Key Insights

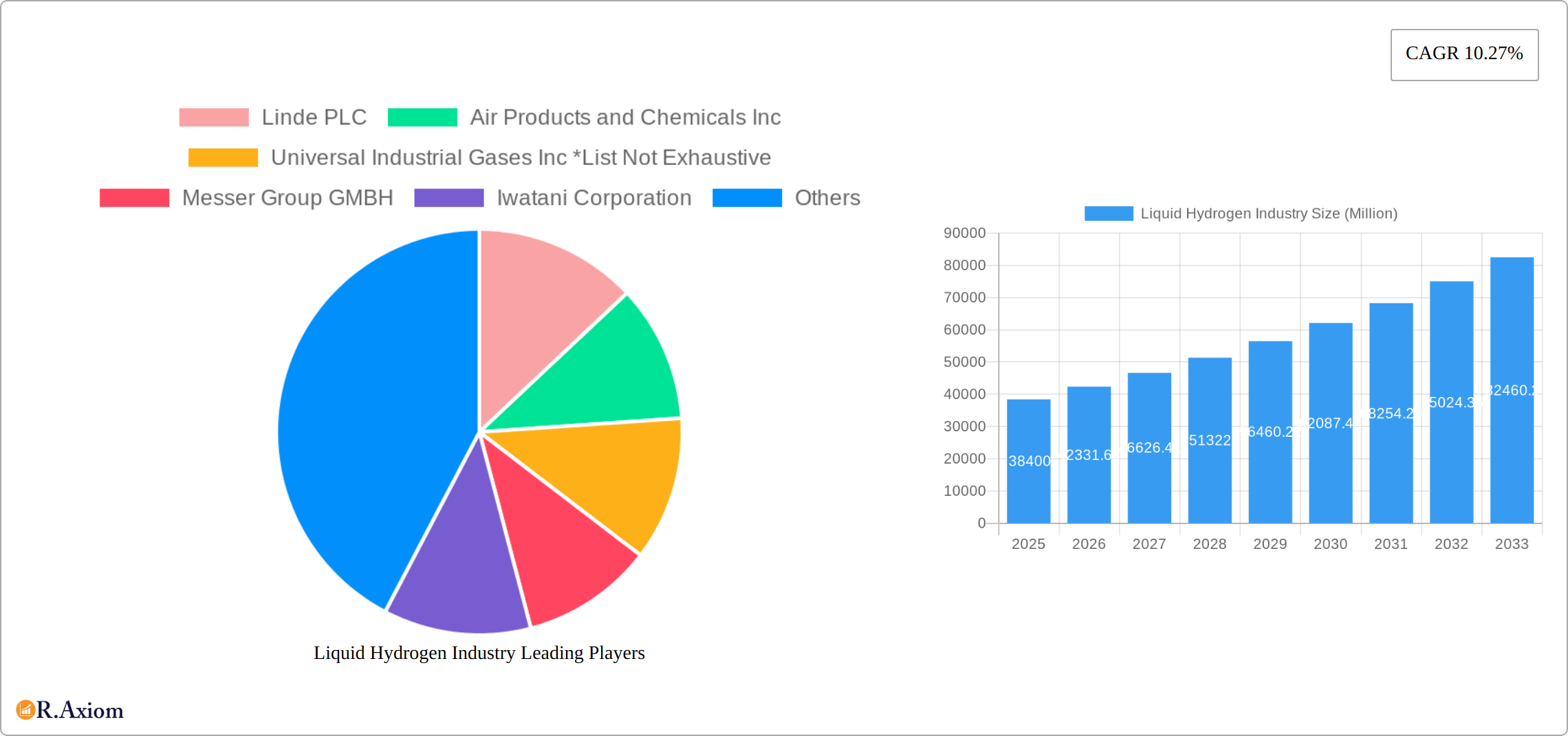

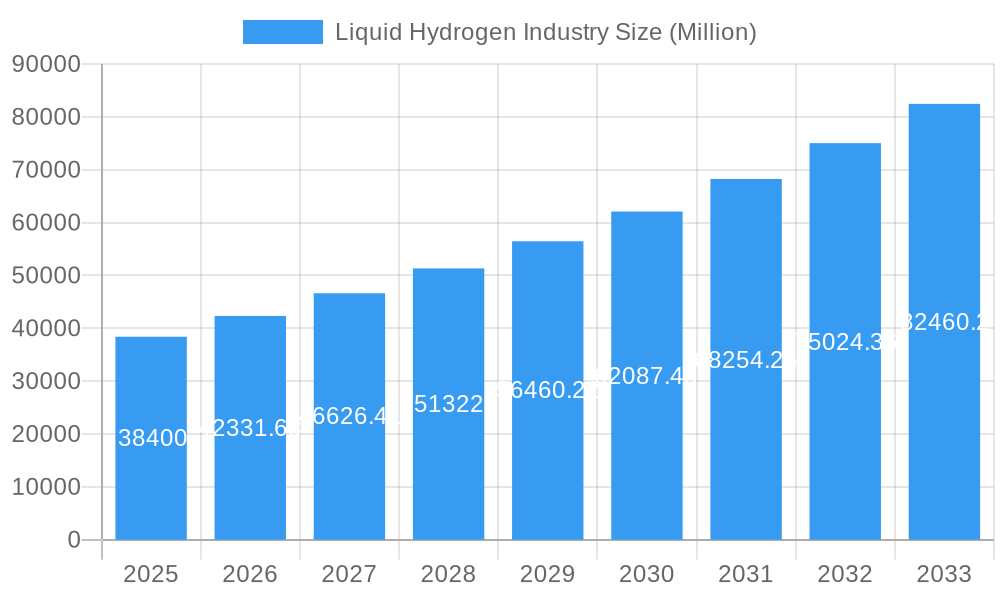

The liquid hydrogen market, valued at $38,400 million in 2025, is projected to experience robust growth, driven by the increasing adoption of hydrogen fuel cell technology across various sectors. A compound annual growth rate (CAGR) of 10.27% from 2025 to 2033 indicates a significant expansion of this market. Key drivers include the global push for decarbonization, stringent emission regulations, and the rising demand for clean energy solutions in transportation (automotive, aerospace, marine), industrial processes, and energy storage. The automotive sector, particularly in fuel cell electric vehicles (FCEVs), is expected to be a significant growth catalyst, alongside the burgeoning aerospace industry's exploration of hydrogen for propulsion and space exploration. Furthermore, advancements in cryogenic storage and transportation technologies, such as improved cryogenic tanks and high-pressure tube trailers, are streamlining the logistical challenges associated with handling liquid hydrogen, further stimulating market growth. However, the high cost of production and infrastructure development, coupled with safety concerns surrounding hydrogen handling, represent significant restraints. The market is segmented by distribution methods (cryogenic tanks, high-pressure tube trailers) and end-user industries. Geographically, North America and Asia-Pacific are likely to dominate the market due to robust government support for hydrogen initiatives and significant investments in renewable energy infrastructure. Competition amongst major players such as Linde PLC, Air Products and Chemicals Inc., and Air Liquide, fuels innovation and market expansion.

Liquid Hydrogen Industry Market Size (In Billion)

The forecast period of 2025-2033 anticipates a continuous upward trajectory for the liquid hydrogen market, fueled by ongoing technological advancements and supportive policies aimed at mitigating climate change. While challenges remain in terms of cost-effectiveness and safety, ongoing research and development efforts are addressing these issues. The diverse applications of liquid hydrogen across various sectors ensure continued demand, contributing to its anticipated rise as a crucial clean energy solution. The market's geographic distribution will likely reflect the pace of renewable energy adoption and the presence of supportive regulatory frameworks in different regions. Companies are actively investing in expanding production capacity, improving efficiency, and developing safer and more cost-effective hydrogen storage and transportation solutions. This competitive landscape and technological innovation should contribute to the market's substantial growth in the projected timeframe.

Liquid Hydrogen Industry Company Market Share

Liquid Hydrogen Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Liquid Hydrogen Industry, covering market size, growth drivers, key players, and future trends. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The forecast period is 2025-2033, and the historical period covers 2019-2024. The report is essential for industry stakeholders, investors, and anyone seeking to understand the dynamics of this rapidly evolving sector. Market values are expressed in Millions.

Liquid Hydrogen Industry Market Concentration & Innovation

The liquid hydrogen market exhibits a moderately concentrated structure, with several major players dominating the landscape. Linde PLC, Air Products and Chemicals Inc., Air Liquide, Messer Group GMBH, Iwatani Corporation, and Nippon Sanso Holdings Corporation control significant market share, estimated at xx% collectively in 2025. However, the emergence of smaller players like ITM Power and Universal Industrial Gases Inc., along with ongoing M&A activity, suggests a potential shift towards a more dynamic competitive environment. Innovation is driven by advancements in electrolysis technologies (PEM, Alkaline), cryogenic storage and transportation solutions, and the development of efficient liquefaction processes. Stringent environmental regulations globally, particularly concerning carbon emissions, are significant catalysts for innovation. Product substitutes, primarily natural gas and other fossil fuels, face increasing pressure due to sustainability concerns. End-user trends indicate a growing demand for green hydrogen across diverse sectors. M&A activity, while not exceedingly high in value terms (estimated at USD xx Million in 2024), plays a significant role in consolidating market share and accelerating technological development. Recent deals have focused on expanding production capacity, integrating the supply chain, and securing access to renewable energy sources.

- Market Share (2025): Linde PLC (xx%), Air Products (xx%), Air Liquide (xx%), Others (xx%)

- Estimated M&A Deal Value (2024): USD xx Million

Liquid Hydrogen Industry Industry Trends & Insights

The liquid hydrogen market is poised for robust growth, driven by the increasing global focus on decarbonization and the expanding adoption of hydrogen as a clean energy carrier. The compound annual growth rate (CAGR) is projected at xx% from 2025 to 2033, with market penetration increasing from xx% in 2025 to xx% by 2033, particularly within the automotive and aerospace sectors. Technological advancements in hydrogen production (e.g., improved electrolysis efficiency), storage (e.g., advanced cryogenic tanks), and transportation are key growth enablers. Consumer preferences are shifting towards cleaner energy solutions, fueling demand for liquid hydrogen-powered vehicles and industrial processes. Competitive dynamics are marked by intense rivalry among major players, focused on capacity expansion, strategic partnerships, and technological differentiation. Challenges such as hydrogen's high production and storage costs, along with infrastructural limitations, remain significant hurdles.

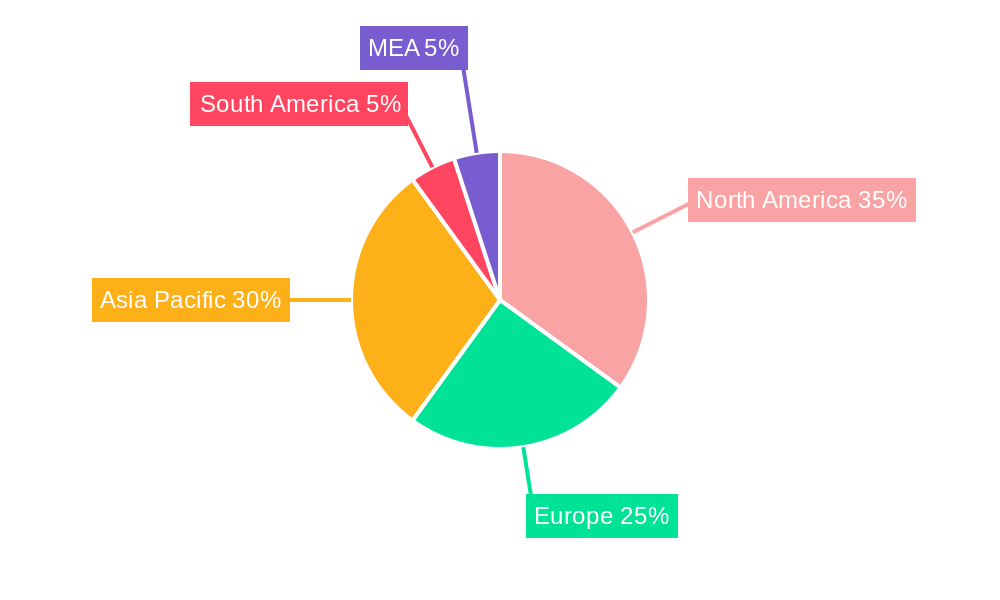

Dominant Markets & Segments in Liquid Hydrogen Industry

The Asia-Pacific region is currently the dominant market for liquid hydrogen, driven by substantial investments from governments and rapid industrial growth in countries like Japan, South Korea, and China. Significant economic policies supporting hydrogen development, coupled with substantial infrastructure development, bolster this dominance. Within segments:

Distribution: Cryogenic tanks currently hold a larger market share than high-pressure tube trailers due to their established infrastructure and greater storage capacity. However, high-pressure tube trailers are expected to experience faster growth due to their better suitability for long-distance transportation.

End-User Industry: The automotive sector is projected to witness the most significant growth, driven by increasing adoption of fuel-cell electric vehicles (FCEVs). The aerospace sector, particularly for outer space applications, presents a significant, albeit smaller, market segment due to the high energy density of liquid hydrogen. The marine sector is emerging as a promising area, with initiatives like the Iwatani Corporation project aiming to reduce transportation costs.

Key Drivers in Asia-Pacific:

- Government subsidies and incentives

- Strong industrial demand

- Investments in hydrogen infrastructure

Liquid Hydrogen Industry Product Developments

Recent innovations are significantly enhancing the efficiency and cost-effectiveness of the entire liquid hydrogen value chain, from production to transportation and storage. These advancements include breakthroughs in electrolysis technologies, resulting in higher yields and lower energy consumption; the development of more efficient and durable cryogenic tanks with increased storage capacity and reduced boil-off rates; and the design of lightweight, high-pressure tube trailers optimized for safe and cost-effective long-distance transport. These technological leaps are crucial for expanding liquid hydrogen's market reach and establishing it as a truly competitive and commercially viable alternative to fossil fuels. The overarching goal is to substantially reduce the overall cost of liquid hydrogen production while simultaneously increasing its energy density to streamline transportation and storage logistics. The industry's competitiveness hinges on sustained technological leadership, relentless cost optimization, and the establishment of robust and resilient supply chains. This includes addressing challenges related to materials sourcing, manufacturing processes, and logistics infrastructure.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation of the liquid hydrogen market, analyzing it across key distribution methods – cryogenic tanks and high-pressure tube trailers – and major end-user industries, including automotive, aerospace (with a particular focus on space applications), marine, and others. Each segment undergoes detailed scrutiny, examining its current market size, projected growth trajectories, and the prevailing competitive landscape. While cryogenic tanks are anticipated to maintain a considerable market share, leveraging their existing infrastructure and suitability for large-volume handling, high-pressure tube trailers are projected to demonstrate faster growth due to their inherent advantages in transportation efficiency and flexibility. The automotive industry is predicted to be the fastest-growing end-user segment, reflecting the accelerating adoption of hydrogen fuel cell vehicles. Simultaneously, strong growth is also anticipated in the aerospace sector, especially in space exploration and propulsion systems, and within the marine industry for applications such as powering vessels and reducing emissions.

Key Drivers of Liquid Hydrogen Industry Growth

The burgeoning liquid hydrogen industry is propelled by a confluence of powerful factors. Stringent government regulations designed to curb greenhouse gas emissions are forcing industries to adopt cleaner, more sustainable energy alternatives. This regulatory pressure is complemented by remarkable technological advancements in hydrogen production, storage, and transportation, making liquid hydrogen a progressively more viable and attractive option. Significant investments from both the public and private sectors are further accelerating infrastructure development and commercialization efforts, fostering a supportive environment for market expansion. Finally, the steadily increasing demand from diverse end-user industries, particularly the automotive and aerospace sectors, is creating a strong market pull, driving the adoption of liquid hydrogen at an accelerated pace. This increasing demand is fueled by both environmental concerns and the desire for improved performance and efficiency in various applications.

Challenges in the Liquid Hydrogen Industry Sector

Significant challenges impede the widespread adoption of liquid hydrogen. The high cost of production and infrastructure development remains a major barrier. The energy-intensive nature of liquefaction processes and the need for specialized cryogenic infrastructure increase costs. Supply chain complexities, including hydrogen transportation and storage, pose logistical challenges. The competitive landscape, with established players and new entrants, introduces significant competitive pressures. Regulatory frameworks and safety standards also vary across regions, creating inconsistencies.

Emerging Opportunities in Liquid Hydrogen Industry

Emerging opportunities abound in the liquid hydrogen industry. The burgeoning green hydrogen sector, powered by renewable energy sources, presents substantial growth potential. The development of innovative storage solutions, such as solid-state hydrogen storage, offers prospects for improved efficiency and safety. Expansion into new end-user sectors, such as energy storage and power generation, holds significant promise. Finally, strategic partnerships and collaborations among industry players can accelerate innovation and commercialization.

Leading Players in the Liquid Hydrogen Industry Market

- Linde PLC

- Air Products and Chemicals Inc

- Universal Industrial Gases Inc

- Messer Group GMBH

- Iwatani Corporation

- Air Liquide

- Nippon Sanso Holdings Corporation

- Praxair Technology Inc.

- ITM Power

Key Developments in Liquid Hydrogen Industry Industry

March 2023: Iwatani Corporation and ENEOS Corporation launched a "Liquefied Hydrogen Supply Chain Commercialization Demonstration Project," aiming to reduce hydrogen supply costs to 30 JPY/Nm3 by 2030 through marine transportation advancements. This signifies a crucial step towards cost-competitive hydrogen transport.

September 2022: Linde announced the construction of a 35-megawatt PEM electrolyzer in Niagara Falls, New York, significantly expanding its green liquid hydrogen production capacity in the US. This demonstrates significant investment in green hydrogen production capacity.

May 2022: Air Liquide invested USD 250 Million in a large liquid hydrogen production and logistics complex in Nevada, capable of producing 30 tons daily. This highlights the strategic investment in large-scale production capacity to meet growing demand in the hydrogen mobility sector.

Strategic Outlook for Liquid Hydrogen Industry Market

The liquid hydrogen market is poised for exceptional growth, driven by the global imperative to decarbonize economies and the continuous advancements in hydrogen technologies. Sustained investment in green hydrogen production methods, coupled with the parallel development of supporting infrastructure and ongoing cost reductions, will act as key catalysts for market expansion. The diversification of liquid hydrogen applications across transportation, industrial processes, and energy storage will further accelerate market growth. The strategic focus for industry leaders must be on building highly efficient and sustainable supply chains, improving storage technologies to minimize losses and maximize efficiency, and creating a supportive and well-defined regulatory environment to foster innovation and growth within the sector. Collaboration across industry stakeholders will be crucial to address technical challenges and ensure market readiness.

Liquid Hydrogen Industry Segmentation

-

1. Distribution

- 1.1. Cryogenic Tank

- 1.2. High-Pressure Tube Trailers

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Aerospace (including Outer Space)

- 2.3. Marine

- 2.4. Other End-User Industries

Liquid Hydrogen Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Liquid Hydrogen Industry Regional Market Share

Geographic Coverage of Liquid Hydrogen Industry

Liquid Hydrogen Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.27% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Distribution

- 5.1.1. Cryogenic Tank

- 5.1.2. High-Pressure Tube Trailers

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Aerospace (including Outer Space)

- 5.2.3. Marine

- 5.2.4. Other End-User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Distribution

- 6. Global Liquid Hydrogen Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Distribution

- 6.1.1. Cryogenic Tank

- 6.1.2. High-Pressure Tube Trailers

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Automotive

- 6.2.2. Aerospace (including Outer Space)

- 6.2.3. Marine

- 6.2.4. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Distribution

- 7. Asia Pacific Liquid Hydrogen Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Distribution

- 7.1.1. Cryogenic Tank

- 7.1.2. High-Pressure Tube Trailers

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Automotive

- 7.2.2. Aerospace (including Outer Space)

- 7.2.3. Marine

- 7.2.4. Other End-User Industries

- 7.1. Market Analysis, Insights and Forecast - by Distribution

- 8. North America Liquid Hydrogen Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Distribution

- 8.1.1. Cryogenic Tank

- 8.1.2. High-Pressure Tube Trailers

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Automotive

- 8.2.2. Aerospace (including Outer Space)

- 8.2.3. Marine

- 8.2.4. Other End-User Industries

- 8.1. Market Analysis, Insights and Forecast - by Distribution

- 9. Europe Liquid Hydrogen Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Distribution

- 9.1.1. Cryogenic Tank

- 9.1.2. High-Pressure Tube Trailers

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Automotive

- 9.2.2. Aerospace (including Outer Space)

- 9.2.3. Marine

- 9.2.4. Other End-User Industries

- 9.1. Market Analysis, Insights and Forecast - by Distribution

- 10. Rest of the World Liquid Hydrogen Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Distribution

- 10.1.1. Cryogenic Tank

- 10.1.2. High-Pressure Tube Trailers

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Automotive

- 10.2.2. Aerospace (including Outer Space)

- 10.2.3. Marine

- 10.2.4. Other End-User Industries

- 10.1. Market Analysis, Insights and Forecast - by Distribution

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Linde PLC

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Air Products and Chemicals Inc

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Universal Industrial Gases Inc *List Not Exhaustive

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Messer Group GMBH

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Iwatani Corporation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Air Liquide

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Nippon Sanso Holdings Corporation

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Nippon Sanso Holdings Corporation

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Praxair Technology Inc.

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 ITM Power

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Linde PLC

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Liquid Hydrogen Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Liquid Hydrogen Industry Volume Breakdown (kilotons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Liquid Hydrogen Industry Revenue (Million), by Distribution 2025 & 2033

- Figure 4: Asia Pacific Liquid Hydrogen Industry Volume (kilotons), by Distribution 2025 & 2033

- Figure 5: Asia Pacific Liquid Hydrogen Industry Revenue Share (%), by Distribution 2025 & 2033

- Figure 6: Asia Pacific Liquid Hydrogen Industry Volume Share (%), by Distribution 2025 & 2033

- Figure 7: Asia Pacific Liquid Hydrogen Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 8: Asia Pacific Liquid Hydrogen Industry Volume (kilotons), by End-user Industry 2025 & 2033

- Figure 9: Asia Pacific Liquid Hydrogen Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 10: Asia Pacific Liquid Hydrogen Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 11: Asia Pacific Liquid Hydrogen Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: Asia Pacific Liquid Hydrogen Industry Volume (kilotons), by Country 2025 & 2033

- Figure 13: Asia Pacific Liquid Hydrogen Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Liquid Hydrogen Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America Liquid Hydrogen Industry Revenue (Million), by Distribution 2025 & 2033

- Figure 16: North America Liquid Hydrogen Industry Volume (kilotons), by Distribution 2025 & 2033

- Figure 17: North America Liquid Hydrogen Industry Revenue Share (%), by Distribution 2025 & 2033

- Figure 18: North America Liquid Hydrogen Industry Volume Share (%), by Distribution 2025 & 2033

- Figure 19: North America Liquid Hydrogen Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 20: North America Liquid Hydrogen Industry Volume (kilotons), by End-user Industry 2025 & 2033

- Figure 21: North America Liquid Hydrogen Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: North America Liquid Hydrogen Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 23: North America Liquid Hydrogen Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: North America Liquid Hydrogen Industry Volume (kilotons), by Country 2025 & 2033

- Figure 25: North America Liquid Hydrogen Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Liquid Hydrogen Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Liquid Hydrogen Industry Revenue (Million), by Distribution 2025 & 2033

- Figure 28: Europe Liquid Hydrogen Industry Volume (kilotons), by Distribution 2025 & 2033

- Figure 29: Europe Liquid Hydrogen Industry Revenue Share (%), by Distribution 2025 & 2033

- Figure 30: Europe Liquid Hydrogen Industry Volume Share (%), by Distribution 2025 & 2033

- Figure 31: Europe Liquid Hydrogen Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 32: Europe Liquid Hydrogen Industry Volume (kilotons), by End-user Industry 2025 & 2033

- Figure 33: Europe Liquid Hydrogen Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 34: Europe Liquid Hydrogen Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 35: Europe Liquid Hydrogen Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe Liquid Hydrogen Industry Volume (kilotons), by Country 2025 & 2033

- Figure 37: Europe Liquid Hydrogen Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Liquid Hydrogen Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Rest of the World Liquid Hydrogen Industry Revenue (Million), by Distribution 2025 & 2033

- Figure 40: Rest of the World Liquid Hydrogen Industry Volume (kilotons), by Distribution 2025 & 2033

- Figure 41: Rest of the World Liquid Hydrogen Industry Revenue Share (%), by Distribution 2025 & 2033

- Figure 42: Rest of the World Liquid Hydrogen Industry Volume Share (%), by Distribution 2025 & 2033

- Figure 43: Rest of the World Liquid Hydrogen Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 44: Rest of the World Liquid Hydrogen Industry Volume (kilotons), by End-user Industry 2025 & 2033

- Figure 45: Rest of the World Liquid Hydrogen Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: Rest of the World Liquid Hydrogen Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: Rest of the World Liquid Hydrogen Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Rest of the World Liquid Hydrogen Industry Volume (kilotons), by Country 2025 & 2033

- Figure 49: Rest of the World Liquid Hydrogen Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Rest of the World Liquid Hydrogen Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Liquid Hydrogen Industry Revenue Million Forecast, by Distribution 2020 & 2033

- Table 2: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Distribution 2020 & 2033

- Table 3: Global Liquid Hydrogen Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Liquid Hydrogen Industry Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 5: Global Liquid Hydrogen Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Region 2020 & 2033

- Table 7: Global Liquid Hydrogen Industry Revenue Million Forecast, by Distribution 2020 & 2033

- Table 8: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Distribution 2020 & 2033

- Table 9: Global Liquid Hydrogen Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 10: Global Liquid Hydrogen Industry Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Liquid Hydrogen Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 13: China Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: China Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 15: India Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: India Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 17: Japan Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Japan Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 19: South Korea Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: South Korea Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 23: Global Liquid Hydrogen Industry Revenue Million Forecast, by Distribution 2020 & 2033

- Table 24: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Distribution 2020 & 2033

- Table 25: Global Liquid Hydrogen Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 26: Global Liquid Hydrogen Industry Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 27: Global Liquid Hydrogen Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 29: United States Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: United States Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 31: Canada Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Canada Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 33: Mexico Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Mexico Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 35: Global Liquid Hydrogen Industry Revenue Million Forecast, by Distribution 2020 & 2033

- Table 36: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Distribution 2020 & 2033

- Table 37: Global Liquid Hydrogen Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Liquid Hydrogen Industry Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Liquid Hydrogen Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 41: Germany Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Germany Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 45: Italy Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Italy Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 47: France Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: France Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 51: Global Liquid Hydrogen Industry Revenue Million Forecast, by Distribution 2020 & 2033

- Table 52: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Distribution 2020 & 2033

- Table 53: Global Liquid Hydrogen Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 54: Global Liquid Hydrogen Industry Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 55: Global Liquid Hydrogen Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Liquid Hydrogen Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 57: South America Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: South America Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 59: Middle East and Africa Liquid Hydrogen Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Middle East and Africa Liquid Hydrogen Industry Volume (kilotons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Hydrogen Industry?

The projected CAGR is approximately 10.27%.

2. Which companies are prominent players in the Liquid Hydrogen Industry?

Key companies in the market include Linde PLC, Air Products and Chemicals Inc, Universal Industrial Gases Inc *List Not Exhaustive, Messer Group GMBH, Iwatani Corporation, Air Liquide, Nippon Sanso Holdings Corporation, Nippon Sanso Holdings Corporation , Praxair Technology Inc. , ITM Power.

3. What are the main segments of the Liquid Hydrogen Industry?

The market segments include Distribution, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 38400 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Liquid Hydrogen for Space Exploration; Increasing Adoption of Hydrogen Fuel Cell in Commercial Vehicle.

6. What are the notable trends driving market growth?

Aerospace Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

High Cost Associated with Handling and Storage; Other Restraints.

8. Can you provide examples of recent developments in the market?

Mar 2023: Iwatani Corporation and ENEOS Corporation were working to deliver a "Liquefied Hydrogen Supply Chain Commercialization Demonstration Project. The project aims to develop marine transportation technologies of liquefied clean hydrogen, which will help to achieve a hydrogen supply cost of 30 JPY/Nm3 by 2030.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in kilotons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Hydrogen Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Hydrogen Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Hydrogen Industry?

To stay informed about further developments, trends, and reports in the Liquid Hydrogen Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence