Key Insights

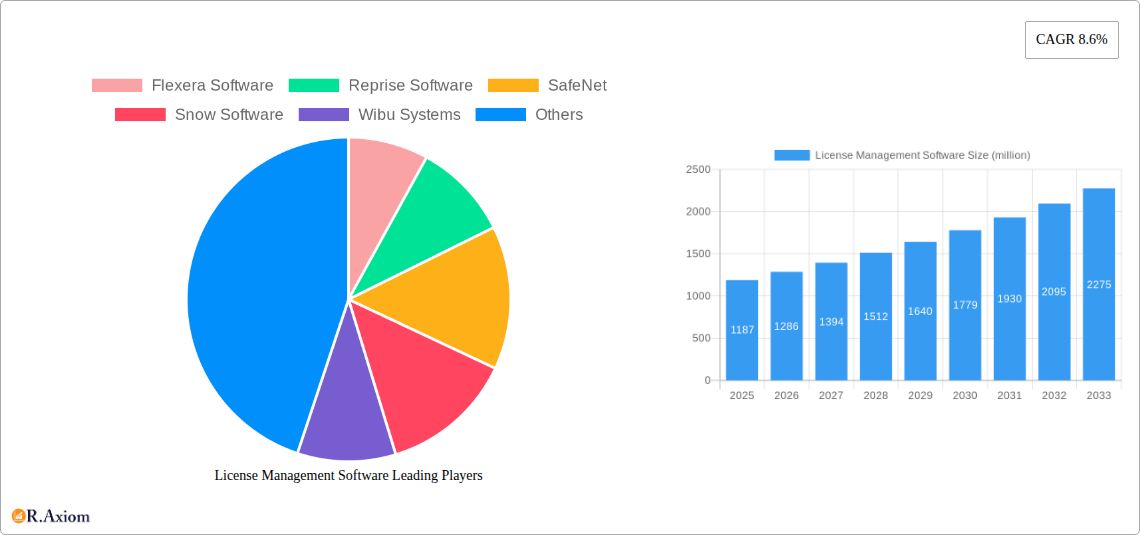

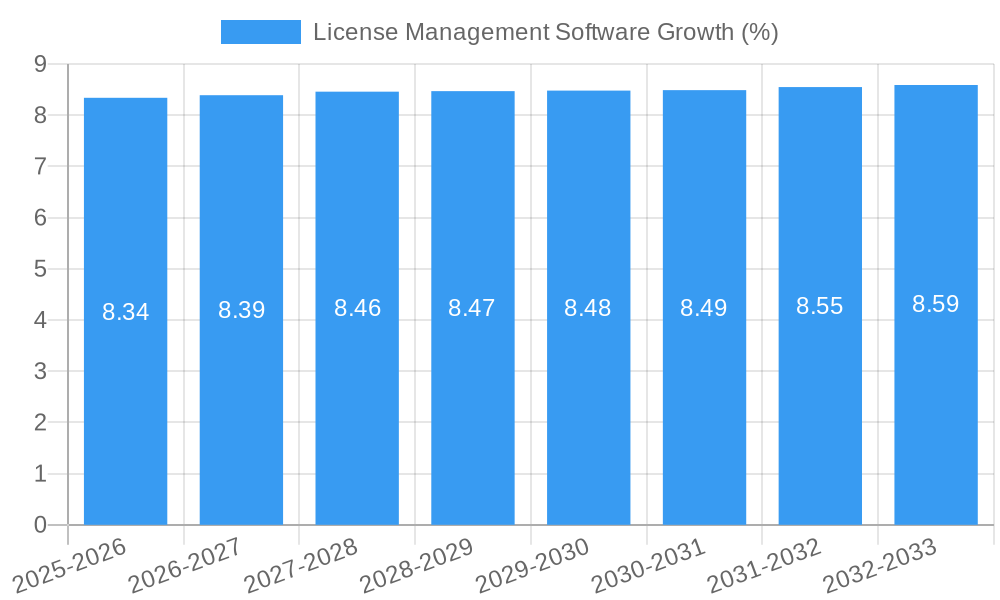

The global License Management Software market is poised for substantial expansion, projected to reach a market size of $1187 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 8.6% anticipated throughout the forecast period of 2025-2033. This significant growth is primarily propelled by the increasing complexity of software deployment across diverse industries and the growing need for efficient license optimization to control costs and ensure compliance. Businesses are actively seeking solutions that can automate license tracking, prevent over-licensing, and mitigate the risks associated with software audits. The escalating adoption of cloud-based services and the proliferation of SaaS applications further amplify the demand for sophisticated license management tools that can provide centralized control and visibility. Moreover, the rise in remote work models necessitates advanced license management to cater to dispersed workforces and ensure equitable software access, thereby driving market adoption.

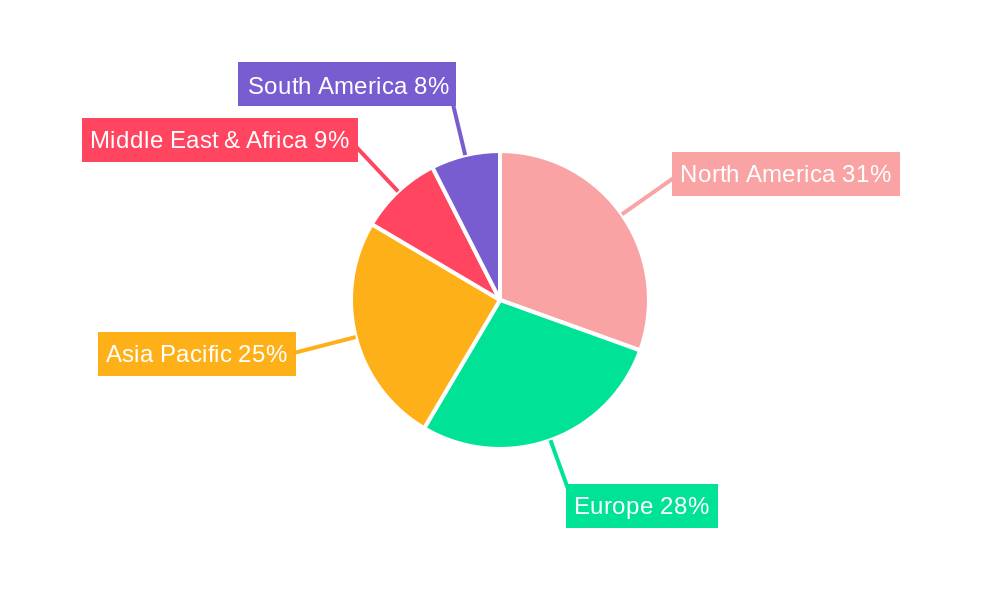

The market is segmented into key applications such as B2B Vendors, B2C Vendors, and Others, alongside a bifurcation in enforcement types: Hardware-based Enforcement and Software-based & Cloud-based Enforcement. The dominance of Software-based & Cloud-based Enforcement is expected to continue, owing to its scalability, flexibility, and cost-effectiveness. Major players like Flexera Software, Reprise Software, and Snow Software are at the forefront, offering innovative solutions that address the evolving needs of enterprises. Geographically, North America and Europe are anticipated to lead the market due to early adoption of software license management practices and strong regulatory frameworks. However, the Asia Pacific region is projected to exhibit the fastest growth, driven by rapid digital transformation, increasing software investments, and a burgeoning B2B and B2C vendor landscape eager to optimize their software assets. The market's trajectory indicates a clear shift towards smarter, automated, and cloud-integrated license management solutions that empower organizations to maximize their software investments.

License Management Software Market Concentration & Innovation

The global License Management Software market, valued at over X million in the historical period, exhibits a moderate concentration. Leading entities like Flexera Software and Snow Software hold significant market share, estimated at over 20% and 18% respectively. However, a dynamic ecosystem of mid-tier and emerging players, including Reprise Software, SafeNet, Wibu Systems, Inishtech, Moduslink, Pace Anti-Piracy, and Nalpeiron, contributes to a competitive landscape. Innovation is primarily driven by the escalating complexity of software licensing models, the rise of cloud-based deployments, and the imperative for robust intellectual property protection. Regulatory frameworks, such as GDPR and various software audit requirements, are shaping product development and mandating compliance features. Product substitutes, including manual tracking and custom-built solutions, are becoming less viable as the scale and sophistication of software usage grow, pushing organizations towards dedicated license management platforms. End-user trends highlight a strong demand for automated workflows, detailed usage analytics, and seamless integration with existing IT infrastructure. Merger and acquisition (M&A) activities are notable, with significant deal values over the past few years, signaling consolidation and strategic expansion by key players seeking to broaden their portfolios and customer reach. For instance, a major acquisition in 2023 valued at over X million aimed at integrating advanced analytics capabilities.

License Management Software Industry Trends & Insights

The License Management Software industry is poised for substantial growth, driven by an array of transformative trends. The projected Compound Annual Growth Rate (CAGR) for the forecast period of 2025–2033 is estimated at over 12%. This expansion is fueled by the increasing adoption of Software as a Service (SaaS) and the proliferation of hybrid cloud environments, which introduce intricate licensing complexities that necessitate sophisticated management solutions. Organizations are increasingly recognizing the financial implications of underutilized software assets and the risks associated with license non-compliance, leading to a heightened demand for effective license optimization. Technological disruptions, such as the integration of artificial intelligence (AI) and machine learning (ML) for predictive analytics and automated license compliance, are redefining market offerings. AI-powered tools can now identify license optimization opportunities with a precision previously unattainable, leading to significant cost savings estimated to be in the millions for large enterprises. Consumer preferences are shifting towards user-friendly interfaces, comprehensive reporting dashboards, and agile solutions that can adapt to evolving business needs. Competitive dynamics are characterized by intense innovation, with vendors differentiating themselves through specialized features, vertical-specific solutions, and enhanced security capabilities. Market penetration is expected to reach over 70% across major enterprises by 2030. The ongoing shift from perpetual licenses to subscription-based models further underscores the need for continuous and adaptive license management. The market is also witnessing a growing emphasis on vendor-agnostic solutions that can manage licenses across diverse software portfolios.

Dominant Markets & Segments in License Management Software

The License Management Software market's dominance is significantly influenced by regional economic policies, robust IT infrastructure, and the high adoption rates of digital technologies. North America, particularly the United States, currently holds the largest market share, estimated at over 35 million in 2025. This dominance is attributable to the presence of a large number of enterprises across various sectors, a strong emphasis on cybersecurity, and the early adoption of advanced software management solutions.

Within the Application segment, B2B Vendors represent the most dominant category, accounting for over 60% of the market.

- Key Drivers for B2B Vendor Dominance:

- High volume of software deployments in enterprise environments.

- Complex licensing agreements requiring professional management.

- Significant financial implications of license audits and non-compliance for businesses.

- The need for centralized control and visibility over software assets across multiple departments and users.

The Software-based & Cloud-based Enforcement Type segment is experiencing unparalleled growth and dominance, projected to capture over 75% of the market by 2033.

- Key Drivers for Software-based & Cloud-based Enforcement Dominance:

- Scalability and flexibility offered by cloud solutions to manage distributed software assets.

- Reduced hardware dependency and associated costs.

- Agility in responding to dynamic software usage patterns and remote work trends.

- Integration capabilities with cloud platforms like AWS, Azure, and Google Cloud.

- The increasing shift of software delivery and consumption models to cloud-based architectures.

Europe follows North America in market size, with Germany and the UK being key contributors. Asia Pacific, driven by countries like China and India, is emerging as a rapidly growing market due to the increasing digital transformation initiatives and the expanding IT sectors. The dominance within these regions is further solidified by government initiatives promoting digital adoption and stringent data protection regulations.

License Management Software Product Developments

Recent product developments in License Management Software are centered around enhancing automation, predictive analytics, and user experience. Innovations include AI-driven license optimization engines that can forecast future license needs, reducing over-provisioning and associated costs by millions. The integration of advanced metering capabilities for granular tracking of software usage across all devices and cloud environments is a key trend. Furthermore, vendors are focusing on robust reporting dashboards that provide actionable insights for IT and procurement teams, simplifying complex license compliance and audit readiness. Competitive advantages are increasingly derived from seamless integration with existing IT asset management (ITAM) and IT service management (ITSM) solutions, offering a holistic view of the software landscape.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global License Management Software market, segmented by Application and Type.

Application Segmentation:

- B2B Vendors: This segment encompasses organizations that purchase and manage software licenses for their internal business operations. Projected market size for this segment is over X million by 2033, driven by increasing enterprise software adoption and the need for compliance.

- B2C Vendors: This segment includes vendors who are themselves software providers and need to manage licenses for their end-user customers. While smaller than B2B, this segment is crucial for software monetization strategies, with projected growth of X million.

- Others: This residual segment includes various other use cases and niche applications of license management, contributing an estimated X million to the market.

Type Segmentation:

- Hardware-based Enforcement: This traditional method utilizes hardware keys or dongles for license protection. While still relevant for some specialized applications, its market share is gradually declining, with a projected market size of X million.

- Software-based & Cloud-based Enforcement: This modern approach leverages software agents, cloud platforms, and digital certificates for license management. This segment is the fastest-growing, expected to reach over X million by 2033 due to its scalability, flexibility, and integration capabilities.

Key Drivers of License Management Software Growth

The License Management Software market is propelled by several significant growth drivers. The escalating complexity of software licensing models, particularly with the rise of SaaS and hybrid cloud environments, necessitates sophisticated management tools to ensure compliance and cost-efficiency. The growing awareness of the financial risks associated with software license non-compliance, including hefty penalties and reputational damage, is a major impetus. Furthermore, the increasing adoption of IT asset management (ITAM) best practices, which emphasize optimizing software spend and maximizing ROI, directly benefits license management solutions. The ongoing digital transformation initiatives across industries, leading to greater software dependency, also contribute significantly to market expansion. For example, the shift to remote work has amplified the need for flexible and robust license management to cover dispersed workforces.

Challenges in the License Management Software Sector

Despite robust growth, the License Management Software sector faces certain challenges. The inherent complexity of many software vendor licensing agreements can be a significant hurdle, often requiring specialized expertise to interpret and implement correctly. Ensuring seamless integration with a diverse and ever-evolving landscape of IT systems and third-party applications can also be challenging. Furthermore, the cybersecurity threat landscape poses a constant challenge, requiring robust protection of license data and the enforcement mechanisms themselves. Competitive pressures from established players and emerging niche solutions can lead to pricing pressures and the need for continuous innovation to maintain market share. The initial investment cost for comprehensive license management solutions can also be a barrier for smaller organizations.

Emerging Opportunities in License Management Software

Emerging opportunities in the License Management Software market are abundant, driven by technological advancements and evolving business needs. The increasing adoption of AI and machine learning presents significant opportunities for developing more intelligent and automated license optimization and forecasting tools. The growing demand for integrated ITAM solutions, where license management plays a crucial role, opens avenues for vendors offering comprehensive platforms. The expansion of cloud-native applications and microservices architectures creates a need for specialized license management capabilities tailored to these modern development paradigms. Furthermore, the rise of the Internet of Things (IoT) and the increasing deployment of embedded software present new frontiers for license management strategies.

Leading Players in the License Management Software Market

- Flexera Software

- Reprise Software

- SafeNet

- Snow Software

- Wibu Systems

- Inishtech

- Moduslink

- Pace Anti-Piracy

- Nalpeiron

Key Developments in License Management Software Industry

- 2023 September: Flexera Software announced enhanced AI capabilities for its FlexNet Manager Suite, providing more predictive license optimization.

- 2023 March: Snow Software acquired a leading provider of cloud cost management solutions, expanding its cloud optimization offerings.

- 2022 December: SafeNet introduced a new cloud-based licensing platform designed for rapid deployment and scalability.

- 2022 August: Wibu Systems launched a new generation of their hardware-based protection technology, offering enhanced security for industrial IoT applications.

- 2021 October: Reprise Software unveiled a significant update to its license management platform, focusing on improved analytics for software vendors.

Strategic Outlook for License Management Software Market

The strategic outlook for the License Management Software market is highly promising, fueled by the indispensable role these solutions play in modern enterprise IT. Continued growth will be driven by the ongoing transition to cloud and hybrid IT infrastructures, the persistent need for cost optimization, and the ever-evolving regulatory landscape surrounding software usage. Vendors focusing on integrated ITAM, advanced analytics, AI-driven automation, and seamless cloud integration will be best positioned for success. The market is expected to see further consolidation and strategic partnerships as companies aim to offer comprehensive solutions that address the full spectrum of software lifecycle management. The increasing demand for security and compliance will continue to be a core growth catalyst.

License Management Software Segmentation

-

1. Application

- 1.1. B2B Vendors

- 1.2. B2C Vendors

- 1.3. Others

-

2. Type

- 2.1. Hardware-based Enforcement

- 2.2. Software-based & Cloud-based Enforcement

License Management Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

License Management Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.6% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global License Management Software Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. B2B Vendors

- 5.1.2. B2C Vendors

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hardware-based Enforcement

- 5.2.2. Software-based & Cloud-based Enforcement

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America License Management Software Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. B2B Vendors

- 6.1.2. B2C Vendors

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hardware-based Enforcement

- 6.2.2. Software-based & Cloud-based Enforcement

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America License Management Software Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. B2B Vendors

- 7.1.2. B2C Vendors

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Hardware-based Enforcement

- 7.2.2. Software-based & Cloud-based Enforcement

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe License Management Software Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. B2B Vendors

- 8.1.2. B2C Vendors

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Hardware-based Enforcement

- 8.2.2. Software-based & Cloud-based Enforcement

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa License Management Software Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. B2B Vendors

- 9.1.2. B2C Vendors

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Hardware-based Enforcement

- 9.2.2. Software-based & Cloud-based Enforcement

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific License Management Software Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. B2B Vendors

- 10.1.2. B2C Vendors

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Hardware-based Enforcement

- 10.2.2. Software-based & Cloud-based Enforcement

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Flexera Software

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Reprise Software

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SafeNet

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Snow Software

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Wibu Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Inishtech

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Moduslink

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Pace Anti-Piracy

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Nalpeiron

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Flexera Software

List of Figures

- Figure 1: Global License Management Software Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America License Management Software Revenue (million), by Application 2024 & 2032

- Figure 3: North America License Management Software Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America License Management Software Revenue (million), by Type 2024 & 2032

- Figure 5: North America License Management Software Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America License Management Software Revenue (million), by Country 2024 & 2032

- Figure 7: North America License Management Software Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America License Management Software Revenue (million), by Application 2024 & 2032

- Figure 9: South America License Management Software Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America License Management Software Revenue (million), by Type 2024 & 2032

- Figure 11: South America License Management Software Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America License Management Software Revenue (million), by Country 2024 & 2032

- Figure 13: South America License Management Software Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe License Management Software Revenue (million), by Application 2024 & 2032

- Figure 15: Europe License Management Software Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe License Management Software Revenue (million), by Type 2024 & 2032

- Figure 17: Europe License Management Software Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe License Management Software Revenue (million), by Country 2024 & 2032

- Figure 19: Europe License Management Software Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa License Management Software Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa License Management Software Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa License Management Software Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa License Management Software Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa License Management Software Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa License Management Software Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific License Management Software Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific License Management Software Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific License Management Software Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific License Management Software Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific License Management Software Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific License Management Software Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global License Management Software Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global License Management Software Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global License Management Software Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global License Management Software Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global License Management Software Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global License Management Software Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global License Management Software Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global License Management Software Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global License Management Software Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global License Management Software Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global License Management Software Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global License Management Software Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global License Management Software Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global License Management Software Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global License Management Software Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global License Management Software Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global License Management Software Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global License Management Software Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global License Management Software Revenue million Forecast, by Country 2019 & 2032

- Table 41: China License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania License Management Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific License Management Software Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the License Management Software?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the License Management Software?

Key companies in the market include Flexera Software, Reprise Software, SafeNet, Snow Software, Wibu Systems, Inishtech, Moduslink, Pace Anti-Piracy, Nalpeiron.

3. What are the main segments of the License Management Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1187 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "License Management Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the License Management Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the License Management Software?

To stay informed about further developments, trends, and reports in the License Management Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence