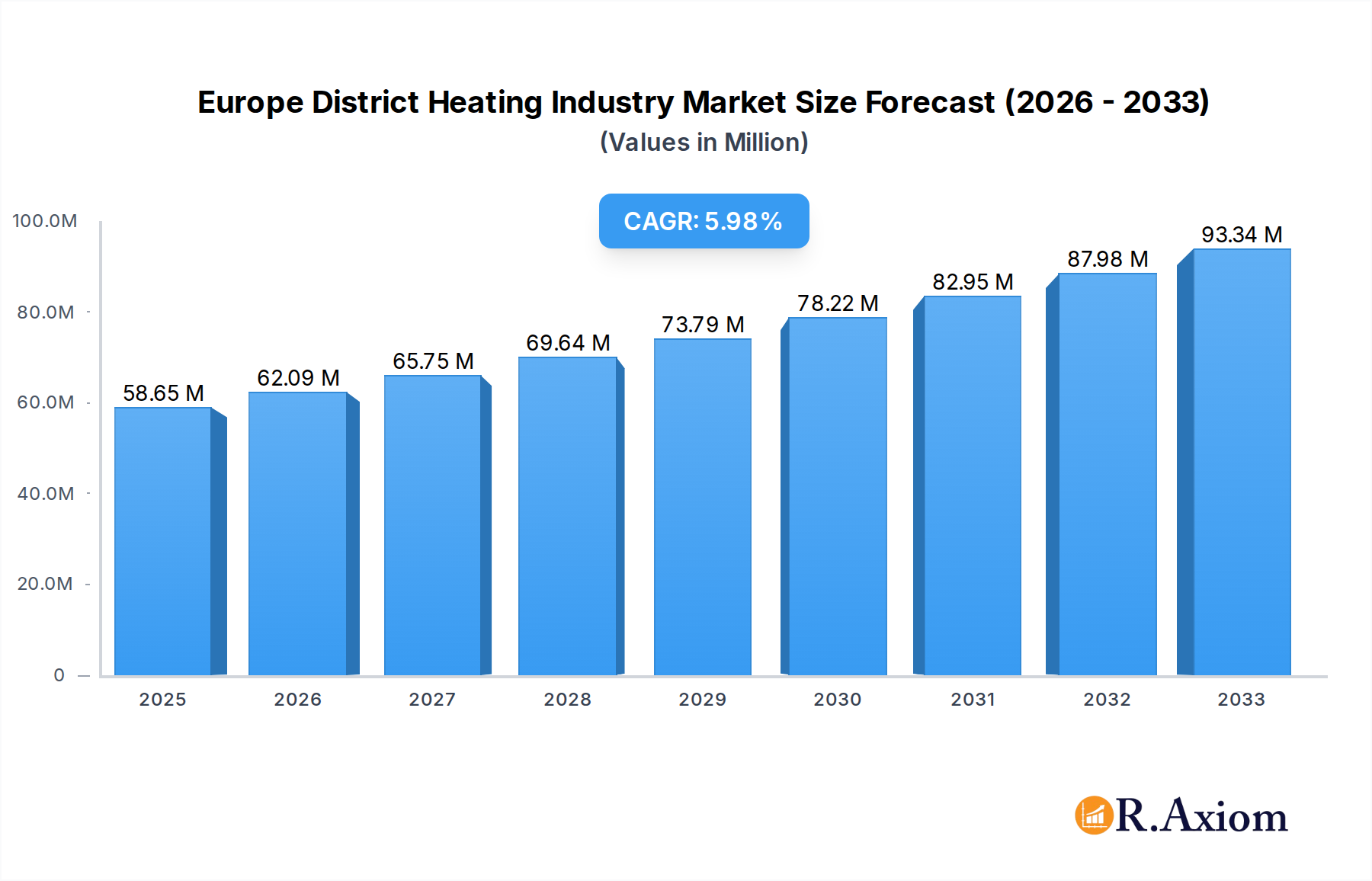

The European District Heating market is poised for significant expansion, currently valued at an estimated $58.65 million and projected to grow at a robust Compound Annual Growth Rate (CAGR) of 5.90% from 2025 to 2033. This substantial growth trajectory is fueled by a confluence of factors, primarily driven by increasing governmental support for renewable energy integration and the urgent need to decarbonize urban heating systems. The push towards sustainable energy solutions, coupled with the inherent efficiency and reliability of district heating networks, positions this market as a critical component of Europe's energy transition strategy. Key drivers include stringent environmental regulations, rising fossil fuel prices making centralized heating more economically viable, and advancements in heat network technologies that enhance operational efficiency and reduce heat loss. The growing awareness of climate change and the imperative to reduce carbon footprints are further accelerating the adoption of district heating solutions across residential, commercial, and industrial sectors.

Europe District Heating Industry Market Size (In Million)

The European District Heating market's expansion is further bolstered by a strong emphasis on energy efficiency and the utilization of waste heat sources, such as industrial processes and wastewater. The market is witnessing significant investments from prominent players like Danfoss AS, Engie SA, and Vattenfall AB, indicating a healthy competitive landscape and ongoing innovation. Emerging trends include the integration of smart grid technologies for optimized heat distribution, the development of advanced materials for lower heat loss, and the increasing use of biomass and geothermal energy as primary heat sources. While the market benefits from strong governmental backing and technological advancements, potential restraints include high initial infrastructure investment costs and complex regulatory frameworks in certain regions. However, the long-term benefits of reduced emissions, enhanced energy security, and lower operational costs are expected to outweigh these challenges, paving the way for sustained growth throughout the forecast period.

Europe District Heating Industry Company Market Share

Europe District Heating Industry Market Concentration & Innovation

The Europe District Heating Industry is characterized by a moderate to high level of market concentration, with established players like Engie SA, Vattenfall AB, and Danfoss AS holding significant market shares. Innovation is a key driver, propelled by the increasing demand for sustainable energy solutions and stringent environmental regulations. Companies are investing heavily in research and development for more efficient heat generation technologies, smart grid integration, and waste heat recovery systems. Regulatory frameworks, particularly those promoting decarbonization and renewable energy adoption, are crucial. For instance, the EU's Renewable Energy Directive and Energy Efficiency Directive significantly influence market dynamics. Product substitutes, such as individual heat pumps and direct electric heating, exist but face increasing competition from district heating's economies of scale and environmental benefits. End-user trends are shifting towards greater demand for low-carbon heating options, particularly from residential and commercial sectors seeking to reduce their carbon footprint. Mergers and acquisitions (M&A) activities are on the rise as larger companies consolidate their market positions and acquire innovative technologies. For example, M&A deal values are projected to reach hundreds of millions of Euros annually.

Europe District Heating Industry Industry Trends & Insights

The Europe District Heating Industry is experiencing robust growth, driven by a confluence of factors including escalating energy prices, a strong political will towards decarbonization, and increasing awareness of the environmental benefits of centralized heating systems. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 8% over the forecast period of 2025–2033. Technological disruptions are playing a pivotal role, with advancements in heat pump technology, geothermal energy utilization, and sophisticated waste heat recovery systems transforming the landscape. Alfa Laval AB's innovative waste heat recovery solutions, as exemplified by its project in Hamburg, Germany, highlight the industry's move towards circular economy principles and leveraging industrial byproducts for heating. Consumer preferences are increasingly leaning towards sustainable and cost-effective heating solutions. The residential sector, in particular, is showing a growing appetite for district heating due to its reliability and reduced operational burdens compared to individual heating systems. Commercial and industrial sectors are also key adopters, driven by corporate sustainability goals and the potential for significant cost savings through optimized energy management. Competitive dynamics are intensifying, with traditional energy providers, utility companies, and technology manufacturers vying for market share. The integration of smart technologies, such as IoT-enabled sensors and advanced data analytics, is enhancing operational efficiency and enabling personalized heating solutions. Market penetration is steadily increasing across the continent, with countries like Sweden, Denmark, and Finland leading the way due to their long-standing commitment to district heating infrastructure. The trend towards electrification and the integration of renewable energy sources into district heating networks are further shaping the industry's trajectory, creating a more resilient and sustainable energy future. The Bristol City Leap project, a significant partnership between Ameresco and Vattenfall, demonstrates a substantial investment of approximately USD 1.28 billion in low-carbon energy infrastructure, underscoring the massive scale of ongoing decarbonization efforts and the central role of district heating in achieving these ambitious goals. This project alone aims to deliver substantial carbon savings and zero-carbon energy generation, showcasing the tangible impact of these industry trends.

Dominant Markets & Segments in Europe District Heating Industry

The leading region within the Europe District Heating Industry is undeniably Northern Europe, with countries like Sweden, Denmark, and Finland at the forefront of adoption and development. This dominance stems from a combination of long-standing economic policies that have prioritized energy efficiency and renewable energy, a historical reliance on centralized heating solutions, and a strong societal commitment to environmental sustainability.

- Economic Policies: Governments in these Nordic countries have consistently implemented supportive policies, including generous subsidies, tax incentives, and stringent building codes that favor district heating. These policies have created a stable and predictable investment environment, encouraging the expansion of existing networks and the development of new ones.

- Infrastructure Development: Decades of strategic investment in robust district heating infrastructure have established a strong foundation. This includes extensive pipe networks, efficient heat generation plants utilizing diverse fuel sources, and advanced control systems.

- Environmental Regulations: Strict emission standards and ambitious climate targets have pushed utilities and consumers towards cleaner heating alternatives. District heating, especially when powered by renewable sources or waste heat, offers a clear path to decarbonization.

- Societal Acceptance and Awareness: A high level of public awareness regarding the benefits of district heating, such as reduced local air pollution and stable heating costs, has fostered widespread acceptance and demand.

Within the End User segment, the Residential sector often represents the largest share of demand for district heating due to the high density of households in urban and suburban areas. This segment benefits from the convenience, reliability, and often lower operational costs associated with district heating compared to individual heating systems.

The Commercial sector is another significant segment, encompassing office buildings, retail spaces, and public institutions. These users are increasingly driven by corporate social responsibility (CSR) initiatives, seeking to reduce their carbon footprint and enhance their building's energy performance. District heating provides a straightforward way to achieve these goals.

The Industrial segment, while sometimes more complex in its heating requirements, presents substantial opportunities, particularly through waste heat recovery. Industries generating significant amounts of waste heat, such as manufacturing plants and power stations, can integrate their heat byproducts into district heating networks, creating a mutually beneficial synergy. The Alfa Laval example in Hamburg vividly illustrates this potential, where industrial waste heat from a sulphuric acid plant now serves over 23,000 households, hotels, offices, and a university, showcasing the immense potential for this segment to contribute to a greener energy future.

Europe District Heating Industry Product Developments

Product developments in the Europe District Heating Industry are focused on enhancing efficiency, sustainability, and integration. Innovations in advanced heat exchangers, such as those developed by Alfa Laval AB, are enabling more effective recovery and transfer of waste heat from industrial processes and data centers. Smart grid technologies and IoT sensors are being integrated to optimize heat distribution, improve energy management, and enable demand-side response. Furthermore, the development of low-temperature district heating networks, powered by renewable sources like geothermal and solar thermal energy, is a key trend, reducing heat loss and increasing the viability of a wider range of heat sources. The competitive advantage lies in solutions that offer lower operational costs, reduced carbon emissions, and increased reliability for end-users across residential, commercial, and industrial sectors.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Europe District Heating Industry, segmented by end-user type. The primary segments covered are:

- Residential: This segment focuses on the demand for district heating in homes, apartments, and multi-unit dwellings. Growth projections indicate a steady increase driven by urban densification and a preference for reliable, low-carbon heating solutions. Market sizes are significant due to the high volume of households.

- Commercial: This segment encompasses heating solutions for office buildings, retail establishments, hotels, hospitals, and educational institutions. Growth in this segment is spurred by corporate sustainability mandates and the desire for energy cost predictability.

- Industrial: This segment includes district heating applications for manufacturing plants, processing facilities, and other industrial operations. Significant growth is anticipated from the integration of waste heat recovery systems, offering unique competitive dynamics based on energy synergy.

Key Drivers of Europe District Heating Industry Growth

Several key drivers are propelling the growth of the Europe District Heating Industry. Technologically, advancements in heat pump efficiency, the successful integration of renewable energy sources like geothermal and solar thermal, and the innovative recovery of industrial waste heat are paramount. Economically, rising fossil fuel prices and the demand for stable, predictable energy costs for consumers and businesses are major catalysts. Regulatorily, stringent government mandates for decarbonization, ambitious climate targets, and supportive policies such as subsidies and tax incentives for renewable energy infrastructure are crucial. The growing public awareness and demand for sustainable living further amplify these drivers, creating a fertile ground for district heating expansion across the continent.

Challenges in the Europe District Heating Industry Sector

Despite its promising growth, the Europe District Heating Industry faces several significant challenges. Regulatory hurdles, including complex permitting processes and varying national policies, can slow down project development. Supply chain issues, particularly for specialized components and skilled labor, can lead to project delays and increased costs. The significant upfront capital investment required for network expansion and new plant construction presents a substantial barrier, especially for smaller operators. Furthermore, competition from decentralized renewable energy solutions like individual heat pumps, though often less efficient at scale, can pose a challenge in certain markets. The need for extensive infrastructure upgrades and the potential for disruptions during construction also contribute to the complexities of market expansion.

Emerging Opportunities in Europe District Heating Industry

Emerging opportunities in the Europe District Heating Industry are abundant and diverse. The integration of waste heat from new sources, such as data centers and wastewater treatment plants, presents a significant untapped potential. The expansion of district heating networks into new urban and suburban areas, previously underserved, offers substantial market growth. The development and adoption of advanced smart grid technologies and AI-driven optimization tools can enhance network efficiency and customer experience. Furthermore, the increasing focus on circular economy principles and the utilization of biomass and other sustainable fuels present exciting avenues for innovation and market expansion, contributing to a more resilient and environmentally friendly energy landscape.

Leading Players in the Europe District Heating Industry Market

- Danfoss AS

- Engie SA

- Vattenfall AB

- Göteborg Energi

- Statkraft AS

- Logstor AS

- Vital Energi Ltd

- Ramboll Group AS

- Alfa Laval AB

Key Developments in Europe District Heating Industry Industry

- May 2022: Alfa Laval deployed its unique technology to recover industrial waste heat from a sulphuric acid plant for reuse in a district heating network in Hamburg, Germany. More than 23,000 households, hotels, offices, and the university will benefit from more heating as the company expands the waste heat recovery project, which Alfa Laval first installed in 2018. The project contributes to the city’s green footprint as a part of a German government initiative.

- March 2022: A prominent American energy services company, Ameresco, announced that it would partner with Vattenfall, attracting investment worth around EUR 1.2 billion (USD 1.28 billion) for the Bristol City Leap project, a 20-year concession to decarbonize the city. Over the first five years of the partnership, the project will deliver around GBP 424 million (USD 521.49 million) in low-carbon energy infrastructure across heat networks, renewable energy, heat pumps, energy efficiency, and electric vehicle charging. The project will account for around 140,000 tonnes of carbon savings and 182 MW of zero-carbon energy generation.

Strategic Outlook for Europe District Heating Industry Market

The strategic outlook for the Europe District Heating Industry is exceptionally positive, driven by the imperative to decarbonize energy systems and achieve ambitious climate goals. Continued investment in renewable energy integration and waste heat recovery will be central to future growth. Policy support, particularly for expanding infrastructure and incentivizing adoption, will remain a critical growth catalyst. The industry is poised for significant expansion, leveraging technological advancements to offer more efficient, sustainable, and cost-effective heating solutions to a growing number of residential, commercial, and industrial customers across the continent. The ongoing shift towards smart cities and sustainable urban development further solidifies district heating's role as a cornerstone of future energy systems.

Europe District Heating Industry Segmentation

-

1. End User

- 1.1. Residential

- 1.2. Commercial and Industrial

Europe District Heating Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

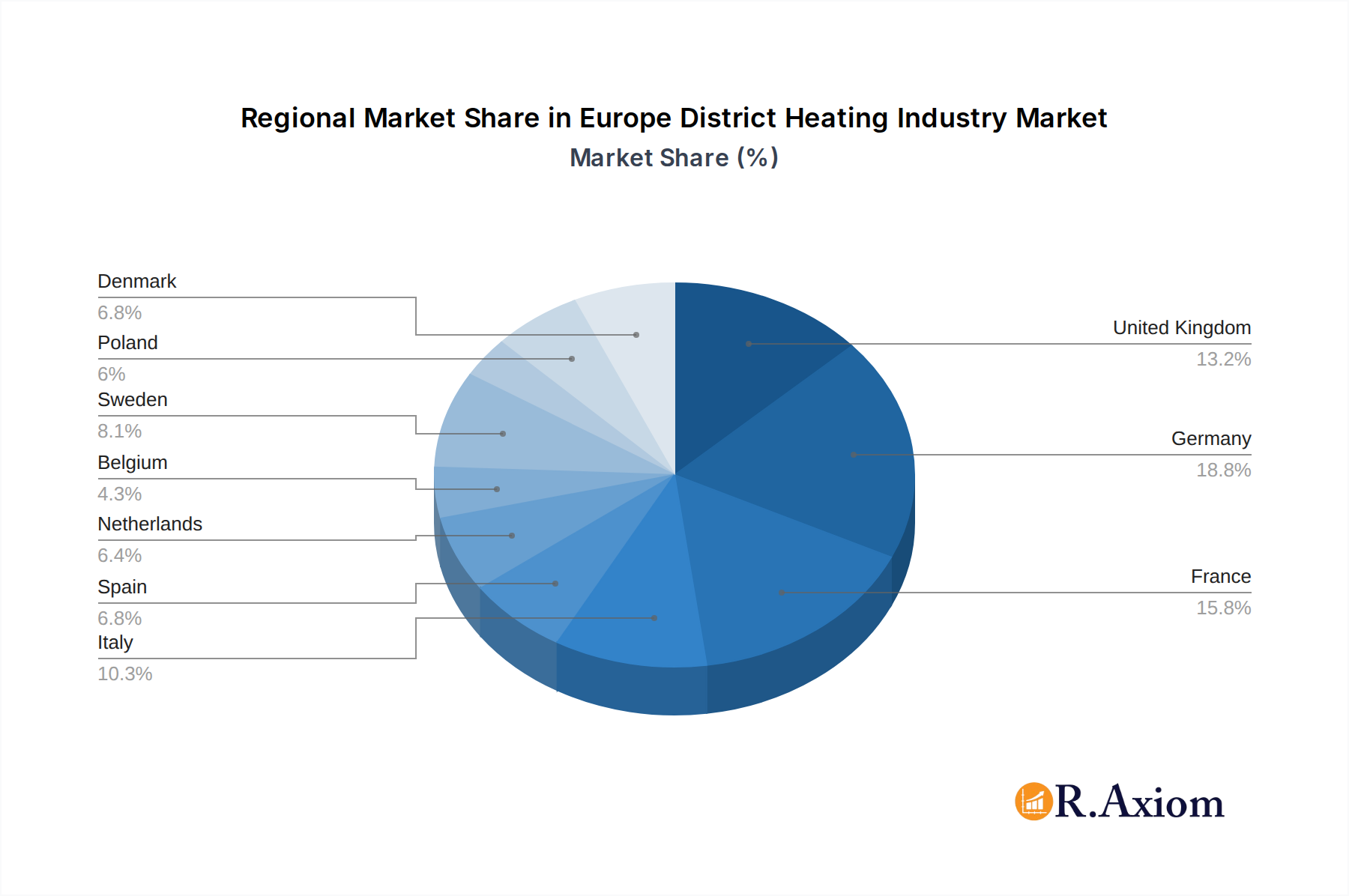

Europe District Heating Industry Regional Market Share

Geographic Coverage of Europe District Heating Industry

Europe District Heating Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Residential

- 5.1.2. Commercial and Industrial

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. Europe District Heating Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User

- 6.1.1. Residential

- 6.1.2. Commercial and Industrial

- 6.1. Market Analysis, Insights and Forecast - by End User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Danfoss AS

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Engie SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Vattenfall AB

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Göteborg Energi

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Statkraft AS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Logstor AS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Vital Energi Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ramboll Group AS*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Alfa Laval AB

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Danfoss AS

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe District Heating Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe District Heating Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe District Heating Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 2: Europe District Heating Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Europe District Heating Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Europe District Heating Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: France Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe District Heating Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe District Heating Industry?

The projected CAGR is approximately 5.90%.

2. Which companies are prominent players in the Europe District Heating Industry?

Key companies in the market include Danfoss AS, Engie SA, Vattenfall AB, Göteborg Energi, Statkraft AS, Logstor AS, Vital Energi Ltd, Ramboll Group AS*List Not Exhaustive, Alfa Laval AB.

3. What are the main segments of the Europe District Heating Industry?

The market segments include End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 58.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Augmented Demand for Energy-efficient and Cost effective Heating Systems; Rising Urbanization and Industrialization.

6. What are the notable trends driving market growth?

Residential End User Segment is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Stringent Regulations and Validatory Guidelines.

8. Can you provide examples of recent developments in the market?

May 2022: Alfa Laval deployed its unique technology to recover industrial waste heat from a sulphuric acid plant for reuse in a district heating network in Hamburg, Germany. More than 23,000 households, hotels, offices, and the university will benefit from more heating as the company expands the waste heat recovery project, which Alfa Laval first installed in 2018. The project contributes to the city’s green footprint as a part of a German government initiative.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe District Heating Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe District Heating Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe District Heating Industry?

To stay informed about further developments, trends, and reports in the Europe District Heating Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence