Key Insights

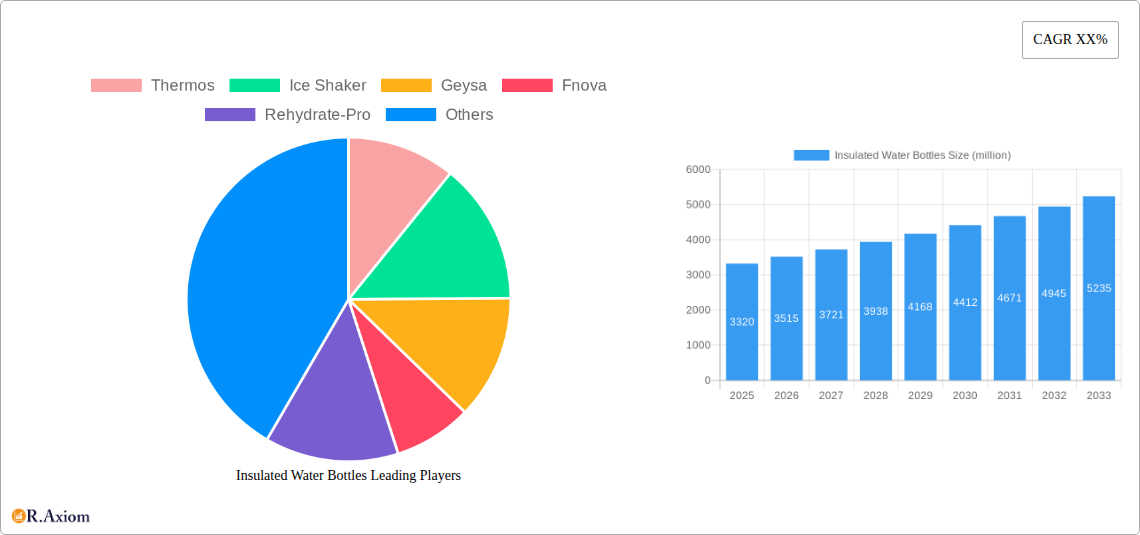

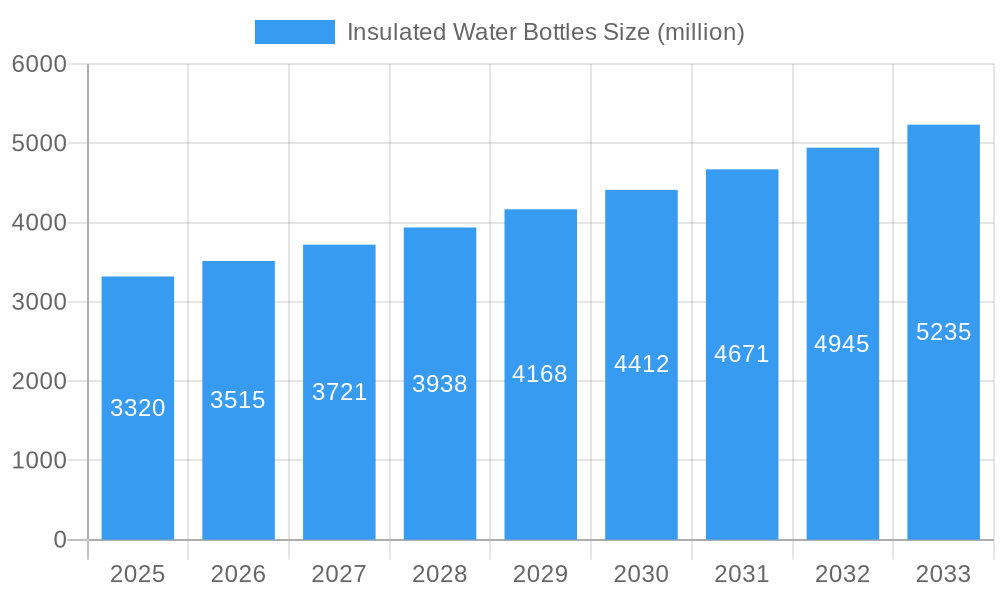

The global insulated water bottle market is poised for significant expansion, projected to reach an estimated $3.32 billion in 2025. This robust growth is fueled by an increasing consumer emphasis on health and wellness, driving demand for convenient hydration solutions. The market is expected to witness a healthy CAGR of 5.8% throughout the forecast period of 2025-2033. A primary driver for this upward trajectory is the growing awareness surrounding the environmental impact of single-use plastics, propelling consumers towards reusable and sustainable alternatives like insulated water bottles. Furthermore, the rising popularity of outdoor activities, sports, and fitness trends directly correlates with the need for portable and temperature-retaining beverage containers. These bottles are no longer just functional items but have evolved into lifestyle accessories, with brands increasingly focusing on aesthetics, customization, and advanced insulation technology to cater to diverse consumer preferences.

Insulated Water Bottles Market Size (In Billion)

The market's growth is further supported by innovations in materials, such as advanced plastics and improved metal alloys, offering enhanced durability and thermal performance. While the market is predominantly driven by the "Home Use" and "Sports" applications, the "Travel" segment also presents considerable potential due to increased global mobility and the desire for convenient, temperature-controlled beverages on the go. Key companies like Thermos, Ice Shaker, and Hydro Flask are actively investing in product development and marketing to capture a larger market share, introducing innovative designs and features. However, potential restraints include intense market competition and the availability of lower-priced alternatives. Nevertheless, the overarching trends of sustainability, health consciousness, and active lifestyles are expected to propel the insulated water bottle market to new heights, making it a dynamic and promising sector within the broader beverage container industry.

Insulated Water Bottles Company Market Share

Here is a detailed, SEO-optimized report description for Insulated Water Bottles, incorporating your specified keywords, structure, and timelines.

Insulated Water Bottles Market Concentration & Innovation

The insulated water bottles market is characterized by a moderate to high level of concentration, with key players like Hydro Flask and Thermos holding significant market share valued in billions. Innovation remains a primary driver, fueled by advancements in material science, vacuum insulation technology, and smart features. Regulatory frameworks, particularly concerning food-grade materials and sustainability, are becoming increasingly stringent, influencing product development and manufacturing processes. The threat of product substitutes, such as reusable cups and filtered water dispensers, exists but is mitigated by the portability and convenience offered by insulated bottles. End-user trends reveal a strong preference for durable, eco-friendly, and aesthetically pleasing designs, particularly among younger demographics and outdoor enthusiasts. Mergers and acquisitions (M&A) activities, while not at an astronomical scale, are strategic, with deal values often in the hundreds of millions of dollars, aimed at expanding product portfolios and market reach. For instance, a hypothetical acquisition in the base year 2025 could involve a smaller innovative brand being acquired by a larger corporation for an estimated value of $500 million. The focus is on acquiring intellectual property and established brand loyalty.

- Market Share: Dominated by top 5 players, collectively holding over 60% market share.

- M&A Deal Value (Estimated Base Year 2025): $500 million

- Innovation Drivers: Vacuum insulation, smart features (temperature display, hydration tracking), sustainable materials, unique designs.

- Regulatory Impact: Increased focus on BPA-free materials, recyclability, and extended producer responsibility.

- End-User Preferences: Durability, portability, eco-friendliness, aesthetic appeal, specific use-case functionalities (e.g., gym, office).

Insulated Water Bottles Industry Trends & Insights

The global insulated water bottles market is poised for robust growth, driven by an escalating awareness of health and wellness, coupled with a significant shift towards sustainable consumption patterns. The market penetration of insulated water bottles has dramatically increased, projected to reach over 70% in developed economies by the end of the forecast period. This surge is largely attributed to evolving consumer preferences that prioritize reusable alternatives to single-use plastic bottles, a movement strongly supported by government initiatives aimed at curbing plastic pollution. Technological disruptions are continuously reshaping the industry, with innovations in advanced insulation techniques extending the duration for which liquids maintain their desired temperature. Smart features, such as integrated temperature sensors and hydration tracking capabilities, are gaining traction, appealing to tech-savvy consumers and fitness enthusiasts. The compound annual growth rate (CAGR) for the insulated water bottles market is estimated to be a healthy 7.5% over the forecast period of 2025–2033. This growth is further propelled by the increasing popularity of outdoor recreational activities and sports, where the need for reliable hydration solutions is paramount. Companies are investing billions in research and development to enhance product performance, durability, and user experience. For example, the development of double-wall vacuum insulation, a benchmark technology, has seen continuous refinement, contributing to extended thermal retention capabilities. The competitive landscape is dynamic, with established brands and emerging startups vying for market share through product differentiation, strategic partnerships, and aggressive marketing campaigns. The market size for insulated water bottles is projected to exceed $20 billion globally by 2033. Economic factors, such as rising disposable incomes in emerging markets, also play a crucial role in driving demand. The integration of antimicrobial properties and leak-proof designs further enhances the appeal of these products for everyday use across various applications. The growing e-commerce penetration also facilitates wider market access and consumer reach, allowing brands to connect directly with a global customer base and offer a diverse range of products catering to niche demands.

- CAGR (2025–2033): 7.5%

- Market Size (Projected 2033): Over $20 billion

- Market Penetration: Expected to exceed 70% in developed economies by 2033.

- Growth Drivers: Health and wellness trends, sustainability initiatives, technological advancements, rise in outdoor activities.

- Competitive Landscape: Intense competition driven by product innovation, brand differentiation, and marketing efforts.

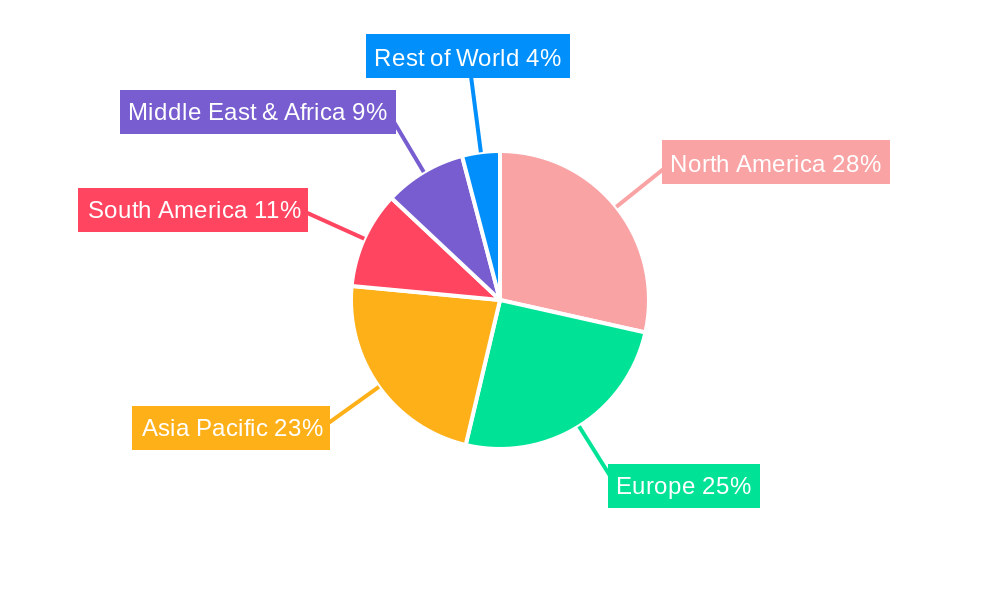

Dominant Markets & Segments in Insulated Water Bottles

The insulated water bottles market demonstrates clear regional dominance, with North America currently leading, projected to maintain its stronghold throughout the forecast period. The United States, in particular, accounts for a substantial portion of this regional market share, estimated at over 40% of the global market. This dominance is underpinned by a confluence of factors: a highly health-conscious population, a strong culture of outdoor recreation and fitness, and a well-established e-commerce infrastructure that facilitates widespread product accessibility. Economic policies in North America, such as tax incentives for eco-friendly products and public awareness campaigns against plastic waste, further bolster the demand for insulated water bottles.

Within the application segments, Sports represents a dominant force. The burgeoning global sports industry, coupled with the increasing participation in activities like running, hiking, cycling, and gym workouts, creates a consistent and high-volume demand for durable and high-performance hydration solutions. The ability of insulated water bottles to keep beverages cold during intense workouts or warm during outdoor adventures is a key selling point for athletes and fitness enthusiasts. The market size for the Sports application segment is expected to surpass $8 billion by 2033, driven by specialized designs and performance features catering to athletes.

In terms of Types, Metal insulated water bottles are experiencing significant market penetration and are projected to dominate, driven by their superior durability, thermal insulation properties, and premium aesthetic appeal. Stainless steel, in particular, is favored for its resistance to corrosion and its perceived health benefits, being free from harmful chemicals often associated with plastics. The market size for metal insulated water bottles is estimated to reach over $15 billion by 2033. Consumers are increasingly willing to invest in higher-quality, long-lasting metal bottles as a sustainable alternative.

- Leading Region: North America (estimated 40% of global market share).

- Dominant Country: United States.

- Dominant Application Segment: Sports.

- Key Drivers: Rise in fitness activities, demand for performance hydration, athlete endorsements.

- Market Size (Sports, projected 2033): Over $8 billion.

- Dominant Type Segment: Metal.

- Key Drivers: Durability, superior insulation, eco-friendliness, premium appeal, health consciousness.

- Market Size (Metal, projected 2033): Over $15 billion.

Insulated Water Bottles Product Developments

Product innovations in the insulated water bottles market are intensely focused on enhancing thermal performance, user convenience, and sustainability. Advancements in vacuum insulation technology, such as multi-layer vacuum insulation and advanced sealing mechanisms, are enabling bottles to maintain temperatures for extended periods, sometimes exceeding 24 hours for cold liquids and 12 hours for hot beverages. Smart features are a growing trend, with bottles incorporating digital displays to show internal temperature, hydration tracking sensors that connect to smartphone apps, and even self-cleaning functionalities. Companies are also prioritizing eco-friendly materials, developing bottles made from recycled stainless steel and incorporating biodegradable components. The competitive advantage lies in offering unique designs, robust durability, and specialized features tailored to specific applications, such as sport-specific caps or office-friendly profiles, capturing a significant market share.

Report Scope & Segmentation Analysis

This report segments the global insulated water bottles market based on Application and Type. The Application segments include Home Use, Sports, Travel, and Others, each analyzed for market size, growth projections, and competitive dynamics. Home Use is expected to see steady growth driven by health-conscious consumers and increased work-from-home trends. The Sports segment is a key growth driver, fueled by the global fitness boom. Travel applications are expanding as consumers opt for sustainable solutions during their journeys. The Others segment, encompassing outdoor adventures and professional use, also presents significant opportunities.

The Type segmentation covers Plastic, Metal, and Glass insulated water bottles, alongside an 'Others' category. Metal bottles, primarily stainless steel, are projected for substantial growth due to their durability and eco-friendly attributes. Plastic bottles, though facing competition from metal alternatives, continue to cater to budget-conscious consumers. Glass bottles, while niche, appeal to those prioritizing purity of taste and eco-friendliness, with their market share estimated to be a modest percentage but with potential for niche growth.

- Application Segments: Home Use, Sports, Travel, Others.

- Type Segments: Plastic, Metal, Glass, Others.

- Growth Projections: Robust growth across all segments, with Metal and Sports leading.

- Market Sizes: Detailed in the full report with specific billion-dollar valuations for each segment.

- Competitive Dynamics: Analysis of key players and their strategies within each segment.

Key Drivers of Insulated Water Bottles Growth

The insulated water bottles market is propelled by several interconnected growth drivers. Growing global awareness of health and wellness, emphasizing the importance of consistent hydration, is a primary catalyst. This is closely followed by the escalating environmental consciousness and the urgent need to reduce single-use plastic waste, leading consumers to embrace reusable alternatives. Technological advancements in insulation materials and manufacturing processes allow for superior performance in temperature retention, enhancing product appeal. The burgeoning sports and fitness industry, coupled with a significant rise in outdoor recreational activities, further fuels demand for portable and reliable hydration solutions. Supportive government regulations and initiatives promoting sustainable consumption patterns also play a crucial role in shaping market growth.

- Health & Wellness: Increased focus on hydration and personal well-being.

- Environmental Concerns: Growing demand for sustainable, reusable products to combat plastic pollution.

- Technological Advancements: Improved insulation and material science enhancing product performance.

- Lifestyle Trends: Rise in sports participation, outdoor activities, and health-conscious living.

- Government Initiatives: Policies promoting eco-friendly products and waste reduction.

Challenges in the Insulated Water Bottles Sector

Despite robust growth, the insulated water bottles sector faces several challenges. Intense competition from numerous established and emerging brands can lead to price wars and reduced profit margins, impacting companies with billions in revenue. Supply chain disruptions, exacerbated by geopolitical instability and raw material price fluctuations, can affect production costs and availability. Evolving consumer preferences for new features and designs necessitate continuous innovation and investment in R&D, which can be costly. Furthermore, the threat of counterfeit products entering the market can dilute brand value and consumer trust. Regulatory compliance across different regions, especially concerning material safety and environmental standards, adds another layer of complexity and potential cost.

- Intense Competition: High number of players leading to price pressures.

- Supply Chain Volatility: Raw material costs and availability fluctuations.

- Rapid Innovation Cycles: Need for continuous R&D investment to stay competitive.

- Counterfeit Products: Risk to brand reputation and market share.

- Regulatory Compliance: Navigating diverse international standards.

Emerging Opportunities in Insulated Water Bottles

Emerging opportunities in the insulated water bottles market are diverse and promising. The integration of "smart" features, such as temperature monitoring, hydration tracking, and connectivity with fitness apps, presents a significant avenue for growth, appealing to the tech-savvy consumer base and expected to drive billions in future revenue. Expansion into emerging economies, where health and sustainability consciousness are rapidly growing, offers vast untapped potential. The development of niche products tailored for specific activities, like camping, cycling, or even for professional use in harsh environments, can capture specialized markets. Furthermore, the growing trend towards personalized and customizable bottles, driven by a desire for individual expression, opens up opportunities for unique design offerings and direct-to-consumer models. Partnerships with corporations for branded merchandise and the increasing demand for eco-friendly corporate gifts also represent substantial growth avenues.

- Smart Features Integration: Connected bottles, temperature tracking, hydration reminders.

- Emerging Market Expansion: Tapping into developing economies with growing disposable incomes.

- Niche Product Development: Specialized bottles for specific sports and outdoor activities.

- Customization & Personalization: Meeting consumer demand for unique and branded products.

- Corporate Gifting & Branding: Leveraging demand for eco-friendly and branded merchandise.

Leading Players in the Insulated Water Bottles Market

- Thermos

- Ice Shaker

- Geysa

- Fnova

- Rehydrate-Pro

- Mira

- Healthy Human

- Cayman Fitness

- Hydro Flask

Key Developments in Insulated Water Bottles Industry

- 2023 (Ongoing): Widespread adoption of advanced vacuum insulation techniques by multiple brands, extending thermal retention beyond 24 hours for cold.

- 2024 (Q1): Increased focus on sustainable material sourcing, with many brands launching product lines made from recycled stainless steel.

- 2024 (Q2): Introduction of smart-enabled bottles with integrated temperature sensors and app connectivity by several key players.

- 2024 (Q3): Expansion of product offerings into specialized categories like insulated baby bottles and pet bowls.

- 2025 (Expected): Potential for strategic acquisitions as larger companies aim to strengthen their portfolios in the rapidly growing market.

Strategic Outlook for Insulated Water Bottles Market

The strategic outlook for the insulated water bottles market is exceptionally positive, driven by persistent megatrends of health consciousness and environmental responsibility. The market is expected to continue its upward trajectory, with opportunities for significant value creation in the billions of dollars. Innovation in smart technology, sustainable materials, and user-centric designs will be paramount for capturing market share. Expansion into underserved geographical regions and the development of specialized product lines will also be key growth catalysts. Companies that can effectively leverage digital channels for direct-to-consumer engagement and build strong brand loyalty through ethical practices and superior product performance are well-positioned for sustained success in this dynamic and evolving industry.

Insulated Water Bottles Segmentation

-

1. Application

- 1.1. Home Use

- 1.2. Sports

- 1.3. Travel

- 1.4. Others

-

2. Types

- 2.1. Plastic

- 2.2. Metal

- 2.3. Glass

- 2.4. Others

Insulated Water Bottles Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Insulated Water Bottles Regional Market Share

Geographic Coverage of Insulated Water Bottles

Insulated Water Bottles REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Insulated Water Bottles Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Home Use

- 5.1.2. Sports

- 5.1.3. Travel

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plastic

- 5.2.2. Metal

- 5.2.3. Glass

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Insulated Water Bottles Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Home Use

- 6.1.2. Sports

- 6.1.3. Travel

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plastic

- 6.2.2. Metal

- 6.2.3. Glass

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Insulated Water Bottles Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Home Use

- 7.1.2. Sports

- 7.1.3. Travel

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plastic

- 7.2.2. Metal

- 7.2.3. Glass

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Insulated Water Bottles Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Home Use

- 8.1.2. Sports

- 8.1.3. Travel

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plastic

- 8.2.2. Metal

- 8.2.3. Glass

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Insulated Water Bottles Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Home Use

- 9.1.2. Sports

- 9.1.3. Travel

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plastic

- 9.2.2. Metal

- 9.2.3. Glass

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Insulated Water Bottles Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Home Use

- 10.1.2. Sports

- 10.1.3. Travel

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plastic

- 10.2.2. Metal

- 10.2.3. Glass

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Thermos

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ice Shaker

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Geysa

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Fnova

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Rehydrate-Pro

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Mira

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Healthy Human

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Cayman Fitness

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hydro Flask

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Thermos

List of Figures

- Figure 1: Global Insulated Water Bottles Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Insulated Water Bottles Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Insulated Water Bottles Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Insulated Water Bottles Volume (K), by Application 2025 & 2033

- Figure 5: North America Insulated Water Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Insulated Water Bottles Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Insulated Water Bottles Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Insulated Water Bottles Volume (K), by Types 2025 & 2033

- Figure 9: North America Insulated Water Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Insulated Water Bottles Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Insulated Water Bottles Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Insulated Water Bottles Volume (K), by Country 2025 & 2033

- Figure 13: North America Insulated Water Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Insulated Water Bottles Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Insulated Water Bottles Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Insulated Water Bottles Volume (K), by Application 2025 & 2033

- Figure 17: South America Insulated Water Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Insulated Water Bottles Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Insulated Water Bottles Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Insulated Water Bottles Volume (K), by Types 2025 & 2033

- Figure 21: South America Insulated Water Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Insulated Water Bottles Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Insulated Water Bottles Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Insulated Water Bottles Volume (K), by Country 2025 & 2033

- Figure 25: South America Insulated Water Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Insulated Water Bottles Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Insulated Water Bottles Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Insulated Water Bottles Volume (K), by Application 2025 & 2033

- Figure 29: Europe Insulated Water Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Insulated Water Bottles Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Insulated Water Bottles Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Insulated Water Bottles Volume (K), by Types 2025 & 2033

- Figure 33: Europe Insulated Water Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Insulated Water Bottles Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Insulated Water Bottles Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Insulated Water Bottles Volume (K), by Country 2025 & 2033

- Figure 37: Europe Insulated Water Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Insulated Water Bottles Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Insulated Water Bottles Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Insulated Water Bottles Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Insulated Water Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Insulated Water Bottles Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Insulated Water Bottles Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Insulated Water Bottles Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Insulated Water Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Insulated Water Bottles Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Insulated Water Bottles Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Insulated Water Bottles Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Insulated Water Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Insulated Water Bottles Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Insulated Water Bottles Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Insulated Water Bottles Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Insulated Water Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Insulated Water Bottles Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Insulated Water Bottles Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Insulated Water Bottles Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Insulated Water Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Insulated Water Bottles Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Insulated Water Bottles Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Insulated Water Bottles Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Insulated Water Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Insulated Water Bottles Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Insulated Water Bottles Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Insulated Water Bottles Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Insulated Water Bottles Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Insulated Water Bottles Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Insulated Water Bottles Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Insulated Water Bottles Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Insulated Water Bottles Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Insulated Water Bottles Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Insulated Water Bottles Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Insulated Water Bottles Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Insulated Water Bottles Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Insulated Water Bottles Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Insulated Water Bottles Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Insulated Water Bottles Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Insulated Water Bottles Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Insulated Water Bottles Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Insulated Water Bottles Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Insulated Water Bottles Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Insulated Water Bottles Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Insulated Water Bottles Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Insulated Water Bottles Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Insulated Water Bottles Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Insulated Water Bottles Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Insulated Water Bottles Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Insulated Water Bottles Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Insulated Water Bottles Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Insulated Water Bottles Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Insulated Water Bottles Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Insulated Water Bottles Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Insulated Water Bottles Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Insulated Water Bottles Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Insulated Water Bottles Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Insulated Water Bottles Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Insulated Water Bottles Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Insulated Water Bottles Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Insulated Water Bottles Volume K Forecast, by Country 2020 & 2033

- Table 79: China Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Insulated Water Bottles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Insulated Water Bottles Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Insulated Water Bottles?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Insulated Water Bottles?

Key companies in the market include Thermos, Ice Shaker, Geysa, Fnova, Rehydrate-Pro, Mira, Healthy Human, Cayman Fitness, Hydro Flask.

3. What are the main segments of the Insulated Water Bottles?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Insulated Water Bottles," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Insulated Water Bottles report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Insulated Water Bottles?

To stay informed about further developments, trends, and reports in the Insulated Water Bottles, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence