Key Insights

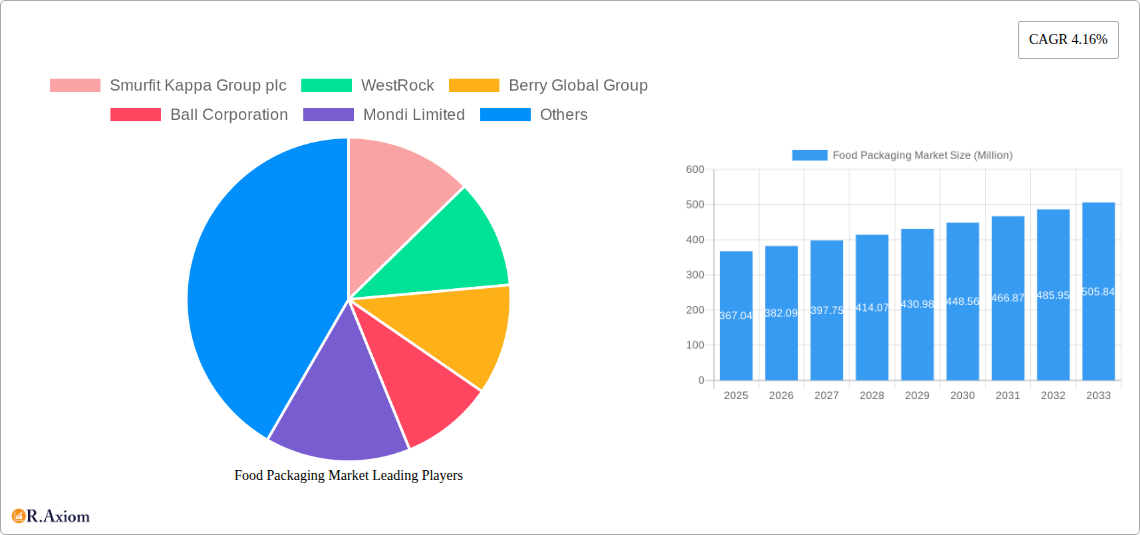

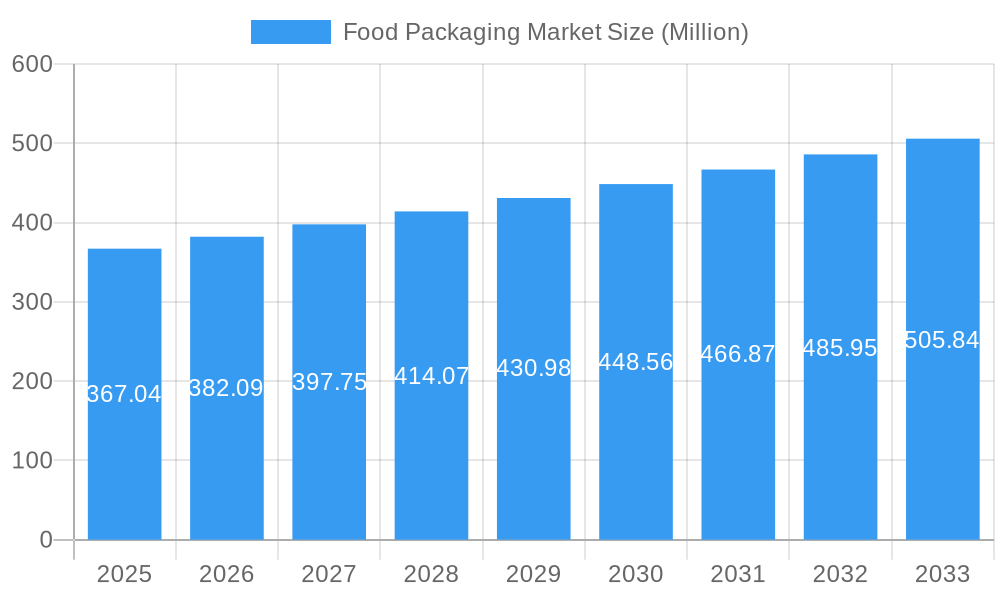

The global Food Packaging Market is poised for significant expansion, projected to reach a substantial USD 367.04 million in 2025 and grow at a healthy Compound Annual Growth Rate (CAGR) of 4.16% throughout the forecast period of 2025-2033. This robust growth is primarily fueled by evolving consumer preferences for convenience, the increasing demand for safe and hygienic food products, and the growing influence of e-commerce in food retail. The market is witnessing a strong emphasis on sustainable packaging solutions, with a notable shift towards recyclable and biodegradable materials like paper and paperboard, and innovative plastic alternatives. Rigid packaging, including cans and gusseted boxes, continues to hold a significant share, driven by its protective qualities for various food items. However, flexible packaging, encompassing pouches and bottles, is experiencing rapid adoption due to its cost-effectiveness and suitability for a wide range of applications, particularly for convenience foods and on-the-go consumption. The dairy products and poultry & meat products segments are significant contributors to market revenue, owing to their consistent demand and the critical need for effective barrier properties.

Food Packaging Market Market Size (In Million)

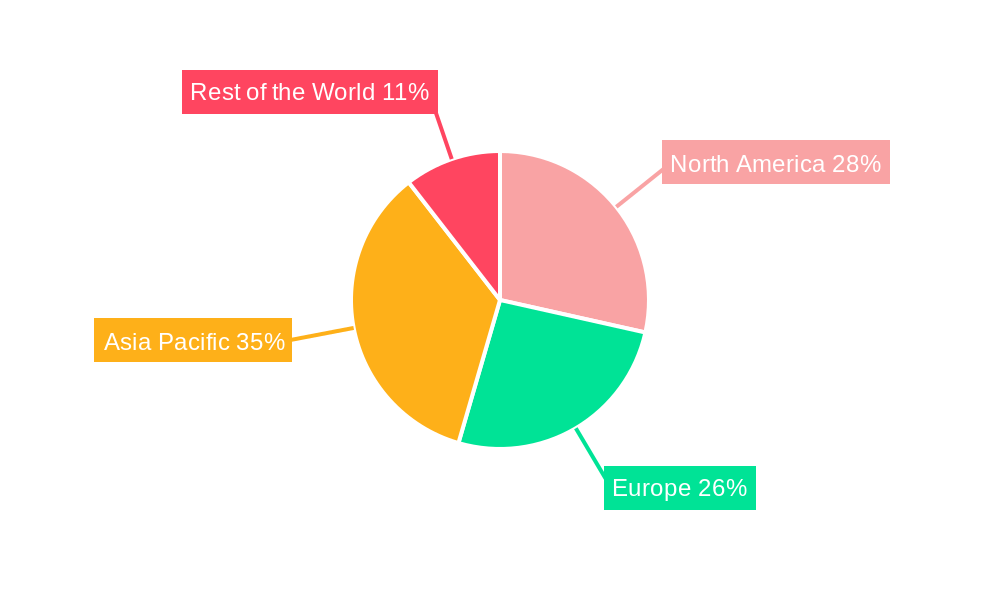

Key market drivers include the burgeoning middle class in emerging economies, leading to increased disposable income and a higher consumption of processed and packaged foods. Furthermore, advancements in packaging technology, such as smart packaging solutions offering enhanced traceability and extended shelf life, are actively contributing to market dynamism. While the market presents considerable opportunities, certain restraints, such as fluctuating raw material prices and stringent environmental regulations that necessitate costly material innovations, could temper growth. Nevertheless, strategic investments in research and development, coupled with a focus on circular economy principles, are expected to mitigate these challenges. Companies like Smurfit Kappa Group plc, WestRock, Berry Global Group, and Amcor Plc are at the forefront of this transformation, innovating to meet the diverse needs of the food industry across regions like North America, Europe, and the Asia Pacific. The Asia Pacific region, particularly China and India, is anticipated to be a major growth engine, driven by rapid industrialization and an expanding consumer base.

Food Packaging Market Company Market Share

Food Packaging Market: Comprehensive Analysis, Growth Drivers, and Future Outlook (2019-2033)

This in-depth report provides a strategic overview of the global Food Packaging Market, encompassing market dynamics, segmentation analysis, competitive landscape, and future projections. With a study period spanning from 2019 to 2033, the report offers valuable insights for stakeholders seeking to capitalize on the evolving demands for safe, sustainable, and innovative food packaging solutions. The estimated market size is projected to reach USD 500,000 Million by 2025, with a projected Compound Annual Growth Rate (CAGR) of 5.8% during the forecast period of 2025–2033.

Food Packaging Market Market Concentration & Innovation

The Food Packaging Market exhibits a moderate level of concentration, with several large multinational corporations holding significant market share. Key players like Amcor Plc, Ball Corporation, Smurfit Kappa Group plc, and WestRock dominate a substantial portion of the market, driven by their extensive product portfolios, global reach, and ongoing investment in research and development. Innovation is a critical determinant of success, fueled by the increasing demand for sustainable materials, enhanced product shelf life, and consumer convenience. Regulatory frameworks, particularly concerning food safety, environmental impact, and recyclability, also play a pivotal role in shaping product development and market strategies. The threat of product substitutes, especially from emerging biodegradable and compostable materials, is a constant consideration for traditional packaging providers. End-user trends, such as the rise of e-commerce, demand for portion-controlled packaging, and a growing preference for premiumization, are directly influencing packaging design and functionality. Mergers and acquisitions (M&A) activity remains robust, with recent deal values indicating a strategic consolidation trend. For instance, the acquisition of Scholle IPN by SIG in June 2022, valued at USD 1,530 Million, highlights the industry's focus on expanding capabilities in flexible and sustainable packaging solutions.

- Market Share Dominance: Key players hold a collective market share of approximately 65%.

- M&A Deal Value: Significant M&A activities are anticipated to exceed USD 10,000 Million annually in the coming years.

- Innovation Drivers: Sustainability, convenience, barrier properties, and cost-effectiveness are primary innovation drivers.

- Regulatory Influence: Stringent regulations on food contact materials and single-use plastics are shaping R&D priorities.

Food Packaging Market Industry Trends & Insights

The global Food Packaging Market is on a trajectory of robust growth, propelled by a confluence of technological advancements, shifting consumer preferences, and evolving industry dynamics. The increasing global population and rising disposable incomes, particularly in emerging economies, are directly translating into higher demand for packaged food products, thereby fueling market expansion. Technological disruptions, such as the development of advanced barrier materials, smart packaging solutions, and innovative printing techniques, are revolutionizing how food is preserved and presented. Consumers are increasingly demanding packaging that not only ensures food safety and extends shelf life but also aligns with their personal values regarding sustainability and convenience. This has led to a significant surge in demand for eco-friendly packaging options, including recyclable, compostable, and biodegradable materials. The competitive landscape is characterized by intense rivalry, with companies differentiating themselves through product innovation, supply chain efficiency, and strategic partnerships. The market penetration of flexible packaging, for instance, has witnessed substantial growth due to its versatility, cost-effectiveness, and lightweight properties. The market is projected to grow at a CAGR of 5.8% from 2025 to 2033, with an estimated market size of USD 500,000 Million in 2025. Key growth drivers include the expanding e-commerce sector, which necessitates robust and secure packaging solutions, and the growing trend of on-the-go consumption, driving demand for convenient, single-serving formats. Furthermore, the food processing industry's continuous efforts to reduce food waste through effective packaging are indirectly stimulating market growth. The increasing adoption of automation and advanced manufacturing processes is also contributing to improved production efficiencies and cost reductions, making packaged food more accessible. The industry is also witnessing a growing emphasis on circular economy principles, encouraging the design of packaging that can be easily reused or recycled, thereby minimizing environmental impact.

Dominant Markets & Segments in Food Packaging Market

The Food Packaging Market is characterized by distinct regional dominance and segment leadership, driven by economic policies, infrastructure development, and localized consumer preferences. Globally, the Plastic segment within the Type of Material category holds a commanding position, driven by its versatility, cost-effectiveness, and excellent barrier properties, which are crucial for preserving food quality and extending shelf life. Within the Packaging Type segment, Flexible Packaging continues to lead, owing to its lightweight nature, adaptability to various product shapes, and cost advantages, making it ideal for a wide array of food applications, from snacks to ready-to-eat meals. The Pouches and bottles sub-segment under Other Packaging Types is also experiencing significant growth, catering to the demand for convenience and portability. In terms of Product Type, Converted Roll Stock remains a dominant segment, serving as a foundational component for many flexible packaging formats. The Dairy Products and Poultry and Meat Products application segments are major contributors to market revenue, necessitating specialized packaging that ensures safety, hygiene, and extended shelf life.

- Leading Material: Plastic packaging, estimated to hold over 40% of the market share, driven by its diverse applications and performance characteristics.

- Dominant Packaging Type: Flexible packaging, projected to account for approximately 35% of the market by 2025, favored for its versatility and cost-efficiency.

- Key Product Type: Converted Roll Stock, essential for producing a wide range of flexible packaging formats.

- Major Application Segments: Dairy products and Poultry & Meat Products, representing a combined market share of over 45%, due to stringent safety and preservation requirements.

- Regional Dominance: North America and Europe are leading markets, driven by high consumer spending and advanced packaging infrastructure, with Asia Pacific showing the fastest growth potential.

Food Packaging Market Product Developments

Product innovation in the Food Packaging Market is accelerating, with a strong emphasis on sustainability and functionality. Companies are actively developing novel materials and designs to meet evolving consumer demands and regulatory pressures. Advancements in biodegradable and compostable plastics, alongside improved paper-based solutions, are gaining traction. Smart packaging technologies, incorporating features like freshness indicators and tamper-evident seals, are enhancing product safety and consumer experience. The development of lightweight yet robust packaging for e-commerce is also a key trend, ensuring products arrive undamaged while minimizing shipping costs and environmental impact. These innovations aim to enhance shelf life, reduce food waste, and provide greater convenience for consumers, while also contributing to a more sustainable packaging ecosystem.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Food Packaging Market across its diverse segments. The Type of Material segmentation includes Plastic, Metal, Glass, and Paper and Paperboard, each offering unique properties and applications. The Packaging Type segmentation covers Rigid, Semi Rigid, and Flexible formats, catering to a wide spectrum of product needs. Within Product Type, key categories include Cans, Converted Roll Stock, Gusseted Box, Corrugated Box, Boxboard, and Other Packaging Types (Pouches and bottles). The Application segmentation further breaks down the market by Dairy Products, Poultry and Meat Products, Fruits & Vegetables, Bakery & Confectionery, and Other Applications. Each segment is analyzed for market size, growth projections, and competitive dynamics, providing a granular understanding of market opportunities and challenges. The Plastic segment is expected to maintain its lead with a projected market size of USD 200,000 Million by 2025. Flexible packaging is forecast to grow at a CAGR of 6.2% during the forecast period.

Key Drivers of Food Packaging Market Growth

The Food Packaging Market is propelled by several key drivers that are reshaping its landscape.

- Rising Global Population and Urbanization: Increased demand for conveniently packaged food products to meet the needs of growing urban populations.

- Growing E-commerce Penetration: The surge in online grocery shopping necessitates robust, secure, and appealing packaging solutions for direct-to-consumer delivery.

- Consumer Preference for Convenience and Portability: Demand for single-serving packages, resealable options, and easy-to-open designs for on-the-go consumption.

- Emphasis on Food Safety and Shelf-Life Extension: Advanced barrier properties and preservation technologies in packaging are crucial for reducing food spoilage and waste.

- Sustainability and Eco-Friendly Packaging Initiatives: Growing consumer and regulatory pressure for recyclable, biodegradable, and compostable packaging solutions, driving innovation in material science.

Challenges in the Food Packaging Market Sector

Despite the positive growth trajectory, the Food Packaging Market faces several challenges that can hinder its expansion.

- Stringent Regulatory Frameworks: Evolving regulations related to food contact materials, plastic waste, and recycling standards can increase compliance costs and necessitate product redesign.

- Volatile Raw Material Prices: Fluctuations in the cost of key raw materials, such as crude oil (for plastics) and pulp (for paper and paperboard), can impact profitability.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and logistics challenges can disrupt the availability and timely delivery of packaging materials.

- Consumer Perception and Environmental Concerns: Negative public perception surrounding certain packaging materials, particularly plastics, can lead to market resistance and increased demand for alternatives.

- High Capital Investment for Advanced Technologies: Adoption of cutting-edge sustainable packaging technologies often requires substantial capital investment, posing a barrier for smaller players.

Emerging Opportunities in Food Packaging Market

The Food Packaging Market is ripe with emerging opportunities, driven by innovation and evolving consumer demands.

- Growth in Sustainable and Biodegradable Packaging: The increasing demand for eco-friendly solutions presents a significant opportunity for companies offering compostable, biodegradable, and recycled content packaging.

- Development of Smart Packaging: Integration of IoT technologies for tracking, monitoring, and enhancing food safety and consumer engagement through features like QR codes and temperature sensors.

- Expansion of Ready-to-Eat and Meal Kit Services: These sectors require specialized, convenient, and safe packaging solutions, driving demand for innovative designs.

- Growth in Emerging Economies: Rising disposable incomes and evolving lifestyles in developing nations are creating new markets for packaged food and consequently, food packaging.

- Innovation in Barrier Technologies: Development of advanced materials that provide superior protection against oxygen, moisture, and light, leading to extended shelf life and reduced food waste.

Leading Players in the Food Packaging Market Market

- Smurfit Kappa Group plc

- WestRock

- Berry Global Group

- Ball Corporation

- Mondi Limited

- Tetra Pak

- Amcor Plc

- Crown Holdings Inc

- Schur Flexibles Group

- International Papers

- Sealed Air Corp

- Anchor Packaging Inc

- Graham Packaging Company Inc

Key Developments in Food Packaging Market Industry

- August 2022: Seal Packaging introduced fresh eco-friendly packaging options. The first UKCA-marked plastic-free paper cups, the It's Not Paper bag collection, a workable and ecological replacement for conventional paper bags, and the Compostabowl are just a few of the new, creative goods now being introduced. This development highlights a strategic focus on sustainable alternatives to traditional single-use packaging, catering to increasing environmental awareness.

- June 2022: SIG completed the acquisition of Scholle IPN, a flexible packaging solution provider with an enterprise value of USD 1.53 billion. The acquisition is expected to enable SIG to offer sustainable, low-carbon packaging solutions across a broad range of categories and product sizes. This move signifies a significant consolidation in the flexible packaging sector, aiming to enhance offerings in sustainable and low-carbon solutions.

Strategic Outlook for Food Packaging Market Market

The strategic outlook for the Food Packaging Market remains overwhelmingly positive, driven by sustained demand and a strong impetus for innovation. The ongoing shift towards sustainable packaging materials, coupled with advancements in smart packaging technologies, will continue to shape market dynamics. Companies that prioritize eco-friendly solutions, invest in R&D for enhanced functionality, and adapt to evolving consumer preferences for convenience and safety will be best positioned for success. The increasing adoption of automation and digitalization across the value chain will also be critical for operational efficiency and cost competitiveness. Furthermore, strategic partnerships and mergers & acquisitions will likely continue as companies seek to expand their product portfolios and geographical reach. The market's ability to address challenges related to raw material volatility and regulatory compliance will be crucial for unlocking its full growth potential.

Food Packaging Market Segmentation

-

1. Type of Material

- 1.1. Plastic

- 1.2. Metal

- 1.3. Glass

- 1.4. Paper and Paperboard

-

2. Packaging Type

- 2.1. Rigid

- 2.2. Semi Rigid

- 2.3. Flexible

-

3. Product Type

- 3.1. Cans

- 3.2. Converted Roll Stock

- 3.3. Gusseted Box

- 3.4. Corrugated Box

- 3.5. Boxboard

- 3.6. Other Packaging Types (Pouches and bottles)

-

4. Application

- 4.1. Dairy Products

- 4.2. Poultry and Meat Products

- 4.3. Fruits & Vegetables

- 4.4. Bakery & Confectionery

- 4.5. Other Ap

Food Packaging Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. France

- 2.3. United Kingdom

- 2.4. Spain

- 2.5. Italy

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

- 4. Rest of the World

Food Packaging Market Regional Market Share

Geographic Coverage of Food Packaging Market

Food Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.16% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Material

- 5.1.1. Plastic

- 5.1.2. Metal

- 5.1.3. Glass

- 5.1.4. Paper and Paperboard

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Rigid

- 5.2.2. Semi Rigid

- 5.2.3. Flexible

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Cans

- 5.3.2. Converted Roll Stock

- 5.3.3. Gusseted Box

- 5.3.4. Corrugated Box

- 5.3.5. Boxboard

- 5.3.6. Other Packaging Types (Pouches and bottles)

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Dairy Products

- 5.4.2. Poultry and Meat Products

- 5.4.3. Fruits & Vegetables

- 5.4.4. Bakery & Confectionery

- 5.4.5. Other Ap

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type of Material

- 6. Global Food Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Material

- 6.1.1. Plastic

- 6.1.2. Metal

- 6.1.3. Glass

- 6.1.4. Paper and Paperboard

- 6.2. Market Analysis, Insights and Forecast - by Packaging Type

- 6.2.1. Rigid

- 6.2.2. Semi Rigid

- 6.2.3. Flexible

- 6.3. Market Analysis, Insights and Forecast - by Product Type

- 6.3.1. Cans

- 6.3.2. Converted Roll Stock

- 6.3.3. Gusseted Box

- 6.3.4. Corrugated Box

- 6.3.5. Boxboard

- 6.3.6. Other Packaging Types (Pouches and bottles)

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Dairy Products

- 6.4.2. Poultry and Meat Products

- 6.4.3. Fruits & Vegetables

- 6.4.4. Bakery & Confectionery

- 6.4.5. Other Ap

- 6.1. Market Analysis, Insights and Forecast - by Type of Material

- 7. North America Food Packaging Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Material

- 7.1.1. Plastic

- 7.1.2. Metal

- 7.1.3. Glass

- 7.1.4. Paper and Paperboard

- 7.2. Market Analysis, Insights and Forecast - by Packaging Type

- 7.2.1. Rigid

- 7.2.2. Semi Rigid

- 7.2.3. Flexible

- 7.3. Market Analysis, Insights and Forecast - by Product Type

- 7.3.1. Cans

- 7.3.2. Converted Roll Stock

- 7.3.3. Gusseted Box

- 7.3.4. Corrugated Box

- 7.3.5. Boxboard

- 7.3.6. Other Packaging Types (Pouches and bottles)

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. Dairy Products

- 7.4.2. Poultry and Meat Products

- 7.4.3. Fruits & Vegetables

- 7.4.4. Bakery & Confectionery

- 7.4.5. Other Ap

- 7.1. Market Analysis, Insights and Forecast - by Type of Material

- 8. Europe Food Packaging Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Material

- 8.1.1. Plastic

- 8.1.2. Metal

- 8.1.3. Glass

- 8.1.4. Paper and Paperboard

- 8.2. Market Analysis, Insights and Forecast - by Packaging Type

- 8.2.1. Rigid

- 8.2.2. Semi Rigid

- 8.2.3. Flexible

- 8.3. Market Analysis, Insights and Forecast - by Product Type

- 8.3.1. Cans

- 8.3.2. Converted Roll Stock

- 8.3.3. Gusseted Box

- 8.3.4. Corrugated Box

- 8.3.5. Boxboard

- 8.3.6. Other Packaging Types (Pouches and bottles)

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. Dairy Products

- 8.4.2. Poultry and Meat Products

- 8.4.3. Fruits & Vegetables

- 8.4.4. Bakery & Confectionery

- 8.4.5. Other Ap

- 8.1. Market Analysis, Insights and Forecast - by Type of Material

- 9. Asia Pacific Food Packaging Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Material

- 9.1.1. Plastic

- 9.1.2. Metal

- 9.1.3. Glass

- 9.1.4. Paper and Paperboard

- 9.2. Market Analysis, Insights and Forecast - by Packaging Type

- 9.2.1. Rigid

- 9.2.2. Semi Rigid

- 9.2.3. Flexible

- 9.3. Market Analysis, Insights and Forecast - by Product Type

- 9.3.1. Cans

- 9.3.2. Converted Roll Stock

- 9.3.3. Gusseted Box

- 9.3.4. Corrugated Box

- 9.3.5. Boxboard

- 9.3.6. Other Packaging Types (Pouches and bottles)

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. Dairy Products

- 9.4.2. Poultry and Meat Products

- 9.4.3. Fruits & Vegetables

- 9.4.4. Bakery & Confectionery

- 9.4.5. Other Ap

- 9.1. Market Analysis, Insights and Forecast - by Type of Material

- 10. Rest of the World Food Packaging Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Material

- 10.1.1. Plastic

- 10.1.2. Metal

- 10.1.3. Glass

- 10.1.4. Paper and Paperboard

- 10.2. Market Analysis, Insights and Forecast - by Packaging Type

- 10.2.1. Rigid

- 10.2.2. Semi Rigid

- 10.2.3. Flexible

- 10.3. Market Analysis, Insights and Forecast - by Product Type

- 10.3.1. Cans

- 10.3.2. Converted Roll Stock

- 10.3.3. Gusseted Box

- 10.3.4. Corrugated Box

- 10.3.5. Boxboard

- 10.3.6. Other Packaging Types (Pouches and bottles)

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. Dairy Products

- 10.4.2. Poultry and Meat Products

- 10.4.3. Fruits & Vegetables

- 10.4.4. Bakery & Confectionery

- 10.4.5. Other Ap

- 10.1. Market Analysis, Insights and Forecast - by Type of Material

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Smurfit Kappa Group plc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 WestRock

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Berry Global Group

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Ball Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Mondi Limited

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Tetra Pak

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Amcor Plc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Crown Holdings Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Schur Flexibles Group

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 International Papers

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Sealed Air Corp

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Anchor Packaging Inc

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Graham Packaging Company Inc *List Not Exhaustive

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.1 Smurfit Kappa Group plc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Food Packaging Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Food Packaging Market Revenue (Million), by Type of Material 2025 & 2033

- Figure 3: North America Food Packaging Market Revenue Share (%), by Type of Material 2025 & 2033

- Figure 4: North America Food Packaging Market Revenue (Million), by Packaging Type 2025 & 2033

- Figure 5: North America Food Packaging Market Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 6: North America Food Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 7: North America Food Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: North America Food Packaging Market Revenue (Million), by Application 2025 & 2033

- Figure 9: North America Food Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Food Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Food Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Food Packaging Market Revenue (Million), by Type of Material 2025 & 2033

- Figure 13: Europe Food Packaging Market Revenue Share (%), by Type of Material 2025 & 2033

- Figure 14: Europe Food Packaging Market Revenue (Million), by Packaging Type 2025 & 2033

- Figure 15: Europe Food Packaging Market Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 16: Europe Food Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 17: Europe Food Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Europe Food Packaging Market Revenue (Million), by Application 2025 & 2033

- Figure 19: Europe Food Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 20: Europe Food Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Food Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Food Packaging Market Revenue (Million), by Type of Material 2025 & 2033

- Figure 23: Asia Pacific Food Packaging Market Revenue Share (%), by Type of Material 2025 & 2033

- Figure 24: Asia Pacific Food Packaging Market Revenue (Million), by Packaging Type 2025 & 2033

- Figure 25: Asia Pacific Food Packaging Market Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 26: Asia Pacific Food Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 27: Asia Pacific Food Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Asia Pacific Food Packaging Market Revenue (Million), by Application 2025 & 2033

- Figure 29: Asia Pacific Food Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Food Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 32: Rest of the World Food Packaging Market Revenue (Million), by Type of Material 2025 & 2033

- Figure 33: Rest of the World Food Packaging Market Revenue Share (%), by Type of Material 2025 & 2033

- Figure 34: Rest of the World Food Packaging Market Revenue (Million), by Packaging Type 2025 & 2033

- Figure 35: Rest of the World Food Packaging Market Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 36: Rest of the World Food Packaging Market Revenue (Million), by Product Type 2025 & 2033

- Figure 37: Rest of the World Food Packaging Market Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Rest of the World Food Packaging Market Revenue (Million), by Application 2025 & 2033

- Figure 39: Rest of the World Food Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 40: Rest of the World Food Packaging Market Revenue (Million), by Country 2025 & 2033

- Figure 41: Rest of the World Food Packaging Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Packaging Market Revenue Million Forecast, by Type of Material 2020 & 2033

- Table 2: Global Food Packaging Market Revenue Million Forecast, by Packaging Type 2020 & 2033

- Table 3: Global Food Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: Global Food Packaging Market Revenue Million Forecast, by Application 2020 & 2033

- Table 5: Global Food Packaging Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Food Packaging Market Revenue Million Forecast, by Type of Material 2020 & 2033

- Table 7: Global Food Packaging Market Revenue Million Forecast, by Packaging Type 2020 & 2033

- Table 8: Global Food Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 9: Global Food Packaging Market Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Global Food Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Food Packaging Market Revenue Million Forecast, by Type of Material 2020 & 2033

- Table 14: Global Food Packaging Market Revenue Million Forecast, by Packaging Type 2020 & 2033

- Table 15: Global Food Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 16: Global Food Packaging Market Revenue Million Forecast, by Application 2020 & 2033

- Table 17: Global Food Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Germany Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: France Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: United Kingdom Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Spain Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Food Packaging Market Revenue Million Forecast, by Type of Material 2020 & 2033

- Table 25: Global Food Packaging Market Revenue Million Forecast, by Packaging Type 2020 & 2033

- Table 26: Global Food Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 27: Global Food Packaging Market Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Food Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 29: China Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Japan Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: India Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Australia Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Asia Pacific Food Packaging Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Food Packaging Market Revenue Million Forecast, by Type of Material 2020 & 2033

- Table 35: Global Food Packaging Market Revenue Million Forecast, by Packaging Type 2020 & 2033

- Table 36: Global Food Packaging Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 37: Global Food Packaging Market Revenue Million Forecast, by Application 2020 & 2033

- Table 38: Global Food Packaging Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Packaging Market?

The projected CAGR is approximately 4.16%.

2. Which companies are prominent players in the Food Packaging Market?

Key companies in the market include Smurfit Kappa Group plc, WestRock, Berry Global Group, Ball Corporation, Mondi Limited, Tetra Pak, Amcor Plc, Crown Holdings Inc, Schur Flexibles Group, International Papers, Sealed Air Corp, Anchor Packaging Inc, Graham Packaging Company Inc *List Not Exhaustive.

3. What are the main segments of the Food Packaging Market?

The market segments include Type of Material, Packaging Type, Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 367.04 Million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Convenience Foods in Developing Economies; Increasing Demand for Shelf-Life Extension of Foods Accelerating the Food Packaging Market; Trend of Small Households.

6. What are the notable trends driving market growth?

Increasing Demand for Shelf-Life Extension of Foods Accelerating the Food Packaging Market.

7. Are there any restraints impacting market growth?

Stringent Regulations Pertaining to Food Packaging.

8. Can you provide examples of recent developments in the market?

August 2022: Seal Packaging introduced fresh eco-friendly packaging options. The first UKCA-marked plastic-free paper cups, the It's Not Paper bag collection, a workable and ecological replacement for conventional paper bags, and the Compostabowl are just a few of the new, creative goods now being introduced.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Packaging Market?

To stay informed about further developments, trends, and reports in the Food Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence