Key Insights

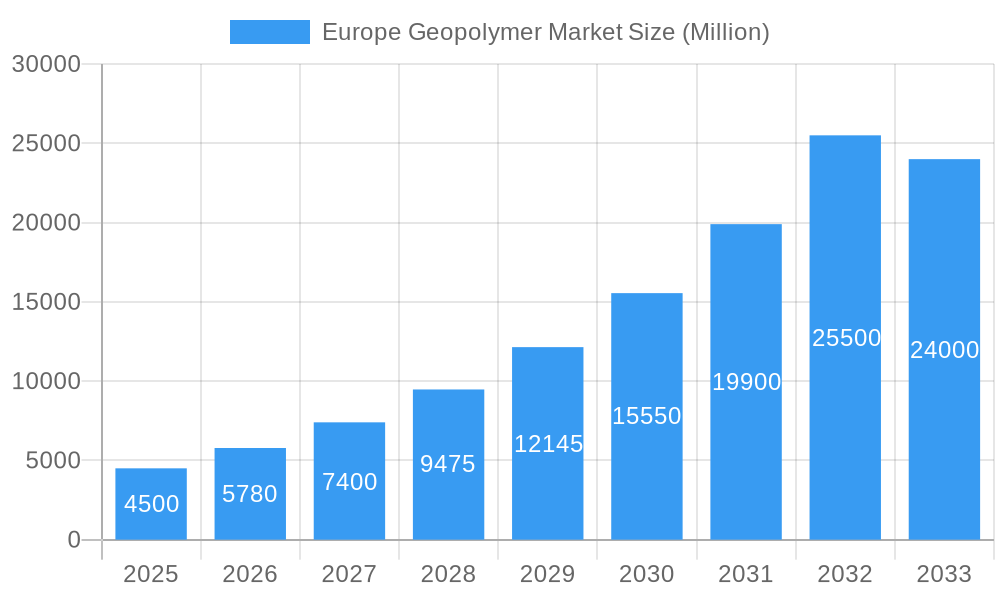

The Europe Geopolymer Market is set for substantial growth, with a market size of $1.8 billion in 2024. This sector is projected to achieve a robust Compound Annual Growth Rate (CAGR) of 16.5% from 2024 to 2033, reaching an estimated $9.0 billion by 2033. This expansion is driven by the increasing demand for sustainable construction materials, spurred by stringent environmental regulations and heightened awareness of traditional cement's carbon footprint. Geopolymers offer a significant reduction in CO2 emissions and energy consumption, making them an attractive alternative for building construction, road infrastructure, pipe and concrete repair, and bridge construction.

Europe Geopolymer Market Market Size (In Billion)

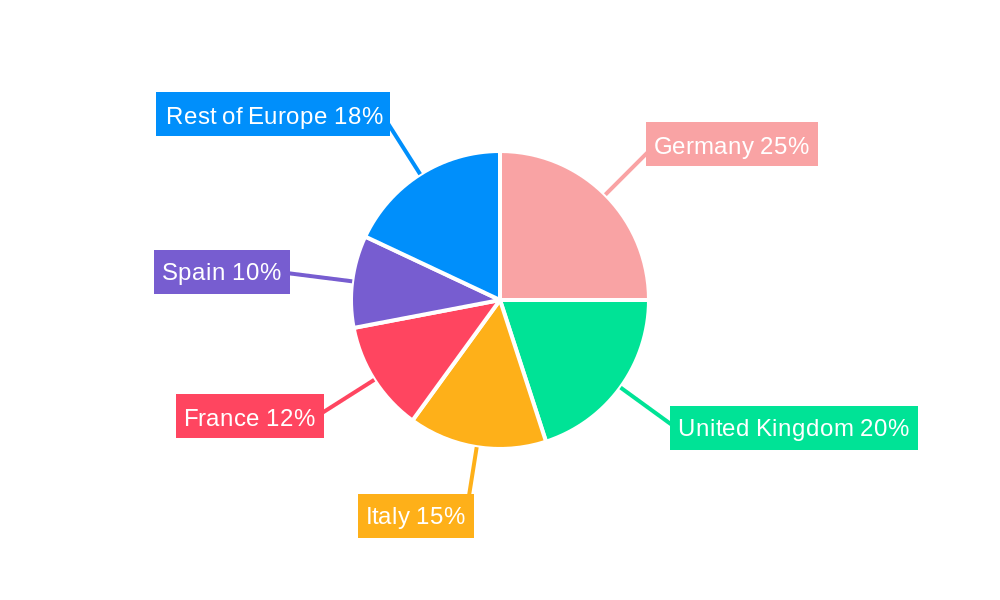

Europe's geopolymer market is further boosted by substantial infrastructure development investments and the growing adoption of advanced building materials. Challenges, including initial production facility setup costs and the need for greater standardization and industry acceptance, are being addressed through ongoing research and development and strategic collaborations. Key product segments include Cement, Concrete, and Precast Panels, with Building and Road & Pavement dominating application areas. Major markets include Germany, the United Kingdom, Italy, France, and Spain, alongside steady growth in the Rest of Europe.

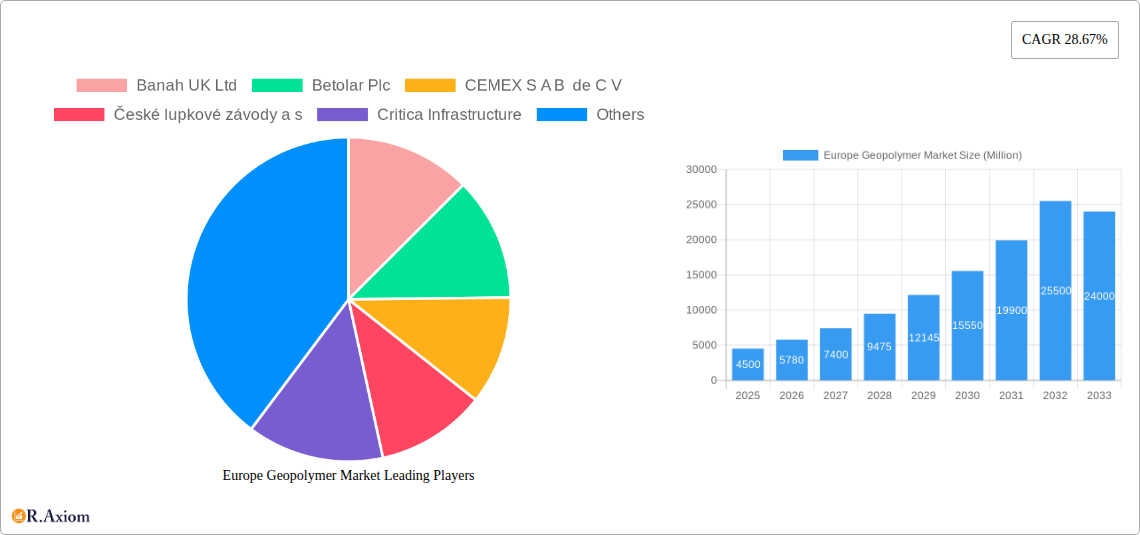

Europe Geopolymer Market Company Market Share

Europe Geopolymer Market Market Concentration & Innovation

The Europe Geopolymer Market exhibits a moderate to high market concentration, with a blend of established construction material giants and agile, specialized geopolymer innovators vying for market share. Innovation is a primary driver, fueled by the urgent need for sustainable building materials and stringent environmental regulations across Europe. Companies are actively investing in R&D to develop novel geopolymer formulations with enhanced properties, faster curing times, and broader application ranges. Regulatory frameworks, particularly those focusing on carbon emissions reduction and circular economy principles, are instrumental in shaping the market, favoring geopolymers over traditional Portland cement.

- Innovation Drivers:

- Growing demand for low-carbon construction materials.

- Advancements in activator chemistries and binder formulations.

- Development of geopolymer applications in specialized sectors like waste immobilization.

- Digitalization and 3D printing integration with geopolymer solutions.

- Product Substitutes: Traditional Portland cement, fly ash-based cements, slag cements, and other supplementary cementitious materials (SCMs).

- End-User Trends: Increasing adoption by construction companies seeking to meet sustainability targets, infrastructure developers prioritizing durability and longevity, and industries requiring specialized chemical resistance.

- M&A Activities: The market has seen strategic acquisitions and partnerships as larger players aim to integrate geopolymer technology into their portfolios and smaller, innovative firms seek expansion capital and broader market access. While specific deal values are often proprietary, the trend indicates a strong appetite for consolidation and growth. The market share is gradually shifting, with leading geopolymer developers gaining traction.

Europe Geopolymer Market Industry Trends & Insights

The Europe Geopolymer Market is poised for significant expansion, driven by a confluence of environmental imperatives, technological advancements, and evolving consumer preferences. The compounded annual growth rate (CAGR) is projected to be robust, reflecting the increasing adoption of geopolymer solutions as viable and often superior alternatives to conventional concrete and cement. The market penetration of geopolymers is steadily increasing, moving beyond niche applications to mainstream construction and infrastructure projects.

Technological disruptions are at the forefront of this growth. Researchers and manufacturers are continuously innovating, focusing on improving the performance characteristics of geopolymer binders and concretes, such as enhanced strength, durability, and resistance to aggressive environments. The development of novel activators and the utilization of diverse industrial byproducts as precursor materials are key areas of research. Furthermore, the integration of geopolymer technology with advanced construction techniques like 3D printing is opening up new avenues for rapid and sustainable construction, particularly for specialized or complex architectural designs.

Consumer preferences are increasingly leaning towards environmentally conscious building solutions. As awareness of the significant carbon footprint associated with Portland cement production grows, specifiers, developers, and end-users are actively seeking alternatives. Geopolymers, with their substantially lower embodied CO2 emissions, directly address this demand. The circular economy principles are also gaining traction, encouraging the use of waste materials in construction, a core tenet of geopolymer production.

Competitive dynamics within the Europe Geopolymer Market are characterized by a growing number of specialized companies and the increasing interest from established cement and construction material manufacturers. This competitive landscape fosters innovation and drives down costs, making geopolymer solutions more accessible. Strategic collaborations, joint ventures, and acquisitions are becoming more common as companies aim to leverage each other's expertise and market reach. The market is transitioning from a nascent stage to a more mature growth phase, driven by tangible benefits in sustainability, performance, and lifecycle cost.

Dominant Markets & Segments in Europe Geopolymer Market

The Europe Geopolymer Market's dominance is multifaceted, influenced by geographical advantages, robust industrial ecosystems, and specific application demands. Geographically, Western Europe, particularly countries with strong environmental policies and advanced construction sectors like Germany, the UK, France, and the Netherlands, represents a leading region. These nations are at the forefront of adopting sustainable building materials, driven by both regulatory incentives and corporate sustainability initiatives. The high density of construction projects, coupled with significant investment in infrastructure upgrades and maintenance, further bolsters demand.

Within this region, Germany often emerges as a dominant country, owing to its advanced manufacturing capabilities, strong emphasis on research and development, and its significant role in the European construction industry. The country's commitment to reducing carbon emissions aligns perfectly with the value proposition of geopolymers.

In terms of product types, Cement, Concrete, and Precast Panel stands out as the most dominant segment. This broad category encompasses a wide array of geopolymer-based products that directly substitute traditional concrete and cement in conventional construction. The widespread acceptance and established use of concrete in various applications make this segment the natural entry point and largest market for geopolymers.

- Key Drivers for Dominance in Cement, Concrete, and Precast Panel:

- Infrastructure Development: Continuous investment in roads, bridges, and buildings necessitates large volumes of concrete.

- Durability and Longevity: Geopolymer concrete offers superior resistance to chemical attack and freeze-thaw cycles, making it ideal for demanding environments.

- Sustainability Initiatives: Government mandates and corporate goals for reducing embodied carbon are accelerating the adoption of geopolymer concrete.

- Cost-Effectiveness (Lifecycle): While initial costs might vary, the extended lifespan and reduced maintenance requirements of geopolymer structures translate to significant lifecycle savings.

The Application segment that exhibits significant dominance is Building. This includes residential, commercial, and industrial constructions where geopolymer concrete can be used for foundations, walls, floors, and structural elements. The high volume of new construction and the renovation market within Europe create substantial demand. However, Road and Pavement applications are rapidly gaining traction due to the need for durable, sustainable, and low-maintenance infrastructure solutions. The ability of geopolymers to withstand heavy traffic loads and harsh weather conditions makes them an attractive option for road construction and repair.

- Dominance Analysis for Building Applications:

- Urbanization and Housing Demand: Growing urban populations necessitate continuous construction of residential and commercial spaces.

- Retrofitting and Renovation: The aging building stock in Europe requires sustainable materials for repair and upgrades.

- Architectural Flexibility: Geopolymer concrete can be cast into various shapes, offering design freedom for architects.

- Fire Resistance: Geopolymers inherently possess superior fire-resistant properties, a critical factor in building safety regulations.

While other segments like Runway, Bridge, Tunnel Lining, and Nuclear and Other Toxic Waste Immobilization are crucial and growing, their volume is comparatively smaller than the widespread use in general building and road construction. The dominance is thus driven by the sheer scale of these primary applications, supported by the increasing awareness and performance benefits of geopolymer technology.

Europe Geopolymer Market Product Developments

The Europe Geopolymer Market is witnessing rapid product innovation, primarily focused on enhancing performance and expanding application horizons. Key developments include the formulation of novel geopolymer cements and concretes with superior compressive strength and enhanced durability, making them competitive with, and often superior to, traditional Portland cement-based products. Innovations in activator chemistries are leading to faster curing times and broader compatibility with various industrial waste streams, thereby improving cost-effectiveness and sustainability. Furthermore, the development of specialized geopolymer mortars for additive manufacturing (3D printing) is a significant advancement, enabling the creation of complex structural components with reduced waste and increased construction speed. These developments aim to leverage the inherent advantages of geopolymers, such as low embodied energy, excellent chemical resistance, and fireproofing capabilities, to address a wider range of construction and industrial challenges.

Report Scope & Segmentation Analysis

The Europe Geopolymer Market report provides a comprehensive analysis of the industry, segmented across key product types and applications. The Product Type segmentation includes Cement, Concrete, and Precast Panel, which represents the largest market share due to its widespread use in traditional construction. Grout and Binder is a significant segment, offering specialized solutions for repairs and anchoring. The Other Pr category encompasses emerging geopolymer formulations and niche products.

The Application segmentation is extensive, covering major sectors such as Building, which is projected for substantial growth driven by sustainability mandates. Road and Pavement applications are also a key growth area, fueled by infrastructure development and the demand for durable materials. The report delves into specific applications like Runway, Pipe and Concrete Repair, Bridge, Tunnel Lining, Railroad Sleeper, Coating, Fireproofing, Nuclear and Other Toxic Waste Immobilization, and Specific Mold Products, detailing their market sizes, growth projections, and competitive dynamics. Each segment's unique demand drivers and adoption rates are analyzed to provide a holistic view of the market landscape.

Key Drivers of Europe Geopolymer Market Growth

The Europe Geopolymer Market's growth is propelled by a powerful combination of environmental, economic, and technological factors. The foremost driver is the intensifying global and European focus on sustainability and carbon footprint reduction. Geopolymer binders, by utilizing industrial byproducts and requiring significantly less energy to produce than Portland cement, offer a compelling solution for de-carbonizing the construction sector. Regulatory mandates and incentives promoting low-carbon building materials further accelerate this trend. Economically, the increasing demand for durable and long-lasting infrastructure, coupled with the rising costs of traditional materials and the potential for lifecycle cost savings with geopolymers, presents a strong economic incentive. Technologically, ongoing research and development are leading to improved geopolymer formulations with enhanced performance characteristics, wider applicability, and cost reductions, making them increasingly competitive and attractive to a broader market.

Challenges in the Europe Geopolymer Market Sector

Despite its promising growth, the Europe Geopolymer Market faces several challenges that can hinder its widespread adoption. A significant barrier is the lack of standardization and established codes of practice in many European countries, which creates hesitancy among architects, engineers, and contractors to specify and use geopolymer materials in large-scale projects. Public awareness and acceptance also remain a challenge; the familiarity and long-standing trust in Portland cement mean that geopolymer alternatives require significant educational efforts to gain traction. Supply chain logistics for the diverse alkali activators and precursor materials can also be complex and sometimes inconsistent, impacting availability and cost. Furthermore, the initial perceived higher cost of some geopolymer formulations compared to conventional cement, although offset by lifecycle benefits, can be a deterrent for budget-sensitive projects. Competition from established players in the traditional cement industry, who may have vested interests in maintaining the status quo, also presents a hurdle.

Emerging Opportunities in Europe Geopolymer Market

The Europe Geopolymer Market is ripe with emerging opportunities, primarily driven by innovation and the increasing demand for sustainable solutions. The growing trend of circular economy initiatives within Europe presents a significant opportunity for geopolymer manufacturers, as these materials effectively utilize industrial waste streams like fly ash and slag. The burgeoning field of 3D printing in construction is another major opportunity, with geopolymer binders showing great promise for creating complex and sustainable structures rapidly. The increasing focus on resilient infrastructure that can withstand extreme weather events and chemical attack opens doors for geopolymer concrete's superior durability. Furthermore, the development of geopolymer applications in specialized areas such as nuclear and toxic waste immobilization offers high-value niche markets. The European Green Deal and its emphasis on sustainable construction provide a favorable regulatory environment, creating substantial opportunities for market expansion.

Leading Players in the Europe Geopolymer Market Market

- Banah UK Ltd

- Betolar Plc

- CEMEX S A B de C V

- České lupkové závody a s

- Critica Infrastructure

- Gement Ltd

- MITSUI & CO LTD

- PCI Augsburg GmbH

- Pyromeral Systems

- RENCA

- SLB (Schlumberger Limited)

- W R Meadows Inc

Key Developments in Europe Geopolymer Market Industry

- July 2023: RENCA launched a cement-free geopolymer mortar for 3D printing of houses, enhancing the company's product portfolio and strengthening its position in the market.

- March 2023: SLB introduced the EcoShield geopolymer cement-free system that minimizes the CO2 footprint of a well's construction. This innovative technology eliminates up to 85% of embodied CO2 emissions compared with traditional well-cementing systems, which include Portland cement.

Strategic Outlook for Europe Geopolymer Market Market

The strategic outlook for the Europe Geopolymer Market is overwhelmingly positive, driven by a sustained push towards decarbonization and sustainable development across the continent. The increasing regulatory pressure to reduce embodied carbon in construction materials is a primary growth catalyst, directly favoring geopolymer solutions. Significant investment in green infrastructure projects, coupled with the inherent durability and longevity of geopolymer-based products, positions them as ideal alternatives to traditional cement. The ongoing advancements in geopolymer technology, including faster curing times, improved performance characteristics, and cost optimization through the utilization of diverse waste streams, are further enhancing their market competitiveness. Emerging opportunities in sectors like 3D printed construction and specialized waste immobilization present substantial avenues for future growth. Strategic partnerships, increased R&D, and the development of standardized specifications will be crucial for unlocking the full market potential and accelerating the transition towards a more sustainable built environment in Europe.

Europe Geopolymer Market Segmentation

-

1. Product Type

- 1.1. Cement, Concrete, and Precast Panel

- 1.2. Grout and Binder

- 1.3. Other Pr

-

2. Application

- 2.1. Building

- 2.2. Road and Pavement

- 2.3. Runway

- 2.4. Pipe and Concrete Repair

- 2.5. Bridge

- 2.6. Tunnel Lining

- 2.7. Railroad Sleeper

- 2.8. Coating

- 2.9. Fireproofing

- 2.10. Nuclear and Other Toxic Waste Immobilization

- 2.11. Specific Mold Products

Europe Geopolymer Market Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. France

- 5. Spain

- 6. Rest of Europe

Europe Geopolymer Market Regional Market Share

Geographic Coverage of Europe Geopolymer Market

Europe Geopolymer Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Cement, Concrete, and Precast Panel

- 5.1.2. Grout and Binder

- 5.1.3. Other Pr

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Building

- 5.2.2. Road and Pavement

- 5.2.3. Runway

- 5.2.4. Pipe and Concrete Repair

- 5.2.5. Bridge

- 5.2.6. Tunnel Lining

- 5.2.7. Railroad Sleeper

- 5.2.8. Coating

- 5.2.9. Fireproofing

- 5.2.10. Nuclear and Other Toxic Waste Immobilization

- 5.2.11. Specific Mold Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. Italy

- 5.3.4. France

- 5.3.5. Spain

- 5.3.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Europe Geopolymer Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Cement, Concrete, and Precast Panel

- 6.1.2. Grout and Binder

- 6.1.3. Other Pr

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Building

- 6.2.2. Road and Pavement

- 6.2.3. Runway

- 6.2.4. Pipe and Concrete Repair

- 6.2.5. Bridge

- 6.2.6. Tunnel Lining

- 6.2.7. Railroad Sleeper

- 6.2.8. Coating

- 6.2.9. Fireproofing

- 6.2.10. Nuclear and Other Toxic Waste Immobilization

- 6.2.11. Specific Mold Products

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Germany Europe Geopolymer Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Cement, Concrete, and Precast Panel

- 7.1.2. Grout and Binder

- 7.1.3. Other Pr

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Building

- 7.2.2. Road and Pavement

- 7.2.3. Runway

- 7.2.4. Pipe and Concrete Repair

- 7.2.5. Bridge

- 7.2.6. Tunnel Lining

- 7.2.7. Railroad Sleeper

- 7.2.8. Coating

- 7.2.9. Fireproofing

- 7.2.10. Nuclear and Other Toxic Waste Immobilization

- 7.2.11. Specific Mold Products

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. United Kingdom Europe Geopolymer Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Cement, Concrete, and Precast Panel

- 8.1.2. Grout and Binder

- 8.1.3. Other Pr

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Building

- 8.2.2. Road and Pavement

- 8.2.3. Runway

- 8.2.4. Pipe and Concrete Repair

- 8.2.5. Bridge

- 8.2.6. Tunnel Lining

- 8.2.7. Railroad Sleeper

- 8.2.8. Coating

- 8.2.9. Fireproofing

- 8.2.10. Nuclear and Other Toxic Waste Immobilization

- 8.2.11. Specific Mold Products

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Italy Europe Geopolymer Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Cement, Concrete, and Precast Panel

- 9.1.2. Grout and Binder

- 9.1.3. Other Pr

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Building

- 9.2.2. Road and Pavement

- 9.2.3. Runway

- 9.2.4. Pipe and Concrete Repair

- 9.2.5. Bridge

- 9.2.6. Tunnel Lining

- 9.2.7. Railroad Sleeper

- 9.2.8. Coating

- 9.2.9. Fireproofing

- 9.2.10. Nuclear and Other Toxic Waste Immobilization

- 9.2.11. Specific Mold Products

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. France Europe Geopolymer Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Cement, Concrete, and Precast Panel

- 10.1.2. Grout and Binder

- 10.1.3. Other Pr

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Building

- 10.2.2. Road and Pavement

- 10.2.3. Runway

- 10.2.4. Pipe and Concrete Repair

- 10.2.5. Bridge

- 10.2.6. Tunnel Lining

- 10.2.7. Railroad Sleeper

- 10.2.8. Coating

- 10.2.9. Fireproofing

- 10.2.10. Nuclear and Other Toxic Waste Immobilization

- 10.2.11. Specific Mold Products

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain Europe Geopolymer Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Cement, Concrete, and Precast Panel

- 11.1.2. Grout and Binder

- 11.1.3. Other Pr

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Building

- 11.2.2. Road and Pavement

- 11.2.3. Runway

- 11.2.4. Pipe and Concrete Repair

- 11.2.5. Bridge

- 11.2.6. Tunnel Lining

- 11.2.7. Railroad Sleeper

- 11.2.8. Coating

- 11.2.9. Fireproofing

- 11.2.10. Nuclear and Other Toxic Waste Immobilization

- 11.2.11. Specific Mold Products

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Europe Europe Geopolymer Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Cement, Concrete, and Precast Panel

- 12.1.2. Grout and Binder

- 12.1.3. Other Pr

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Building

- 12.2.2. Road and Pavement

- 12.2.3. Runway

- 12.2.4. Pipe and Concrete Repair

- 12.2.5. Bridge

- 12.2.6. Tunnel Lining

- 12.2.7. Railroad Sleeper

- 12.2.8. Coating

- 12.2.9. Fireproofing

- 12.2.10. Nuclear and Other Toxic Waste Immobilization

- 12.2.11. Specific Mold Products

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Banah UK Ltd

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Betolar Plc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 CEMEX S A B de C V

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 České lupkové závody a s

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Critica Infrastructure

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Gement Ltd

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 MITSUI & CO LTD

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 PCI Augsburg GmbH

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Pyromeral Systems

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 RENCA

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 SLB (Schlumberger Limited)

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 W R Meadows Inc *List Not Exhaustive

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.1 Banah UK Ltd

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Europe Geopolymer Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Germany Europe Geopolymer Market Revenue (billion), by Product Type 2025 & 2033

- Figure 3: Germany Europe Geopolymer Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: Germany Europe Geopolymer Market Revenue (billion), by Application 2025 & 2033

- Figure 5: Germany Europe Geopolymer Market Revenue Share (%), by Application 2025 & 2033

- Figure 6: Germany Europe Geopolymer Market Revenue (billion), by Country 2025 & 2033

- Figure 7: Germany Europe Geopolymer Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: United Kingdom Europe Geopolymer Market Revenue (billion), by Product Type 2025 & 2033

- Figure 9: United Kingdom Europe Geopolymer Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 10: United Kingdom Europe Geopolymer Market Revenue (billion), by Application 2025 & 2033

- Figure 11: United Kingdom Europe Geopolymer Market Revenue Share (%), by Application 2025 & 2033

- Figure 12: United Kingdom Europe Geopolymer Market Revenue (billion), by Country 2025 & 2033

- Figure 13: United Kingdom Europe Geopolymer Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Italy Europe Geopolymer Market Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Italy Europe Geopolymer Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Italy Europe Geopolymer Market Revenue (billion), by Application 2025 & 2033

- Figure 17: Italy Europe Geopolymer Market Revenue Share (%), by Application 2025 & 2033

- Figure 18: Italy Europe Geopolymer Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Italy Europe Geopolymer Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: France Europe Geopolymer Market Revenue (billion), by Product Type 2025 & 2033

- Figure 21: France Europe Geopolymer Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: France Europe Geopolymer Market Revenue (billion), by Application 2025 & 2033

- Figure 23: France Europe Geopolymer Market Revenue Share (%), by Application 2025 & 2033

- Figure 24: France Europe Geopolymer Market Revenue (billion), by Country 2025 & 2033

- Figure 25: France Europe Geopolymer Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Spain Europe Geopolymer Market Revenue (billion), by Product Type 2025 & 2033

- Figure 27: Spain Europe Geopolymer Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Spain Europe Geopolymer Market Revenue (billion), by Application 2025 & 2033

- Figure 29: Spain Europe Geopolymer Market Revenue Share (%), by Application 2025 & 2033

- Figure 30: Spain Europe Geopolymer Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Spain Europe Geopolymer Market Revenue Share (%), by Country 2025 & 2033

- Figure 32: Rest of Europe Europe Geopolymer Market Revenue (billion), by Product Type 2025 & 2033

- Figure 33: Rest of Europe Europe Geopolymer Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 34: Rest of Europe Europe Geopolymer Market Revenue (billion), by Application 2025 & 2033

- Figure 35: Rest of Europe Europe Geopolymer Market Revenue Share (%), by Application 2025 & 2033

- Figure 36: Rest of Europe Europe Geopolymer Market Revenue (billion), by Country 2025 & 2033

- Figure 37: Rest of Europe Europe Geopolymer Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Europe Geopolymer Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Europe Geopolymer Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Global Europe Geopolymer Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 11: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global Europe Geopolymer Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Europe Geopolymer Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 17: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global Europe Geopolymer Market Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Global Europe Geopolymer Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: Global Europe Geopolymer Market Revenue billion Forecast, by Application 2020 & 2033

- Table 21: Global Europe Geopolymer Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Geopolymer Market?

The projected CAGR is approximately 16.5%.

2. Which companies are prominent players in the Europe Geopolymer Market?

Key companies in the market include Banah UK Ltd, Betolar Plc, CEMEX S A B de C V, České lupkové závody a s, Critica Infrastructure, Gement Ltd, MITSUI & CO LTD, PCI Augsburg GmbH, Pyromeral Systems, RENCA, SLB (Schlumberger Limited), W R Meadows Inc *List Not Exhaustive.

3. What are the main segments of the Europe Geopolymer Market?

The market segments include Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Green Concrete and Construction Materials; Environmental Regulations and Sustainability Initiatives; Other Drivers.

6. What are the notable trends driving market growth?

Building Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Growing Demand for Green Concrete and Construction Materials; Environmental Regulations and Sustainability Initiatives; Other Drivers.

8. Can you provide examples of recent developments in the market?

July 2023: RENCA launched a cement-free geopolymer mortar for 3D printing of houses. It enhanced the company's product portfolio and strengthened its position in the market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Geopolymer Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Geopolymer Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Geopolymer Market?

To stay informed about further developments, trends, and reports in the Europe Geopolymer Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence