Key Insights

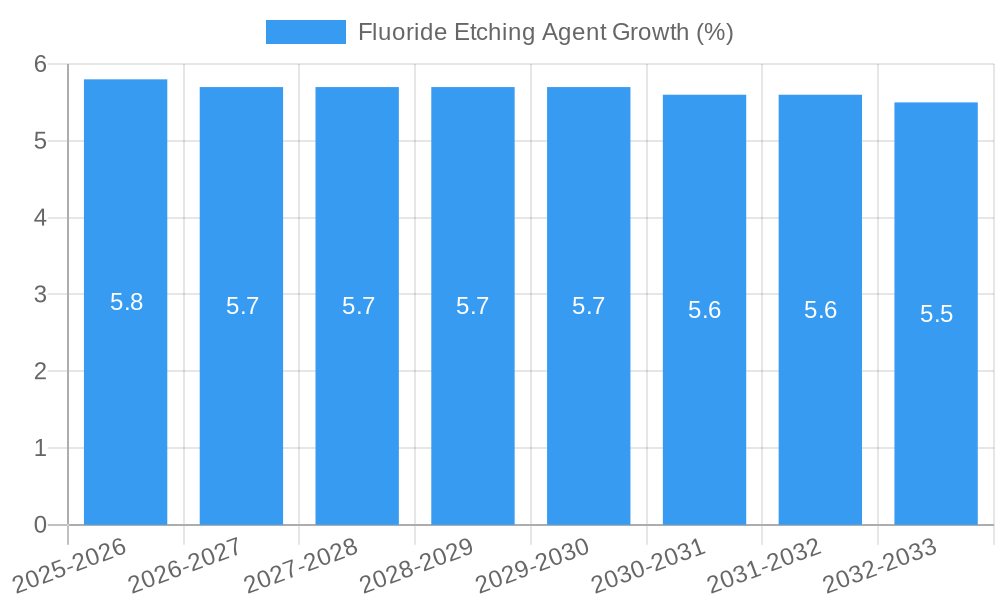

The global market for Fluoride Etching Agents is poised for robust expansion, driven by the ever-increasing demand for advanced semiconductor manufacturing, the burgeoning display industry, and the rapid growth of solar energy installations. Valued at approximately USD 997 million in 2025, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033, reaching an estimated value of over USD 1.5 billion by the end of the forecast period. This sustained growth is underpinned by the critical role of fluoride etching agents in precision microfabrication processes, enabling the creation of smaller, more powerful, and energy-efficient electronic components. The semiconductor sector, in particular, will continue to be the primary consumer, fueled by the proliferation of IoT devices, 5G infrastructure, artificial intelligence, and high-performance computing. Furthermore, the expanding production of high-resolution LCD and OLED displays, coupled with the global push towards renewable energy sources, will significantly contribute to the market's upward trajectory. Innovations in etching technologies, aimed at achieving finer feature sizes and improved process yields, will also act as significant catalysts for market growth.

Despite the strong growth prospects, the market faces certain challenges that could temper its expansion. Volatility in raw material prices, particularly for fluorine-containing precursors, can impact production costs and profitability for manufacturers. Stringent environmental regulations concerning the handling and disposal of certain fluoride compounds, though essential for sustainability, may also necessitate additional investment in compliance and waste management, potentially adding to operational expenses. Moreover, the development of alternative etching technologies or materials, though nascent, could pose a long-term threat. Nevertheless, the inherent advantages of fluoride etching agents in terms of performance and cost-effectiveness for many critical applications are expected to ensure their continued dominance. Key market segments, including C5F8, C4F6, and CF4, are anticipated to witness substantial demand, with ongoing research focused on developing new formulations with enhanced performance and reduced environmental impact. The competitive landscape features prominent global players like Nippon Sanso Holdings Corporation, Linde, and Air Liquide, actively investing in research and development and strategic expansions to capture market share.

This comprehensive report delves into the global Fluoride Etching Agent market, offering an in-depth analysis of its current landscape, future trajectory, and competitive dynamics. Spanning from 2019 to 2033, with a base year of 2025 and an extensive forecast period from 2025 to 2033, this study provides actionable insights for stakeholders seeking to navigate this critical sector of the electronics and semiconductor industry. The historical period covered is 2019–2024.

Fluoride Etching Agent Market Concentration & Innovation

The global Fluoride Etching Agent market exhibits a moderate to high level of concentration, with a significant portion of market share held by a few key players. Major contributors include Nippon Sanso Holdings Corporation, Kanto Denka Kogyo Co., Ltd., Linde, SK Specialty, Foosung, Air Liquide, Merck, Resonac, DAIKIN, Zeon Corporation, Air Products, Chengdu KMT Gas, Haohua Chemical Science and Technology, TEMC, Grandit Co., Ltd, Solvay, Ling Gas, Peric Special Gases, Ingentec Corporation, Yuji Tech, Jing He Science, Jinhong Gas Co., Ltd, Fujian Deer Technology. Innovation is a primary driver, fueled by the relentless demand for smaller, faster, and more power-efficient electronic devices. Companies are investing heavily in research and development to produce etching agents with higher purity, improved selectivity, and reduced environmental impact. Regulatory frameworks, particularly concerning emissions and hazardous materials, are becoming increasingly stringent, shaping product development and market entry strategies. Product substitutes, such as alternative etching technologies or different chemical compositions, pose a constant challenge, necessitating continuous innovation and cost optimization. End-user trends, dominated by the burgeoning semiconductor, LCD, and solar cell industries, dictate the demand for specific etching agents like C5F8, C4F6, CF4, CHF3, CH2F2, CH3F, and C2F6. Mergers and acquisitions (M&A) are also prevalent, with significant M&A deal values in the past contributing to market consolidation and expansion of product portfolios. For instance, an estimated market share concentration among the top five players currently stands at approximately 65 million, with M&A deal values reaching an estimated 800 million in the last five years.

Fluoride Etching Agent Industry Trends & Insights

The Fluoride Etching Agent industry is poised for robust growth, driven by a confluence of technological advancements, escalating demand from key application segments, and evolving manufacturing processes. The projected Compound Annual Growth Rate (CAGR) for the market is an impressive 7.5 million, indicating a significant expansion over the forecast period. This growth is predominantly fueled by the insatiable global demand for advanced semiconductor chips, essential for powering everything from smartphones and artificial intelligence to automotive electronics and 5G infrastructure. The increasing complexity and miniaturization of integrated circuits necessitate highly precise and selective etching processes, driving the demand for high-purity fluoride etching agents.

Technological disruptions are at the forefront of industry evolution. Innovations in plasma etching techniques, including the development of novel gas mixtures and etching chemistries, are continually pushing the boundaries of semiconductor fabrication. Manufacturers are focusing on developing etching agents that offer superior etch rates, reduced damage to sensitive materials, and enhanced uniformity across wafer surfaces. The quest for higher yields and lower manufacturing costs is a key consumer preference, compelling suppliers to deliver cost-effective yet high-performance solutions.

The competitive dynamics within the Fluoride Etching Agent market are characterized by intense competition among established global players and emerging regional manufacturers. Strategic partnerships, mergers, and acquisitions are common strategies employed to gain market share, expand product portfolios, and enhance technological capabilities. Companies are also investing in vertical integration to secure raw material supply and control the entire production chain, ensuring product quality and cost competitiveness.

The increasing adoption of advanced packaging technologies in semiconductors, which involve intricate layering and etching processes, is a significant growth driver. Furthermore, the burgeoning solar cell industry, with its continuous drive for higher efficiency and lower manufacturing costs, presents a substantial opportunity for fluoride etching agents in wafer processing. The liquid crystal display (LCD) market, though mature, still contributes to the demand for specific etching agents, particularly in the production of specialized display technologies. Market penetration is expected to reach 80 million units by 2030.

Dominant Markets & Segments in Fluoride Etching Agent

The global Fluoride Etching Agent market is characterized by its vital role in the production of advanced electronic components. The Semiconductor application segment is undoubtedly the dominant force, driven by the exponential growth in demand for microprocessors, memory chips, and application-specific integrated circuits (ASICs). This segment's dominance is underpinned by several key drivers:

- Technological Advancements in Chip Manufacturing: The relentless pursuit of Moore's Law, which predicts the doubling of transistors on a microchip approximately every two years, necessitates increasingly sophisticated etching processes. Fluoride etching agents are crucial for achieving the sub-micron and nanometer-scale features required for next-generation semiconductors.

- Growing Demand for AI and Machine Learning Hardware: The rapid expansion of artificial intelligence and machine learning applications requires massive computational power, translating into a surge in demand for high-performance AI chips.

- Proliferation of IoT Devices: The Internet of Things (IoT) ecosystem, encompassing smart homes, wearable technology, and industrial automation, relies heavily on a vast array of interconnected semiconductor devices, further fueling demand.

- 5G Network Deployment: The rollout of 5G infrastructure and devices necessitates advanced semiconductors capable of handling higher frequencies and data throughput, thereby increasing the need for precision etching.

Within the Type segmentation, C4F6 and CF4 are historically dominant due to their established use in various etching applications, offering a balance of etch rate and selectivity. However, newer fluorocarbons like C5F8 are gaining traction for specific advanced processes requiring enhanced selectivity and lower damage.

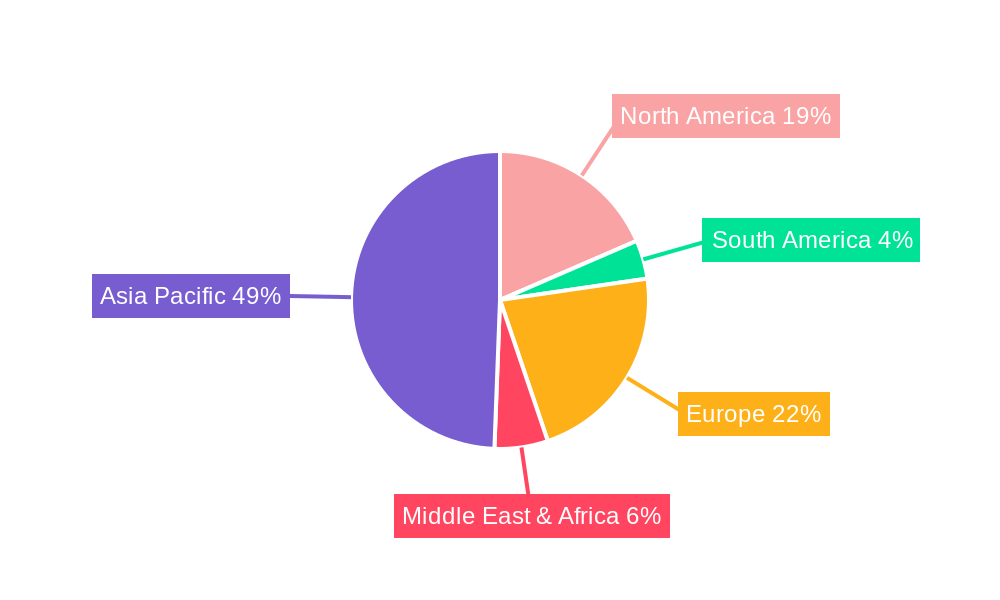

Geographically, Asia Pacific, particularly China, South Korea, and Taiwan, represents the dominant market. This dominance is attributed to:

- Concentration of Semiconductor Manufacturing Hubs: The region hosts the majority of the world's leading semiconductor foundries and fabrication plants.

- Government Initiatives and Investments: Proactive government policies and substantial investments in the semiconductor industry in countries like China are creating a highly favorable ecosystem.

- Expanding Electronics Manufacturing Base: Asia Pacific is a global manufacturing hub for consumer electronics, further driving demand for etched components.

The LCD segment, while experiencing shifts due to the rise of OLED technology, still contributes significantly to the market, especially for specialized displays. The Solar Cell segment is a growing area of interest, with etching agents playing a role in the manufacturing of photovoltaic cells to improve efficiency.

Fluoride Etching Agent Product Developments

Product innovation in Fluoride Etching Agents is a critical aspect of market competitiveness. Manufacturers are continuously developing ultra-high purity grades of existing etching gases and introducing novel fluorinated compounds with improved properties. Key trends include the development of etching agents with enhanced selectivity for specific materials like silicon, silicon dioxide, and silicon nitride, enabling finer feature creation and reduced substrate damage. Environmental considerations are also driving the development of lower global warming potential (GWP) alternatives. These advancements are crucial for meeting the stringent requirements of next-generation semiconductor fabrication processes, advanced display technologies, and high-efficiency solar cells, offering a competitive edge through superior performance and process optimization. The market size for these specialized products is projected to reach an estimated 2,500 million by 2033.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Fluoride Etching Agent market across key segmentation parameters. The Application segment is divided into Semiconductor, LCD, Solar Cell, and Others. The Semiconductor segment is projected to exhibit a CAGR of 8.2 million, driven by advanced chip manufacturing needs. The LCD segment, while more mature, still accounts for a significant market share, estimated at 300 million. The Solar Cell segment is anticipated to grow at a CAGR of 6.5 million, spurred by renewable energy initiatives. The Others segment, encompassing applications in MEMS and specialized industrial processes, is expected to contribute an estimated 150 million.

The Type segmentation includes C5F8, C4F6, CF4, CHF3, CH2F2, CH3F, C2F6, and Others. C4F6 and CF4 represent established segments with a combined market value of approximately 1,800 million. C5F8 is witnessing rapid growth, projected at a CAGR of 9.0 million, driven by its advanced etching capabilities. CHF3, CH2F2, CH3F, and C2F6 cater to specific niche applications and are expected to maintain steady growth. The Others category, encompassing emerging fluorocarbons, is projected to grow at a CAGR of 5.5 million.

Key Drivers of Fluoride Etching Agent Growth

The Fluoride Etching Agent market is propelled by several interconnected drivers. Technologically, the miniaturization of electronic components and the increasing complexity of semiconductor architectures necessitate highly precise and selective etching processes, directly boosting demand for advanced fluoride etching agents. Economically, the booming demand for consumer electronics, artificial intelligence, 5G technology, and the expansion of the electric vehicle market are creating substantial market pull. Regulatory factors, such as stricter environmental regulations, are indirectly driving innovation towards lower GWP and safer etching agents. For example, the increasing adoption of EUV lithography in semiconductor manufacturing requires specialized etching chemicals, creating a significant growth opportunity.

Challenges in the Fluoride Etching Agent Sector

Despite the robust growth prospects, the Fluoride Etching Agent sector faces several challenges. Stringent environmental regulations and the push for sustainable manufacturing processes can increase compliance costs and necessitate the development of costly alternative chemicals. Supply chain disruptions, geopolitical instability, and raw material price volatility can impact production costs and availability. Furthermore, the high capital expenditure required for establishing and maintaining advanced chemical manufacturing facilities presents a barrier to entry for new players. Intense competition and the threat of substitute technologies also pose ongoing challenges, demanding continuous innovation and cost optimization. The estimated impact of supply chain disruptions on market growth is around 150 million annually.

Emerging Opportunities in Fluoride Etching Agent

Emerging opportunities in the Fluoride Etching Agent market are primarily driven by advancements in key end-user industries. The rapid growth of the Internet of Things (IoT) ecosystem, with its diverse array of connected devices, is creating a sustained demand for semiconductors requiring specialized etching processes. The expansion of advanced packaging technologies in semiconductors, such as 3D stacking and heterogeneous integration, opens new avenues for tailored etching solutions. Furthermore, the increasing adoption of electric vehicles (EVs) and the development of next-generation battery technologies will necessitate advanced semiconductor components, thus driving demand. The growing focus on next-generation displays, including MicroLED technology, also presents significant opportunities for novel etching agents.

Leading Players in the Fluoride Etching Agent Market

- Nippon Sanso Holdings Corporation

- Kanto Denka Kogyo Co., Ltd.

- Linde

- SK Specialty

- Foosung

- Air Liquide

- Merck

- Resonac

- DAIKIN

- Zeon Corporation

- Air Products

- Chengdu KMT Gas

- Haohua Chemical Science and Technology

- TEMC

- Grandit Co., Ltd

- Solvay

- Ling Gas

- Peric Special Gases

- Ingentec Corporation

- Yuji Tech

- Jing He Science

- Jinhong Gas Co., Ltd

- Fujian Deer Technology

Key Developments in Fluoride Etching Agent Industry

- 2023: Launch of new ultra-high purity CF4 variants by a leading player for advanced node semiconductor manufacturing, impacting market dynamics by improving etch selectivity by an estimated 10%.

- 2022: Significant investment in R&D by a major chemical company to develop low-GWP alternatives to traditional etching gases, reflecting a shift towards sustainability.

- 2021: Acquisition of a specialty gas manufacturer by a global industrial gas supplier to expand its portfolio of electronic chemicals, demonstrating market consolidation.

- 2020: Introduction of novel C5F8 formulations by a key player for enhanced plasma etch processes in display manufacturing, leading to improved resolution and yield.

- 2019: Agreement between two major semiconductor material suppliers to collaborate on next-generation etching solutions, highlighting strategic partnerships.

Strategic Outlook for Fluoride Etching Agent Market

The strategic outlook for the Fluoride Etching Agent market remains highly optimistic, fueled by the continuous innovation in the electronics industry. The increasing demand for more powerful and efficient semiconductors for AI, 5G, and IoT applications will be a primary growth catalyst. Investments in advanced manufacturing technologies and a growing emphasis on supply chain resilience will shape market strategies. Companies that can effectively balance performance, cost-effectiveness, and environmental sustainability in their product offerings will be best positioned for long-term success. The ongoing evolution of display technologies and the expanding solar energy sector also present significant avenues for market expansion and diversification.

Fluoride Etching Agent Segmentation

-

1. Application

- 1.1. Semiconductor

- 1.2. LCD

- 1.3. Solar Cell

- 1.4. Others

-

2. Type

- 2.1. C5F8

- 2.2. C4F6

- 2.3. CF4

- 2.4. CHF3

- 2.5. CH2F2

- 2.6. CH3F

- 2.7. C2F6

- 2.8. Others

Fluoride Etching Agent Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fluoride Etching Agent REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.8% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fluoride Etching Agent Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Semiconductor

- 5.1.2. LCD

- 5.1.3. Solar Cell

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. C5F8

- 5.2.2. C4F6

- 5.2.3. CF4

- 5.2.4. CHF3

- 5.2.5. CH2F2

- 5.2.6. CH3F

- 5.2.7. C2F6

- 5.2.8. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fluoride Etching Agent Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Semiconductor

- 6.1.2. LCD

- 6.1.3. Solar Cell

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. C5F8

- 6.2.2. C4F6

- 6.2.3. CF4

- 6.2.4. CHF3

- 6.2.5. CH2F2

- 6.2.6. CH3F

- 6.2.7. C2F6

- 6.2.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fluoride Etching Agent Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Semiconductor

- 7.1.2. LCD

- 7.1.3. Solar Cell

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. C5F8

- 7.2.2. C4F6

- 7.2.3. CF4

- 7.2.4. CHF3

- 7.2.5. CH2F2

- 7.2.6. CH3F

- 7.2.7. C2F6

- 7.2.8. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fluoride Etching Agent Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Semiconductor

- 8.1.2. LCD

- 8.1.3. Solar Cell

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. C5F8

- 8.2.2. C4F6

- 8.2.3. CF4

- 8.2.4. CHF3

- 8.2.5. CH2F2

- 8.2.6. CH3F

- 8.2.7. C2F6

- 8.2.8. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fluoride Etching Agent Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Semiconductor

- 9.1.2. LCD

- 9.1.3. Solar Cell

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. C5F8

- 9.2.2. C4F6

- 9.2.3. CF4

- 9.2.4. CHF3

- 9.2.5. CH2F2

- 9.2.6. CH3F

- 9.2.7. C2F6

- 9.2.8. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fluoride Etching Agent Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Semiconductor

- 10.1.2. LCD

- 10.1.3. Solar Cell

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. C5F8

- 10.2.2. C4F6

- 10.2.3. CF4

- 10.2.4. CHF3

- 10.2.5. CH2F2

- 10.2.6. CH3F

- 10.2.7. C2F6

- 10.2.8. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Nippon Sanso Holdings Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Kanto Denka Kogyo Co. Ltd.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Linde

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 SK Specialty

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Foosung

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Air Liquide

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Merck

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Resonac

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DAIKIN

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Zeon Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Air Products

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Chengdu KMT Gas

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Haohua Chemical Science and Technology

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 TEMC

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Grandit Co. Ltd

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Solvay

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Ling Gas

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Peric Special Gases

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Ingentec Corporation

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Yuji Tech

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Jing He Science

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Jinhong Gas Co. Ltd

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Fujian Deer Technology

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.1 Nippon Sanso Holdings Corporation

List of Figures

- Figure 1: Global Fluoride Etching Agent Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Fluoride Etching Agent Revenue (million), by Application 2024 & 2032

- Figure 3: North America Fluoride Etching Agent Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Fluoride Etching Agent Revenue (million), by Type 2024 & 2032

- Figure 5: North America Fluoride Etching Agent Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Fluoride Etching Agent Revenue (million), by Country 2024 & 2032

- Figure 7: North America Fluoride Etching Agent Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Fluoride Etching Agent Revenue (million), by Application 2024 & 2032

- Figure 9: South America Fluoride Etching Agent Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Fluoride Etching Agent Revenue (million), by Type 2024 & 2032

- Figure 11: South America Fluoride Etching Agent Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Fluoride Etching Agent Revenue (million), by Country 2024 & 2032

- Figure 13: South America Fluoride Etching Agent Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Fluoride Etching Agent Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Fluoride Etching Agent Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Fluoride Etching Agent Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Fluoride Etching Agent Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Fluoride Etching Agent Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Fluoride Etching Agent Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Fluoride Etching Agent Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Fluoride Etching Agent Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Fluoride Etching Agent Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Fluoride Etching Agent Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Fluoride Etching Agent Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Fluoride Etching Agent Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Fluoride Etching Agent Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Fluoride Etching Agent Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Fluoride Etching Agent Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Fluoride Etching Agent Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Fluoride Etching Agent Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Fluoride Etching Agent Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Fluoride Etching Agent Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Fluoride Etching Agent Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Fluoride Etching Agent Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Fluoride Etching Agent Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Fluoride Etching Agent Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Fluoride Etching Agent Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Fluoride Etching Agent Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Fluoride Etching Agent Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Fluoride Etching Agent Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Fluoride Etching Agent Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Fluoride Etching Agent Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Fluoride Etching Agent Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Fluoride Etching Agent Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Fluoride Etching Agent Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Fluoride Etching Agent Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Fluoride Etching Agent Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Fluoride Etching Agent Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Fluoride Etching Agent Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Fluoride Etching Agent Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Fluoride Etching Agent Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluoride Etching Agent?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Fluoride Etching Agent?

Key companies in the market include Nippon Sanso Holdings Corporation, Kanto Denka Kogyo Co., Ltd., Linde, SK Specialty, Foosung, Air Liquide, Merck, Resonac, DAIKIN, Zeon Corporation, Air Products, Chengdu KMT Gas, Haohua Chemical Science and Technology, TEMC, Grandit Co., Ltd, Solvay, Ling Gas, Peric Special Gases, Ingentec Corporation, Yuji Tech, Jing He Science, Jinhong Gas Co., Ltd, Fujian Deer Technology.

3. What are the main segments of the Fluoride Etching Agent?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 997 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fluoride Etching Agent," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fluoride Etching Agent report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fluoride Etching Agent?

To stay informed about further developments, trends, and reports in the Fluoride Etching Agent, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence