Key Insights

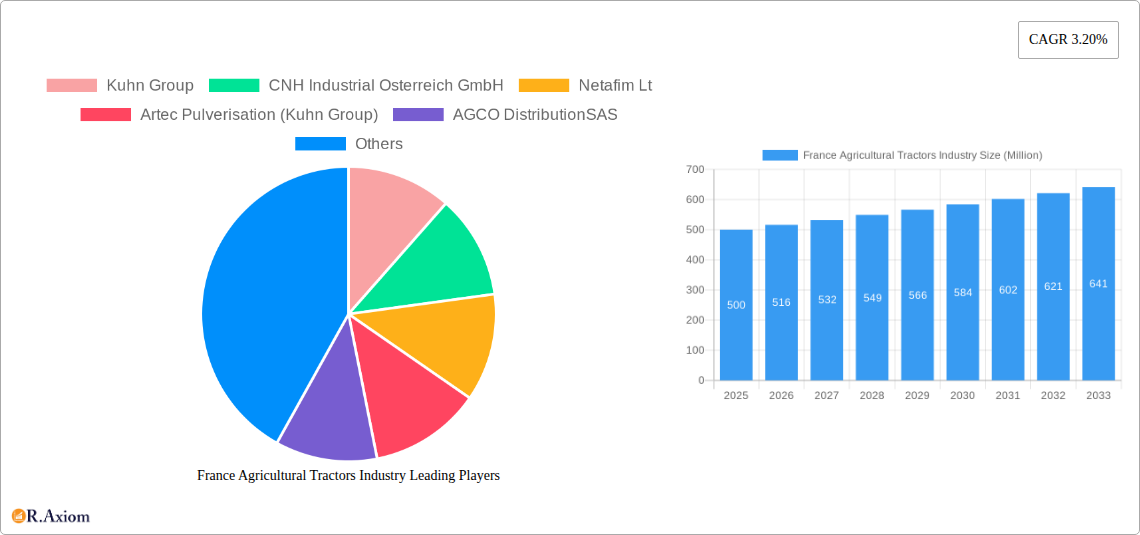

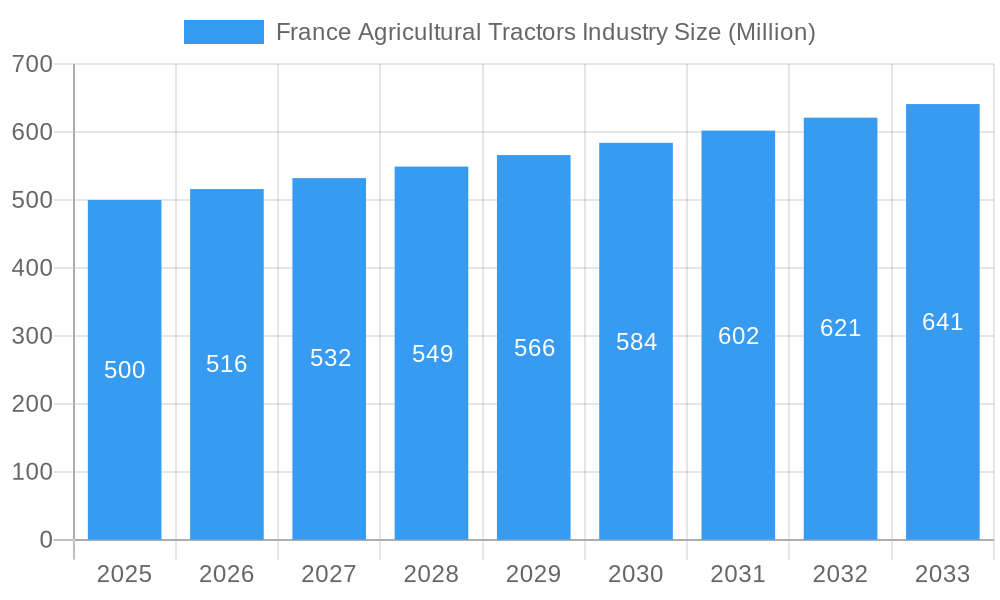

The French agricultural tractor market, valued at approximately €[Estimate based on market size XX and value unit Million; assume XX is a value, for example, 500 million Euros in 2025] in 2025, exhibits a steady growth trajectory, projected at a CAGR of 3.20% from 2025 to 2033. This growth is fueled by several key factors. Firstly, increasing demand for efficient and technologically advanced machinery to enhance agricultural productivity in France is a major driver. Farmers are increasingly adopting tractors with advanced features like precision farming technologies (GPS guidance, auto-steer), improving yields and reducing operational costs. Secondly, supportive government policies aimed at modernizing the agricultural sector and encouraging the adoption of sustainable farming practices are also contributing to market expansion. Finally, the rising prevalence of large-scale farming operations necessitates the use of more powerful and versatile tractors, further driving market demand.

France Agricultural Tractors Industry Market Size (In Million)

However, the market faces some challenges. Fluctuations in agricultural commodity prices and the overall economic climate can significantly impact investment in new machinery. Furthermore, increasing regulations related to emissions and environmental sustainability might put pressure on tractor manufacturers to adopt expensive technological upgrades, potentially impacting profitability and slowing down the overall market growth in the short term. Segment-wise, the high horsepower (80 HP and above) tractor segment is expected to witness robust growth due to the increasing trend towards larger farm sizes and the need for heavier-duty machinery. The market is highly competitive, with key players like John Deere, Kubota, CNH Industrial, and CLAAS dominating the landscape through their established dealer networks and brand recognition. The market's future hinges on a balanced interplay between technological advancements, favorable government policies, and stable economic conditions.

France Agricultural Tractors Industry Company Market Share

France Agricultural Tractors Industry: A Comprehensive Market Analysis (2019-2033)

This in-depth report provides a comprehensive analysis of the France agricultural tractors industry, encompassing market size, segmentation, growth drivers, challenges, and key players. The report covers the period from 2019 to 2033, with a focus on the forecast period 2025-2033 and a base year of 2025. It offers actionable insights for industry stakeholders, investors, and businesses operating within or seeking entry into this dynamic market. The report’s findings are based on extensive primary and secondary research, encompassing data from official sources, industry publications, and expert interviews. The total market value in 2024 is estimated at xx Million, with projections extending to 2033.

France Agricultural Tractors Industry Market Concentration & Innovation

The French agricultural tractor market exhibits a moderately concentrated structure, with several multinational corporations commanding significant market share. Key players include John Deere SAS, CNH Industrial Osterreich GmbH, and CLAAS Group, amongst others. While precise market share figures for each company are proprietary and vary by tractor segment, John Deere and CNH Industrial consistently hold leading positions. The industry is characterized by ongoing innovation, driven by the need for enhanced efficiency, precision farming techniques, and sustainability.

- Innovation Drivers: Technological advancements in automation, precision agriculture (GPS-guided machinery, sensor technology), and alternative fuel sources are reshaping the industry landscape.

- Regulatory Framework: EU regulations concerning emissions, safety, and sustainable farming practices significantly influence the market. Compliance necessitates continuous technological upgrades, impacting both production costs and product features.

- Product Substitutes: While direct substitutes for tractors are limited, the rise of alternative farming methods and labor-saving technologies indirectly affects demand.

- End-User Trends: A growing emphasis on sustainable farming practices and reduced environmental impact is driving demand for fuel-efficient and technologically advanced tractors.

- M&A Activities: While precise M&A deal values are confidential, the sector has witnessed several mergers and acquisitions in recent years, reflecting consolidation trends. These activities aim to increase market share, expand product portfolios, and achieve economies of scale.

France Agricultural Tractors Industry Industry Trends & Insights

The French agricultural tractor market is projected to experience a CAGR of xx% during the forecast period (2025-2033). Several factors contribute to this growth:

- Increased mechanization: Modernization of French farms continues to drive demand for higher horsepower tractors, along with advanced machinery. The market penetration of technologically sophisticated equipment is gradually increasing.

- Government support: Agricultural subsidies and policies aimed at improving farming efficiency have positively impacted market growth.

- Favorable climatic conditions: Although subject to year-to-year fluctuations, France’s generally favorable agricultural climate supports strong agricultural output, hence equipment demand.

- Competitive landscape: Intense competition among major players fosters innovation and price competitiveness, benefits consumers, and encourages adoption. However, this also leads to pressures on profit margins.

The market is witnessing a significant technological disruption with the increasing adoption of precision farming technologies. Consumer preferences are shifting towards fuel-efficient, versatile, and technologically advanced tractors capable of precision tasks.

Dominant Markets & Segments in France Agricultural Tractors Industry

The French agricultural tractor market is regionally diverse, with higher demand concentrated in major agricultural regions. Specific regional dominance data is proprietary but generally aligns with known high agricultural output areas. Among segments, the demand for tractors in the 50-79 HP and 80-99 HP ranges is relatively high, reflecting the prevalence of medium-sized farms.

Key Drivers:

- Strong agricultural production base

- Government support for farm modernization

- Favorable climatic conditions in certain regions

- Well-developed agricultural infrastructure

Dominance Analysis: The 'Tractors' segment, broken down by horsepower, and 'Harvesting Machinery' (particularly combine harvesters) constitute the largest market shares. Within the harvesting segment, the demand for forage harvesters shows robust growth driven by the livestock sector. The high demand for 50-79 HP and 80-99 HP tractors reflects the size distribution of French farms.

France Agricultural Tractors Industry Product Developments

Recent product innovations focus on enhancing efficiency, precision, and sustainability. Manufacturers are introducing tractors with improved fuel economy, advanced automation features (GPS-guided steering, automated implement control), and telematics capabilities for remote monitoring and data analysis. These advancements enhance operational efficiency, reduce labor costs, and improve yield. The market also sees a rise in specialized equipment tailored to specific crops and farming techniques.

Report Scope & Segmentation Analysis

This report segments the French agricultural tractor market into various categories:

- Plowing and Cultivating Machinery: This includes plows (disc and moldboard), harrows, cultivators, tillers, and other machinery. The market for minimum-till equipment is growing, reflecting a focus on soil conservation.

- Planting Machinery: This covers seed drills, planters, spreaders, and other planting equipment. Precision planting technology is gaining traction.

- Harvesting Machinery: This segment includes combine harvesters, forage harvesters, and equipment for harvesting root crops and fruits/vegetables. The demand for high-capacity harvesters is increasing.

- Haying and Forage Machinery: This encompasses mowers, balers, and other equipment used in hay and forage production.

- Irrigation Machinery: This includes sprinkler and drip irrigation systems. The market is seeing increased adoption of water-efficient irrigation technologies.

- Tractors: This segment is further divided by horsepower (less than 50 HP, 50-79 HP, 80-99 HP, 100-120 HP, greater than 120 HP).

Each segment's growth trajectory is analyzed, considering factors like market size, competitive dynamics, and technological advancements.

Key Drivers of France Agricultural Tractors Industry Growth

The growth of the French agricultural tractor market is primarily driven by:

- Technological advancements: Precision farming, automation, and improved fuel efficiency are key factors driving adoption.

- Government policies: Subsidies and support for farm modernization are crucial.

- Favorable climatic conditions (generally): Climate influences crop yields and hence demand for machinery.

- Rising labor costs: Mechanization helps offset increasing labor costs.

Challenges in the France Agricultural Tractors Industry Sector

The industry faces several challenges:

- High initial investment costs: Advanced tractors and machinery require substantial upfront investment.

- Economic fluctuations: Agricultural commodity prices influence farmer investment decisions.

- Competition: Intense competition among manufacturers leads to price pressures.

- Supply chain disruptions: Global events can impact the availability of components and equipment.

Emerging Opportunities in France Agricultural Tractors Industry

Opportunities exist in:

- Precision farming technologies: Further development and adoption of GPS-guided systems and sensor technologies.

- Sustainable farming practices: Equipment tailored to minimize environmental impact.

- Data analytics and farm management software: Integrating data from machinery to optimize farming operations.

Leading Players in the France Agricultural Tractors Industry Market

- Kuhn Group

- CNH Industrial Osterreich GmbH

- Netafim Lt

- Artec Pulverisation (Kuhn Group)

- AGCO Distribution SAS

- CLAAS Group

- Yanmar Co Ltd

- Same Deutz-Fahr France

- Kubota Europe SAS

- John Deere SAS

- Lely France

Key Developments in France Agricultural Tractors Industry Industry

- November 2022: AGCO launched the Geo-Bird, a free online operational planning tool for Western European farmers, including France (launched at the Valtra stand in Paris). This development enhances farm management efficiency.

- March 2022: KUHN SAS announced a new 12m Optimer minimum tillage stubble cultivator, featuring the Steady Control system. This innovation improves tillage efficiency and soil conservation.

- February 2022: John Deere launched the 6R 185 tractor, emphasizing fuel efficiency. This launch strengthens their position in the fuel-efficient tractor segment.

Strategic Outlook for France Agricultural Tractors Industry Market

The French agricultural tractor market is poised for continued growth, driven by technological advancements, government support, and the ongoing need for improved farming efficiency and sustainability. Focus on precision agriculture, automation, and data-driven solutions will shape future market dynamics. Opportunities abound for companies that can offer innovative, sustainable, and cost-effective solutions to address the evolving needs of French farmers.

France Agricultural Tractors Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

France Agricultural Tractors Industry Segmentation By Geography

- 1. France

France Agricultural Tractors Industry Regional Market Share

Geographic Coverage of France Agricultural Tractors Industry

France Agricultural Tractors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. France

- 6. France Agricultural Tractors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Kuhn Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CNH Industrial Osterreich GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Netafim Lt

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Artec Pulverisation (Kuhn Group)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 AGCO DistributionSAS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CLAAS Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Yanmar Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Same Deutz-Fahr France

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Kubota Europe SAS

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 John Deere SAS

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Lely France

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Kuhn Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: France Agricultural Tractors Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: France Agricultural Tractors Industry Share (%) by Company 2025

List of Tables

- Table 1: France Agricultural Tractors Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: France Agricultural Tractors Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: France Agricultural Tractors Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: France Agricultural Tractors Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: France Agricultural Tractors Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: France Agricultural Tractors Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: France Agricultural Tractors Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: France Agricultural Tractors Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: France Agricultural Tractors Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: France Agricultural Tractors Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: France Agricultural Tractors Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: France Agricultural Tractors Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Agricultural Tractors Industry?

The projected CAGR is approximately 3.20%.

2. Which companies are prominent players in the France Agricultural Tractors Industry?

Key companies in the market include Kuhn Group, CNH Industrial Osterreich GmbH, Netafim Lt, Artec Pulverisation (Kuhn Group), AGCO DistributionSAS, CLAAS Group, Yanmar Co Ltd, Same Deutz-Fahr France, Kubota Europe SAS, John Deere SAS, Lely France.

3. What are the main segments of the France Agricultural Tractors Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

Large-scale Agricultural Production is Driving Mechanization.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

November 2022: AGCO Launched a online Free Operational Planning Tool called Geo-Bird for Farmers in Western Europe. In France, this has launched on the Valtra Stand in Paris.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Agricultural Tractors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Agricultural Tractors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Agricultural Tractors Industry?

To stay informed about further developments, trends, and reports in the France Agricultural Tractors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence