Key Insights

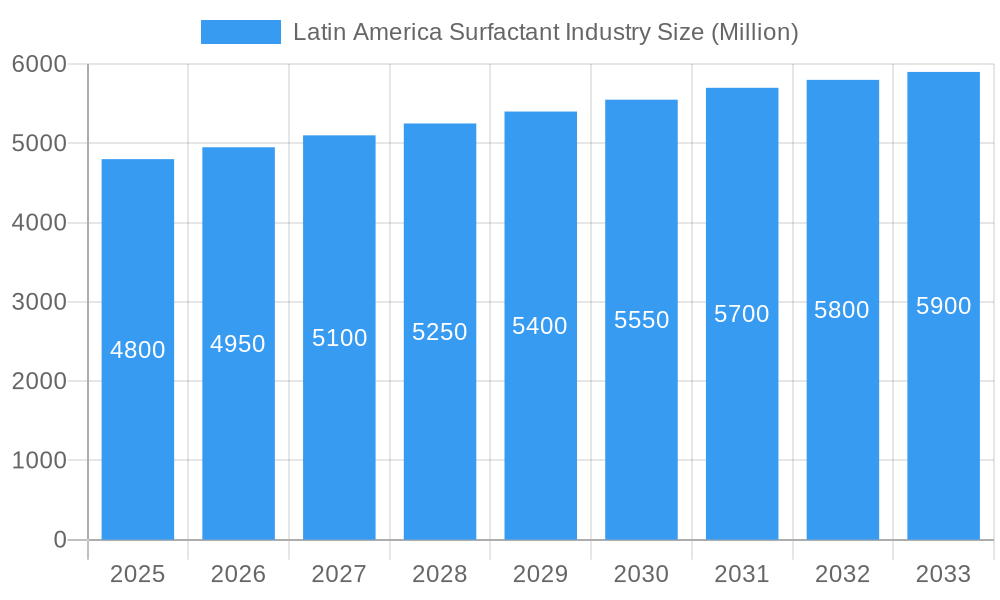

The Latin America Surfactant Industry is poised for significant expansion, driven by robust demand across diverse end-use sectors. Valued at 4139.4 million in 2025, the market is projected to grow at a CAGR of 5.1% during the forecast period of 2025-2033. This growth is primarily fueled by increasing disposable incomes and urbanization, which in turn boost consumption of household chemicals and personal care products. Rapid industrialization and expanding agricultural activities across the region further contribute to the demand for specialized surfactants in crop protection and industrial cleaning. The flourishing oil & gas sector, particularly in countries like Brazil and Mexico, also represents a substantial driver for demulsifying, wetting, and foaming agents essential in extraction and processing. Among product types, anionic and non-ionic surfactants are expected to maintain their dominant positions due to their widespread application in detergents, personal care, and industrial formulations, offering cost-effectiveness and versatile performance.

Latin America Surfactant Industry Market Size (In Billion)

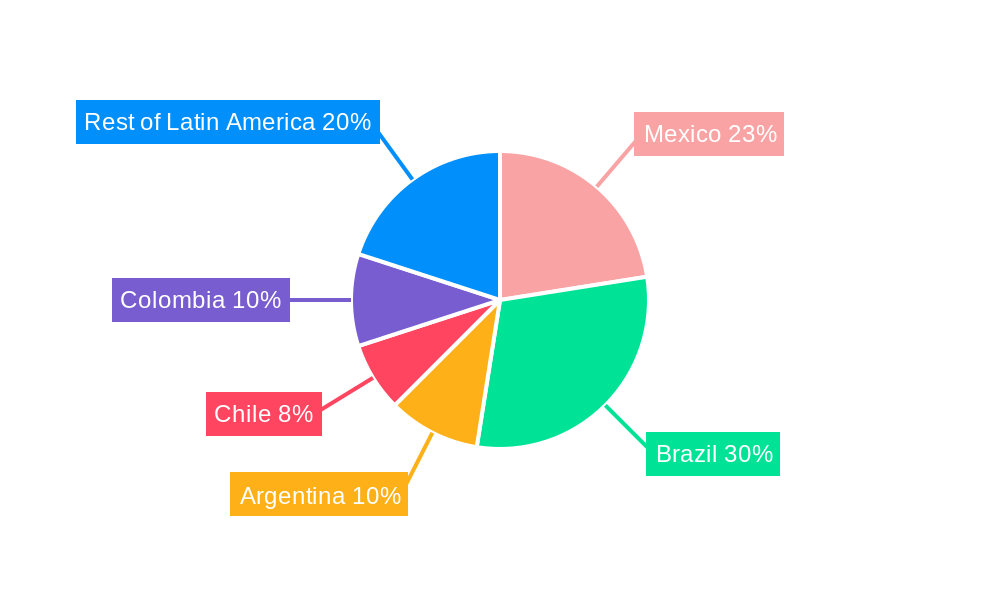

Key trends shaping the Latin American surfactant landscape include a growing emphasis on sustainability and the adoption of bio-based surfactants, driven by consumer preference for eco-friendly products and evolving regulatory frameworks. Manufacturers are increasingly investing in research and development to offer high-performance and specialty surfactants tailored to specific applications, such as enhanced emulsifiers for food processing or effective wetting agents for advanced agricultural formulations. Despite its promising outlook, the market faces challenges such as the volatility of raw material prices and the need to comply with increasingly stringent environmental regulations regarding biodegradability and toxicity. The competitive environment is characterized by the presence of global chemical giants and regional players, all vying for market share through product innovation, strategic partnerships, and expansion into high-growth segments like pharmaceuticals and specialty applications. Brazil and Mexico are anticipated to remain the leading markets, leveraging their strong industrial bases and large consumer populations.

Latin America Surfactant Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Latin America Surfactant Industry, offering critical insights into market dynamics, competitive landscapes, and future growth opportunities. Covering the Study Period 2019–2033, with a Base Year 2025, an Estimated Year 2025, a Forecast Period 2025–2033, and a Historical Period 2019–2024, this study is an essential resource for stakeholders seeking to navigate the evolving surfactant market in Latin America. Gain a strategic advantage with detailed segmentation, key developments, and projections for market expansion.

Latin America Surfactant Industry Market Concentration & Innovation

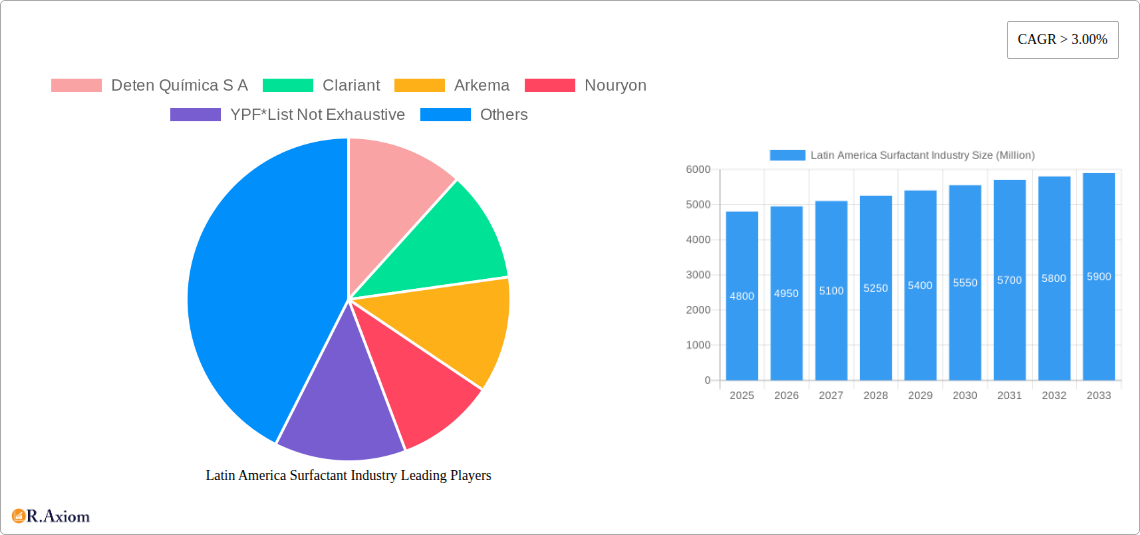

The Latin America Surfactant Industry exhibits a moderate to high level of market concentration, with leading global and regional players holding significant market share. The top three companies, including industry giants like BASF SE, Dow, and Solvay, collectively command approximately 35% of the market share, underscoring a competitive yet somewhat consolidated landscape. This concentration is particularly evident in segments requiring specialized chemistry and significant R&D investment, such as high-performance industrial surfactants and emerging biosurfactant technologies. Innovation is a primary driver within the market, fueled by increasing demand for sustainable, bio-based, and high-performance surfactant solutions across diverse end-user industries. Companies are heavily investing in green chemistry, developing novel products that offer improved environmental profiles and enhanced functional benefits, as demonstrated by recent advancements in APE-free polymerizable surfactants and glycolipid biosurfactants.

Regulatory frameworks across Latin American countries, though varying, increasingly lean towards stricter environmental compliance and product safety standards. This regulatory push encourages manufacturers to innovate, shifting towards readily biodegradable and less toxic alternatives. Product substitutes, while not directly threatening core surfactant functionalities, do influence market dynamics, especially in commodity segments where cost-effectiveness often dictates choice. However, the unique properties of surfactants in applications like emulsification, detergency, and wetting agents ensure their indispensability across industries. End-user trends significantly shape market concentration and innovation; for instance, the growing consumer preference for natural and organic personal care products directly stimulates innovation in milder, naturally derived surfactants. Similarly, the expanding oil & gas sector and agricultural practices demand specialized, high-performance surfactants tailored to specific regional conditions. Merger and acquisition (M&A) activities play a crucial role in consolidating market positions and acquiring new technologies or regional footholds. Over the historical period, M&A deals in the Latin America surfactant sector were valued at over 250 million, reflecting strategic efforts by larger players to expand product portfolios, enhance distribution networks, and leverage synergies. These activities often lead to increased market concentration in specific segments while also fostering innovation through the integration of acquired expertise and technologies. The drive for sustainability and performance continues to redefine market dynamics, pushing both large and smaller players to continuously innovate and adapt to evolving demands.

Latin America Surfactant Industry Industry Trends & Insights

The Latin America Surfactant Industry is on a robust growth trajectory, propelled by a confluence of market growth drivers, technological disruptions, evolving consumer preferences, and dynamic competitive landscapes. The market is projected to expand significantly, exhibiting a compound annual growth rate (CAGR) of 5.8% from 2025 to 2033, driven largely by burgeoning demand from household chemicals, personal care, and industrial applications. Urbanization across Latin America continues to fuel the household chemicals segment, as increased disposable incomes and growing populations translate into higher consumption of detergents, cleaning agents, and fabric softeners. The rising awareness regarding hygiene and sanitation further amplifies this demand.

Technological disruptions are a critical trend shaping the industry, with a strong emphasis on sustainability and bio-based solutions. The development of biosurfactants, derived from renewable resources and offering superior biodegradability, represents a significant shift. For instance, the penetration of biosurfactants in the overall surfactant market in Latin America is expected to reach 18% by 2033, indicating a substantial move away from traditional petroleum-based alternatives. Innovations in process technology, such as enzymatic synthesis and fermentation techniques, are making the production of these sustainable surfactants more economically viable and scalable. Furthermore, advances in polymerizable surfactants, like Solvay’s Reactsurf 2490, are enhancing product performance in critical applications such as exterior coatings and pressure-sensitive adhesives, offering improved functional and aesthetic benefits even in challenging conditions.

Consumer preferences are increasingly leaning towards products that are not only effective but also environmentally friendly and safe for human health. This sentiment drives demand for "green" surfactants, APE-free formulations, and ingredients free from harsh chemicals. The personal care segment, in particular, is highly responsive to these preferences, with consumers actively seeking shampoos, shower gels, and cosmetics formulated with natural and mild surfactants. This trend is compelling manufacturers to reformulate existing products and introduce new lines that align with these values, as exemplified by Clariant's Vita line of 100% bio-based surfactants and PEGs.

The competitive dynamics within the Latin America Surfactant Industry are characterized by intense rivalry among both multinational corporations and strong regional players. Companies like BASF SE, Dow, Solvay, and Clariant leverage their extensive R&D capabilities, global supply chains, and diverse product portfolios to maintain leadership. However, regional players such as Deten Química S.A. and YPF are carving out niches by offering localized solutions, competitive pricing, and strong distribution networks. Strategic collaborations, mergers, and acquisitions are common strategies employed to gain market share, access new technologies, and expand geographic reach. For example, acquisition of specialized biosurfactant manufacturers allows larger firms to quickly integrate sustainable offerings into their portfolios. The competitive landscape is also influenced by the fluctuating prices of raw materials, primarily petrochemicals and oleochemicals, compelling companies to optimize their supply chains and explore alternative feedstocks. Overall, the Latin America Surfactant Industry is poised for continued innovation and growth, driven by a blend of economic expansion, technological advancements towards sustainability, and evolving consumer demands for high-performance, eco-conscious products.

Dominant Markets & Segments in Latin America Surfactant Industry

Within the dynamic Latin America Surfactant Industry, the Anionic Surfactants segment under the Type category currently holds the dominant position, driven by their widespread and versatile applications across various end-user industries. Anionic surfactants, particularly linear alkylbenzene sulfonates (LAS) and alcohol ether sulfates (AES), are highly effective cleaning agents and foaming agents, making them indispensable in the production of household detergents, personal care products, and industrial cleaners. Their superior detergency and cost-effectiveness compared to other surfactant types ensure their continued market leadership.

- Economic Policies: Favorable economic policies promoting manufacturing and consumer goods production in countries like Brazil and Mexico directly boost the demand for anionic surfactants, which are core ingredients in these industries.

- Infrastructure Development: Robust infrastructure for chemical production and distribution supports the manufacturing and supply chain of anionic surfactants across the region.

- Raw Material Availability: Access to key petrochemical raw materials and oleochemicals, despite price fluctuations, underpins the production of traditional anionic surfactants.

- Consumer Penetration: High penetration of conventional detergents and cleaning products in Latin American households ensures a steady and substantial demand for anionic surfactants.

Following Type, the Detergents application segment is the largest consumer of surfactants in Latin America. The massive volume of detergents used in household laundry, dishwashing, and general cleaning ensures that this application segment continues to dominate. The growth of this segment is intrinsically linked to urbanization, increasing disposable incomes, and heightened awareness of hygiene standards across the region. As more households gain access to modern cleaning products, the demand for surfactants, predominantly anionic and non-ionic types, escalates.

In terms of End User Industry, Household Chemicals stands out as the most dominant segment. This encompasses a broad range of products including laundry detergents, dishwashing liquids, surface cleaners, and toilet cleaners. The consistent and high-volume consumption of these products by millions of households across Latin America ensures that this segment remains the primary driver of surfactant demand. The emphasis on health and hygiene, particularly post-pandemic, has further solidified the growth in this sector.

- Population Growth: A growing population across Latin America translates directly into increased demand for household cleaning products.

- Urbanization: Rapid urbanization leads to changes in lifestyles and a greater reliance on packaged cleaning solutions.

- Disposable Income: Rising disposable incomes enable consumers to purchase a wider variety of specialized household cleaning products.

- Hygiene Awareness: Enhanced public health awareness and promotion of hygiene practices significantly boost demand for disinfectants and cleaning agents.

Finally, regarding Sales Channel, Direct Sales and Distributors collectively form the dominant channel. Large surfactant manufacturers often engage in direct sales to major industrial clients and multinational consumer goods companies, leveraging long-term contracts and technical support. Distributors, on the other hand, play a crucial role in reaching smaller and medium-sized enterprises (SMEs) and ensuring market penetration across vast and diverse geographic regions within Latin America. The online sales channel is emerging but currently holds a smaller share, predominantly for specialized or niche surfactant products. The strategic importance of established distribution networks cannot be overstated in a region with varying logistical challenges and diverse market access requirements.

Latin America Surfactant Industry Product Developments

Product developments in the Latin America Surfactant Industry are significantly driven by the imperative for sustainability and enhanced performance. Recent innovations highlight a strong trend towards biosurfactants and APE-free alternatives. Solvay's November 2022 introduction of Reactsurf 2490, an APE-free polymerizable surfactant, exemplifies this by boosting performance in exterior coatings and pressure-sensitive adhesives, even at high temperatures, showcasing improved functional and aesthetic benefits. Furthermore, Solvay expanded its biosurfactant portfolio in June 2022 with Mirasoft SL L60 and Mirasoft SL A60, high-performance glycolipid biosurfactants derived from rapeseed oil and sugar. These innovations, with minimal environmental and carbon footprints, cater to the burgeoning sustainable beauty care market, finding applications in shampoos, conditioners, and facial washes. Complementing this, Clariant's February 2022 launch of the Vita line of 100% bio-based surfactants and polyethylene glycols (PEGs) directly addresses climate change by removing fossil carbon from the value chain, demonstrating a clear market fit for eco-conscious consumers and manufacturers seeking to reduce their environmental impact. These developments collectively underscore a shift towards advanced, environmentally friendly solutions that do not compromise on efficacy.

Report Scope & Segmentation Analysis

This comprehensive report meticulously segments the Latin America Surfactant Industry to provide granular insights. Under the Type segmentation, the market is analyzed across Amphoteric Surfactants, Anionic Surfactants, Cationic Surfactants, and Non-ionic Surfactants. Anionic surfactants currently dominate due to their widespread use in detergents, with the non-ionic segment projected to grow by 6.5% during the forecast period as demand for mild, environmentally friendly options increases. The Application segment includes Detergents, Emulsifying Agents, Foaming Agents, Dispersing Agents, Wetting Agents, Demulsifying Agents, and Antifoaming Agents, with detergents representing the largest application due to high consumer demand. The End User Industry covers Household Chemicals, Food Industry, Oil & Gas, Agriculture, Textile, and Pharmaceutical sectors, among others. The household chemicals segment is valued at an estimated 750 million in 2025, driven by urbanization and hygiene awareness, while oil & gas is a significant specialized consumer. Finally, the Sales Channel segment differentiates between Direct Sales, Distributors, and Online platforms, with distributors playing a critical role in regional market penetration. Each segment’s growth projections, market sizes, and competitive dynamics are detailed, offering a holistic view of the market landscape.

Key Drivers of Latin America Surfactant Industry Growth

The Latin America Surfactant Industry is primarily driven by escalating demand from diverse end-user industries, particularly household chemicals and personal care. Rapid urbanization and increasing disposable incomes across the region are boosting the consumption of cleaning products, detergents, and cosmetics, directly translating to higher surfactant demand. Technologically, the shift towards bio-based and sustainable surfactants, spurred by environmental regulations and consumer preferences, is a significant catalyst. Innovations like the development of glycolipid biosurfactants and APE-free formulations offer enhanced performance and reduced ecological footprints, attracting investments and expanding application areas. For example, Solvay’s new biosurfactants meet the growing consumer desire for sustainable beauty care products. Furthermore, robust growth in sectors such as agriculture and oil & gas, where specialized surfactants are crucial for emulsification, wetting, and demulsification processes, also contributes significantly to market expansion. The continuous evolution of regulatory frameworks advocating for greener chemicals incentivizes manufacturers to innovate and adopt more environmentally friendly production methods, thereby stimulating growth.

Challenges in the Latin America Surfactant Industry Sector

The Latin America Surfactant Industry faces several inherent challenges that could impede its growth trajectory. One significant barrier is the volatility of raw material prices, particularly for petrochemical derivatives and oleochemicals. Fluctuations in crude oil prices and agricultural feedstock costs directly impact production expenses, leading to unstable profit margins for manufacturers. Regulatory hurdles, although sometimes driving innovation towards sustainability, can also create complexities due to varying environmental standards and compliance requirements across different Latin American countries. This patchwork of regulations can increase operational costs and time for companies operating regionally. Supply chain issues, including logistical complexities, inadequate infrastructure in some remote areas, and trade barriers, pose challenges for efficient distribution and market access. For instance, transportation costs in certain landlocked regions can significantly inflate product prices. Intense competitive pressures from both large multinational corporations and numerous regional players further strain pricing power and market share, especially in commodity surfactant segments. The economic instability in some Latin American economies also translates into reduced consumer purchasing power, directly affecting demand for end-user products like household chemicals. These factors collectively require manufacturers to adopt agile strategies to maintain competitiveness and profitability.

Emerging Opportunities in Latin America Surfactant Industry

The Latin America Surfactant Industry is ripe with emerging opportunities, primarily driven by the escalating demand for sustainable and high-performance solutions. A significant opportunity lies in the burgeoning market for biosurfactants and green chemicals. Growing consumer awareness and stricter environmental regulations are accelerating the adoption of bio-based surfactants in personal care, household, and industrial applications, creating a lucrative niche for innovators. For instance, the demand for products like Solvay's Mirasoft SL biosurfactants for beauty care is rapidly expanding. Another key opportunity is the increasing investment in oil & gas exploration and production in countries like Brazil and Mexico, which fuels demand for specialized surfactants used in enhanced oil recovery (EOR), drilling fluids, and demulsification. The expanding agricultural sector also presents growth avenues, with a rising need for agricultural adjuvants that improve the efficacy of pesticides and fertilizers. Furthermore, the growth of the pharmaceutical and food processing industries across Latin America creates demand for high-purity, food-grade, and pharmaceutical-grade surfactants, offering premium market segments. Technological advancements in surfactant synthesis and formulation, particularly in functional surfactants for paints, coatings, and adhesives, also represent significant untapped potential for companies capable of delivering advanced solutions.

Leading Players in the Latin America Surfactant Industry Market

- 3M

- Arkema

- Ashland

- BASF SE

- Bayer AG

- Clariant

- Croda International Plc

- Deten Química S A

- Dow

- Evonik Industries AG

- Godrej Industries

- Innospec

- Kao Corporation

- Lonza

- Nouryon

- Indorama Ventures Public Company Limited

- P&G Chemicals

- Reliance Industries Ltd

- Solvay

- Stepan Company

- TENSAC

- YPF

- Others

Key Developments in Latin America Surfactant Industry Industry

- November 2022: Solvay introduced Reactsurf 2490, a novel APE-free polymerizable surfactant. This development enhances emulsion performance, offering improved functional and aesthetic benefits in exterior coatings and pressure-sensitive adhesives (PSAs), even at high temperatures, significantly impacting the performance chemicals segment.

- June 2022: Solvay launched Mirasoft SL L60 and Mirasoft SL A60, two novel high-performance biosurfactants. These glycolipid biosurfactants, based on rapeseed oil and sugar, boast minimal environmental and carbon footprints, catering to the growing demand for sustainable beauty care products like shampoos, conditioners, and face washes.

- February 2022: Clariant introduced their new Vita line of 100% bio-based surfactants and polyethylene glycols (PEGs). This initiative directly addresses climate change by removing fossil carbon from the value chain, marking a significant step towards fully bio-based chemical solutions and impacting sustainable ingredient sourcing.

Strategic Outlook for Latin America Surfactant Industry Market

The strategic outlook for the Latin America Surfactant Industry market is overwhelmingly positive, driven by persistent growth catalysts and evolving market demands. Future market potential is significant, with urbanization and increasing disposable incomes continuously fueling the demand for household chemicals, personal care products, and industrial cleaners across the region. Opportunities are particularly strong in the realm of sustainable chemistry, as regulatory pressures and consumer preferences push for bio-based, biodegradable, and eco-friendly surfactant solutions. Companies investing in research and development for novel biosurfactants and APE-free formulations will secure a competitive edge. Furthermore, the expansion of critical end-user sectors such as agriculture, oil & gas, and pharmaceuticals provides specialized high-value segments for tailored surfactant products. Strategic partnerships and targeted acquisitions will be crucial for market players to expand their technological capabilities, distribution networks, and regional footprint, capitalizing on the robust growth trajectory projected for the Latin America Surfactant Industry.

Latin America Surfactant Industry Segmentation

-

1. Type

- 1.1. Amphoteric Surfactants

- 1.2. Anionic Surfactants

- 1.3. Cationic Surfactants

- 1.4. Non-ionic Surfactants

-

2. Application

- 2.1. Detergents

- 2.2. Emulsify Agents

- 2.3. Foaming Agents

- 2.4. Dispersing Agents

- 2.5. Wetting Agents

- 2.6. Demulsifying Agents

- 2.7. Demulsifying Agents

- 2.8. Antifoaming Agents

- 2.9. Antistatic Agents

- 2.10. Others

-

3. End User Industry

- 3.1. Household Chemicals

- 3.2. Food Industry

- 3.3. Oil & Gas

- 3.4. Agriculture

- 3.5. Textile

- 3.6. Pharmaceutical

- 3.7. Others

-

4. Sales Channel

- 4.1. Direct Sales

- 4.2. Distributors

- 4.3. Online

- 4.4. Others

Latin America Surfactant Industry Segmentation By Geography

- 1. Mexico

- 2. Brazil

- 3. Argentina

- 4. Chile

- 5. Colombia

- 6. Rest of Latin America

Latin America Surfactant Industry Regional Market Share

Geographic Coverage of Latin America Surfactant Industry

Latin America Surfactant Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Amphoteric Surfactants

- 5.1.2. Anionic Surfactants

- 5.1.3. Cationic Surfactants

- 5.1.4. Non-ionic Surfactants

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Detergents

- 5.2.2. Emulsify Agents

- 5.2.3. Foaming Agents

- 5.2.4. Dispersing Agents

- 5.2.5. Wetting Agents

- 5.2.6. Demulsifying Agents

- 5.2.7. Demulsifying Agents

- 5.2.8. Antifoaming Agents

- 5.2.9. Antistatic Agents

- 5.2.10. Others

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. Household Chemicals

- 5.3.2. Food Industry

- 5.3.3. Oil & Gas

- 5.3.4. Agriculture

- 5.3.5. Textile

- 5.3.6. Pharmaceutical

- 5.3.7. Others

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. Direct Sales

- 5.4.2. Distributors

- 5.4.3. Online

- 5.4.4. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Mexico

- 5.5.2. Brazil

- 5.5.3. Argentina

- 5.5.4. Chile

- 5.5.5. Colombia

- 5.5.6. Rest of Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Latin America Surfactant Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Amphoteric Surfactants

- 6.1.2. Anionic Surfactants

- 6.1.3. Cationic Surfactants

- 6.1.4. Non-ionic Surfactants

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Detergents

- 6.2.2. Emulsify Agents

- 6.2.3. Foaming Agents

- 6.2.4. Dispersing Agents

- 6.2.5. Wetting Agents

- 6.2.6. Demulsifying Agents

- 6.2.7. Demulsifying Agents

- 6.2.8. Antifoaming Agents

- 6.2.9. Antistatic Agents

- 6.2.10. Others

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. Household Chemicals

- 6.3.2. Food Industry

- 6.3.3. Oil & Gas

- 6.3.4. Agriculture

- 6.3.5. Textile

- 6.3.6. Pharmaceutical

- 6.3.7. Others

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. Direct Sales

- 6.4.2. Distributors

- 6.4.3. Online

- 6.4.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Mexico Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Amphoteric Surfactants

- 7.1.2. Anionic Surfactants

- 7.1.3. Cationic Surfactants

- 7.1.4. Non-ionic Surfactants

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Detergents

- 7.2.2. Emulsify Agents

- 7.2.3. Foaming Agents

- 7.2.4. Dispersing Agents

- 7.2.5. Wetting Agents

- 7.2.6. Demulsifying Agents

- 7.2.7. Demulsifying Agents

- 7.2.8. Antifoaming Agents

- 7.2.9. Antistatic Agents

- 7.2.10. Others

- 7.3. Market Analysis, Insights and Forecast - by End User Industry

- 7.3.1. Household Chemicals

- 7.3.2. Food Industry

- 7.3.3. Oil & Gas

- 7.3.4. Agriculture

- 7.3.5. Textile

- 7.3.6. Pharmaceutical

- 7.3.7. Others

- 7.4. Market Analysis, Insights and Forecast - by Sales Channel

- 7.4.1. Direct Sales

- 7.4.2. Distributors

- 7.4.3. Online

- 7.4.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Brazil Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Amphoteric Surfactants

- 8.1.2. Anionic Surfactants

- 8.1.3. Cationic Surfactants

- 8.1.4. Non-ionic Surfactants

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Detergents

- 8.2.2. Emulsify Agents

- 8.2.3. Foaming Agents

- 8.2.4. Dispersing Agents

- 8.2.5. Wetting Agents

- 8.2.6. Demulsifying Agents

- 8.2.7. Demulsifying Agents

- 8.2.8. Antifoaming Agents

- 8.2.9. Antistatic Agents

- 8.2.10. Others

- 8.3. Market Analysis, Insights and Forecast - by End User Industry

- 8.3.1. Household Chemicals

- 8.3.2. Food Industry

- 8.3.3. Oil & Gas

- 8.3.4. Agriculture

- 8.3.5. Textile

- 8.3.6. Pharmaceutical

- 8.3.7. Others

- 8.4. Market Analysis, Insights and Forecast - by Sales Channel

- 8.4.1. Direct Sales

- 8.4.2. Distributors

- 8.4.3. Online

- 8.4.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Argentina Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Amphoteric Surfactants

- 9.1.2. Anionic Surfactants

- 9.1.3. Cationic Surfactants

- 9.1.4. Non-ionic Surfactants

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Detergents

- 9.2.2. Emulsify Agents

- 9.2.3. Foaming Agents

- 9.2.4. Dispersing Agents

- 9.2.5. Wetting Agents

- 9.2.6. Demulsifying Agents

- 9.2.7. Demulsifying Agents

- 9.2.8. Antifoaming Agents

- 9.2.9. Antistatic Agents

- 9.2.10. Others

- 9.3. Market Analysis, Insights and Forecast - by End User Industry

- 9.3.1. Household Chemicals

- 9.3.2. Food Industry

- 9.3.3. Oil & Gas

- 9.3.4. Agriculture

- 9.3.5. Textile

- 9.3.6. Pharmaceutical

- 9.3.7. Others

- 9.4. Market Analysis, Insights and Forecast - by Sales Channel

- 9.4.1. Direct Sales

- 9.4.2. Distributors

- 9.4.3. Online

- 9.4.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Chile Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Amphoteric Surfactants

- 10.1.2. Anionic Surfactants

- 10.1.3. Cationic Surfactants

- 10.1.4. Non-ionic Surfactants

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Detergents

- 10.2.2. Emulsify Agents

- 10.2.3. Foaming Agents

- 10.2.4. Dispersing Agents

- 10.2.5. Wetting Agents

- 10.2.6. Demulsifying Agents

- 10.2.7. Demulsifying Agents

- 10.2.8. Antifoaming Agents

- 10.2.9. Antistatic Agents

- 10.2.10. Others

- 10.3. Market Analysis, Insights and Forecast - by End User Industry

- 10.3.1. Household Chemicals

- 10.3.2. Food Industry

- 10.3.3. Oil & Gas

- 10.3.4. Agriculture

- 10.3.5. Textile

- 10.3.6. Pharmaceutical

- 10.3.7. Others

- 10.4. Market Analysis, Insights and Forecast - by Sales Channel

- 10.4.1. Direct Sales

- 10.4.2. Distributors

- 10.4.3. Online

- 10.4.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Colombia Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Amphoteric Surfactants

- 11.1.2. Anionic Surfactants

- 11.1.3. Cationic Surfactants

- 11.1.4. Non-ionic Surfactants

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Detergents

- 11.2.2. Emulsify Agents

- 11.2.3. Foaming Agents

- 11.2.4. Dispersing Agents

- 11.2.5. Wetting Agents

- 11.2.6. Demulsifying Agents

- 11.2.7. Demulsifying Agents

- 11.2.8. Antifoaming Agents

- 11.2.9. Antistatic Agents

- 11.2.10. Others

- 11.3. Market Analysis, Insights and Forecast - by End User Industry

- 11.3.1. Household Chemicals

- 11.3.2. Food Industry

- 11.3.3. Oil & Gas

- 11.3.4. Agriculture

- 11.3.5. Textile

- 11.3.6. Pharmaceutical

- 11.3.7. Others

- 11.4. Market Analysis, Insights and Forecast - by Sales Channel

- 11.4.1. Direct Sales

- 11.4.2. Distributors

- 11.4.3. Online

- 11.4.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Rest of Latin America Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Amphoteric Surfactants

- 12.1.2. Anionic Surfactants

- 12.1.3. Cationic Surfactants

- 12.1.4. Non-ionic Surfactants

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Detergents

- 12.2.2. Emulsify Agents

- 12.2.3. Foaming Agents

- 12.2.4. Dispersing Agents

- 12.2.5. Wetting Agents

- 12.2.6. Demulsifying Agents

- 12.2.7. Demulsifying Agents

- 12.2.8. Antifoaming Agents

- 12.2.9. Antistatic Agents

- 12.2.10. Others

- 12.3. Market Analysis, Insights and Forecast - by End User Industry

- 12.3.1. Household Chemicals

- 12.3.2. Food Industry

- 12.3.3. Oil & Gas

- 12.3.4. Agriculture

- 12.3.5. Textile

- 12.3.6. Pharmaceutical

- 12.3.7. Others

- 12.4. Market Analysis, Insights and Forecast - by Sales Channel

- 12.4.1. Direct Sales

- 12.4.2. Distributors

- 12.4.3. Online

- 12.4.4. Others

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 3M

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Arkema

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Ashland

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 BASF SE

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Bayer AG

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Clariant

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Croda International Plc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Deten Química S A

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Dow

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Evonik Industries AG

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Godrej Industries

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Innospec

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Kao Corporation

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Lonza

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Nouryon

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Indorama Ventures Public Company Limited

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 P&G Chemicals

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.18 Reliance Industries Ltd

- 13.1.18.1. Company Overview

- 13.1.18.2. Products

- 13.1.18.3. Company Financials

- 13.1.18.4. SWOT Analysis

- 13.1.19 Solvay

- 13.1.19.1. Company Overview

- 13.1.19.2. Products

- 13.1.19.3. Company Financials

- 13.1.19.4. SWOT Analysis

- 13.1.20 Stepan Company

- 13.1.20.1. Company Overview

- 13.1.20.2. Products

- 13.1.20.3. Company Financials

- 13.1.20.4. SWOT Analysis

- 13.1.21 TENSAC

- 13.1.21.1. Company Overview

- 13.1.21.2. Products

- 13.1.21.3. Company Financials

- 13.1.21.4. SWOT Analysis

- 13.1.22 YPF

- 13.1.22.1. Company Overview

- 13.1.22.2. Products

- 13.1.22.3. Company Financials

- 13.1.22.4. SWOT Analysis

- 13.1.23 Others

- 13.1.23.1. Company Overview

- 13.1.23.2. Products

- 13.1.23.3. Company Financials

- 13.1.23.4. SWOT Analysis

- 13.1.1 3M

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Latin America Surfactant Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Latin America Surfactant Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 3: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 4: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 5: Latin America Surfactant Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 7: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 9: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 10: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 11: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 13: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 14: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 15: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 16: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 17: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 18: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 19: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 20: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 23: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 24: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 25: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 26: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 27: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 28: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 29: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 30: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 32: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 33: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 34: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 35: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Surfactant Industry?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Latin America Surfactant Industry?

Key companies in the market include 3M, Arkema, Ashland, BASF SE, Bayer AG, Clariant, Croda International Plc, Deten Química S A, Dow, Evonik Industries AG, Godrej Industries, Innospec, Kao Corporation, Lonza, Nouryon, Indorama Ventures Public Company Limited, P&G Chemicals, Reliance Industries Ltd, Solvay, Stepan Company, TENSAC, YPF, Others.

3. What are the main segments of the Latin America Surfactant Industry?

The market segments include Type, Application, End User Industry, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Growing Personal Care and Home Care Industry in Latin America; The Growth of the Oleo Chemicals Market Driving Bio-based Surfactants.

6. What are the notable trends driving market growth?

Growing Demand from Household Soap and Detergent Application.

7. Are there any restraints impacting market growth?

Increasing Focus on Environmental Regulations; Other Restraints.

8. Can you provide examples of recent developments in the market?

November 2022: Solvay introduced Reactsurf 2490, a novel APE-free1 polymerizable surfactant developed as a major emulsifier for acrylic, vinyl-acrylic, and styrene-acrylic latex systems. In comparison to traditional surfactants, Reactsurf 2490 enhances emulsion performance to give improved functional and aesthetic benefits in exterior coatings and pressure-sensitive adhesives (PSAs), even at high temperatures.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Surfactant Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Surfactant Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Surfactant Industry?

To stay informed about further developments, trends, and reports in the Latin America Surfactant Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence