Key Insights

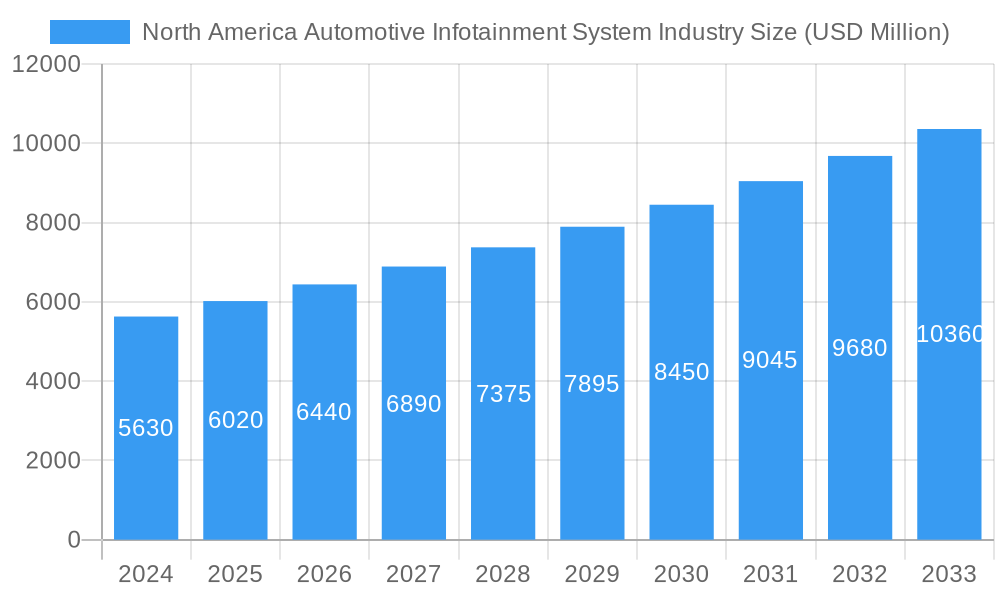

The North American automotive infotainment system market is poised for significant expansion, demonstrating robust growth driven by evolving consumer expectations for seamless connectivity and advanced in-car experiences. In 2024, the market is valued at an estimated USD 5,630 million. This growth is fueled by the increasing integration of sophisticated technologies like AI-powered voice assistants, advanced navigation, augmented reality displays, and robust entertainment options within vehicles. The rising demand for premium features in both passenger cars and commercial vehicles, coupled with the increasing penetration of connected car services, are primary catalysts. Furthermore, the aftermarket segment is experiencing a substantial surge as consumers seek to upgrade their existing vehicle's infotainment capabilities with the latest innovations, complementing the widespread adoption of Original Equipment Manufacturer (OEM) systems. This dynamic landscape presents a fertile ground for innovation and strategic partnerships among leading automotive suppliers and technology providers.

North America Automotive Infotainment System Industry Market Size (In Billion)

The North American automotive infotainment system market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.9% from 2024 through 2033. This sustained growth trajectory is underpinned by continuous technological advancements and a consumer appetite for integrated digital ecosystems within their vehicles. Key trends include the development of larger, higher-resolution displays, intuitive user interfaces, and personalized content delivery. Challenges such as the high cost of advanced systems and cybersecurity concerns are being addressed through ongoing research and development, aiming to balance innovation with affordability and security. Major players like Harman International, Continental AG, and Robert Bosch GmbH are actively investing in R&D to capture market share, focusing on developing next-generation infotainment solutions that enhance safety, convenience, and overall driving pleasure. The market's segmentation into audio units, display units, navigation systems, and comprehensive systems, along with the distinct roles of OEM and aftermarket installations, highlights the diverse opportunities and competitive strategies within this burgeoning sector.

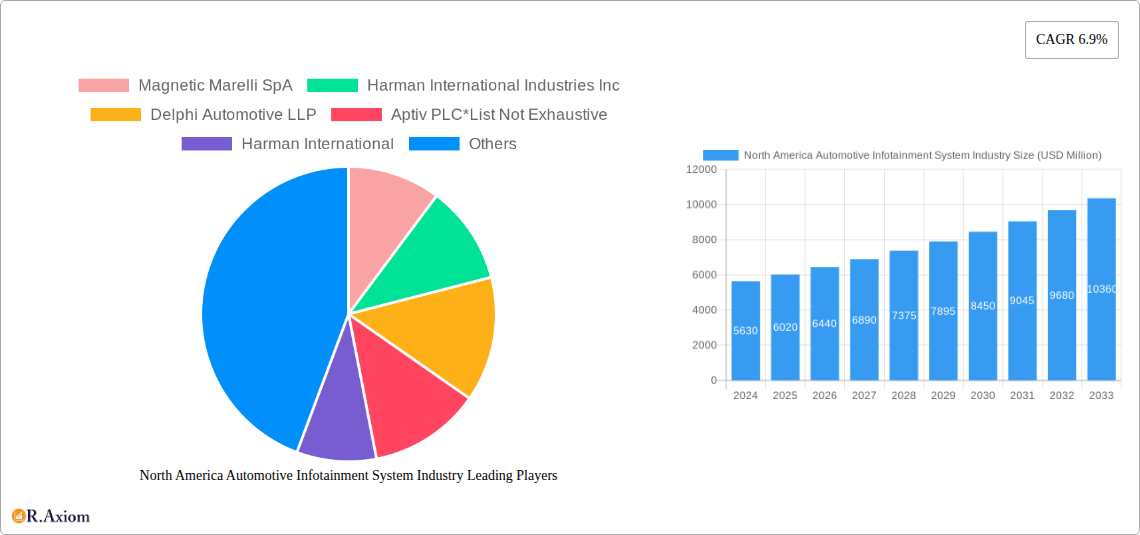

North America Automotive Infotainment System Industry Company Market Share

This in-depth report provides a detailed analysis of the North America Automotive Infotainment System Industry, covering market size, growth trends, segmentation, key players, and future outlook. Leveraging high-traffic keywords such as "automotive infotainment systems," "in-car entertainment," "automotive technology," and "connected car solutions," this report is optimized for search engines to reach industry stakeholders, including automakers, Tier-1 suppliers, technology providers, and investors. The study period spans from 2019 to 2033, with a base year of 2025, offering insights into historical performance, current market dynamics, and robust forecasts for the period 2025–2033.

North America Automotive Infotainment System Industry Market Concentration & Innovation

The North America automotive infotainment system industry is characterized by a moderate to high level of market concentration, with a few dominant players holding significant market share, estimated to be over 65% in 2025. Innovation is a primary driver, fueled by the relentless pursuit of enhanced user experience, increased vehicle connectivity, and advanced driver-assistance systems (ADAS) integration. Regulatory frameworks, particularly those related to data privacy and cybersecurity, are increasingly shaping product development and market entry strategies. Product substitutes, such as aftermarket head units and mobile device integration, continue to pose a challenge, but OEM-integrated systems are gaining traction due to seamless integration and advanced features. End-user trends highlight a growing demand for personalized content, intuitive interfaces, and robust connectivity solutions, including advanced Wi-Fi and Bluetooth capabilities. Mergers and acquisitions (M&A) activities are prevalent, with an estimated M&A deal value exceeding $1.5 billion between 2023-2025, aimed at consolidating market position and acquiring cutting-edge technologies. Key M&A activities include Harman International's acquisition of Apostera, strengthening their AR/MR capabilities.

North America Automotive Infotainment System Industry Industry Trends & Insights

The North America automotive infotainment system industry is experiencing robust growth, driven by several key factors. The increasing adoption of electric vehicles (EVs) and autonomous driving technologies is a significant catalyst, as these vehicles inherently require more sophisticated and integrated infotainment systems for navigation, entertainment, and communication. The escalating consumer demand for personalized in-car experiences, advanced connectivity features, and seamless integration with personal devices is pushing manufacturers to innovate at an unprecedented pace. This is reflected in the projected Compound Annual Growth Rate (CAGR) of approximately 12.5% during the forecast period of 2025–2033. Market penetration of advanced infotainment systems in new vehicle sales is expected to surpass 85% by 2028. Technological disruptions, such as the integration of artificial intelligence (AI) for voice recognition and predictive services, augmented reality (AR) for head-up displays, and enhanced graphics processing capabilities, are reshaping the competitive landscape. Companies are investing heavily in R&D to offer faster processing speeds, richer multimedia experiences, and safer, more intuitive human-machine interfaces (HMIs). The competitive dynamics are intensifying, with established Tier-1 suppliers and technology giants vying for dominance. Consumer preferences are shifting towards larger, higher-resolution displays, customizable interfaces, and over-the-air (OTA) update capabilities, allowing for continuous feature enhancement and bug fixes. The integration of 5G connectivity is also poised to revolutionize in-car services, enabling real-time data streaming, enhanced navigation, and V2X (vehicle-to-everything) communication. The growing importance of cybersecurity and data privacy further influences product development, as manufacturers strive to build trust and secure sensitive user information.

Dominant Markets & Segments in North America Automotive Infotainment System Industry

The North America automotive infotainment system industry demonstrates clear leadership within specific markets and segments.

- Leading Region/Country: The United States currently dominates the North American market, accounting for approximately 70% of the total market share in 2025, driven by its large automotive manufacturing base, high disposable incomes, and early adoption of advanced automotive technologies. Canada and Mexico follow, with Mexico's market expected to grow at a higher CAGR due to increasing vehicle production and demand for value-added features.

- Vehicle Type Dominance: Passenger Cars represent the largest segment, projected to capture over 80% of the market share in 2025. This is attributed to the sheer volume of passenger vehicle sales and the consumer expectation for advanced infotainment features in personal vehicles. Commercial Vehicles, while a smaller segment, are witnessing rapid growth due to the increasing need for fleet management solutions, real-time tracking, and driver comfort features.

- Product Type Dominance: Display Units are the most prevalent product type, forming a significant portion of the market value in 2025. However, Comprehensive Systems, which integrate audio, display, navigation, and connectivity features, are experiencing the fastest growth due to their ability to offer a holistic user experience and leverage advanced software capabilities. Audio Units and Navigation Systems remain crucial components, but are increasingly becoming integrated within broader system architectures.

- Installation Type Dominance: The Original Equipment Manufacturer (OEM) segment overwhelmingly dominates the market, accounting for over 90% of sales in 2025. This is due to automakers' preference for integrated, proprietary systems that offer a seamless brand experience and leverage their vehicle architecture. The Aftermarket segment, while smaller, is expected to grow steadily as consumers seek to upgrade older vehicles or personalize their existing infotainment systems with newer technologies.

North America Automotive Infotainment System Industry Product Developments

Product developments in the North America automotive infotainment system industry are increasingly focused on creating a connected, personalized, and intuitive in-car experience. Innovations such as the integration of next-generation Snapdragon Cockpit Platforms by Qualcomm Technologies Inc., powering Volvo Cars' new electric SUV and Polestar 3, highlight a trend towards significantly faster system performance, improved graphics rendering, and enhanced audio processing. Harman International's acquisition of Apostera signifies a strategic move to integrate augmented reality (AR) and mixed reality (MR) into infotainment systems and head-up displays, offering novel ways to present information and enhance driver engagement. Visteon's unveiling of its fourth-generation SmartCore cockpit domain controller at CES® 2022 exemplifies the industry's push towards consolidating vehicle cockpit functions into a single, intelligent platform, enabling automakers to deliver a more unified and customizable driving environment. These developments underscore a competitive advantage gained through enhanced processing power, advanced software integration, and novel user interface designs.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North America automotive infotainment system market, segmented by key criteria to offer granular insights into market dynamics.

- Vehicle Type: The market is segmented into Passenger Cars and Commercial Vehicles. Passenger Cars are the larger segment, driven by consumer demand for advanced entertainment and connectivity. Commercial Vehicles are a rapidly growing segment, spurred by the need for fleet management and productivity tools.

- Product Type: The segmentation includes Audio Units, Display Units, Navigation Systems, and Comprehensive Systems. Display Units hold a significant share, while Comprehensive Systems, integrating multiple functionalities, are poised for substantial growth as automakers aim for integrated cockpit solutions.

- Installation Type: The market is divided into OEM (Original Equipment Manufacturer) and Aftermarket. The OEM segment is dominant, reflecting automakers' control over vehicle interiors and technology integration. The Aftermarket segment caters to consumers seeking upgrades and personalization.

Key Drivers of North America Automotive Infotainment System Industry Growth

Several key drivers are propelling the growth of the North America automotive infotainment system industry. The relentless advancement in digital technologies, including AI, 5G connectivity, and advanced display technologies, enables the development of more sophisticated and user-friendly infotainment systems. Increasing consumer demand for seamless connectivity, personalized in-car experiences, and advanced entertainment features is a primary growth catalyst. The burgeoning electric vehicle (EV) market, which inherently requires advanced digital interfaces for battery management, charging information, and connected services, further fuels demand. Government initiatives promoting vehicle safety and connectivity, alongside automakers' focus on differentiating their offerings through advanced in-car technology, are also significant contributors to market expansion.

Challenges in the North America Automotive Infotainment System Industry Sector

Despite its robust growth, the North America automotive infotainment system industry faces several challenges. The escalating complexity of infotainment systems, coupled with increasing cybersecurity threats, necessitates stringent security measures and compliance with evolving data privacy regulations, impacting development timelines and costs. Supply chain disruptions, particularly for semiconductors, continue to pose a risk, potentially delaying production and impacting product availability. Intense competition among established players and emerging technology providers leads to price pressures and requires continuous innovation to maintain market share. The high cost of advanced infotainment systems can also be a barrier for some consumer segments, particularly in the aftermarket. Furthermore, the rapid pace of technological obsolescence requires significant investment in R&D to stay ahead of the curve.

Emerging Opportunities in North America Automotive Infotainment System Industry

The North America automotive infotainment system industry is ripe with emerging opportunities. The widespread adoption of 5G technology presents a significant opportunity for enhanced in-car connectivity, enabling real-time data streaming for advanced navigation, infotainment services, and V2X communication. The growing demand for personalized user experiences, driven by AI and machine learning, allows for tailored content delivery and predictive functionalities. The expansion of the electric vehicle (EV) market creates a demand for integrated infotainment systems that manage charging, optimize range, and provide seamless connected services. Furthermore, the increasing integration of AR and VR technologies offers novel avenues for driver assistance, enhanced navigation, and immersive entertainment. The development of sophisticated over-the-air (OTA) update capabilities also presents an opportunity for ongoing revenue generation and continuous product improvement.

Leading Players in the North America Automotive Infotainment System Industry Market

- Magnetic Marelli SpA

- Harman International Industries Inc

- Delphi Automotive LLP

- Aptiv PLC

- Panasonic Corp

- Denso Technologies

- Continental AG

- Kenwood Corporation

- Robert Bosch GmBH

Key Developments in North America Automotive Infotainment System Industry Industry

- April 2022: Qualcomm Technologies Inc. announced that Volvo Cars' upcoming fully electric SUV and Polestar 3 will feature infotainment systems powered by next-generation Snapdragon Cockpit Platforms and advanced wireless technologies for enhanced Wi-Fi and Bluetooth. Qualcomm optimized the software development pipeline, resulting in 2.5 times faster overall system speed, 5 to 10 times faster graphics rendering, and 2.5 times faster audio digital signal processing.

- February 2022: Harman International acquired Apostera, an augmented reality (AR) and Mixed Reality (MR) software developer. This acquisition aims to expand Harman's automotive product offerings with AR and MR technologies, particularly for head-up displays and infotainment systems.

- January 2022: Visteon unveiled the fourth-generation SmartCore cockpit domain controller at CES® 2022, showcasing a solution designed to enable global automakers to deliver a more connected, personalized, and safe driving experience.

Strategic Outlook for North America Automotive Infotainment System Industry Market

The strategic outlook for the North America automotive infotainment system market remains exceptionally positive. The continued integration of advanced digital technologies, such as AI, 5G, and augmented reality, will redefine the in-car experience, driving demand for sophisticated systems. The burgeoning electric and autonomous vehicle sectors will further accelerate the need for seamless, intelligent infotainment solutions. Automakers' focus on differentiating their vehicles through cutting-edge technology, coupled with evolving consumer preferences for connectivity and personalization, will create sustained market momentum. Strategic collaborations between technology providers and automotive manufacturers, along with targeted M&A activities, will shape the competitive landscape, fostering innovation and consolidation. The market is poised for continued robust growth, driven by technological advancements and a deep understanding of evolving consumer needs.

North America Automotive Infotainment System Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Product Type

- 2.1. Audio Unit

- 2.2. Display Unit

- 2.3. Navigation Systems

- 2.4. Comprehensive Systems

-

3. Installation Type

- 3.1. OEM

- 3.2. Aftermarket

North America Automotive Infotainment System Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Automotive Infotainment System Industry Regional Market Share

Geographic Coverage of North America Automotive Infotainment System Industry

North America Automotive Infotainment System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Audio Unit

- 5.2.2. Display Unit

- 5.2.3. Navigation Systems

- 5.2.4. Comprehensive Systems

- 5.3. Market Analysis, Insights and Forecast - by Installation Type

- 5.3.1. OEM

- 5.3.2. Aftermarket

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. North America Automotive Infotainment System Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Audio Unit

- 6.2.2. Display Unit

- 6.2.3. Navigation Systems

- 6.2.4. Comprehensive Systems

- 6.3. Market Analysis, Insights and Forecast - by Installation Type

- 6.3.1. OEM

- 6.3.2. Aftermarket

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Magnetic Marelli SpA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Harman International Industries Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Delphi Automotive LLP

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Aptiv PLC*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Harman International

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Panasonic Corp

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Denso Technologies

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Continental AG

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Kenwood Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Robert Bosch GmBH

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Magnetic Marelli SpA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Automotive Infotainment System Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Automotive Infotainment System Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Automotive Infotainment System Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: North America Automotive Infotainment System Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: North America Automotive Infotainment System Industry Revenue billion Forecast, by Installation Type 2020 & 2033

- Table 4: North America Automotive Infotainment System Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Automotive Infotainment System Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: North America Automotive Infotainment System Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: North America Automotive Infotainment System Industry Revenue billion Forecast, by Installation Type 2020 & 2033

- Table 8: North America Automotive Infotainment System Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States North America Automotive Infotainment System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Automotive Infotainment System Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Automotive Infotainment System Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Infotainment System Industry?

The projected CAGR is approximately 9.7%.

2. Which companies are prominent players in the North America Automotive Infotainment System Industry?

Key companies in the market include Magnetic Marelli SpA, Harman International Industries Inc, Delphi Automotive LLP, Aptiv PLC*List Not Exhaustive, Harman International, Panasonic Corp, Denso Technologies, Continental AG, Kenwood Corporation, Robert Bosch GmBH.

3. What are the main segments of the North America Automotive Infotainment System Industry?

The market segments include Vehicle Type, Product Type, Installation Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for ADAS Integration.

6. What are the notable trends driving market growth?

Increasing Demand for In-Dash Infotainment System to Enhance Market Growth.

7. Are there any restraints impacting market growth?

High Upfront Cost.

8. Can you provide examples of recent developments in the market?

In April 2022, Qualcomm Technologies Inc., announced that the infotainment systems in Volvo Cars' upcoming fully electric SUV and Polestar 3 will be powered by next-generation Snapdragon Cockpit Platforms and its advanced suite of wireless technologies to support advanced Wi-Fi and Bluetooth capabilities. Qualcomm optimized and aligned the software development pipeline to advance a product with improved performance. This means 2.5 times faster overall system speed, 5 to 10 times faster graphics rendering, and 2.5 times faster audio digital signal processing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Infotainment System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Infotainment System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Infotainment System Industry?

To stay informed about further developments, trends, and reports in the North America Automotive Infotainment System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence