Key Insights

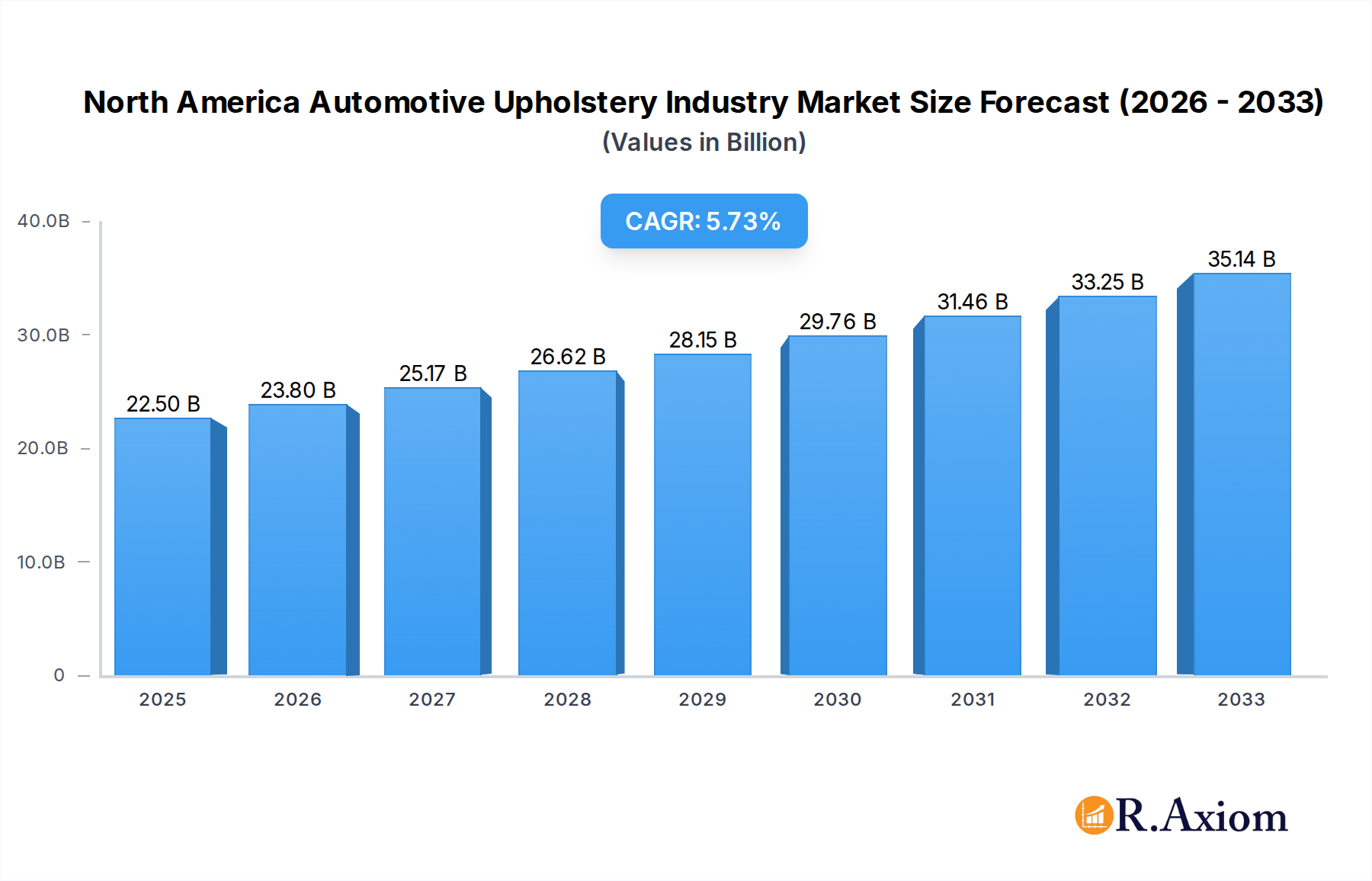

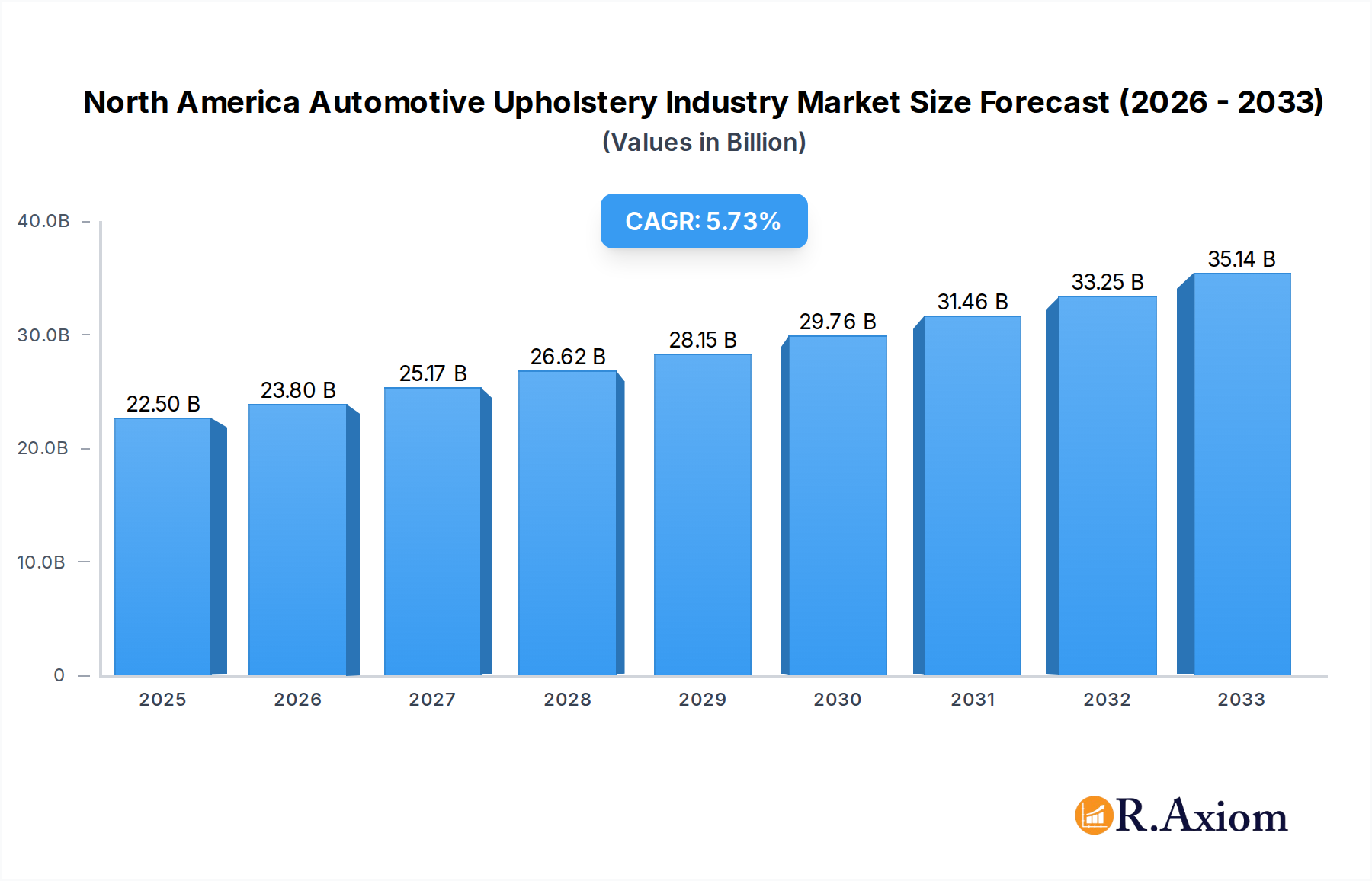

The North American automotive upholstery market is poised for significant growth, projected to reach $22.5 billion in 2025 and expand at a robust CAGR of 5.7% through 2033. This upward trajectory is primarily fueled by increasing consumer demand for premium and customizable vehicle interiors, the continuous innovation in material technologies offering enhanced durability, comfort, and aesthetic appeal, and the rising production of light commercial vehicles and SUVs which often feature more elaborate upholstery. Furthermore, the aftermarket segment is expected to witness substantial expansion as vehicle owners increasingly invest in upgrading their existing car interiors to improve resale value and personal comfort. Key drivers include the growing adoption of sustainable and recycled materials in response to environmental regulations and consumer preferences, alongside advancements in manufacturing techniques that enable more intricate designs and cost-effective production.

North America Automotive Upholstery Industry Market Size (In Billion)

The market is segmented across various material types, with Leather and Vinyl expected to maintain dominant positions due to their established appeal and performance characteristics. However, "Other Material Types" are anticipated to gain traction, driven by the development of advanced synthetic fabrics, eco-friendly alternatives, and novel composite materials that offer unique textures and functionalities. In terms of product segments, Seats will continue to command the largest share, followed by Dashboard and Roof Liners, as manufacturers prioritize passenger comfort and interior aesthetics. The OEM segment will remain the primary sales channel, accounting for the bulk of demand, while the aftermarket is set to experience accelerated growth. Key players like Adient Plc, Lear Corp, and Toyota Boshoku Corp are actively investing in research and development to introduce innovative solutions and expand their market reach across North America.

North America Automotive Upholstery Industry Company Market Share

Here is an SEO-optimized, detailed report description for the North America Automotive Upholstery Industry, designed for immediate use without modification.

North America Automotive Upholstery Industry Market Concentration & Innovation

The North America Automotive Upholstery Industry is characterized by a moderate to high market concentration, with major players like Adient Plc and Lear Corporation holding significant market share. Innovation in this sector is primarily driven by the demand for enhanced comfort, sustainability, and advanced functionalities within vehicle interiors. Regulatory frameworks, particularly those concerning emissions and material safety, are increasingly influencing product development. The prevalence of product substitutes, such as premium textiles and advanced composites, necessitates continuous innovation from traditional upholstery providers. End-user trends lean towards personalized and luxurious interior experiences, especially in the premium and electric vehicle segments, pushing manufacturers to adopt cutting-edge materials and designs. Mergers and acquisitions (M&A) are active, with deal values in the billions, consolidating market power and expanding technological capabilities. For instance, the consolidation of smaller suppliers into larger entities is a recurring theme, aiming for economies of scale and broader product portfolios. Current estimates project the North American automotive upholstery market to reach over \$50 billion by 2025, with M&A activities accounting for over \$5 billion in disclosed deal values within the historical period. The strategic acquisition of technology-focused startups by established OEMs and Tier-1 suppliers is a key trend, bolstering their competitive edge in areas like smart textiles and sustainable materials.

North America Automotive Upholstery Industry Industry Trends & Insights

The North America Automotive Upholstery Industry is poised for substantial growth, driven by a confluence of robust market drivers, technological advancements, evolving consumer preferences, and dynamic competitive landscapes. The market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period of 2025-2033, translating into a market value expected to exceed \$80 billion by 2033. This expansion is significantly fueled by the increasing production of vehicles, particularly SUVs and electric vehicles (EVs), which often feature more elaborate and premium interior upholstery. Technological disruptions are a pivotal force, with innovations in sustainable materials, smart textiles, and advanced manufacturing processes reshaping product offerings. The integration of recycled and bio-based materials, such as those highlighted by Polestar's use of INEOS BIOVYN, is gaining traction due to growing environmental consciousness among consumers and stringent environmental regulations. Consumer preferences are rapidly shifting towards personalized, comfortable, and aesthetically pleasing interior environments. This includes a rising demand for vegan and leather-free alternatives, as demonstrated by BMW Group's strategic move towards entirely vegan interiors, and a desire for enhanced functionality, such as advanced ergonomic seating solutions seen in the new Lexus GX. The competitive dynamics are intense, with both established global players and emerging innovators vying for market share. Original Equipment Manufacturers (OEMs) are increasingly collaborating with upholstery suppliers to co-develop bespoke interior solutions that differentiate their vehicles. The aftermarket segment also remains a significant contributor, offering consumers opportunities to upgrade their existing vehicle interiors with premium materials and custom designs. The penetration of advanced upholstery technologies is expected to rise as more manufacturers adopt sustainable and technologically integrated solutions to meet evolving market demands and regulatory requirements. The ongoing development of lighter, more durable, and aesthetically superior materials will continue to drive innovation and market growth.

Dominant Markets & Segments in North America Automotive Upholstery Industry

The North America Automotive Upholstery Industry is segmented across various material types, sales channels, and product categories, with distinct segments demonstrating dominant performance.

Material Type Dominance:

- Leather: Continues to be a premium choice, particularly in luxury and performance vehicles, driven by its perceived durability, aesthetic appeal, and status symbol. The demand for ethically sourced and sustainably processed leather is also on the rise.

- Vinyl: Remains a strong contender due to its cost-effectiveness, durability, and ease of maintenance. It is prevalent in entry-level and mass-market vehicles. Innovations in synthetic leather are blurring the lines with genuine leather in terms of feel and appearance.

- Other Material Types: This increasingly important segment encompasses a wide array of sustainable and advanced materials, including recycled fabrics, bio-based polymers, and high-performance textiles. The growing emphasis on sustainability and lightweighting is driving significant growth in this category.

Sales Channel Dominance:

- OEM (Original Equipment Manufacturer): This is the largest and most dominant sales channel, directly supplying upholstery components for new vehicle production. The volume and scale of OEM contracts ensure substantial market share for leading suppliers. Economic policies supporting automotive manufacturing and infrastructure development for new vehicle plants are key drivers.

- Aftermarket: This channel caters to vehicle owners seeking to customize, repair, or upgrade their interiors. It is driven by consumer demand for personalization and replacement parts. Economic stability and disposable income levels directly influence aftermarket sales.

Product Dominance:

- Seats: Represent the largest and most complex product segment within automotive upholstery. Innovations in ergonomics, comfort, safety features, and integrated technology are driving growth. The increasing complexity of modern seating systems, including adjustable lumbar support, heating, cooling, and massage functions, contribute to their dominance.

- Dashboard: While not solely upholstery, the soft-touch materials and aesthetic finishes of dashboards are critical interior components. The trend towards integrated digital displays and ambient lighting influences dashboard design and material choices.

- Roof Liners: Offer opportunities for aesthetic enhancement and acoustic insulation. Premium materials and panoramic sunroof integration are key trends.

- Door Trim: Plays a significant role in the overall interior ambiance and tactile experience of a vehicle. The integration of speakers, lighting, and storage solutions shapes door trim design.

The United States remains the dominant market within North America, driven by its large automotive production base and high consumer spending on vehicles. Key economic policies, robust supply chains, and a strong consumer appetite for new and technologically advanced vehicles underpin this dominance.

North America Automotive Upholstery Industry Product Developments

Product innovations in the North America automotive upholstery industry are increasingly focused on sustainability, advanced comfort, and integrated technology. Recent developments include the introduction of modular and sustainable seat designs by Faurecia, offering enhanced durability and recyclability through easily assembled and dismantled components. The integration of bio-attributed vinyl, like INEOS BIOVYN used by Polestar, signifies a commitment to reducing the carbon footprint of automotive interiors by utilizing 100% renewable feedstock. Furthermore, luxury brands are pushing the boundaries of cabin experience, as exemplified by Bentley's "Airline Seats" in the Bentayga Extended Wheelbase Mulliner, setting new benchmarks for passenger comfort and sophistication. The industry is also responding to the growing demand for vegan and leather-free interiors, with significant advancements in materials that mimic the look and feel of traditional leather. These developments cater to evolving consumer preferences and stringent environmental regulations, positioning manufacturers to meet the demands of a conscious and comfort-seeking automotive market.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the North America Automotive Upholstery Industry, covering the historical period from 2019 to 2024 and projecting market dynamics through 2033, with a base year of 2025. The market is meticulously segmented to offer granular insights.

- Material Type: The analysis includes Leather, Vinyl, and Other Material Types. Leather and Vinyl segments are expected to maintain significant market share, while the "Other Material Types" segment, encompassing sustainable and advanced composites, is projected for robust growth due to increasing environmental consciousness and technological innovation.

- Sales Channel: We examine the OEM and Aftermarket channels. The OEM segment is expected to continue its dominance due to high volume production, while the Aftermarket segment offers significant growth potential driven by customization and replacement needs, with projections indicating a substantial market size exceeding \$15 billion by 2025.

- Product: The report details market dynamics for Dashboard, Seats, Roof Liners, and Door Trim. Seats are anticipated to hold the largest market share, driven by comfort and technology integration, with projected growth rates of over 7% annually. Dashboard and Door Trim segments are also experiencing innovation, particularly with integrated lighting and digital interfaces.

Key Drivers of North America Automotive Upholstery Industry Growth

The North America Automotive Upholstery Industry is propelled by several key drivers:

- Increasing Vehicle Production: A consistent rise in the production of new vehicles, particularly SUVs and electric vehicles (EVs), directly boosts demand for upholstery components.

- Technological Advancements: Innovations in sustainable materials, advanced textiles, and smart upholstery solutions are creating new market opportunities and product differentiation.

- Evolving Consumer Preferences: Growing demand for personalized, comfortable, luxurious, and environmentally friendly vehicle interiors is shaping product development.

- Regulatory Landscape: Stringent environmental regulations and safety standards are pushing manufacturers to adopt sustainable and advanced materials.

- Aftermarket Demand: The aftermarket segment, driven by customization and repair needs, provides a steady revenue stream and a platform for premium product adoption.

Challenges in the North America Automotive Upholstery Industry Sector

Despite robust growth, the North America Automotive Upholstery Industry faces several challenges:

- Raw Material Price Volatility: Fluctuations in the prices of key raw materials like leather, petroleum-based plastics for vinyl, and specialized textiles can impact profitability.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and logistical issues can disrupt the supply of raw materials and finished products, leading to production delays and increased costs. The industry experienced significant supply chain strain during 2021-2023, resulting in an estimated 5-10% increase in production costs.

- Intense Competition: The market is highly competitive, with numerous players vying for contracts, leading to pressure on pricing and profit margins.

- Sustainability Pressures: Meeting increasingly stringent environmental regulations and consumer demands for sustainable materials requires significant investment in research and development, potentially increasing production costs.

- Economic Downturns: Economic slowdowns and recessions can lead to reduced consumer spending on new vehicles, consequently impacting upholstery demand.

Emerging Opportunities in North America Automotive Upholstery Industry

The North America Automotive Upholstery Industry is ripe with emerging opportunities:

- Sustainable and Bio-based Materials: The growing demand for eco-friendly solutions presents a significant opportunity for companies developing and supplying recycled, bio-based, and biodegradable upholstery materials. The market for sustainable automotive interiors is projected to grow by over 15% annually.

- Smart Upholstery and Integrated Technology: The integration of sensors, heating/cooling elements, haptic feedback, and connectivity features into upholstery offers advanced comfort and functionality, creating a premium segment.

- Personalization and Customization: As consumers seek unique vehicle experiences, opportunities abound for custom upholstery solutions and premium material options in both OEM and aftermarket segments.

- Electric Vehicle (EV) Market Growth: The rapid expansion of the EV market, often associated with advanced and premium interiors, presents a substantial growth avenue for innovative upholstery solutions.

- Advanced Manufacturing Techniques: The adoption of 3D printing, digital knitting, and other advanced manufacturing methods can lead to more efficient production, reduced waste, and novel design possibilities.

Leading Players in the North America Automotive Upholstery Industry Market

- Adient Plc

- Lear Corporation

- Katzkin Leather Inc

- CMI Enterprise

- The Woodbridge Group

- IMS Nonwoven

- Seiren Co Ltd

- Toyota Boshoku Corp

- Faurecia SE

Key Developments in North America Automotive Upholstery Industry Industry

- August 2023: Bentley unveiled the Bentayga Extended Wheelbase Mulliner during Monterey Car Week in California. The Bentayga EWB Mulliner flagship has greater cabin room than any similar premium competition, owing to its Airline Seats. The rear compartment, which is available in 4+1 and 4-seat configurations, comes standard with the Bentley Airline Seat specification, the world's most sophisticated vehicle seating arrangement.

- June 2023: Faurecia, an automotive supplier, introduced a novel method to the design and production of automobile seats. As a value-added alternative to today's standard seat, Faurecia suggested a modular and sustainable seat comprised of a small number of modules rather than a huge number of components, developed using sustainable materials. The modules are readily attached and dismantled, allowing the seat's pieces to be upgraded and new capabilities to be added over its lifespan, resulting in improved durability and easier recycling of its constituent parts.

- June 2023: Lexus launched the newly revamped 2024 GX. The first-generation GX arrived in North America in 2002 as a mid-luxury SUV force to be reckoned with. Lexus enthusiasts have hailed the company's famed off-road aptitude and ability to navigate tough terrain, transporting clients comfortably from errands to distant locations. The all-new GX has seating for up to 7, and ergonomic measures have been introduced to assist in reducing load and work to promote driving posture through seat cushions, seatback bolsters, and headrest upgrades. The front seat hip point-to-heel height has been increased by 1.18 inches.

- November 2022: Volvo spin-off and electric car maker Polestar integrated INEOS BIOVYN in its fresh new Polestar 3 SUV. Microtech seat upholstery made of BIOVYNTM was one of the vehicle's features. Microtech used BIOVYN to lower the carbon impact of the upholstery. BIOVYN stands for bio-attributed vinyl. Polestar claims that it is produced of 100% renewable feedstock and does not compete with the food chain.

- September 2022: The BMW Group intended to debut its first automobiles with entirely vegan interiors in 2023. This was largely made feasible by the development of novel materials with leather-like characteristics. For the first time, fully vegan interiors were to be offered for BMW and MINI cars beginning in 2023. The BMW Group is thereby meeting a growing demand for vegan and leather-free interiors, which is expected to rise further in the near future, particularly in the United States, China, and Europe.

Strategic Outlook for North America Automotive Upholstery Industry Market

The North America Automotive Upholstery Industry is set for a dynamic and prosperous future, driven by innovation and evolving consumer demands. The strategic outlook centers on leveraging sustainable material technologies, developing advanced ergonomic and smart seating solutions, and expanding capabilities within the burgeoning electric vehicle segment. Increased collaboration between material suppliers, Tier-1 manufacturers, and OEMs will be crucial for co-creating differentiated interior experiences. Opportunities lie in capitalizing on the aftermarket's demand for personalization and the OEM segment's push for premium, eco-conscious interiors. Continued investment in R&D for next-generation materials, such as those derived from agricultural waste or advanced recycled polymers, will be a key growth catalyst, ensuring market leadership and sustained profitability in the years to come.

North America Automotive Upholstery Industry Segmentation

-

1. Material Type

- 1.1. Leather

- 1.2. Vinyl

- 1.3. Other Material Types

-

2. Sales Channel

- 2.1. OEM

- 2.2. Aftermarket

-

3. Product

- 3.1. Dashboard

- 3.2. Seats

- 3.3. Roof Liners

- 3.4. Door Trim

North America Automotive Upholstery Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest Of North America

North America Automotive Upholstery Industry Regional Market Share

Geographic Coverage of North America Automotive Upholstery Industry

North America Automotive Upholstery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Leather

- 5.1.2. Vinyl

- 5.1.3. Other Material Types

- 5.2. Market Analysis, Insights and Forecast - by Sales Channel

- 5.2.1. OEM

- 5.2.2. Aftermarket

- 5.3. Market Analysis, Insights and Forecast - by Product

- 5.3.1. Dashboard

- 5.3.2. Seats

- 5.3.3. Roof Liners

- 5.3.4. Door Trim

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest Of North America

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Leather

- 6.1.2. Vinyl

- 6.1.3. Other Material Types

- 6.2. Market Analysis, Insights and Forecast - by Sales Channel

- 6.2.1. OEM

- 6.2.2. Aftermarket

- 6.3. Market Analysis, Insights and Forecast - by Product

- 6.3.1. Dashboard

- 6.3.2. Seats

- 6.3.3. Roof Liners

- 6.3.4. Door Trim

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. United States North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Leather

- 7.1.2. Vinyl

- 7.1.3. Other Material Types

- 7.2. Market Analysis, Insights and Forecast - by Sales Channel

- 7.2.1. OEM

- 7.2.2. Aftermarket

- 7.3. Market Analysis, Insights and Forecast - by Product

- 7.3.1. Dashboard

- 7.3.2. Seats

- 7.3.3. Roof Liners

- 7.3.4. Door Trim

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Canada North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Leather

- 8.1.2. Vinyl

- 8.1.3. Other Material Types

- 8.2. Market Analysis, Insights and Forecast - by Sales Channel

- 8.2.1. OEM

- 8.2.2. Aftermarket

- 8.3. Market Analysis, Insights and Forecast - by Product

- 8.3.1. Dashboard

- 8.3.2. Seats

- 8.3.3. Roof Liners

- 8.3.4. Door Trim

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Rest Of North America North America Automotive Upholstery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Leather

- 9.1.2. Vinyl

- 9.1.3. Other Material Types

- 9.2. Market Analysis, Insights and Forecast - by Sales Channel

- 9.2.1. OEM

- 9.2.2. Aftermarket

- 9.3. Market Analysis, Insights and Forecast - by Product

- 9.3.1. Dashboard

- 9.3.2. Seats

- 9.3.3. Roof Liners

- 9.3.4. Door Trim

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Adient Plc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Lear Corp

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Katzkin Leather Inc *List Not Exhaustive

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 CMI Enterprise

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 The Woodbridge Group

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 IMS Nonwoven

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Seiren Co Ltd

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Toyota Boshoku Corp

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Faurecia SE

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Adient Plc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Automotive Upholstery Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Automotive Upholstery Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 3: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 4: North America Automotive Upholstery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 7: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 8: North America Automotive Upholstery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 10: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 11: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 12: North America Automotive Upholstery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Automotive Upholstery Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 14: North America Automotive Upholstery Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 15: North America Automotive Upholstery Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 16: North America Automotive Upholstery Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Upholstery Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the North America Automotive Upholstery Industry?

Key companies in the market include Adient Plc, Lear Corp, Katzkin Leather Inc *List Not Exhaustive, CMI Enterprise, The Woodbridge Group, IMS Nonwoven, Seiren Co Ltd, Toyota Boshoku Corp, Faurecia SE.

3. What are the main segments of the North America Automotive Upholstery Industry?

The market segments include Material Type, Sales Channel, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Passenger Car Sales Propelling Market Growth.

6. What are the notable trends driving market growth?

Increasing Demand for Aftermarket Upholstery Modifications May Drive the Market.

7. Are there any restraints impacting market growth?

Fluctuation in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

August 2023: Bentley unveiled the Bentayga Extended Wheelbase Mulliner during Monterey Car Week in California. The Bentayga EWB Mulliner flagship has greater cabin room than any similar premium competition, owing to its Airline Seats. The rear compartment, which is available in 4+1 and 4-seat configurations, comes standard with the Bentley Airline Seat specification, the world's most sophisticated vehicle seating arrangement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Upholstery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Upholstery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Upholstery Industry?

To stay informed about further developments, trends, and reports in the North America Automotive Upholstery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence