Key Insights

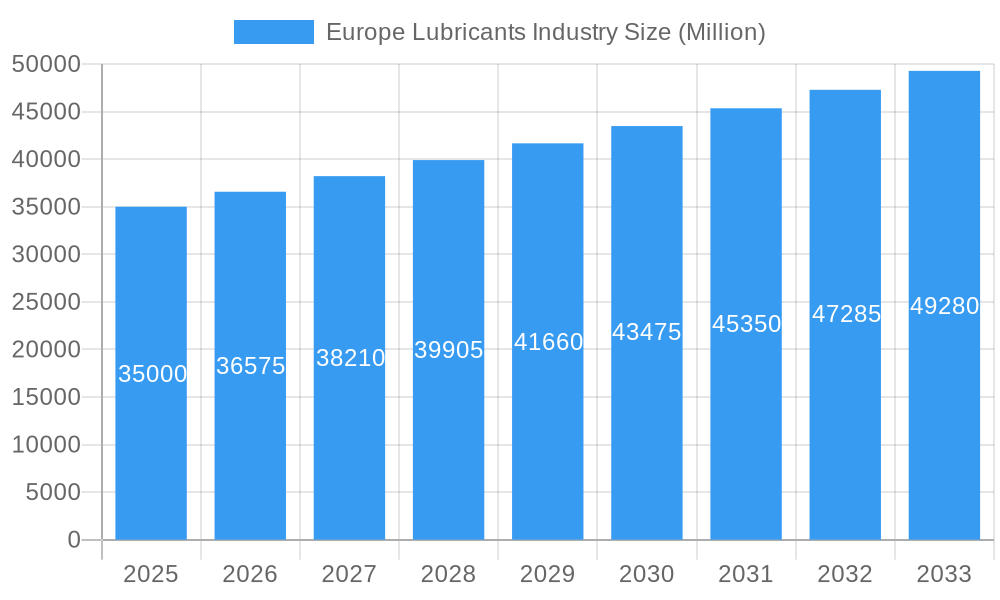

The European lubricants market is projected for significant expansion, expected to reach $6.41 billion by 2025, with a compound annual growth rate (CAGR) of 1.81% from 2025 to 2033. This growth is primarily driven by the automotive sector's recovery and an aging vehicle fleet requiring regular maintenance. The heavy equipment industry, particularly in construction and infrastructure development in Germany and the UK, also significantly contributes. The metallurgy and metalworking sector consistently demands specialized lubricants to enhance operational efficiency and extend machinery life. Key emerging trends include the development and adoption of high-performance, eco-friendly lubricants, and those with extended drain intervals, influenced by sustainability initiatives and stringent environmental regulations pushing for bio-based and synthetic alternatives.

Europe Lubricants Industry Market Size (In Billion)

Despite positive growth prospects, the increasing adoption of electric vehicles (EVs) poses a long-term challenge due to their reduced lubricant requirements. However, the gradual transition and the existing internal combustion engine vehicle fleet will sustain demand for traditional lubricants. Fluctuating raw material prices, especially for base oils and additives, can impact manufacturer profit margins. The market features intense competition among global players like ExxonMobil, Shell, and BP (Castrol), alongside regional specialists. Strategic collaborations, mergers, and acquisitions are anticipated to consolidate market positions, broaden product offerings, and expand geographical reach. The forecast period also highlights the growing importance of industrial lubricants for the power generation sector, particularly with investments in renewable energy infrastructure.

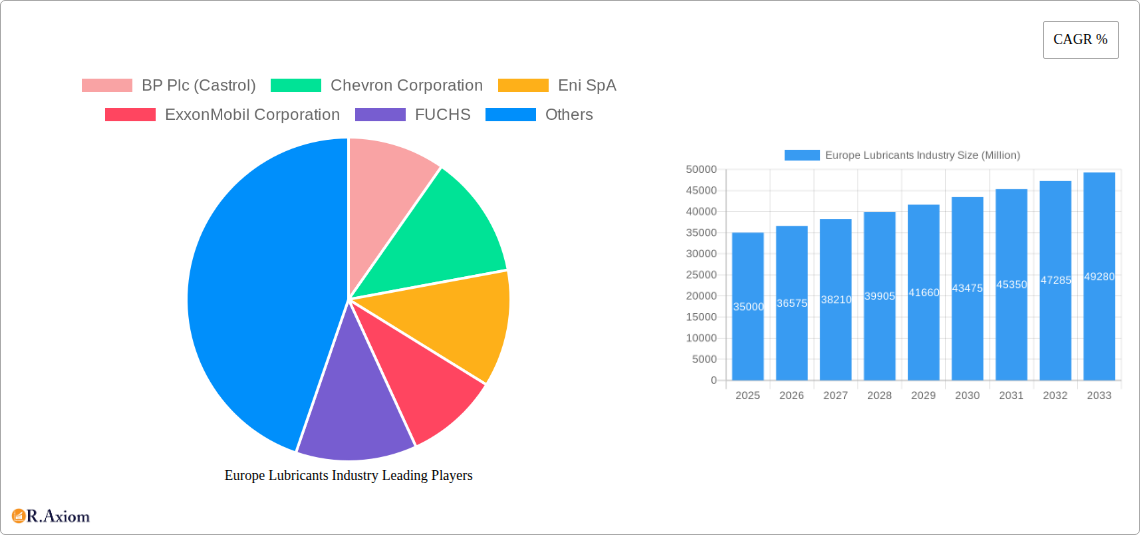

Europe Lubricants Industry Company Market Share

This report provides a comprehensive analysis of the Europe Lubricants Market, detailing market dynamics, growth drivers, challenges, and opportunities. Covering the historical period 2019-2024 and projecting through 2033, with 2025 as the base year, this research is essential for stakeholders navigating this evolving market.

Europe Lubricants Industry Market Concentration & Innovation

The Europe Lubricants Industry exhibits a moderately concentrated market structure, with a few major global players holding significant market share. Companies like Royal Dutch Shell Plc, ExxonMobil Corporation, Chevron Corporation, BP Plc (Castrol), and TotalEnergie dominate, commanding substantial portions of the overall market. However, specialized regional players and emerging manufacturers are carving out niches, particularly in high-performance and niche application lubricants. Innovation is a key differentiator, driven by stringent environmental regulations and evolving end-user demands for improved fuel efficiency, extended equipment life, and reduced emissions. Research and development efforts are heavily focused on synthetic and bio-based lubricants, as well as advanced additive technologies that enhance performance under extreme conditions. Regulatory frameworks, such as REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), play a crucial role in shaping product development and market access, pushing manufacturers towards more sustainable and compliant formulations. The threat of product substitutes, while present in certain low-performance applications, is diminishing as the demand for specialized, high-performance lubricants grows. End-user trends continue to pivot towards electrification in the automotive sector, which, while reducing traditional engine oil demand, is creating new opportunities in specialized fluids for electric vehicles. Mergers and acquisitions (M&A) are a consistent feature of the industry, enabling companies to consolidate market positions, acquire new technologies, and expand their geographical reach. Recent M&A deal values, while not specified here, are estimated to be in the hundreds of millions to billions of Euros, reflecting strategic consolidations within the sector. The market share of leading companies is estimated to be between 10% and 20% each for the top 3-5 players.

Europe Lubricants Industry Industry Trends & Insights

The Europe Lubricants Industry is poised for steady growth, driven by a confluence of technological advancements, evolving consumer preferences, and supportive economic policies. The Compound Annual Growth Rate (CAGR) for the forecast period is estimated to be between 3% and 5%. A significant trend is the increasing demand for high-performance and synthetic lubricants across all end-user segments. These advanced formulations offer superior protection, extended drain intervals, and improved energy efficiency, directly addressing the growing need for cost savings and reduced environmental impact. The automotive sector, despite the gradual shift towards electric vehicles, will remain a dominant end-user, with a sustained demand for engine oils, transmission fluids, and greases for internal combustion engine vehicles during the transition period. Furthermore, the burgeoning electric vehicle market itself is creating new product categories, such as specialized coolants and lubricants for EV powertrains and batteries. In the industrial sector, the focus is on lubricants that can withstand extreme operating conditions, reduce wear and tear on heavy equipment, and enhance operational efficiency in metallurgy & metalworking, power generation, and other manufacturing processes. Technological disruptions, such as the development of advanced additive chemistries, nanotechnology-based lubricants, and bio-lubricants derived from renewable sources, are transforming the product landscape. Consumer preferences are increasingly aligned with sustainability and performance. End-users are actively seeking lubricants that are not only effective but also environmentally friendly and contribute to a lower carbon footprint. This is driving innovation in biodegradable and low-toxicity lubricant formulations. The competitive dynamics within the Europe Lubricants Industry are characterized by intense competition among established global players, regional manufacturers, and specialized niche providers. Companies are differentiating themselves through product innovation, strategic partnerships, and customer-centric service offerings. Market penetration for advanced lubricants is steadily increasing as end-users recognize the long-term economic and environmental benefits. The increasing adoption of stricter emission standards across Europe is further fueling the demand for high-quality, compliant lubricants. The overall market size is projected to reach approximately €35 Billion by 2033.

Dominant Markets & Segments in Europe Lubricants Industry

The Automotive segment continues to be a dominant force within the Europe Lubricants Industry, driven by a vast and diverse vehicle parc across the continent. Despite the gradual transition to electric vehicles, internal combustion engine vehicles still constitute a significant portion of the market, necessitating continuous demand for engine oils, transmission fluids, and other specialized automotive lubricants. Key drivers for this segment's dominance include:

- Extensive Vehicle Fleet: Millions of passenger cars, commercial vehicles, and motorcycles operate across Europe.

- Strict Emission Standards: European regulations mandate advanced lubricant formulations that improve fuel efficiency and reduce emissions, thereby supporting the demand for high-quality engine oils.

- Aftermarket Demand: The aftermarket for vehicle maintenance and repair ensures a consistent need for lubricants.

Among product types, Engine Oils hold a substantial market share due to their pervasive use in both automotive and industrial applications.

- Automotive Engine Oils: Catering to a wide range of engines, from small passenger cars to heavy-duty trucks.

- Industrial Engine Oils: Essential for power generation, construction equipment, and agricultural machinery.

The Metallurgy & Metalworking segment is another crucial contributor to the Europe Lubricants Industry. The robust industrial base in countries like Germany, France, and Italy fuels a strong demand for specialized lubricants that enhance machinery performance and product quality in manufacturing processes.

- High-Performance Requirements: Lubricants are critical for reducing friction and wear in stamping, cutting, and forming operations.

- Process Efficiency: Specialized metalworking fluids contribute to improved surface finishes and extended tool life.

Hydraulic Fluids represent a significant product category, vital for the operation of a wide array of industrial machinery and mobile equipment across sectors such as construction, agriculture, and manufacturing.

- Operational Reliability: Essential for power transmission in hydraulic systems, ensuring smooth and efficient operation.

- Environmental Considerations: Increasing demand for biodegradable and fire-resistant hydraulic fluids.

The Heavy Equipment sector, encompassing construction, mining, and agricultural machinery, also represents a substantial market for lubricants. The ongoing infrastructure development and modernization projects across Europe continue to drive the demand for robust and high-performance lubricants that can withstand demanding operating conditions.

- Durability and Longevity: Lubricants are crucial for extending the lifespan of expensive heavy machinery.

- Operational Uptime: Reliable lubrication minimizes downtime and maintenance costs.

Transmission & Gear Oils are indispensable for the efficient functioning of mechanical power transmission systems in vehicles and industrial machinery, further solidifying their market importance.

Europe Lubricants Industry Product Developments

Product development in the Europe Lubricants Industry is increasingly focused on sustainability and enhanced performance. This includes the innovation of advanced synthetic lubricants that offer superior thermal stability, oxidation resistance, and wear protection, leading to extended equipment life and reduced maintenance. The rise of electric vehicles is spurring the development of specialized dielectric coolants and greases designed for EV powertrains and battery systems, addressing unique thermal management and electrical insulation needs. Furthermore, the industry is witnessing a growing trend towards bio-based and biodegradable lubricants derived from renewable resources, catering to environmentally conscious consumers and stringent regulatory mandates. These innovations aim to reduce environmental impact without compromising on lubrication efficacy, offering competitive advantages in a market that values both performance and ecological responsibility.

Report Scope & Segmentation Analysis

This report segments the Europe Lubricants Industry by End User and Product Type. The End User segments include Automotive, Heavy Equipment, Metallurgy & Metalworking, Power Generation, and Other End-user Industries. The Product Type segments encompass Engine Oils, Greases, Hydraulic Fluids, Metalworking Fluids, Transmission & Gear Oils, and Other Product Types. Each segment is analyzed for its market size, growth projections, and competitive dynamics. For instance, the Automotive segment, projected to grow at a CAGR of approximately 2% to 4%, is expected to maintain its dominance, while the "Other End-user Industries" category, including marine and aerospace, may exhibit higher growth rates due to specialized demands. Engine Oils are projected to maintain the largest market share within product types, estimated at over 30% of the total market value.

Key Drivers of Europe Lubricants Industry Growth

Several key factors are propelling the growth of the Europe Lubricants Industry. The increasing industrialization and manufacturing output across the continent necessitate a continuous supply of high-performance lubricants for machinery and equipment. Stringent environmental regulations, such as Euro 7 emission standards, are driving the demand for advanced, low-emission lubricants that enhance fuel efficiency and reduce operational impact. Technological advancements in lubricant formulations, including the development of synthetic and bio-based alternatives, are meeting evolving end-user preferences for sustainability and performance. Furthermore, the ongoing modernization of infrastructure and the robust automotive aftermarket segment are providing consistent demand. The growth of niche sectors like renewable energy, with its specific lubrication requirements for wind turbines and solar power systems, also contributes significantly.

Challenges in the Europe Lubricants Industry Sector

The Europe Lubricants Industry faces several significant challenges. The transition towards electric vehicles poses a long-term threat to the demand for traditional engine oils, requiring manufacturers to adapt their product portfolios. Fluctuating raw material prices, particularly for base oils derived from crude oil, can impact profit margins and market pricing. Increasingly stringent environmental regulations, while driving innovation, also impose higher compliance costs on manufacturers. Supply chain disruptions, as experienced in recent years, can affect the availability and cost of raw materials and finished products. Intense competition from both global players and localized manufacturers can lead to price wars and squeeze profit margins, especially in less specialized market segments.

Emerging Opportunities in Europe Lubricants Industry

The Europe Lubricants Industry is ripe with emerging opportunities. The burgeoning electric vehicle market presents a significant opportunity for the development and supply of specialized lubricants, coolants, and greases for EV powertrains, batteries, and charging infrastructure. The growing emphasis on sustainability is fueling demand for bio-based and biodegradable lubricants, creating a market for eco-friendly alternatives. Advancements in additive technology are enabling the creation of high-performance lubricants that offer extended drain intervals and improved fuel efficiency, appealing to cost-conscious consumers. Furthermore, the industrial automation and digitalization trends are driving the need for smart lubricants with enhanced monitoring capabilities and predictive maintenance features. Emerging markets within Europe and expanding applications in sectors like renewable energy (wind turbines, solar farms) also offer significant growth potential.

Leading Players in the Europe Lubricants Industry Market

- BP Plc (Castrol)

- Chevron Corporation

- Eni SpA

- ExxonMobil Corporation

- FUCHS

- Gazprom

- Lukoil

- Rosneft

- Royal Dutch Shell Plc

- TotalEnergie

Key Developments in Europe Lubricants Industry Industry

- May 2022: TotalEnergies, NEXUS Automotive Extend Strategic Partnership for a period of five years. As part of this partnership, TotalEnergies Lubricants will be expanding its presence in the burgeoning N! community, which has seen rapid growth in sales from EUR 7.2 billion in 2015 to nearly EUR 35 billion by the end of 2021.

- March 2022: ExxonMobil Corporation company has appointed Jay Hooley as lead managing director of the company.

- January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.

Strategic Outlook for Europe Lubricants Industry Market

The strategic outlook for the Europe Lubricants Industry is characterized by innovation, sustainability, and adaptation to evolving market demands. Companies are prioritizing the development of advanced synthetic and bio-based lubricants to meet stringent environmental regulations and consumer preferences for greener products. The transition to electric vehicles will necessitate a strategic pivot towards specialized fluids for EV components, opening new avenues for growth. Continued investment in research and development will be crucial for maintaining a competitive edge, particularly in areas like additive technology and high-performance formulations for demanding industrial applications. Strategic partnerships and potential M&A activities will likely continue as companies seek to consolidate market share, acquire new technologies, and expand their geographical reach. The focus on operational efficiency and cost optimization will remain paramount for navigating raw material price volatility and competitive pressures.

Europe Lubricants Industry Segmentation

-

1. End User

- 1.1. Automotive

- 1.2. Heavy Equipment

- 1.3. Metallurgy & Metalworking

- 1.4. Power Generation

- 1.5. Other End-user Industries

-

2. Product Type

- 2.1. Engine Oils

- 2.2. Greases

- 2.3. Hydraulic Fluids

- 2.4. Metalworking Fluids

- 2.5. Transmission & Gear Oils

- 2.6. Other Product Types

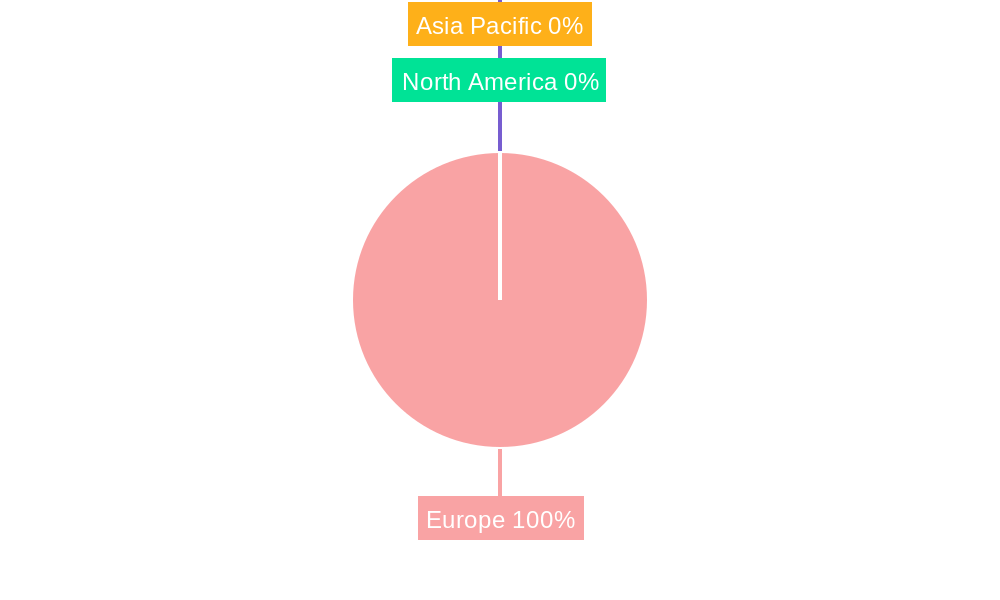

Europe Lubricants Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Lubricants Industry Regional Market Share

Geographic Coverage of Europe Lubricants Industry

Europe Lubricants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.81% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Automotive

- 5.1.2. Heavy Equipment

- 5.1.3. Metallurgy & Metalworking

- 5.1.4. Power Generation

- 5.1.5. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Engine Oils

- 5.2.2. Greases

- 5.2.3. Hydraulic Fluids

- 5.2.4. Metalworking Fluids

- 5.2.5. Transmission & Gear Oils

- 5.2.6. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. Europe Lubricants Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User

- 6.1.1. Automotive

- 6.1.2. Heavy Equipment

- 6.1.3. Metallurgy & Metalworking

- 6.1.4. Power Generation

- 6.1.5. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Engine Oils

- 6.2.2. Greases

- 6.2.3. Hydraulic Fluids

- 6.2.4. Metalworking Fluids

- 6.2.5. Transmission & Gear Oils

- 6.2.6. Other Product Types

- 6.1. Market Analysis, Insights and Forecast - by End User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BP Plc (Castrol)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Chevron Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Eni SpA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ExxonMobil Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FUCHS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Gazprom

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Lukoil

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Rosneft

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Royal Dutch Shell Plc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 TotalEnergie

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 BP Plc (Castrol)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Lubricants Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Lubricants Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Lubricants Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 2: Europe Lubricants Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Europe Lubricants Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Lubricants Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Europe Lubricants Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: Europe Lubricants Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Lubricants Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Lubricants Industry?

The projected CAGR is approximately 1.81%.

2. Which companies are prominent players in the Europe Lubricants Industry?

Key companies in the market include BP Plc (Castrol), Chevron Corporation, Eni SpA, ExxonMobil Corporation, FUCHS, Gazprom, Lukoil, Rosneft, Royal Dutch Shell Plc, TotalEnergie.

3. What are the main segments of the Europe Lubricants Industry?

The market segments include End User, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.41 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Largest Segment By End User : Automotive.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

May 2022: TotalEnergies, NEXUS Automotive Extend Strategic Partnership for a period of five years. As part of this partnership, TotalEnergies Lubricants will be expanding its presence in the burgeoning N! community, which has seen rapid growth in sales from EUR 7.2 billion in 2015 to nearly EUR 35 billion by the end of 2021.March 2022: ExxonMobil Corporation company has appointed Jay Hooley as lead managing director of the company.January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Lubricants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Lubricants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Lubricants Industry?

To stay informed about further developments, trends, and reports in the Europe Lubricants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence