Key Insights

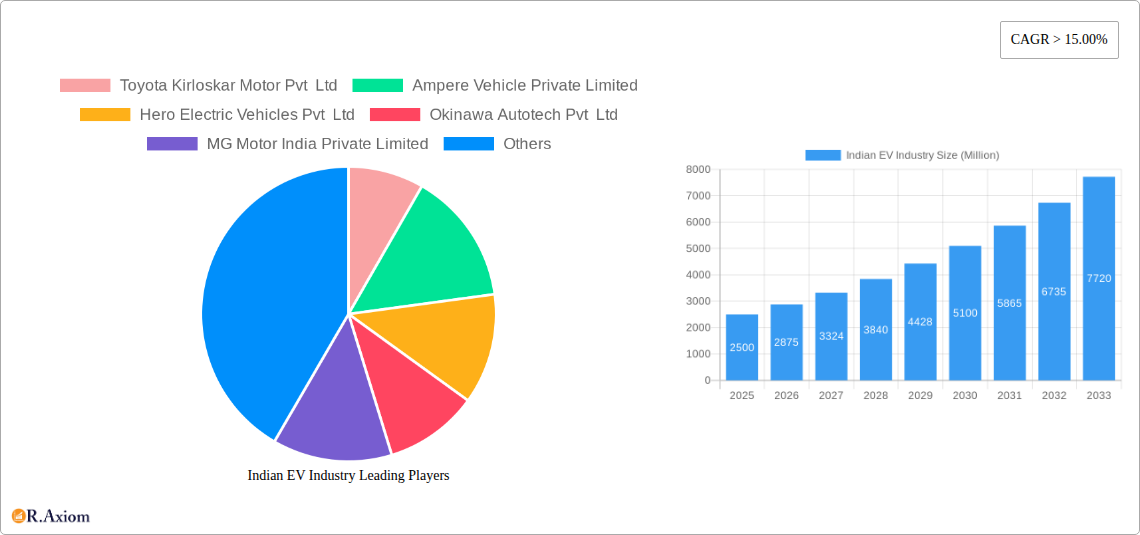

India's electric vehicle (EV) sector is experiencing rapid expansion, fueled by government mandates for sustainable transport, heightened consumer environmental consciousness, and decreasing battery prices. The market exhibits a projected Compound Annual Growth Rate (CAGR) of 57.23%. As of the base year 2025, the market size is valued at 2.3 million. This dynamic market presents significant opportunities across key segments, including two-wheelers, which lead due to affordability and urban commute suitability, and passenger vehicles, with a notable increase in demand for electric cars and SUVs. The commercial vehicle segment, encompassing trucks and buses, also shows strong potential driven by fleet operators' objectives for cost reduction and sustainability compliance. While infrastructure and initial costs pose challenges, government incentives, advancements in battery technology, and growing eco-friendly consumer preferences are mitigating these barriers. The expansion of charging networks and innovations in battery performance are expected to further accelerate market adoption. Regional adoption rates may vary, with urbanized areas potentially exhibiting higher penetration due to infrastructure development and consumer purchasing power. The competitive landscape is intense, featuring established domestic and international manufacturers alongside emerging players, all competing on technology, manufacturing prowess, and distribution networks. The forecast period of 2025-2033 indicates sustained growth, positioning India as a global leader in sustainable transportation.

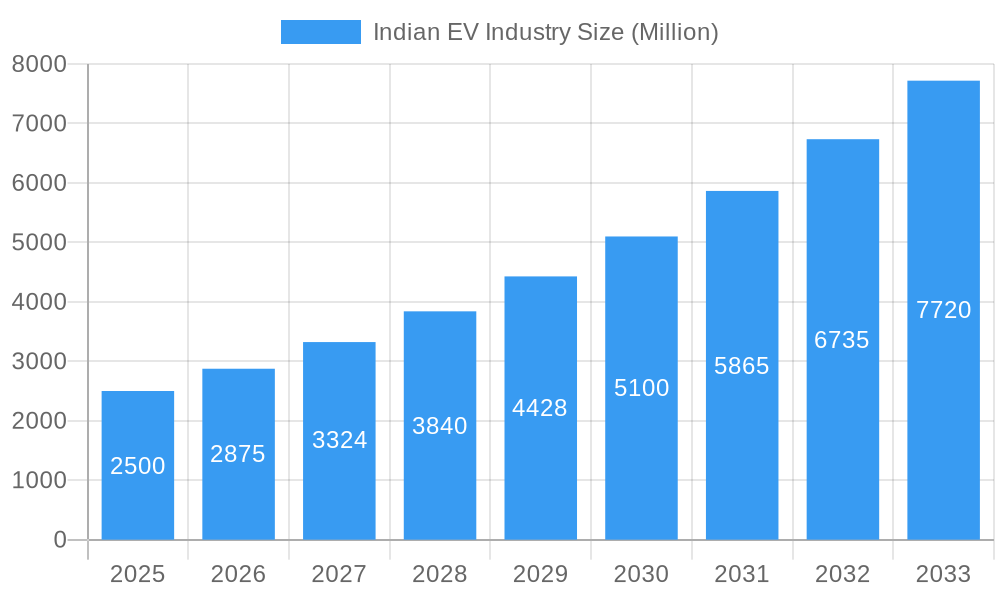

Indian EV Industry Market Size (In Million)

To ensure the continued success of the Indian EV market, addressing key challenges is paramount. Increased investment in charging infrastructure is vital to alleviate consumer range anxiety. Government policies must sustain support through subsidies and incentives while fostering a robust domestic supply chain for battery components. Technological advancements, especially in battery technology, are critical for reducing costs and enhancing EV performance, thereby increasing market appeal. Public awareness campaigns highlighting the advantages of EV adoption are essential for broad acceptance. The integration of smart charging technologies with smart grids will further enhance the sustainability and efficiency of the EV ecosystem. Finally, collaborative efforts among government, industry, and research institutions are fundamental to realizing the full potential of India's EV market and establishing it as a global standard for sustainable mobility.

Indian EV Industry Company Market Share

Indian EV Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Indian Electric Vehicle (EV) industry, encompassing market size, growth projections, competitive landscape, and key technological advancements from 2019 to 2033. It offers actionable insights for stakeholders, including manufacturers, investors, and policymakers. The report utilizes a robust methodology, incorporating historical data (2019-2024), a base year of 2025, and forecasts extending to 2033. All financial values are expressed in Millions.

Indian EV Industry Market Concentration & Innovation

This section analyzes the market concentration, innovation drivers, regulatory landscape, and competitive dynamics within the Indian EV industry. The study period covers 2019-2033, with 2025 serving as the base year and estimated year. The forecast period is 2025-2033, and the historical period encompasses 2019-2024.

The Indian EV market shows a moderate level of concentration, with a few major players holding significant market share, while numerous smaller players contribute to the overall growth. However, the market is rapidly evolving, driven by technological advancements and government initiatives. Innovation is fueled by increased R&D spending, collaborations between domestic and international companies, and a focus on developing cost-effective and localized EV technologies. The regulatory framework, while supportive, faces challenges in terms of standardization and infrastructure development. Product substitution from ICE vehicles to EVs is gaining momentum, influenced by factors such as rising fuel prices and environmental concerns. End-user trends reveal a growing preference for electric two-wheelers and passenger vehicles, particularly in urban areas. M&A activity has been relatively modest so far, but is expected to accelerate as larger players seek to consolidate their market positions and expand their portfolios.

- Market Share (2024): Tata Motors: xx%, Ola Electric: xx%, Hero Electric: xx%, Others: xx%

- M&A Deal Value (2019-2024): xx Million

Indian EV Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the Indian EV industry. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is projected at xx%. Market penetration is expected to increase significantly, driven by a combination of factors.

Government incentives and supportive policies have played a pivotal role in boosting EV adoption. Technological advancements, such as improved battery technology and charging infrastructure, have enhanced the practicality and affordability of EVs. Changing consumer preferences, influenced by environmental consciousness and the desire for cleaner transportation, are creating a strong demand for electric vehicles. Competitive dynamics are characterized by intense rivalry, both among established automakers and emerging EV startups. This competition is fostering innovation and driving down prices, further accelerating market growth.

Dominant Markets & Segments in Indian EV Industry

This section identifies the dominant markets and segments within the Indian EV industry.

Dominant Segments:

- Two-Wheelers: This segment dominates the Indian EV market due to its affordability, suitability for short commutes, and strong consumer demand. Key drivers include favorable government policies, expanding charging infrastructure in urban areas, and the increasing availability of affordable models.

- Passenger Vehicles: This segment is exhibiting strong growth potential, driven by the increasing availability of diverse EV models, technological advancements, and rising consumer awareness.

- Commercial Vehicles: The commercial vehicle segment is witnessing gradual adoption, driven by the economic benefits and environmental advantages. However, the high initial cost and range anxiety remain challenges.

- Fuel Category: HEV currently hold the largest market share due to existing infrastructure. However, the FCEV segment is expected to gain traction in future.

Key Drivers for Dominant Segments:

- Economic Policies: Government subsidies, tax benefits, and other financial incentives are crucial drivers.

- Infrastructure Development: The expansion of charging infrastructure is a critical factor enabling EV adoption.

- Technological Advancements: Improved battery technology, efficient motors, and innovative charging solutions are key growth enablers.

Indian EV Industry Product Developments

The Indian EV industry is witnessing rapid product innovation, driven by advancements in battery technology, motor design, and charging infrastructure. New models are constantly being introduced, offering improved range, faster charging times, and enhanced features. Competition is fierce, with companies focusing on delivering cost-effective and feature-rich vehicles to meet diverse consumer needs. The market is witnessing a trend towards localization of EV components and manufacturing, which reduces costs and dependence on imports.

Report Scope & Segmentation Analysis

This report segments the Indian EV market based on vehicle type (Two-Wheelers, Passenger Vehicles, Commercial Vehicles, Medium-duty Commercial Trucks), fuel category (FCEV, HEV), and others. Growth projections, market sizes, and competitive dynamics are analyzed for each segment.

- Two-Wheelers: This segment is projected to witness significant growth, driven by affordability and increasing consumer preference.

- Passenger Vehicles: This segment shows strong growth potential, driven by technological advancements and rising demand.

- Commercial Vehicles: This segment's growth will be driven by government initiatives promoting EV adoption in fleet operations.

- Medium-duty Commercial Trucks: This segment is expected to show gradual growth.

- Fuel Category (FCEV, HEV): HEV will have a significant market share initially, with FCEV showing gradual growth, particularly in niche applications.

Key Drivers of Indian EV Industry Growth

The Indian EV industry is experiencing rapid growth fueled by a confluence of factors: Government initiatives promoting EV adoption through subsidies and tax breaks are significantly stimulating demand. The falling prices of batteries and other EV components are making them more affordable for consumers. Technological advancements are continually improving the range, performance, and overall user experience of electric vehicles.

Challenges in the Indian EV Industry Sector

Despite its potential, the Indian EV industry faces significant challenges. Range anxiety, high initial purchase cost, limited charging infrastructure, and the development of a robust battery recycling system remain major obstacles. Supply chain disruptions, particularly related to battery materials, can significantly impact production and availability. The lack of awareness among consumers regarding EV benefits and technology also poses a challenge.

Emerging Opportunities in Indian EV Industry

The Indian EV industry presents several emerging opportunities. The growth of the charging infrastructure, technological breakthroughs in battery technology offering enhanced performance and longer ranges, and increasing consumer awareness are creating a favorable environment for market expansion. Focus on developing cost-effective solutions and adapting to the needs of the diverse Indian market will pave the way for success.

Leading Players in the Indian EV Industry Market

- Toyota Kirloskar Motor Pvt Ltd

- Ampere Vehicle Private Limited

- Hero Electric Vehicles Pvt Ltd

- Okinawa Autotech Pvt Ltd

- MG Motor India Private Limited

- Tata Motors Limited

- Olectra Greentech Ltd

- BYD India Private Limited

- TVS Motor Company Limited

- Mahindra & Mahindra Limited

- JBM Auto Limited

- Switch Mobility (Ashok Leyland Limited)

- Hyundai Motor India Limited

- Ola Electric Mobility Pvt Ltd

- Ather Energy Pvt Ltd

Key Developments in Indian EV Industry Industry

- August 2023: Ola Electric launched the S1X electric scooter at INR 79,999, offering two battery options (2 kWh and 3 kWh) with ranges of 91 km and 151 km, respectively.

- August 2023: Gabriel India Limited announced the development of components for Maruti Suzuki Jimny and Stellantis electric Citroen C3, highlighting its expansion into the EV component supply chain.

- August 2023: Hyundai Motor India Limited acquired assets from General Motors India’s Talegaon plant, expanding its manufacturing capabilities.

Strategic Outlook for Indian EV Industry Market

The Indian EV market is poised for exponential growth. Continued government support, technological advancements, and improving affordability will drive market expansion. Focus on developing robust charging infrastructure and addressing supply chain challenges will be crucial for realizing the full potential of this sector. The market presents significant opportunities for both established automakers and new entrants, fostering innovation and competition.

Indian EV Industry Segmentation

-

1. Vehicle Type

-

1.1. Commercial Vehicles

- 1.1.1. Buses

- 1.1.2. Heavy-duty Commercial Trucks

- 1.1.3. Light Commercial Pick-up Trucks

- 1.1.4. Light Commercial Vans

- 1.1.5. Medium-duty Commercial Trucks

-

1.2. Passenger Vehicles

- 1.2.1. Hatchback

- 1.2.2. Multi-purpose Vehicle

- 1.2.3. Sedan

- 1.2.4. Sports Utility Vehicle

- 1.3. Two-Wheelers

-

1.1. Commercial Vehicles

-

2. Fuel Category

- 2.1. FCEV

- 2.2. HEV

Indian EV Industry Segmentation By Geography

- 1. India

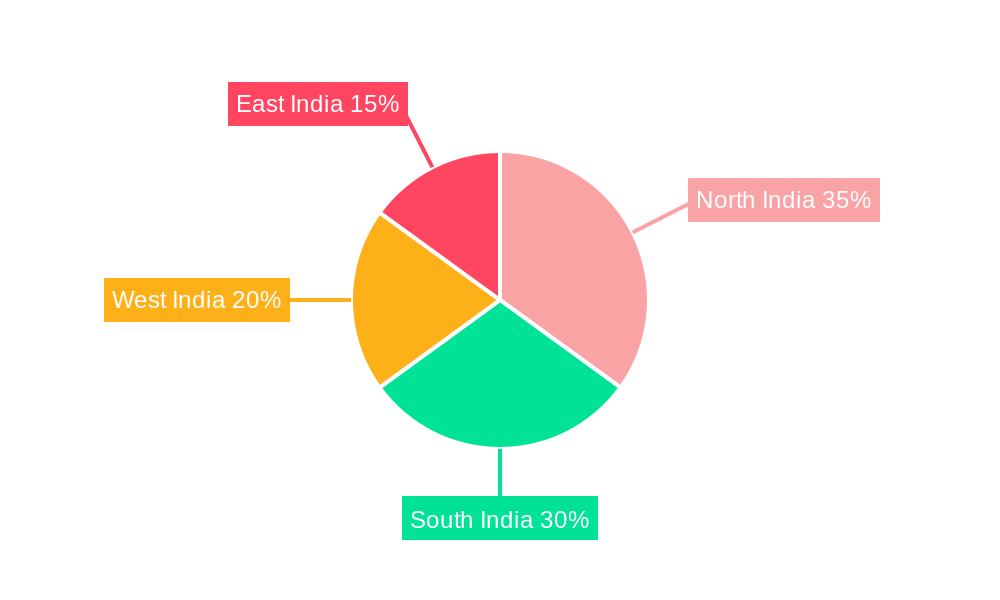

Indian EV Industry Regional Market Share

Geographic Coverage of Indian EV Industry

Indian EV Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 57.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Commercial Vehicles

- 5.1.1.1. Buses

- 5.1.1.2. Heavy-duty Commercial Trucks

- 5.1.1.3. Light Commercial Pick-up Trucks

- 5.1.1.4. Light Commercial Vans

- 5.1.1.5. Medium-duty Commercial Trucks

- 5.1.2. Passenger Vehicles

- 5.1.2.1. Hatchback

- 5.1.2.2. Multi-purpose Vehicle

- 5.1.2.3. Sedan

- 5.1.2.4. Sports Utility Vehicle

- 5.1.3. Two-Wheelers

- 5.1.1. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Fuel Category

- 5.2.1. FCEV

- 5.2.2. HEV

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Indian EV Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Commercial Vehicles

- 6.1.1.1. Buses

- 6.1.1.2. Heavy-duty Commercial Trucks

- 6.1.1.3. Light Commercial Pick-up Trucks

- 6.1.1.4. Light Commercial Vans

- 6.1.1.5. Medium-duty Commercial Trucks

- 6.1.2. Passenger Vehicles

- 6.1.2.1. Hatchback

- 6.1.2.2. Multi-purpose Vehicle

- 6.1.2.3. Sedan

- 6.1.2.4. Sports Utility Vehicle

- 6.1.3. Two-Wheelers

- 6.1.1. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Fuel Category

- 6.2.1. FCEV

- 6.2.2. HEV

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Toyota Kirloskar Motor Pvt Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Ampere Vehicle Private Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hero Electric Vehicles Pvt Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Okinawa Autotech Pvt Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 MG Motor India Private Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Tata Motors Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Olectra Greentech Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BYD India Private Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 TVS Motor Company Limite

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Mahindra & Mahindra Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 JBM Auto Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Switch Mobility (Ashok Leyland Limited)

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Hyundai Motor India Limited

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Ola Electric Mobility Pvt Ltd

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Ather Energy Pvt Ltd

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Toyota Kirloskar Motor Pvt Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian EV Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Indian EV Industry Share (%) by Company 2025

List of Tables

- Table 1: Indian EV Industry Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Indian EV Industry Revenue million Forecast, by Fuel Category 2020 & 2033

- Table 3: Indian EV Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Indian EV Industry Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 5: Indian EV Industry Revenue million Forecast, by Fuel Category 2020 & 2033

- Table 6: Indian EV Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian EV Industry?

The projected CAGR is approximately 57.23%.

2. Which companies are prominent players in the Indian EV Industry?

Key companies in the market include Toyota Kirloskar Motor Pvt Ltd, Ampere Vehicle Private Limited, Hero Electric Vehicles Pvt Ltd, Okinawa Autotech Pvt Ltd, MG Motor India Private Limited, Tata Motors Limited, Olectra Greentech Ltd, BYD India Private Limited, TVS Motor Company Limite, Mahindra & Mahindra Limited, JBM Auto Limited, Switch Mobility (Ashok Leyland Limited), Hyundai Motor India Limited, Ola Electric Mobility Pvt Ltd, Ather Energy Pvt Ltd.

3. What are the main segments of the Indian EV Industry?

The market segments include Vehicle Type, Fuel Category.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.3 million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Vehicle Electrification.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

The Cost of Raw Materials Used in the Manufacturing of Switches is High.

8. Can you provide examples of recent developments in the market?

August 2023: Ola Electric launched S1X for INR 79,999. Ola S1X will be offered in two battery capacities 2-kWh and 3-kWh. The 2-kWh variant will have a range of 91 km while the 3-kWh will have a 151 km range. The scooter has a 3.5-inch segmented display, the physical key unlocks and comes Without smart connectivity.August 2023: Gabriel India Limited (Gabriel India), a flagship company of Anand Group, announced that during the quarter that ended on June 30, 2023, it has developed components for Maruti Suzuki Jimny and Stellantis electric Citroen C3. At present it is developing parts for new models of VW, Tata, Stellantis, Mahindra, and Maruti Suzuki.August 2023: Hyundai Motor India Limited (HMIL) signed an asset purchase agreement (APA), in Gurugram, Haryana, for the acquisition and assignment of identified assets related to General Motors India (GMI)’s Talegaon Plant in Maharashtra.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian EV Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian EV Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian EV Industry?

To stay informed about further developments, trends, and reports in the Indian EV Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence