Key Insights

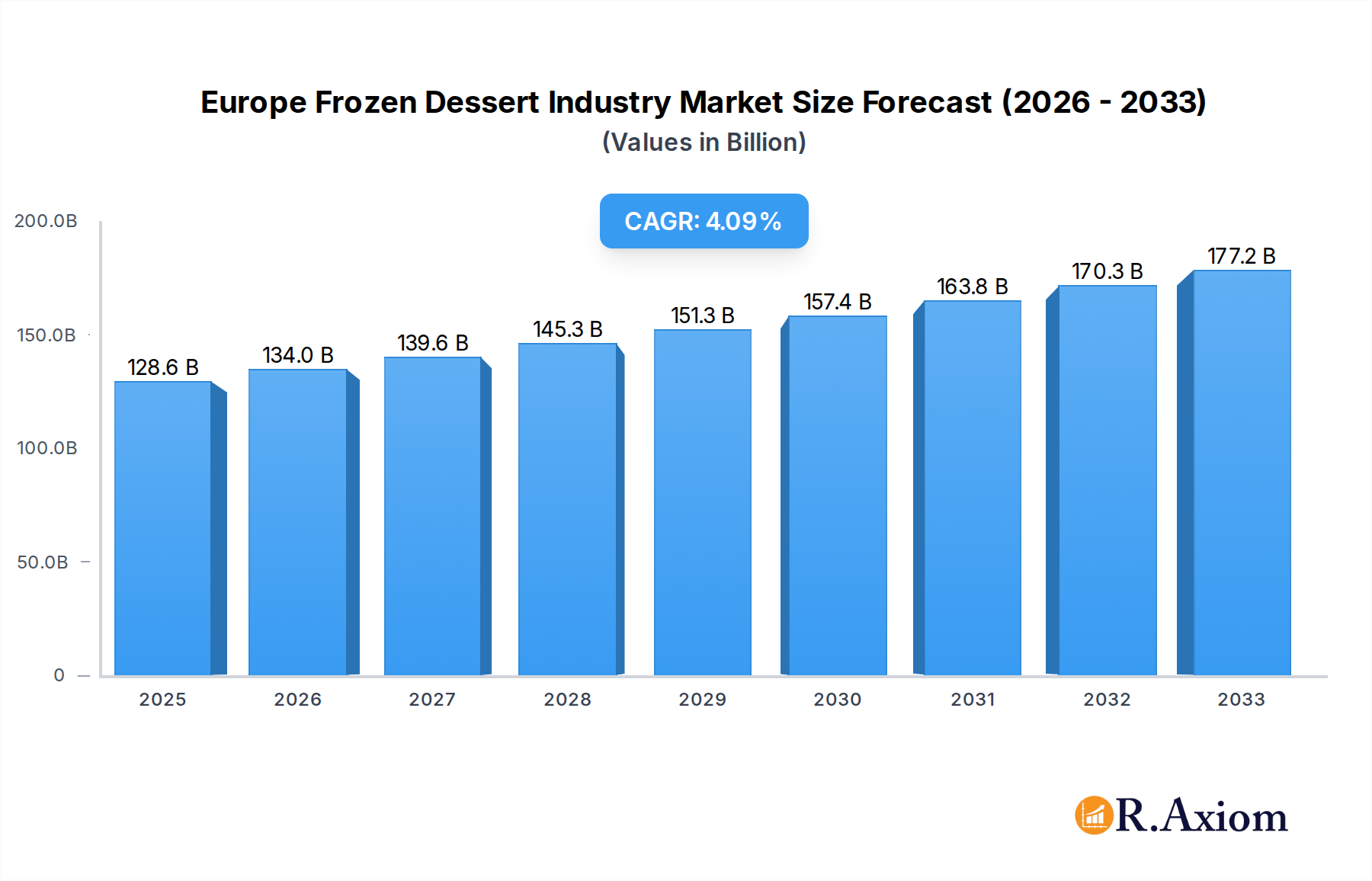

The European frozen dessert market is poised for significant growth, projected to reach USD 128.56 billion in 2025. This expansion is fueled by an anticipated Compound Annual Growth Rate (CAGR) of 4.3% from 2019 to 2033, indicating sustained consumer demand and market dynamism. Key drivers behind this robust performance include the increasing preference for premium and indulgent frozen treats, a growing health-conscious segment opting for lower-fat or plant-based alternatives, and the continuous innovation in product flavors and formats. The market is segmented across various product types, with ice cream, encompassing artisanal, dairy-based, and water-based varieties, holding a substantial share. Frozen yogurt also commands significant attention, reflecting evolving consumer tastes. The expansion of distribution channels, particularly the rise of online retail and the strategic placement in supermarkets and hypermarkets, further propels market accessibility and sales. Major players like Unilever, Mondelēz International, and Nestlé are heavily invested in product development and marketing, contributing to the market's vibrant competitive landscape.

Europe Frozen Dessert Industry Market Size (In Billion)

The trajectory of the European frozen dessert industry is further shaped by evolving consumer trends and the strategic responses of leading companies. The growing demand for artisanal and handcrafted frozen desserts, driven by a desire for unique flavors and higher quality ingredients, is a prominent trend. Simultaneously, the rise of health and wellness concerns has led to an increased demand for frozen desserts with reduced sugar, fat content, and plant-based ingredients, including vegan ice cream and dairy-free frozen yogurt. While these trends present significant opportunities, certain restraints may temper growth. Fluctuations in raw material prices, such as dairy and sugar, can impact production costs and profit margins. Additionally, stringent regulations regarding food labeling and ingredient sourcing in various European countries could pose challenges for manufacturers. Despite these potential headwinds, the overall outlook for the European frozen dessert market remains highly positive, with continuous product innovation and expanding distribution networks set to drive sustained revenue growth throughout the forecast period.

Europe Frozen Dessert Industry Company Market Share

Europe Frozen Dessert Industry Market Concentration & Innovation

The Europe frozen dessert market is characterized by a moderate to high level of concentration, with a few global giants like Unilever, Nestlé S.A., and Mondelēz International holding significant market share. These key players leverage their extensive distribution networks, strong brand recognition, and substantial R&D investments to maintain their dominance. Innovation serves as a crucial driver, with companies continually introducing novel flavors, healthier alternatives, and premium artisanal products to cater to evolving consumer preferences. The artisanal ice cream segment and plant-based frozen desserts are experiencing rapid growth, fueled by a desire for unique taste experiences and a focus on health and sustainability.

Regulatory frameworks, while generally supportive of food safety standards, can present challenges, particularly concerning labeling requirements for allergens and nutritional information. The threat of product substitutes, such as chilled desserts and other sweet treats, remains a constant factor, necessitating continuous product differentiation. End-user trends are strongly influenced by increasing health consciousness, leading to a demand for low-sugar, low-fat, and dairy-free options. Mergers and acquisitions (M&A) play a significant role in market consolidation and expansion, with deals often valued in the hundreds of millions of dollars, allowing larger companies to acquire innovative startups and expand their product portfolios. For instance, the acquisition of smaller craft ice cream brands by larger corporations is a recurring trend.

Europe Frozen Dessert Industry Industry Trends & Insights

The Europe frozen dessert industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.2% over the forecast period of 2025–2033. This expansion is underpinned by several interconnected trends and insights that are reshaping consumer behavior and market dynamics. A primary growth driver is the increasing disposable income across various European nations, enabling consumers to indulge in premium and convenience-oriented frozen dessert options. Coupled with this is a growing trend towards health and wellness, prompting manufacturers to innovate with reduced sugar, low-fat, and plant-based frozen desserts. The market penetration of these healthier alternatives is steadily increasing, particularly within the frozen yogurt and dairy-based ice cream segments.

Technological disruptions are also playing a pivotal role. Advancements in refrigeration and freezing technologies are not only improving product quality and shelf life but also enabling more efficient and sustainable production processes. The rise of online retail channels is another significant trend, offering consumers unparalleled convenience and access to a wider variety of products, including niche and gourmet options. This shift in distribution is forcing traditional brick-and-mortar stores to adapt their strategies. Consumer preferences are becoming more sophisticated, with a growing appetite for diverse and exotic flavors, premium ingredients, and transparent sourcing. The demand for artisanal ice cream is a testament to this, with consumers willing to pay a premium for unique, handcrafted experiences. Competitive dynamics are intensifying, with both established global players and agile regional brands vying for market share. The focus is increasingly shifting from basic product offerings to value-added propositions, including ethical sourcing, sustainable packaging, and personalized flavor options. Furthermore, the exploration of novel ingredients and innovative product formats will continue to drive market evolution. The overall market size is projected to reach over €40 billion by 2033.

Dominant Markets & Segments in Europe Frozen Dessert Industry

Within the expansive Europe frozen dessert industry, the Ice Cream segment stands as the undisputed leader, commanding the largest market share and driving much of the sector's growth. This dominance is further segmented, with Dairy-based Ice Cream representing the largest sub-segment due to its widespread appeal, established production infrastructure, and diverse flavor profiles. However, significant growth is also being witnessed in Artisanal Ice Cream, catering to a discerning consumer base seeking premium quality, unique flavors, and locally sourced ingredients.

Supermarkets/Hypermarkets remain the primary distribution channel, owing to their broad reach, accessibility, and ability to cater to a wide demographic. These outlets offer a comprehensive range of frozen desserts, from mass-market brands to premium offerings. The continued investment in chilled infrastructure within these retail giants further solidifies their position. However, the influence of Online Retailers is rapidly expanding, especially in urban centers, driven by convenience and the ability to offer a wider product selection, including specialized and gourmet options. This channel is particularly important for niche brands and direct-to-consumer models.

Several key drivers contribute to the dominance of these markets and segments:

- Economic Policies: Favorable economic conditions, including rising disposable incomes and a stable retail environment across major European economies like Germany, France, the UK, and Italy, directly correlate with increased consumer spending on discretionary food items such as frozen desserts.

- Infrastructure Development: Robust cold chain logistics and advanced retail infrastructure, particularly in Western Europe, ensure the efficient distribution and availability of frozen desserts, supporting high sales volumes.

- Consumer Lifestyle: Increasingly busy lifestyles and a growing demand for convenient, indulgent treats fuel the consumption of frozen desserts. The emphasis on readily available and easy-to-consume products in supermarkets and via online platforms aligns perfectly with this trend.

- Marketing and Brand Penetration: Established brands, through continuous marketing efforts and extensive distribution networks, have achieved high brand penetration, ensuring broad consumer recognition and preference.

The Frozen Yogurt segment is also experiencing substantial growth, driven by its perception as a healthier alternative to traditional ice cream, appealing to health-conscious consumers. While Frozen Cakes and Others represent smaller segments, they offer specialized opportunities and cater to specific occasions and preferences. The overall market size for frozen desserts in Europe is estimated to be around €30 billion in the base year 2025.

Europe Frozen Dessert Industry Product Developments

Product innovation in the Europe frozen dessert industry is primarily focused on healthier formulations, including reduced sugar, low-fat, and dairy-free options utilizing plant-based milk alternatives like oat, almond, and coconut. A significant trend is the development of gourmet and artisanal flavors, incorporating premium ingredients, exotic fruit fusions, and sophisticated flavor pairings to appeal to discerning palates. Convenience formats, such as single-serving portions and ready-to-eat options, are gaining traction. Technological advancements are enabling the creation of novel textures and sensory experiences, enhancing the overall indulgence factor. These developments aim to meet evolving consumer demands for healthier, more diverse, and premium frozen dessert options, providing a competitive advantage in a dynamic market.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Europe frozen dessert industry, segmented by Product Type and Distribution Channel. Under Product Type, the market is meticulously dissected into Frozen Yogurt, Ice Cream (further broken down into Artisanal Ice Cream, Dairy-based Ice Cream, and Water-based Ice Cream), Frozen Cakes, and Others. The Ice Cream segment is projected to maintain its dominance, with Dairy-based Ice Cream leading in market size, while Artisanal Ice Cream is expected to exhibit the highest growth rate.

The Distribution Channel segmentation includes Supermarkets/Hypermarkets, Convenience Stores, Speciality Stores, Online Retailer, and Others. Supermarkets/Hypermarkets are anticipated to retain the largest market share due to their extensive reach. However, Online Retailers are projected to experience the fastest growth, driven by increasing e-commerce adoption and consumer demand for convenience. Each segment's market size, growth projections, and competitive dynamics are thoroughly examined to provide actionable insights for industry stakeholders. The overall market for frozen desserts in Europe is estimated to be in the range of €30 billion to €32 billion for the base year 2025.

Key Drivers of Europe Frozen Dessert Industry Growth

The Europe frozen dessert industry is propelled by several key growth drivers. Increasing consumer demand for indulgence and premiumization fuels the expansion of the artisanal and gourmet ice cream segments. Simultaneously, a growing health consciousness is driving the demand for healthier alternatives, including low-sugar, low-fat, and plant-based frozen desserts, particularly frozen yogurt. Technological advancements in production and ingredient innovation are enabling the development of novel products and improved manufacturing efficiencies. Furthermore, the expansion of online retail channels is enhancing accessibility and convenience, broadening the market reach for a diverse range of frozen dessert products across Europe.

Challenges in the Europe Frozen Dessert Industry Sector

Despite significant growth opportunities, the Europe frozen dessert industry faces several challenges. Fluctuating raw material prices, particularly for dairy and sugar, can impact production costs and profit margins. Stringent food safety regulations and labeling requirements across different European countries necessitate continuous compliance efforts and can increase operational complexity. Intense competition from both global players and emerging niche brands exerts downward pressure on pricing and demands constant innovation to maintain market share. Furthermore, logistical complexities and the need for maintaining a strict cold chain throughout the supply chain present ongoing operational and cost challenges, particularly for perishable goods like frozen desserts.

Emerging Opportunities in Europe Frozen Dessert Industry

The Europe frozen dessert industry is ripe with emerging opportunities. The increasing consumer interest in sustainable and ethically sourced ingredients presents a significant avenue for brands that prioritize transparency and eco-friendly practices. The burgeoning plant-based food movement continues to create substantial demand for innovative dairy-free frozen desserts. Furthermore, the trend towards personalized and customizable frozen dessert experiences, especially through online platforms and bespoke offerings, offers a unique market niche. The growing popularity of functional frozen desserts, incorporating probiotics, vitamins, or other health-enhancing ingredients, also presents a promising area for product development and market expansion.

Leading Players in the Europe Frozen Dessert Industry Market

- Unilever

- Mondelēz International

- Nestlé S.A.

- General Mills Inc.

- Fonterra Co-operative Group

- Dunkin' Brands Group Inc.

- Chobani LLC

- Blue Bell Creameries LP

Key Developments in Europe Frozen Dessert Industry Industry

- 2023/Q4: Unilever launches a new range of vegan ice cream flavors across key European markets, responding to rising demand for plant-based options.

- 2023/Q3: Mondelēz International acquires a European artisanal gelato producer, strengthening its premium frozen dessert portfolio.

- 2023/Q2: Nestlé S.A. announces significant investments in sustainable packaging solutions for its frozen dessert brands in Europe.

- 2023/Q1: General Mills Inc. expands its partnership with online grocery retailers, enhancing direct-to-consumer delivery of its frozen dessert products.

- 2022/Q4: Fonterra Co-operative Group introduces a new line of dairy-based frozen desserts with reduced sugar content, targeting health-conscious consumers.

Strategic Outlook for Europe Frozen Dessert Industry Market

The strategic outlook for the Europe frozen dessert industry remains highly optimistic, driven by sustained consumer demand for both indulgent and healthier options. Key growth catalysts include the continuous innovation in flavor profiles and ingredient sourcing, particularly with a focus on natural and premium components. The ongoing expansion and optimization of online retail channels will further enhance market accessibility and convenience. Brands that successfully leverage plant-based alternatives and sustainable practices are well-positioned for significant market penetration. Strategic collaborations and potential M&A activities will likely continue to shape the competitive landscape, fostering growth and diversification within this dynamic sector.

Europe Frozen Dessert Industry Segmentation

-

1. Product Type

- 1.1. Frozen Yogurt

-

1.2. Ice Cream

- 1.2.1. Artisanal Ice Cream

- 1.2.2. Dairy-based Ice Cream

- 1.2.3. Water-based Ice Cream

- 1.3. Frozen Cakes

- 1.4. Others

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Speciality Stores

- 2.4. Online Retailer

- 2.5. Others

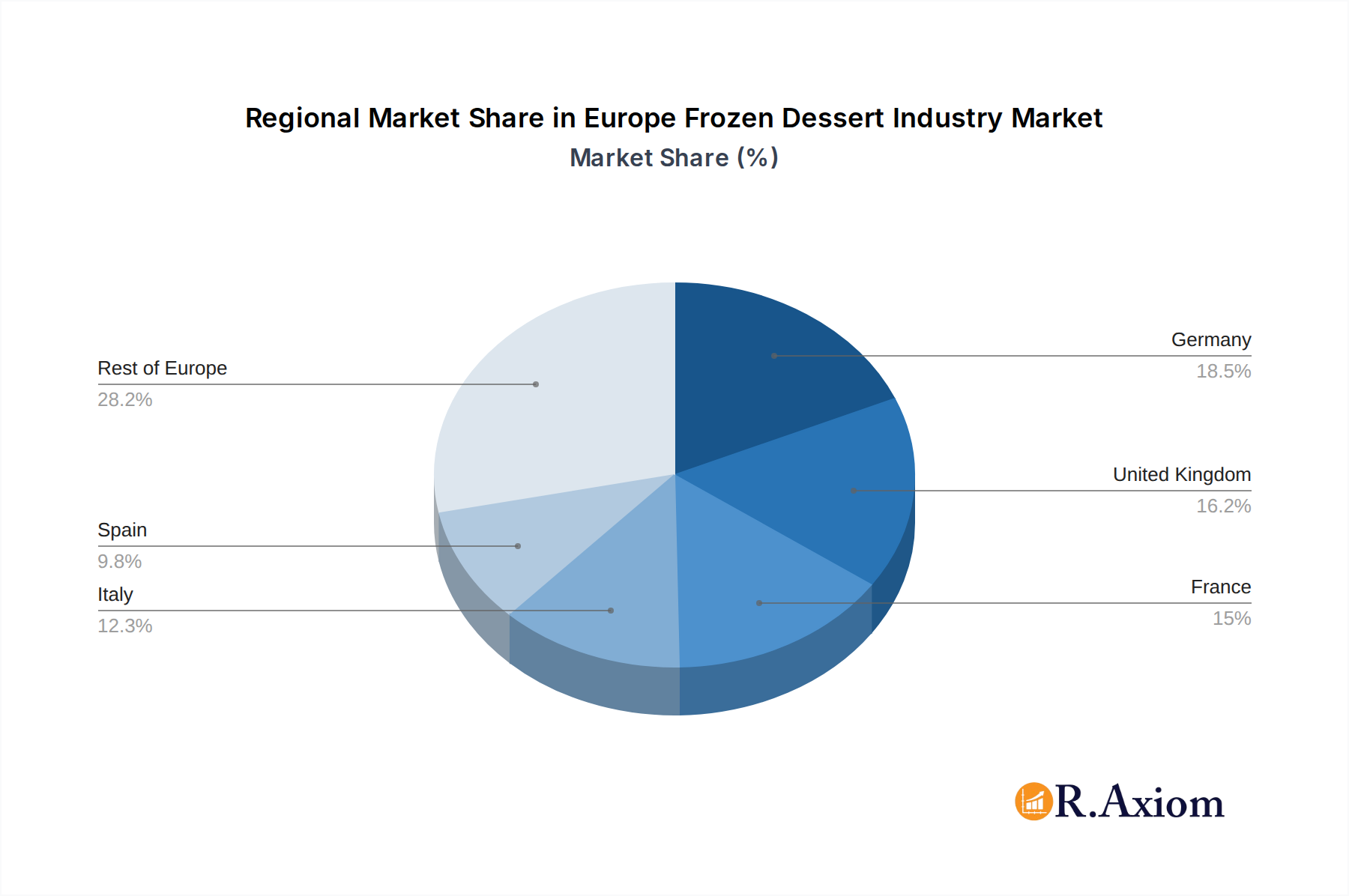

Europe Frozen Dessert Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Frozen Dessert Industry Regional Market Share

Geographic Coverage of Europe Frozen Dessert Industry

Europe Frozen Dessert Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Frozen Yogurt

- 5.1.2. Ice Cream

- 5.1.2.1. Artisanal Ice Cream

- 5.1.2.2. Dairy-based Ice Cream

- 5.1.2.3. Water-based Ice Cream

- 5.1.3. Frozen Cakes

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Speciality Stores

- 5.2.4. Online Retailer

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Spain

- 5.3.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Frozen Yogurt

- 6.1.2. Ice Cream

- 6.1.2.1. Artisanal Ice Cream

- 6.1.2.2. Dairy-based Ice Cream

- 6.1.2.3. Water-based Ice Cream

- 6.1.3. Frozen Cakes

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Speciality Stores

- 6.2.4. Online Retailer

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Germany Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Frozen Yogurt

- 7.1.2. Ice Cream

- 7.1.2.1. Artisanal Ice Cream

- 7.1.2.2. Dairy-based Ice Cream

- 7.1.2.3. Water-based Ice Cream

- 7.1.3. Frozen Cakes

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets/Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Speciality Stores

- 7.2.4. Online Retailer

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. United Kingdom Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Frozen Yogurt

- 8.1.2. Ice Cream

- 8.1.2.1. Artisanal Ice Cream

- 8.1.2.2. Dairy-based Ice Cream

- 8.1.2.3. Water-based Ice Cream

- 8.1.3. Frozen Cakes

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets/Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Speciality Stores

- 8.2.4. Online Retailer

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. France Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Frozen Yogurt

- 9.1.2. Ice Cream

- 9.1.2.1. Artisanal Ice Cream

- 9.1.2.2. Dairy-based Ice Cream

- 9.1.2.3. Water-based Ice Cream

- 9.1.3. Frozen Cakes

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets/Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Speciality Stores

- 9.2.4. Online Retailer

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Italy Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Frozen Yogurt

- 10.1.2. Ice Cream

- 10.1.2.1. Artisanal Ice Cream

- 10.1.2.2. Dairy-based Ice Cream

- 10.1.2.3. Water-based Ice Cream

- 10.1.3. Frozen Cakes

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets/Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Speciality Stores

- 10.2.4. Online Retailer

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Frozen Yogurt

- 11.1.2. Ice Cream

- 11.1.2.1. Artisanal Ice Cream

- 11.1.2.2. Dairy-based Ice Cream

- 11.1.2.3. Water-based Ice Cream

- 11.1.3. Frozen Cakes

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets/Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Speciality Stores

- 11.2.4. Online Retailer

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Europe Europe Frozen Dessert Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Frozen Yogurt

- 12.1.2. Ice Cream

- 12.1.2.1. Artisanal Ice Cream

- 12.1.2.2. Dairy-based Ice Cream

- 12.1.2.3. Water-based Ice Cream

- 12.1.3. Frozen Cakes

- 12.1.4. Others

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Supermarkets/Hypermarkets

- 12.2.2. Convenience Stores

- 12.2.3. Speciality Stores

- 12.2.4. Online Retailer

- 12.2.5. Others

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Unilever

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Mondel?z International

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Nestle S A

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 General Mills Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Fonterra Co-operative Group*List Not Exhaustive

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Dunkin' Brands Group Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Chobani LLC

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Blue Bell Creameries LP

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.1 Unilever

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Europe Frozen Dessert Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Frozen Dessert Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Europe Frozen Dessert Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Europe Frozen Dessert Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Europe Frozen Dessert Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 11: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Europe Frozen Dessert Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Europe Frozen Dessert Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 17: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Europe Frozen Dessert Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Europe Frozen Dessert Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: Europe Frozen Dessert Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 21: Europe Frozen Dessert Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Frozen Dessert Industry?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Europe Frozen Dessert Industry?

Key companies in the market include Unilever, Mondel?z International, Nestle S A, General Mills Inc, Fonterra Co-operative Group*List Not Exhaustive, Dunkin' Brands Group Inc, Chobani LLC, Blue Bell Creameries LP.

3. What are the main segments of the Europe Frozen Dessert Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 128.56 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand for Low-fat and Non-Dairy Ice Cream Products; Growing Acceptance of Experimental Flavors.

6. What are the notable trends driving market growth?

Rising Health Concerns and Innovation in Flavours is Boosting the Market Growth.

7. Are there any restraints impacting market growth?

Rising Concern over Health Issues Associated with Ice Cream.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Frozen Dessert Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Frozen Dessert Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Frozen Dessert Industry?

To stay informed about further developments, trends, and reports in the Europe Frozen Dessert Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence