Key Insights

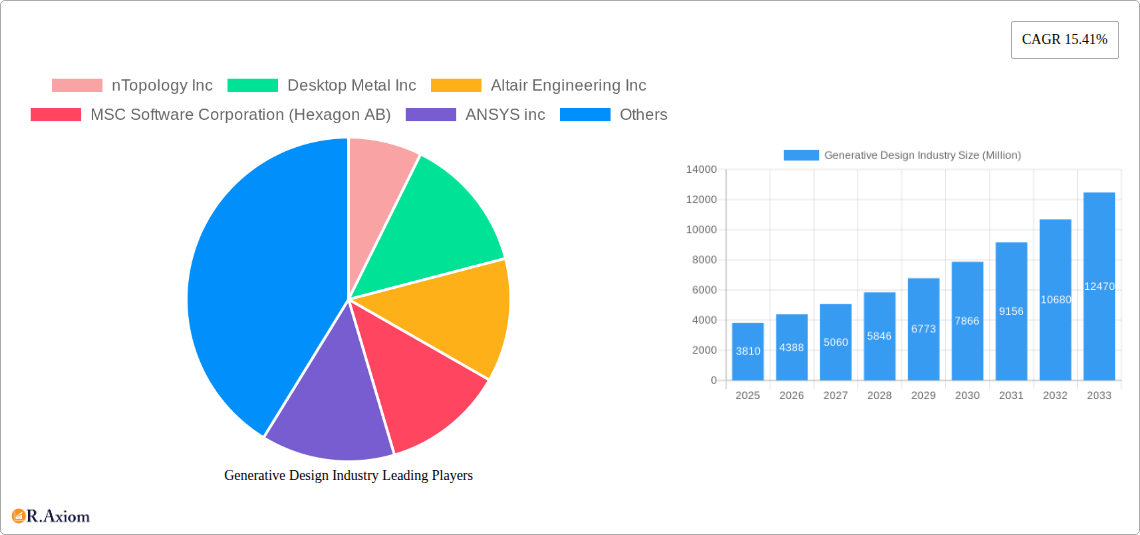

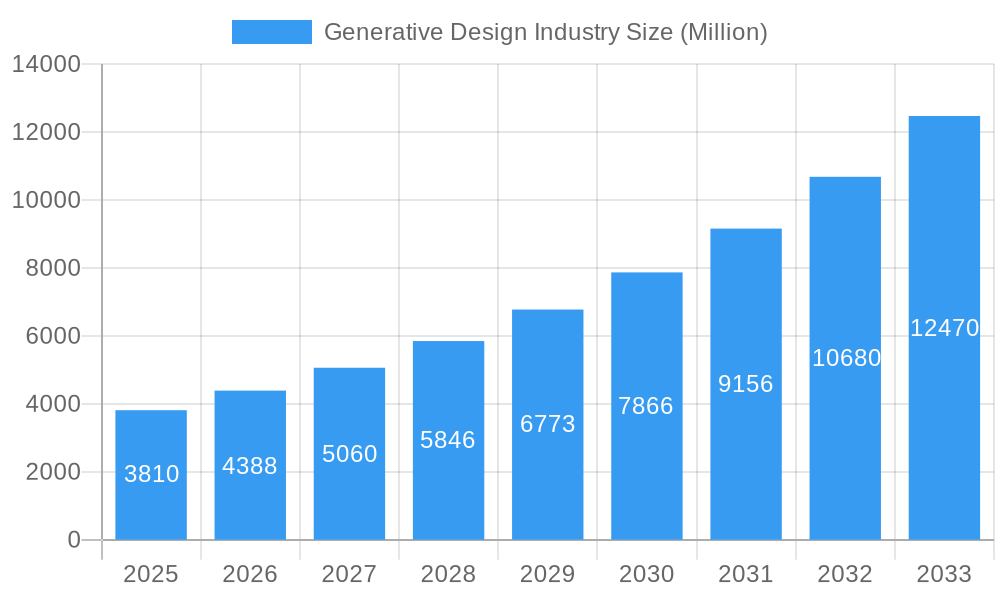

The generative design market is experiencing robust growth, projected to reach $3.81 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 15.41% from 2025 to 2033. This expansion is fueled by several key drivers. Firstly, the increasing need for optimization across various industries, including automotive, aerospace, and manufacturing, is driving adoption. Generative design tools significantly reduce design time and material costs while enhancing product performance and sustainability. Secondly, advancements in artificial intelligence (AI) and machine learning (ML) are continuously improving the capabilities of generative design software, making it more accessible and efficient. This includes improved algorithms for optimization and the integration of advanced simulation tools for more accurate and robust designs. Finally, the growing availability of cloud-based solutions is expanding access to generative design software, particularly for smaller companies and those lacking in-house computational resources.

Generative Design Industry Market Size (In Billion)

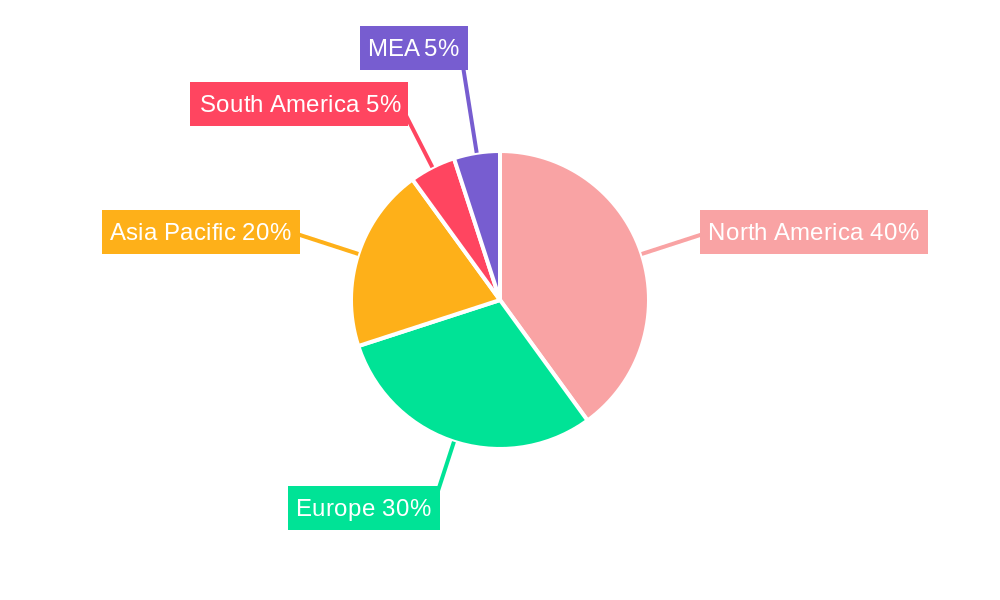

Despite the substantial growth potential, the market faces certain restraints. The high initial investment cost of software and specialized hardware can be a barrier to entry for smaller businesses. Furthermore, a lack of skilled professionals proficient in using these advanced design tools creates a significant hurdle for wider adoption. However, the ongoing development of user-friendly interfaces and the increasing availability of training programs are steadily mitigating these challenges. The market segmentation reveals a strong preference for cloud-based deployment models due to their scalability and cost-effectiveness. The automotive, aerospace, and industrial manufacturing sectors remain the largest consumers of generative design technologies, though architectural and construction applications are also experiencing rapid growth, driven by the need to create efficient and sustainable building designs. The North American market currently holds a significant share, although Asia-Pacific is projected to witness substantial growth in the coming years due to increasing manufacturing activities and technological advancements in the region.

Generative Design Industry Company Market Share

Generative Design Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Generative Design industry, covering market size, growth drivers, competitive landscape, and future outlook from 2019 to 2033. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period covers 2025-2033, and the historical period encompasses 2019-2024. The report features detailed segmentation analysis across deployment models (on-premise, cloud), end-user verticals (automotive, aerospace & defense, architecture & construction, industrial manufacturing, others), and leading market players. The report projects a market value of $XX Million by 2033, with a CAGR of XX% during the forecast period.

Generative Design Industry Market Concentration & Innovation

The Generative Design industry is characterized by a moderately concentrated market, with a few key players holding significant market share. While precise market share data for individual companies is commercially sensitive, nTopology Inc, Desktop Metal Inc, Altair Engineering Inc, MSC Software Corporation (Hexagon AB), and ANSYS inc are consistently recognized as leading vendors. The industry exhibits strong innovation drivers, fueled by advancements in AI, machine learning, and additive manufacturing technologies. Regulatory frameworks, particularly concerning data privacy and intellectual property, are evolving and will continue to shape market dynamics. Product substitutes, such as traditional CAD software with advanced optimization tools, pose a competitive challenge. End-user trends towards automation, efficiency, and sustainable design are key growth factors.

The industry has witnessed significant M&A activity in recent years. Notably, the acquisition of ParaMatters by Carbon in August 2022, valued at approximately $XX Million, signifies the increasing consolidation within the space. This deal highlights the strategic importance of generative design capabilities for additive manufacturing companies. Other significant M&A transactions, though not publicly disclosed with precise values, have contributed to shaping the competitive landscape. Further, the successful funding round for Diabatix in January 2022 underscores investor confidence in the potential of AI-driven generative design solutions.

Generative Design Industry Industry Trends & Insights

The Generative Design industry is experiencing rapid growth, driven by several factors. The increasing adoption of additive manufacturing (3D printing) is a primary catalyst, enabling the creation of complex, lightweight, and optimized designs previously impossible with traditional manufacturing methods. Technological disruptions, such as advancements in AI and machine learning algorithms, further enhance the capabilities and efficiency of generative design software. Consumer preferences for customized and sustainable products are pushing manufacturers towards utilizing generative design to optimize product performance and reduce material waste. The competitive dynamics are marked by intense innovation, strategic partnerships, and acquisitions, all contributing to the overall market growth. The market is expected to reach $XX Million in 2025 and grow at a CAGR of XX% during the forecast period, achieving a market penetration rate of XX% by 2033. The high entry barrier due to expertise requirement in algorithm development and software integration is a significant barrier for entrants.

Dominant Markets & Segments in Generative Design Industry

The automotive and aerospace & defense sectors are currently the dominant end-user verticals for generative design, driven by the need for lightweight, high-performance components. The high demand for fuel efficiency and improved safety standards further contributes to this dominance. The industrial manufacturing segment is also experiencing significant growth, with companies adopting generative design to optimize production processes and reduce manufacturing costs. The architecture and construction sector is showing increasing adoption, leveraging generative design for the design of complex and efficient building structures and infrastructure.

- Key Drivers for Automotive & Aerospace: stringent regulations regarding fuel efficiency, demands for lightweight designs, the need for optimized aerodynamic performance.

- Key Drivers for Industrial Manufacturing: enhanced production efficiency, reduced manufacturing costs, optimized product design for improved functionality.

- Key Drivers for Architecture & Construction: optimized structural design, material reduction, cost savings in building construction.

Cloud-based deployment models are gaining traction due to their scalability, accessibility, and cost-effectiveness. However, on-premise deployments continue to be preferred by organizations with high security requirements and sensitive data. While North America currently holds the largest market share, the Asia-Pacific region is expected to witness the fastest growth due to increasing industrialization and technological advancements.

Generative Design Industry Product Developments

Recent product developments focus on enhancing the ease of use, integration with existing CAD/CAM software, and expanding the application scope of generative design software. New features include advanced simulation capabilities, improved optimization algorithms, and automated design workflows. Companies are strategically focusing on developing solutions that cater to specific industry needs, offering customized features and workflows to enhance the market fit. The competitive advantage lies in the efficiency and accuracy of algorithms and the intuitive user interfaces that streamline the design process.

Report Scope & Segmentation Analysis

This report segments the generative design market based on deployment (on-premise and cloud) and end-user verticals (automotive, aerospace and defense, architecture and construction, industrial manufacturing, and others).

Deployment: The on-premise segment currently holds a larger market share due to data security concerns but the cloud segment is projected to experience higher growth due to cost efficiency and accessibility.

End-User Verticals: The automotive sector is expected to remain the largest segment, followed by aerospace and defense. However, the industrial manufacturing sector is expected to showcase significant growth in the coming years. The architecture and construction sector is projected to grow at a slower pace but shows immense potential for future development. The "other" category will encompass diverse sectors adopting generative design solutions. Each segment demonstrates unique growth trajectories and competitive dynamics, influenced by industry-specific factors.

Key Drivers of Generative Design Industry Growth

Several factors contribute to the growth of the generative design industry. Technological advancements in artificial intelligence, machine learning, and additive manufacturing are paramount. The increasing need for product customization and efficient manufacturing processes further fuels market demand. Favorable government policies and investments in research and development are also contributing to the industry's expansion. The automotive and aerospace sectors, in particular, have strong incentives to adopt generative design for weight reduction and improved performance.

Challenges in the Generative Design Industry Sector

Despite the positive growth outlook, challenges remain. The high cost of software and specialized expertise required to utilize these technologies can be a barrier to entry for smaller companies. Integration with existing manufacturing workflows can be complex and time-consuming. Moreover, the relatively nascent nature of this technology means that industry standards and best practices are still evolving, leading to uncertainties. Addressing these challenges will be crucial for sustainable growth.

Emerging Opportunities in Generative Design Industry

Emerging opportunities include expansion into new industries (e.g., consumer goods, healthcare) and integration with other emerging technologies like the metaverse and digital twins. The development of user-friendly software and cloud-based solutions will improve accessibility and adoption rates. The integration of generative design into broader digital design workflows promises to increase efficiency and reduce design cycles. Focus on sustainable design practices will also open new avenues.

Leading Players in the Generative Design Industry Market

- nTopology Inc

- Desktop Metal Inc

- Altair Engineering Inc

- MSC Software Corporation (Hexagon AB)

- ANSYS inc

- Caracol AM

- Autodesk Inc

- Dassault Systèmes SE

- Bentley Systems Inc

- Paramatters

- Diabatix

Key Developments in Generative Design Industry Industry

- August 2022: ParaMatters, a provider of generative design software for additive manufacturing, was acquired by Carbon. This acquisition strengthened Carbon's generative design capabilities for additive manufacturing.

- January 2022: Diabatix NV, specializing in AI-driven generative thermal design, secured funding from Saffelberg Investments, accelerating the growth of its Coldstream platform.

Strategic Outlook for Generative Design Industry Market

The generative design industry holds immense potential for future growth. Continued technological advancements, coupled with increasing adoption across various industries, will drive market expansion. Focus on ease of use, accessibility, and integration with existing workflows will be crucial for broader market penetration. The industry is poised for significant growth, fueled by the increasing need for efficient, sustainable, and customized product design. Strategic partnerships and collaborations will play a significant role in accelerating innovation and market adoption.

Generative Design Industry Segmentation

-

1. Deployment

- 1.1. On-premise

- 1.2. Cloud

-

2. End User Vertical

- 2.1. Automotive

- 2.2. Aerospace and Defense

- 2.3. Architecture and Construction

- 2.4. Industrial Manufacturing

- 2.5. Other End User Verticals

Generative Design Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. UAE

- 5.2. Saudi Arabia

- 5.3. South Africa

- 5.4. Rest of Middle East and Africa

Generative Design Industry Regional Market Share

Geographic Coverage of Generative Design Industry

Generative Design Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.41% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud

- 5.2. Market Analysis, Insights and Forecast - by End User Vertical

- 5.2.1. Automotive

- 5.2.2. Aerospace and Defense

- 5.2.3. Architecture and Construction

- 5.2.4. Industrial Manufacturing

- 5.2.5. Other End User Verticals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Global Generative Design Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. On-premise

- 6.1.2. Cloud

- 6.2. Market Analysis, Insights and Forecast - by End User Vertical

- 6.2.1. Automotive

- 6.2.2. Aerospace and Defense

- 6.2.3. Architecture and Construction

- 6.2.4. Industrial Manufacturing

- 6.2.5. Other End User Verticals

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. North America Generative Design Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. On-premise

- 7.1.2. Cloud

- 7.2. Market Analysis, Insights and Forecast - by End User Vertical

- 7.2.1. Automotive

- 7.2.2. Aerospace and Defense

- 7.2.3. Architecture and Construction

- 7.2.4. Industrial Manufacturing

- 7.2.5. Other End User Verticals

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Europe Generative Design Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. On-premise

- 8.1.2. Cloud

- 8.2. Market Analysis, Insights and Forecast - by End User Vertical

- 8.2.1. Automotive

- 8.2.2. Aerospace and Defense

- 8.2.3. Architecture and Construction

- 8.2.4. Industrial Manufacturing

- 8.2.5. Other End User Verticals

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Asia Pacific Generative Design Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. On-premise

- 9.1.2. Cloud

- 9.2. Market Analysis, Insights and Forecast - by End User Vertical

- 9.2.1. Automotive

- 9.2.2. Aerospace and Defense

- 9.2.3. Architecture and Construction

- 9.2.4. Industrial Manufacturing

- 9.2.5. Other End User Verticals

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Latin America Generative Design Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. On-premise

- 10.1.2. Cloud

- 10.2. Market Analysis, Insights and Forecast - by End User Vertical

- 10.2.1. Automotive

- 10.2.2. Aerospace and Defense

- 10.2.3. Architecture and Construction

- 10.2.4. Industrial Manufacturing

- 10.2.5. Other End User Verticals

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Middle East and Africa Generative Design Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 11.1.1. On-premise

- 11.1.2. Cloud

- 11.2. Market Analysis, Insights and Forecast - by End User Vertical

- 11.2.1. Automotive

- 11.2.2. Aerospace and Defense

- 11.2.3. Architecture and Construction

- 11.2.4. Industrial Manufacturing

- 11.2.5. Other End User Verticals

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 nTopology Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Desktop Metal Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Altair Engineering Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 MSC Software Corporation (Hexagon AB)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 ANSYS inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Caracol AM

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Autodesk Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Dassault Systèmes SE

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bentley Systems Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Paramatters

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Diabatix

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 nTopology Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Generative Design Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Generative Design Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Generative Design Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 4: North America Generative Design Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 5: North America Generative Design Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 6: North America Generative Design Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 7: North America Generative Design Industry Revenue (Million), by End User Vertical 2025 & 2033

- Figure 8: North America Generative Design Industry Volume (K Unit), by End User Vertical 2025 & 2033

- Figure 9: North America Generative Design Industry Revenue Share (%), by End User Vertical 2025 & 2033

- Figure 10: North America Generative Design Industry Volume Share (%), by End User Vertical 2025 & 2033

- Figure 11: North America Generative Design Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Generative Design Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Generative Design Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Generative Design Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Generative Design Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 16: Europe Generative Design Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 17: Europe Generative Design Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 18: Europe Generative Design Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 19: Europe Generative Design Industry Revenue (Million), by End User Vertical 2025 & 2033

- Figure 20: Europe Generative Design Industry Volume (K Unit), by End User Vertical 2025 & 2033

- Figure 21: Europe Generative Design Industry Revenue Share (%), by End User Vertical 2025 & 2033

- Figure 22: Europe Generative Design Industry Volume Share (%), by End User Vertical 2025 & 2033

- Figure 23: Europe Generative Design Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Generative Design Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Generative Design Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Generative Design Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Generative Design Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 28: Asia Pacific Generative Design Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 29: Asia Pacific Generative Design Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 30: Asia Pacific Generative Design Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 31: Asia Pacific Generative Design Industry Revenue (Million), by End User Vertical 2025 & 2033

- Figure 32: Asia Pacific Generative Design Industry Volume (K Unit), by End User Vertical 2025 & 2033

- Figure 33: Asia Pacific Generative Design Industry Revenue Share (%), by End User Vertical 2025 & 2033

- Figure 34: Asia Pacific Generative Design Industry Volume Share (%), by End User Vertical 2025 & 2033

- Figure 35: Asia Pacific Generative Design Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Generative Design Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Generative Design Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Generative Design Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Latin America Generative Design Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 40: Latin America Generative Design Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 41: Latin America Generative Design Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 42: Latin America Generative Design Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 43: Latin America Generative Design Industry Revenue (Million), by End User Vertical 2025 & 2033

- Figure 44: Latin America Generative Design Industry Volume (K Unit), by End User Vertical 2025 & 2033

- Figure 45: Latin America Generative Design Industry Revenue Share (%), by End User Vertical 2025 & 2033

- Figure 46: Latin America Generative Design Industry Volume Share (%), by End User Vertical 2025 & 2033

- Figure 47: Latin America Generative Design Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Latin America Generative Design Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Latin America Generative Design Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Latin America Generative Design Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Generative Design Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 52: Middle East and Africa Generative Design Industry Volume (K Unit), by Deployment 2025 & 2033

- Figure 53: Middle East and Africa Generative Design Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 54: Middle East and Africa Generative Design Industry Volume Share (%), by Deployment 2025 & 2033

- Figure 55: Middle East and Africa Generative Design Industry Revenue (Million), by End User Vertical 2025 & 2033

- Figure 56: Middle East and Africa Generative Design Industry Volume (K Unit), by End User Vertical 2025 & 2033

- Figure 57: Middle East and Africa Generative Design Industry Revenue Share (%), by End User Vertical 2025 & 2033

- Figure 58: Middle East and Africa Generative Design Industry Volume Share (%), by End User Vertical 2025 & 2033

- Figure 59: Middle East and Africa Generative Design Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Generative Design Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Middle East and Africa Generative Design Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Generative Design Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Generative Design Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 2: Global Generative Design Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 3: Global Generative Design Industry Revenue Million Forecast, by End User Vertical 2020 & 2033

- Table 4: Global Generative Design Industry Volume K Unit Forecast, by End User Vertical 2020 & 2033

- Table 5: Global Generative Design Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Generative Design Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Generative Design Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 8: Global Generative Design Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 9: Global Generative Design Industry Revenue Million Forecast, by End User Vertical 2020 & 2033

- Table 10: Global Generative Design Industry Volume K Unit Forecast, by End User Vertical 2020 & 2033

- Table 11: Global Generative Design Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Generative Design Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Rest of North America Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of North America Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Generative Design Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 20: Global Generative Design Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 21: Global Generative Design Industry Revenue Million Forecast, by End User Vertical 2020 & 2033

- Table 22: Global Generative Design Industry Volume K Unit Forecast, by End User Vertical 2020 & 2033

- Table 23: Global Generative Design Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Generative Design Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Germany Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: France Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Spain Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Spain Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Rest of Europe Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of Europe Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Global Generative Design Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 36: Global Generative Design Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 37: Global Generative Design Industry Revenue Million Forecast, by End User Vertical 2020 & 2033

- Table 38: Global Generative Design Industry Volume K Unit Forecast, by End User Vertical 2020 & 2033

- Table 39: Global Generative Design Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Generative Design Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: China Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: China Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Japan Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Japan Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: India Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: India Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Rest of Asia Pacific Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Rest of Asia Pacific Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Global Generative Design Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 50: Global Generative Design Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 51: Global Generative Design Industry Revenue Million Forecast, by End User Vertical 2020 & 2033

- Table 52: Global Generative Design Industry Volume K Unit Forecast, by End User Vertical 2020 & 2033

- Table 53: Global Generative Design Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 54: Global Generative Design Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 55: Brazil Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: Brazil Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Argentina Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Argentina Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: Rest of Latin America Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Rest of Latin America Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Global Generative Design Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 62: Global Generative Design Industry Volume K Unit Forecast, by Deployment 2020 & 2033

- Table 63: Global Generative Design Industry Revenue Million Forecast, by End User Vertical 2020 & 2033

- Table 64: Global Generative Design Industry Volume K Unit Forecast, by End User Vertical 2020 & 2033

- Table 65: Global Generative Design Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 66: Global Generative Design Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 67: UAE Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 68: UAE Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 69: Saudi Arabia Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: Saudi Arabia Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 71: South Africa Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: South Africa Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: Rest of Middle East and Africa Generative Design Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Rest of Middle East and Africa Generative Design Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Generative Design Industry?

The projected CAGR is approximately 15.41%.

2. Which companies are prominent players in the Generative Design Industry?

Key companies in the market include nTopology Inc, Desktop Metal Inc, Altair Engineering Inc, MSC Software Corporation (Hexagon AB), ANSYS inc, Caracol AM, Autodesk Inc, Dassault Systèmes SE, Bentley Systems Inc, Paramatters, Diabatix.

3. What are the main segments of the Generative Design Industry?

The market segments include Deployment, End User Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.81 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in latest technology in automobile segment to boost the market; Growing Demand for Advanced Technologies to Drive Product Innovation and Production Efficiency.

6. What are the notable trends driving market growth?

Automotive To Hold Significant Share.

7. Are there any restraints impacting market growth?

Fluctuating Market Demands and Customization Issues.

8. Can you provide examples of recent developments in the market?

August 2022 - The provider of generative design software for additive manufacturing, ParaMatters, was acquired by Carbon, a company that develops technology for 3D printing. This acquisition would add topology optimization to Carbon's present software capabilities. Carbon could use the ParaMatters software to increase its generative design capabilities for additive manufacturing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Generative Design Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Generative Design Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Generative Design Industry?

To stay informed about further developments, trends, and reports in the Generative Design Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence