Key Insights

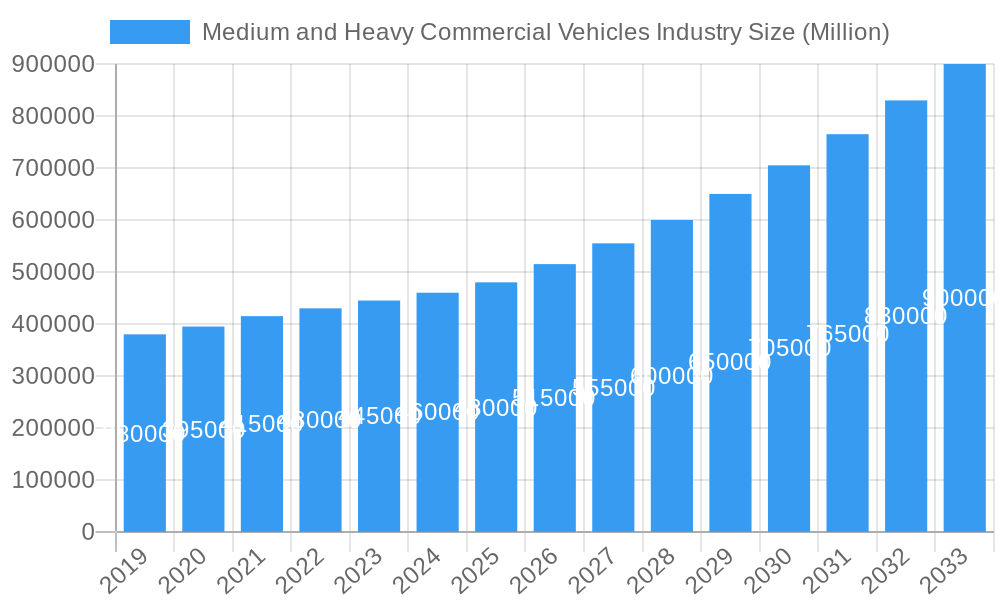

The global Medium and Heavy Commercial Vehicles (M&HCV) market is projected to reach USD 504.97 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 8.6%. Key growth drivers include expanding global trade, the booming e-commerce sector necessitating efficient logistics, and significant infrastructure development worldwide. Increased demand for last-mile delivery solutions and robust transportation networks to support industrial output are pivotal. Furthermore, consumer preference for expedited delivery and the need for fleet modernization with fuel-efficient, technologically advanced vehicles are sustaining market demand.

Medium and Heavy Commercial Vehicles Industry Market Size (In Billion)

Technological innovations are transforming the M&HCV sector, with a pronounced shift towards sustainable propulsion. Battery Electric Vehicles (BEVs) and Plug-In Hybrid Electric Vehicles (PHEVs) are gaining momentum, driven by stringent emission standards and heightened environmental awareness. Alternative fuel vehicles also offer substantial market potential. While technological adoption is a key trend, it presents challenges such as the high initial cost of electric and alternative fuel vehicles and the requirement for extensive charging and refueling infrastructure. Government incentives and decreasing battery costs are anticipated to alleviate these constraints. The market is segmented by tonnage, with the 7.5 - 16 ton and Above 16 ton segments anticipated to lead due to their critical role in freight transport.

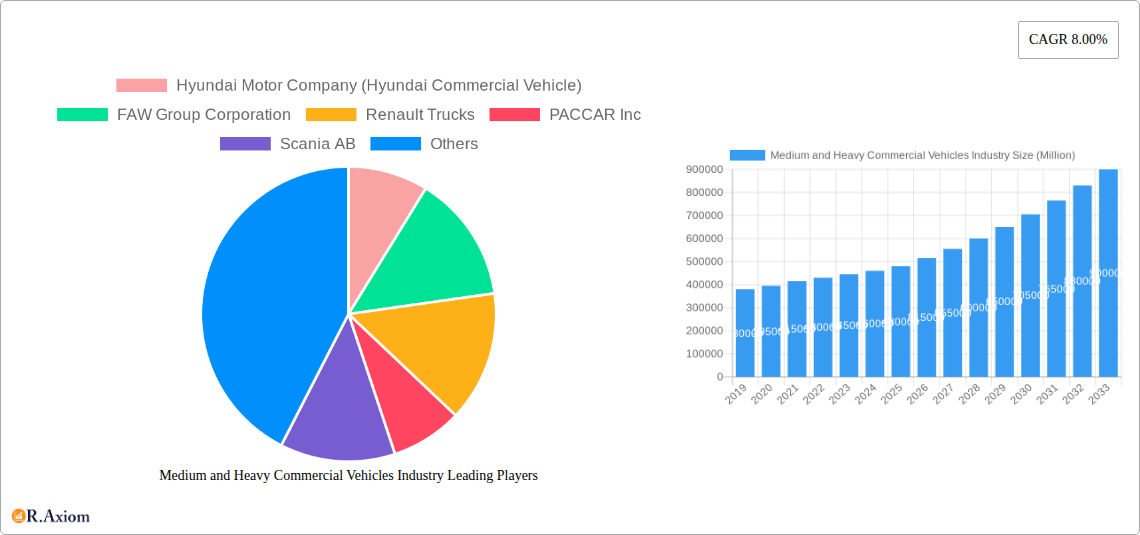

Medium and Heavy Commercial Vehicles Industry Company Market Share

This detailed report provides an SEO-optimized overview of the Medium and Heavy Commercial Vehicles (M&HCV) market, encompassing market size, growth, and forecasts.

Medium and Heavy Commercial Vehicles Industry Market Concentration & Innovation

The global Medium and Heavy Commercial Vehicles (MHCV) industry is characterized by a moderately consolidated market structure, with leading players such as Daimler AG, Volvo Group, and PACCAR Inc holding significant market share, estimated to be over 60 million vehicles in the historical period. Innovation is primarily driven by the urgent need for sustainability, digital integration, and enhanced operational efficiency. Regulatory frameworks, including stringent emission standards (e.g., Euro 7) and government incentives for zero-emission vehicles, are crucial innovation catalysts. Product substitutes, while limited for heavy-duty hauling, are emerging in specialized applications with advancements in electric and autonomous technologies. End-user trends are heavily influenced by e-commerce growth, demanding faster delivery times and more frequent, smaller shipments, which impacts fleet configurations and vehicle types. Mergers and acquisitions (M&A) activity is on the rise, with deal values in the hundreds of millions of dollars, as companies seek to expand their technological capabilities and market reach. For instance, strategic partnerships in battery technology and charging infrastructure development are key M&A targets. The competitive landscape is intensifying, pushing for greater collaboration and consolidation to meet evolving market demands and regulatory pressures.

Medium and Heavy Commercial Vehicles Industry Industry Trends & Insights

The Medium and Heavy Commercial Vehicles (MHCV) industry is experiencing a transformative growth trajectory, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period of 2025–2033. This robust expansion is propelled by a confluence of economic resurgence, booming e-commerce, and a global push towards sustainable logistics solutions. Technological disruptions are at the forefront, with the rapid development and adoption of battery electric vehicles (BEVs) and alternative fuel powered trucks, such as hydrogen fuel cell technology, fundamentally reshaping the propulsion landscape. Traditional Internal Combustion Engine (ICE) vehicles will continue to dominate in the near term, particularly in cost-sensitive markets, but their market penetration is projected to gradually decline as electric alternatives become more viable and infrastructure expands. Consumer preferences are increasingly leaning towards vehicles that offer lower total cost of ownership (TCO), improved driver comfort and safety features, and reduced environmental impact. Fleet operators are actively seeking smart fleet management solutions, predictive maintenance, and advanced telematics to optimize operations and enhance efficiency. The competitive dynamics are characterized by intense innovation, strategic alliances, and increasing investment in R&D by major players including Hyundai Commercial Vehicle, FAW Group Corporation, Renault Trucks, PACCAR Inc, Scania AB, MAN SE, Daimler AG, Tata Motors Limited, Volvo Group, Isuzu Motors Ltd, and Dongfeng Motor Corporation. The market penetration of electric MHCVs is expected to witness exponential growth, driven by declining battery costs, expanding charging networks, and supportive government policies, reaching an estimated xx million units by 2033.

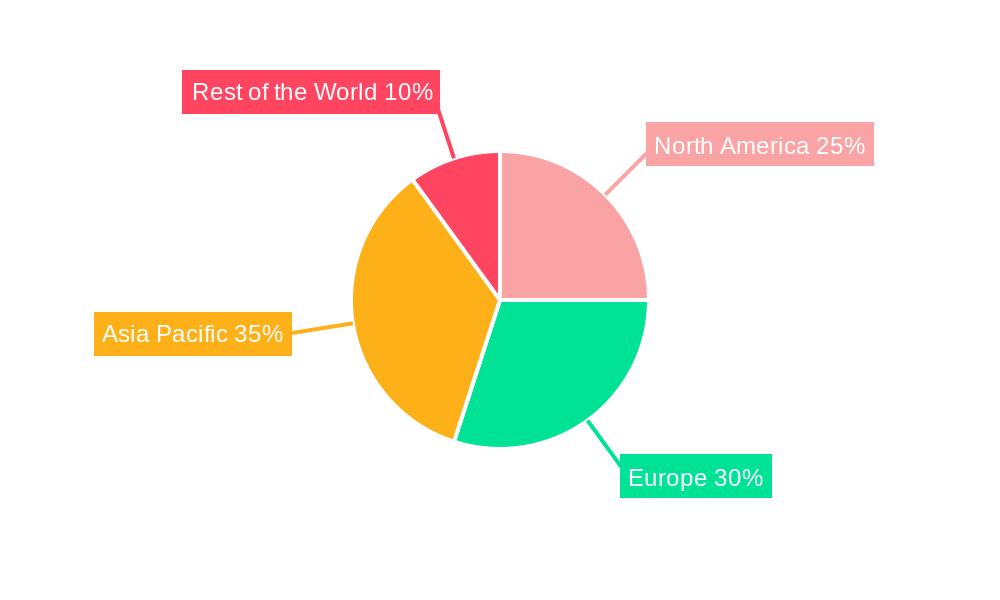

Dominant Markets & Segments in Medium and Heavy Commercial Vehicles Industry

The global Medium and Heavy Commercial Vehicles (MHCV) market exhibits clear regional dominance, with Asia-Pacific, particularly China, leading the charge due to its massive manufacturing base, extensive logistics networks, and significant government investment in infrastructure. Within this dynamic market, the "Above 16 ton" tonnage segment is the largest and most influential, driven by the demands of long-haul freight transportation and heavy industrial applications. Key drivers for this segment’s dominance include robust economic activity, expansion of global supply chains, and the increasing need for efficient movement of large volumes of goods.

In terms of propulsion, the "IC Engine" remains the dominant force in the historical period and the base year (2025), primarily due to its established infrastructure, lower upfront cost, and extensive operational range, particularly in regions with underdeveloped charging networks. However, the "Battery Electric" propulsion type is witnessing the most rapid growth and is poised to capture significant market share in the forecast period (2025–2033). This surge is fueled by tightening emission regulations, corporate sustainability goals, and advancements in battery technology leading to improved range and reduced charging times.

The "7.5 - 16 ton" segment is also a critical component of the MHCV market, catering to medium-distance haulage, urban distribution, and specialized vocational applications. Its growth is closely tied to the expansion of e-commerce and the need for efficient last-mile delivery solutions. Key drivers for this segment include increased urbanization, demand for flexible logistics, and the development of more fuel-efficient and technologically advanced vehicles.

The "Plug-In Hybrid Electric" and "Alternative Fuel Powered" segments, while currently smaller, represent significant emerging trends. Plug-in hybrids offer a transitional solution for fleets seeking to reduce emissions without compromising on range, while alternative fuels like hydrogen offer long-term potential for zero-emission heavy-duty transport. Key drivers for these segments include the pursuit of diverse decarbonization strategies and the exploration of solutions for niche applications where pure electric might not yet be optimal.

Medium and Heavy Commercial Vehicles Industry Product Developments

Recent product developments in the Medium and Heavy Commercial Vehicles (MHCV) industry are sharply focused on electrification, connectivity, and automation. Manufacturers are introducing advanced battery-electric trucks with extended range capabilities and faster charging times, targeting urban delivery and regional haulage. Innovations in lightweight materials and aerodynamic designs are enhancing fuel efficiency for both ICE and alternative fuel vehicles. The integration of sophisticated telematics and AI-powered fleet management systems provides predictive maintenance, route optimization, and enhanced driver safety, offering significant competitive advantages. These developments cater to the growing demand for sustainable, cost-effective, and highly efficient logistics solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global Medium and Heavy Commercial Vehicles (MHCV) market, segmented across key parameters. The tonnage segmentation includes: 3.5 - 7.5 ton, characterized by increasing adoption for urban logistics and light commercial duties, with projected market growth driven by last-mile delivery demands; 7.5 - 16 ton, a vital segment for regional haulage and vocational applications, expected to see steady growth influenced by infrastructure development and economic activity; and Above 16 ton, the largest segment, crucial for long-haul freight and heavy industry, with its growth heavily tied to global trade volumes and the transition to cleaner powertrains. Propulsion types analyzed include: IC Engine, expected to maintain a significant presence but with declining market share; Plug-In Hybrid Electric, offering a bridging technology with projected moderate growth; Battery Electric, the fastest-growing segment, driven by aggressive decarbonization targets and technological advancements; and Alternative Fuel Powered (e.g., hydrogen fuel cell), representing a nascent but high-potential future segment.

Key Drivers of Medium and Heavy Commercial Vehicles Industry Growth

The growth of the Medium and Heavy Commercial Vehicles (MHCV) industry is propelled by several interconnected factors. Government initiatives and stringent emission regulations worldwide are a primary driver, incentivizing the adoption of cleaner technologies like battery-electric and alternative fuel vehicles. The burgeoning e-commerce sector fuels demand for efficient and robust logistics solutions, necessitating an expansion and modernization of commercial fleets. Technological advancements in battery technology, charging infrastructure, and autonomous driving systems are making electric and intelligent vehicles more viable and cost-effective. Furthermore, the global focus on sustainability and corporate social responsibility is pushing companies to reduce their carbon footprint, leading to increased investment in green transportation solutions.

Challenges in the Medium and Heavy Commercial Vehicles Industry Sector

Despite significant growth prospects, the Medium and Heavy Commercial Vehicles (MHCV) industry faces several challenges. The high upfront cost of electric vehicles, coupled with the limited availability and high cost of charging infrastructure, remains a major barrier for widespread adoption. Supply chain disruptions, particularly for critical components like semiconductors and battery raw materials, continue to impact production volumes and lead times. Stringent and evolving regulatory landscapes can create compliance complexities and necessitate significant investment in research and development. Intense competition among established OEMs and new entrants, especially in the electric vehicle space, puts pressure on pricing and profit margins. Furthermore, the operational challenges of range anxiety and charging times for long-haul electric trucking require innovative solutions.

Emerging Opportunities in Medium and Heavy Commercial Vehicles Industry

The Medium and Heavy Commercial Vehicles (MHCV) industry is ripe with emerging opportunities. The rapid expansion of the electric vehicle (EV) market presents a significant opportunity for manufacturers to develop and deploy zero-emission trucks for various applications. The growth of hydrogen fuel cell technology offers a promising avenue for long-haul and heavy-duty applications where battery-electric solutions may face limitations. The increasing adoption of digital technologies, including AI, IoT, and predictive analytics, opens up opportunities for smart fleet management solutions, enhanced vehicle uptime, and improved operational efficiency. Emerging markets in developing economies are also presenting substantial growth potential as their logistics infrastructure expands and demand for goods transportation increases.

Leading Players in the Medium and Heavy Commercial Vehicles Industry Market

- Hyundai Motor Company (Hyundai Commercial Vehicle)

- FAW Group Corporation

- Renault Trucks

- PACCAR Inc

- Scania AB

- MAN SE

- Daimler AG

- Tata Motors Limited

- Volvo Group

- Isuzu Motors Ltd

- Dongfeng Motor Corporation

Key Developments in Medium and Heavy Commercial Vehicles Industry Industry

- 2023/2024: Several major OEMs announce significant investments in battery production facilities and charging infrastructure partnerships to accelerate EV adoption.

- 2023/2024: New models of heavy-duty battery-electric trucks with increased range and payload capacity are launched, targeting long-haul and regional distribution.

- 2023/2024: Advancements in hydrogen fuel cell technology demonstrate improved efficiency and durability, gaining traction for heavy-duty applications.

- 2023/2024: Regulatory bodies worldwide introduce stricter emissions standards and provide incentives for the purchase of zero-emission commercial vehicles.

- 2022/2023: Strategic collaborations and mergers increase, focusing on developing shared charging networks and autonomous driving technologies.

Strategic Outlook for Medium and Heavy Commercial Vehicles Industry Market

The strategic outlook for the Medium and Heavy Commercial Vehicles (MHCV) market is exceptionally positive, driven by a powerful convergence of sustainability mandates, technological innovation, and evolving economic demands. The accelerated transition towards electric and alternative fuel powertrains will continue to be a primary growth catalyst. Investments in expanding charging and refueling infrastructure will be crucial for unlocking the full potential of zero-emission heavy transport. Furthermore, the integration of advanced digital solutions, including AI-powered fleet management, autonomous driving capabilities, and enhanced connectivity, will redefine operational efficiency and customer value. Companies that can effectively navigate regulatory changes, manage supply chain complexities, and deliver innovative, cost-effective, and sustainable solutions will be best positioned for success in this dynamic and rapidly evolving market.

Medium and Heavy Commercial Vehicles Industry Segmentation

-

1. Tonnage

- 1.1. 3.5 - 7.5 ton

- 1.2. 7.5 - 16 ton

- 1.3. Above 16 ton

-

2. Propulsion Type

- 2.1. IC Engine

- 2.2. Plug-In Hybrid Electric

- 2.3. Battery Electric

- 2.4. Alternative Fuel Powered

Medium and Heavy Commercial Vehicles Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Brazil

- 4.2. South Africa

- 4.3. Other Countries

Medium and Heavy Commercial Vehicles Industry Regional Market Share

Geographic Coverage of Medium and Heavy Commercial Vehicles Industry

Medium and Heavy Commercial Vehicles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Tonnage

- 5.1.1. 3.5 - 7.5 ton

- 5.1.2. 7.5 - 16 ton

- 5.1.3. Above 16 ton

- 5.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.2.1. IC Engine

- 5.2.2. Plug-In Hybrid Electric

- 5.2.3. Battery Electric

- 5.2.4. Alternative Fuel Powered

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Tonnage

- 6. Global Medium and Heavy Commercial Vehicles Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Tonnage

- 6.1.1. 3.5 - 7.5 ton

- 6.1.2. 7.5 - 16 ton

- 6.1.3. Above 16 ton

- 6.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 6.2.1. IC Engine

- 6.2.2. Plug-In Hybrid Electric

- 6.2.3. Battery Electric

- 6.2.4. Alternative Fuel Powered

- 6.1. Market Analysis, Insights and Forecast - by Tonnage

- 7. North America Medium and Heavy Commercial Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Tonnage

- 7.1.1. 3.5 - 7.5 ton

- 7.1.2. 7.5 - 16 ton

- 7.1.3. Above 16 ton

- 7.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 7.2.1. IC Engine

- 7.2.2. Plug-In Hybrid Electric

- 7.2.3. Battery Electric

- 7.2.4. Alternative Fuel Powered

- 7.1. Market Analysis, Insights and Forecast - by Tonnage

- 8. Europe Medium and Heavy Commercial Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Tonnage

- 8.1.1. 3.5 - 7.5 ton

- 8.1.2. 7.5 - 16 ton

- 8.1.3. Above 16 ton

- 8.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 8.2.1. IC Engine

- 8.2.2. Plug-In Hybrid Electric

- 8.2.3. Battery Electric

- 8.2.4. Alternative Fuel Powered

- 8.1. Market Analysis, Insights and Forecast - by Tonnage

- 9. Asia Pacific Medium and Heavy Commercial Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Tonnage

- 9.1.1. 3.5 - 7.5 ton

- 9.1.2. 7.5 - 16 ton

- 9.1.3. Above 16 ton

- 9.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 9.2.1. IC Engine

- 9.2.2. Plug-In Hybrid Electric

- 9.2.3. Battery Electric

- 9.2.4. Alternative Fuel Powered

- 9.1. Market Analysis, Insights and Forecast - by Tonnage

- 10. Rest of the World Medium and Heavy Commercial Vehicles Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Tonnage

- 10.1.1. 3.5 - 7.5 ton

- 10.1.2. 7.5 - 16 ton

- 10.1.3. Above 16 ton

- 10.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 10.2.1. IC Engine

- 10.2.2. Plug-In Hybrid Electric

- 10.2.3. Battery Electric

- 10.2.4. Alternative Fuel Powered

- 10.1. Market Analysis, Insights and Forecast - by Tonnage

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Hyundai Motor Company (Hyundai Commercial Vehicle)

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 FAW Group Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Renault Trucks

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 PACCAR Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Scania AB

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 MAN SE

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Daimler AG

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Tata Motors Limited

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Volvo Group

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Isuzu Motors Ltd

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Dongfeng Motor Corporatio

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.1 Hyundai Motor Company (Hyundai Commercial Vehicle)

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Medium and Heavy Commercial Vehicles Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Tonnage 2025 & 2033

- Figure 3: North America Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Tonnage 2025 & 2033

- Figure 4: North America Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 5: North America Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 6: North America Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Tonnage 2025 & 2033

- Figure 9: Europe Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Tonnage 2025 & 2033

- Figure 10: Europe Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 11: Europe Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 12: Europe Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Tonnage 2025 & 2033

- Figure 15: Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Tonnage 2025 & 2033

- Figure 16: Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 17: Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 18: Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Tonnage 2025 & 2033

- Figure 21: Rest of the World Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Tonnage 2025 & 2033

- Figure 22: Rest of the World Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 23: Rest of the World Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 24: Rest of the World Medium and Heavy Commercial Vehicles Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Medium and Heavy Commercial Vehicles Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Tonnage 2020 & 2033

- Table 2: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 3: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Tonnage 2020 & 2033

- Table 5: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 6: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Rest of North America Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Tonnage 2020 & 2033

- Table 11: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 12: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Spain Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Tonnage 2020 & 2033

- Table 19: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 20: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: China Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Japan Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: India Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: South Korea Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Tonnage 2020 & 2033

- Table 27: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 28: Global Medium and Heavy Commercial Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Other Countries Medium and Heavy Commercial Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medium and Heavy Commercial Vehicles Industry?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Medium and Heavy Commercial Vehicles Industry?

Key companies in the market include Hyundai Motor Company (Hyundai Commercial Vehicle), FAW Group Corporation, Renault Trucks, PACCAR Inc, Scania AB, MAN SE, Daimler AG, Tata Motors Limited, Volvo Group, Isuzu Motors Ltd, Dongfeng Motor Corporatio.

3. What are the main segments of the Medium and Heavy Commercial Vehicles Industry?

The market segments include Tonnage, Propulsion Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 504.97 billion as of 2022.

5. What are some drivers contributing to market growth?

Technological Advancements In Vehicles Driving Demand; Others.

6. What are the notable trends driving market growth?

Electric Commercial Vehicle to Witness Steady Sales.

7. Are there any restraints impacting market growth?

High Scan Tool Costs to Limit Growth; Others.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medium and Heavy Commercial Vehicles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medium and Heavy Commercial Vehicles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medium and Heavy Commercial Vehicles Industry?

To stay informed about further developments, trends, and reports in the Medium and Heavy Commercial Vehicles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence