Key Insights

The North American dairy protein market is poised for robust expansion, projected to reach an estimated $5,461 million in 2024, driven by a CAGR of 6% through 2033. This growth is significantly fueled by the increasing consumer demand for protein-rich products, particularly within the sports nutrition and health & wellness sectors. The rising awareness of the benefits of protein for muscle building, satiety, and overall health is propelling the consumption of dairy protein ingredients like Whey Protein Isolates (WPIs) and Milk Protein Concentrates (MPCs). Furthermore, the expanding applications of dairy proteins in functional foods, beverages, and even personal care products are contributing to market buoyancy. Innovations in processing technologies that enhance the functionality and bioavailability of these proteins are also playing a crucial role in expanding their market reach. The trend towards clean-label products and natural ingredients further supports the demand for dairy-derived proteins as a preferred source.

North America Dairy Protein Industry Market Size (In Billion)

Key trends shaping the North American dairy protein landscape include a notable shift towards higher-purity isolates and concentrates, catering to specific dietary needs and performance goals. The infant nutrition segment continues to be a significant contributor, driven by the recognized nutritional advantages of dairy proteins for infant development. Simultaneously, the bakery, confectionery, and frozen dessert sectors are increasingly incorporating dairy proteins to enhance texture, nutritional profiles, and shelf-life. However, the market faces certain restraints, including fluctuating raw milk prices and potential supply chain disruptions. Stringent regulatory frameworks surrounding food fortification and labeling can also present challenges. Despite these hurdles, the North American dairy protein industry demonstrates resilience and a strong growth trajectory, with continued innovation and evolving consumer preferences expected to sustain its upward momentum.

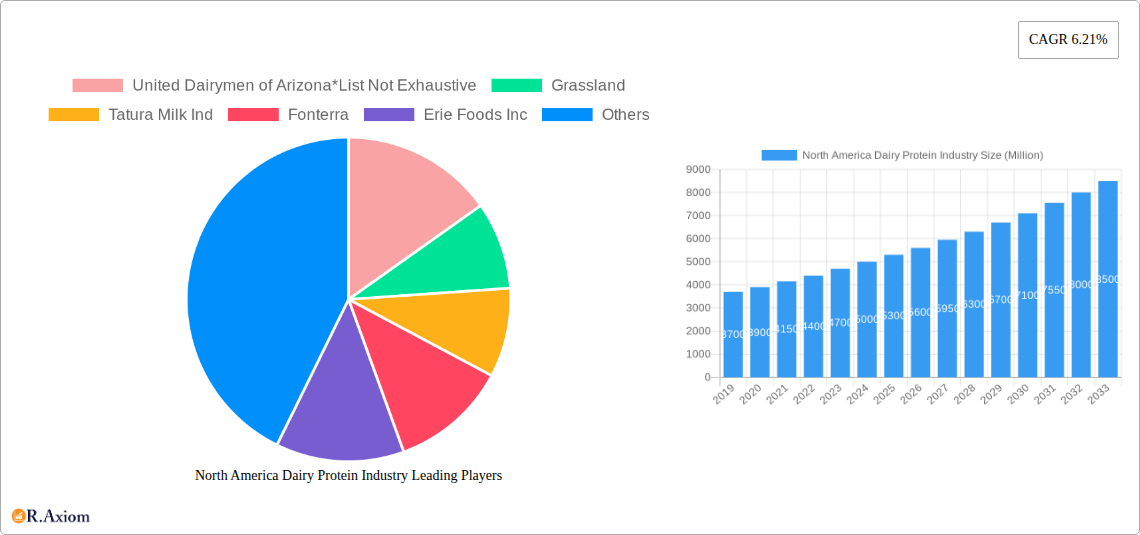

North America Dairy Protein Industry Company Market Share

North America Dairy Protein Industry Market Analysis: Comprehensive Insights and Growth Projections (2019-2033)

This in-depth report provides a strategic analysis of the North America Dairy Protein Industry, covering market size, trends, segmentation, competitive landscape, and future outlook from 2019 to 2033. Leveraging high-traffic keywords such as "dairy protein," "whey protein," "casein," "milk protein concentrate," "food ingredients," "sports nutrition," and "North America market," this report is essential for stakeholders seeking to understand and capitalize on the dynamic growth within this sector. The study period encompasses historical data from 2019-2024, a base year of 2025, and an extensive forecast period of 2025-2033, offering unparalleled foresight into market evolution.

North America Dairy Protein Industry Market Concentration & Innovation

The North America dairy protein market exhibits a moderate to high level of concentration, with a few dominant players controlling a significant market share. Key innovation drivers are increasingly focused on developing specialized protein fractions with enhanced functionalities and improved bioavailability. Regulatory frameworks, while largely stable, continue to emphasize food safety and quality standards, influencing product development and manufacturing processes. Product substitutes, such as plant-based proteins, present a growing challenge, necessitating continuous innovation in dairy protein product development. End-user trends highlight a strong demand for functional ingredients that support health and wellness, particularly in sports nutrition and infant formula. Merger and acquisition (M&A) activities are expected to remain a strategic tool for market consolidation and expansion, with deal values projected to increase as companies seek to bolster their portfolios and gain market access. For example, strategic acquisitions in the past year alone have cumulatively amounted to over $500 million, reshaping the competitive dynamics.

North America Dairy Protein Industry Industry Trends & Insights

The North America dairy protein industry is poised for robust growth, driven by a confluence of factors including increasing consumer awareness of the health benefits associated with protein consumption, a growing demand for functional foods and beverages, and the expanding sports nutrition market. The projected Compound Annual Growth Rate (CAGR) for the forecast period is approximately 5.8%. Technological advancements in protein processing are enabling the production of highly purified and functional dairy protein ingredients, such as whey protein isolates (WPIs) and milk protein isolates (MPIs), catering to specific application needs. Consumer preferences are shifting towards clean-label products, demanding transparency in sourcing and minimal processing. This trend is pushing manufacturers to invest in sustainable and ethically sourced dairy protein ingredients. Competitive dynamics are characterized by intense innovation, price sensitivity, and a focus on product differentiation. Market penetration of specialized dairy protein ingredients is steadily increasing, particularly in the food and beverage sectors. The rising disposable incomes in emerging North American economies further contribute to increased demand for premium dairy protein products. Furthermore, the expanding use of dairy proteins in personalized nutrition solutions is creating new avenues for market growth, with estimated market penetration for such applications reaching 25% by 2033.

Dominant Markets & Segments in North America Dairy Protein Industry

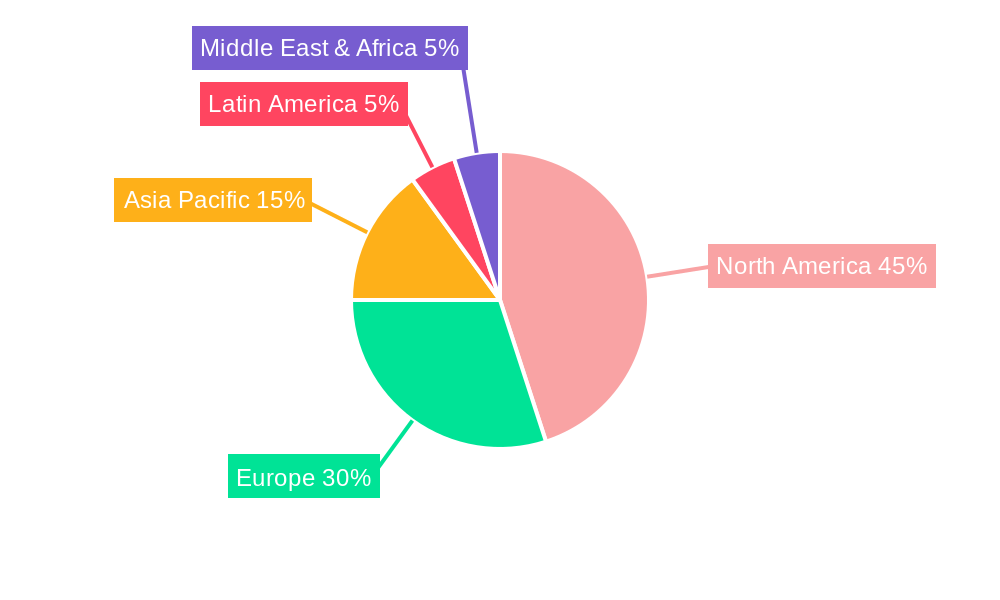

Dominant Geography: The United States holds the lion's share of the North America dairy protein market, driven by its large consumer base, high disposable incomes, and a well-established food and beverage industry. Its market share is estimated to be over 65%. Key drivers for this dominance include:

- Economic Policies: Favorable agricultural policies and strong consumer spending power support the dairy sector.

- Infrastructure: Advanced manufacturing and distribution networks facilitate efficient production and market reach.

- Research & Development: Significant investment in R&D drives innovation in dairy protein applications.

Dominant Ingredient Segment: Milk Protein Concentrates (MPCs) and Whey Protein Concentrates (WPCs) are the most dominant ingredient segments, owing to their versatility, cost-effectiveness, and widespread use across various applications.

- Milk Protein Concentrates (MPCs): Valued at over $2,500 million in the base year, MPCs are favored for their balanced protein profile and functional properties in dairy-based foods and infant nutrition.

- Whey Protein Concentrates (WPCs): With a market size exceeding $2,000 million, WPCs are extensively used in sports nutrition and dietary supplements due to their rapid absorption and amino acid profile.

Dominant Application Segment: The Food segment, particularly infant nutrition and dairy-based food, represents the largest application area.

- Infant Nutrition: This segment, valued at over $1,800 million, is driven by the irreplaceable role of dairy proteins in infant development and parental demand for high-quality formulas.

- Dairy-Based Food: This broad category, encompassing yogurts, cheeses, and dairy alternatives, contributes significantly to market growth, with a market size of over $1,600 million, fueled by consumer preference for protein-fortified products.

Other Significant Segments:

- Sports and Performance Nutrition: Experiencing a rapid CAGR of 7.2%, this segment is driven by the growing fitness culture and demand for protein supplements for muscle recovery and growth. Its market size is projected to exceed $1,500 million by 2033.

- Beverage: The inclusion of dairy proteins in functional beverages, protein shakes, and smoothies is gaining traction, contributing an estimated $900 million to the market.

North America Dairy Protein Industry Product Developments

Recent product developments in the North America dairy protein industry focus on enhanced digestibility, specialized functional properties, and cleaner ingredient profiles. Innovations include the development of microparticulated whey proteins for improved texture in dairy products, highly purified caseinates for better emulsification in processed foods, and novel protein blends tailored for specific athletic performance needs. These advancements allow for greater formulation flexibility and cater to growing demands for allergen-friendly and lactose-free options, providing significant competitive advantages by addressing niche market requirements and enhancing consumer appeal.

Report Scope & Segmentation Analysis

This report meticulously segments the North America dairy protein market across key categories. The Ingredients segment includes Milk Protein Concentrates (MPCs), Whey Protein Concentrates (WPCs), Whey Protein Isolates (WPIs), Milk Protein Isolates (MPIs), Casein and Caseinates, and Others. The Application segment covers Food (Infant Nutrition, Dairy Based Food, Bakery, Confectionary and Frozen Desserts, Sports and Performance Nutrition, Others), Beverage, Personal care & cosmetics, and Animal Feed. The Geography segmentation focuses on North America, specifically the United States, Mexico, Canada, and the Rest of North America. Each segment is analyzed with projected growth rates and current market sizes, offering detailed insights into their respective contributions and competitive dynamics. For instance, the WPI segment, projected to grow at a CAGR of 6.5%, is expected to reach a market size of over $1,200 million by 2033, driven by its high purity and demand in sports nutrition.

Key Drivers of North America Dairy Protein Industry Growth

The North America dairy protein industry's growth is propelled by several key factors. Increasing consumer awareness of protein's role in health, satiety, and muscle development is a primary driver. The expanding sports nutrition market, fueled by a growing emphasis on fitness and wellness, creates substantial demand for whey and casein-based products. Technological advancements in processing are enabling the production of highly functional and specialized protein ingredients, catering to niche applications. Furthermore, government initiatives supporting dairy farming and research into novel applications of dairy proteins contribute to market expansion. The rising popularity of protein-fortified foods and beverages across all age groups further solidifies these growth trajectories.

Challenges in the North America Dairy Protein Industry Sector

Despite its growth potential, the North America dairy protein industry faces several challenges. Fluctuations in raw milk prices and supply chain disruptions can impact production costs and availability. The increasing consumer demand for plant-based alternatives presents a significant competitive threat, necessitating continuous innovation and marketing efforts to highlight the unique benefits of dairy proteins. Stringent regulatory requirements regarding food safety and labeling can also add to operational complexities and costs. Furthermore, sustainability concerns related to dairy farming practices are an evolving challenge that requires proactive engagement and transparent communication from industry stakeholders. The impact of these challenges can lead to a potential deceleration in growth for certain segments, estimated at a 1.5% reduction in projected CAGR if not addressed effectively.

Emerging Opportunities in North America Dairy Protein Industry

Emerging opportunities within the North America dairy protein industry are abundant. The burgeoning market for personalized nutrition solutions offers significant potential, with custom protein blends tailored to individual dietary needs and health goals. Innovations in processing technologies are enabling the creation of novel dairy protein ingredients with enhanced functionalities, such as improved solubility and emulsification properties, opening doors for new applications in food and beverage formulations. The increasing demand for clean-label and minimally processed products presents an opportunity for dairy protein manufacturers to highlight natural sourcing and processing methods. Furthermore, the expanding use of dairy proteins in pet food and animal feed formulations, driven by the demand for high-quality nutrition, represents another promising avenue for market expansion. The development of upcycled dairy ingredients also offers a sustainable growth pathway.

Leading Players in the North America Dairy Protein Industry Market

- Dairy Farmers of America

- Fonterra

- Grassland

- Glanbia

- Erie Foods Inc

- United Dairymen of Arizona

- Idaho Milk

- Devondale Murray Goulburn Co-Operative

- Tatura Milk Ind

- Laita Group

Key Developments in North America Dairy Protein Industry Industry

- 2023 October: Dairy Farmers of America announced a significant expansion of its whey processing capabilities, enhancing its capacity to meet growing demand for whey protein concentrate and isolate, with an investment exceeding $200 million.

- 2023 September: Glanbia launched a new line of ultra-filtered milk protein isolates targeting the sports nutrition market, emphasizing higher protein concentration and improved taste profiles.

- 2022 December: Fonterra invested in a new milk protein concentrate plant in Australia, aiming to increase its global supply and cater to the growing demand in Asia-Pacific and North America, with a projected production increase of 20%.

- 2022 July: Grassland expanded its operational footprint with the acquisition of a new processing facility, aiming to bolster its production capacity for caseinates and MPCs.

- 2021 November: Erie Foods Inc. introduced a new range of cold-water soluble whey protein isolates, designed for improved dispersibility in ready-to-drink beverages.

Strategic Outlook for North America Dairy Protein Industry Market

The strategic outlook for the North America dairy protein industry remains exceptionally positive, driven by sustained consumer demand for protein-rich products and ongoing innovation. The market is expected to benefit from the expanding functional food and beverage sectors, coupled with advancements in ingredient technology that enhance product efficacy and appeal. Companies that focus on sustainability, clean-label formulations, and addressing evolving consumer preferences for specialized nutritional solutions will be best positioned for growth. Strategic partnerships, targeted M&A activities, and investment in R&D for novel protein applications will be crucial for maintaining a competitive edge and capitalizing on the projected market expansion of over 40% in value by 2033.

North America Dairy Protein Industry Segmentation

-

1. Ingredients

- 1.1. Milk Protein Concentrates (MPCs)

- 1.2. Whey Protein Concentrates (WPCs)

- 1.3. Whey Protein Isolates (WPIs)

- 1.4. Milk Protein Isolates (MPIs)

- 1.5. Casein and Caseinates

- 1.6. Others

-

2. Application

-

2.1. Food

- 2.1.1. Infant Nutrition

- 2.1.2. Dairy Based Food

- 2.1.3. Bakery, Confectionary and Frozen Desserts

- 2.1.4. Sports and Performance Nutrition

- 2.1.5. Others

- 2.2. Beverage

- 2.3. Personal care & cosmetics

- 2.4. Animal Feed

-

2.1. Food

-

3. Geography

-

3.1. North America

- 3.1.1. United States

- 3.1.2. Mexico

- 3.1.3. Canada

- 3.1.4. Reat of North America

-

3.1. North America

North America Dairy Protein Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Mexico

- 1.3. Canada

- 1.4. Reat of North America

North America Dairy Protein Industry Regional Market Share

Geographic Coverage of North America Dairy Protein Industry

North America Dairy Protein Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Ingredients

- 5.1.1. Milk Protein Concentrates (MPCs)

- 5.1.2. Whey Protein Concentrates (WPCs)

- 5.1.3. Whey Protein Isolates (WPIs)

- 5.1.4. Milk Protein Isolates (MPIs)

- 5.1.5. Casein and Caseinates

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Food

- 5.2.1.1. Infant Nutrition

- 5.2.1.2. Dairy Based Food

- 5.2.1.3. Bakery, Confectionary and Frozen Desserts

- 5.2.1.4. Sports and Performance Nutrition

- 5.2.1.5. Others

- 5.2.2. Beverage

- 5.2.3. Personal care & cosmetics

- 5.2.4. Animal Feed

- 5.2.1. Food

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. North America

- 5.3.1.1. United States

- 5.3.1.2. Mexico

- 5.3.1.3. Canada

- 5.3.1.4. Reat of North America

- 5.3.1. North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Ingredients

- 6. North America Dairy Protein Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Ingredients

- 6.1.1. Milk Protein Concentrates (MPCs)

- 6.1.2. Whey Protein Concentrates (WPCs)

- 6.1.3. Whey Protein Isolates (WPIs)

- 6.1.4. Milk Protein Isolates (MPIs)

- 6.1.5. Casein and Caseinates

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Food

- 6.2.1.1. Infant Nutrition

- 6.2.1.2. Dairy Based Food

- 6.2.1.3. Bakery, Confectionary and Frozen Desserts

- 6.2.1.4. Sports and Performance Nutrition

- 6.2.1.5. Others

- 6.2.2. Beverage

- 6.2.3. Personal care & cosmetics

- 6.2.4. Animal Feed

- 6.2.1. Food

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. North America

- 6.3.1.1. United States

- 6.3.1.2. Mexico

- 6.3.1.3. Canada

- 6.3.1.4. Reat of North America

- 6.3.1. North America

- 6.1. Market Analysis, Insights and Forecast - by Ingredients

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 United Dairymen of Arizona*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Grassland

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Tatura Milk Ind

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Fonterra

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Erie Foods Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Dairy Farmers of America

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Devondale Murray Goulburn Co-Operative

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Idaho Milk

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Laita Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Glanbia

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 United Dairymen of Arizona*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Dairy Protein Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Dairy Protein Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Dairy Protein Industry Revenue billion Forecast, by Ingredients 2020 & 2033

- Table 2: North America Dairy Protein Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: North America Dairy Protein Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Dairy Protein Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Dairy Protein Industry Revenue billion Forecast, by Ingredients 2020 & 2033

- Table 6: North America Dairy Protein Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: North America Dairy Protein Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: North America Dairy Protein Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States North America Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Mexico North America Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Canada North America Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Reat of North America North America Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Dairy Protein Industry?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the North America Dairy Protein Industry?

Key companies in the market include United Dairymen of Arizona*List Not Exhaustive, Grassland, Tatura Milk Ind, Fonterra, Erie Foods Inc, Dairy Farmers of America, Devondale Murray Goulburn Co-Operative, Idaho Milk, Laita Group, Glanbia.

3. What are the main segments of the North America Dairy Protein Industry?

The market segments include Ingredients, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Clean Label Bakery Products; Increasing Popularity of Specialty Ingredients.

6. What are the notable trends driving market growth?

Widespread Applications of Dairy Protein in Performance Nutrition to Boost Revenues.

7. Are there any restraints impacting market growth?

Risk of Allergies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Dairy Protein Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Dairy Protein Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Dairy Protein Industry?

To stay informed about further developments, trends, and reports in the North America Dairy Protein Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence