Key Insights

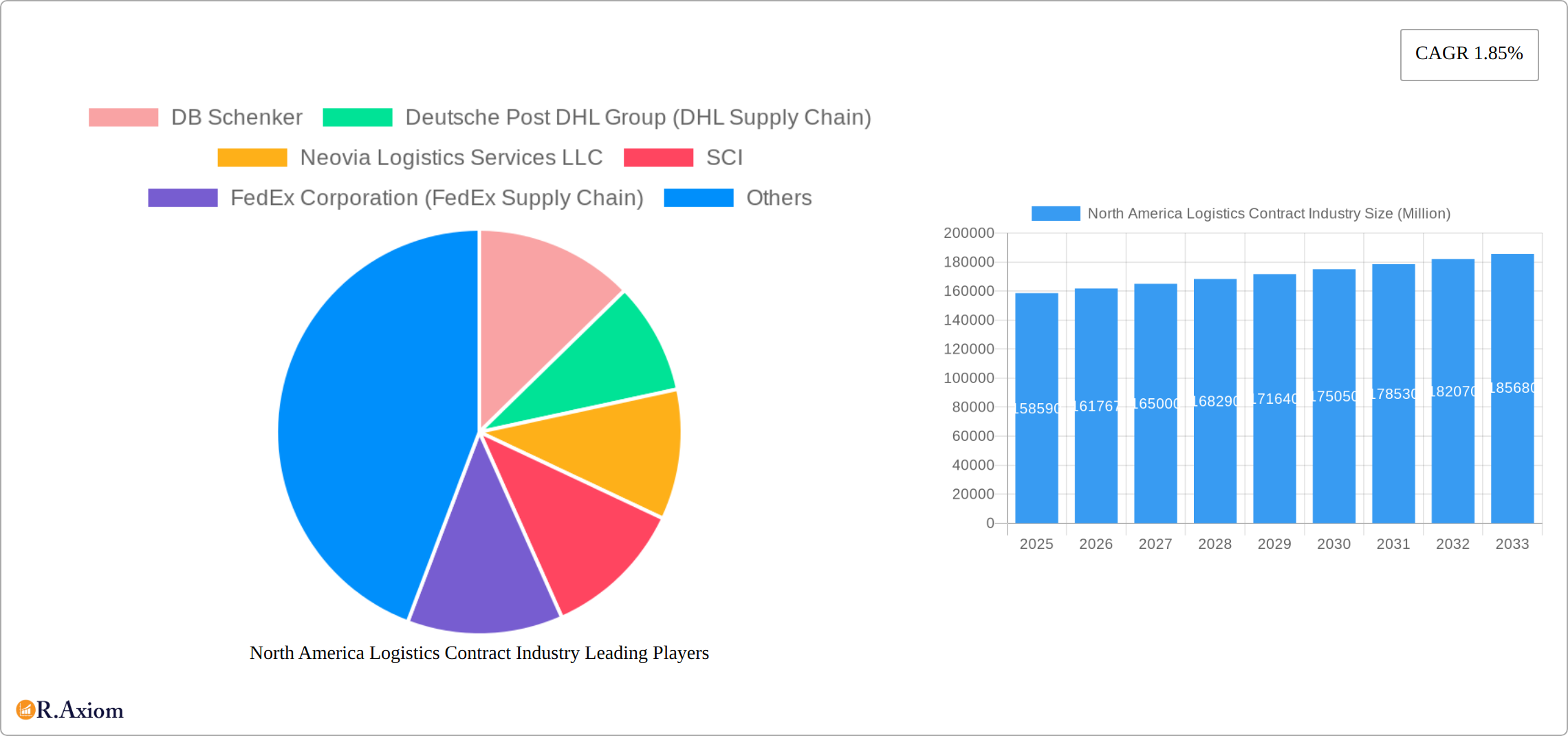

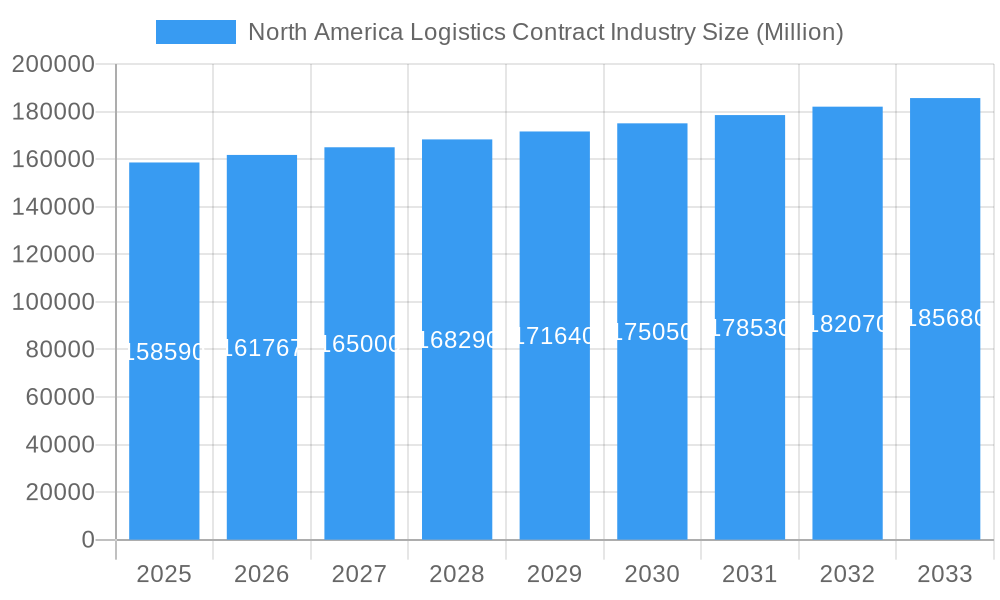

The North American logistics contract industry, valued at $158.59 billion in 2025, exhibits a steady growth trajectory, projected to expand at a compound annual growth rate (CAGR) of 1.85% from 2025 to 2033. This growth is fueled by several key factors. The increasing e-commerce penetration necessitates efficient and reliable supply chain solutions, driving demand for contract logistics services. Furthermore, the automotive and manufacturing sectors, significant end-users of these services, are experiencing ongoing expansion, particularly in North America, further boosting market demand. The rising adoption of advanced technologies like automation, AI, and data analytics within logistics operations contributes to increased efficiency and cost optimization, making contract logistics a more attractive option for businesses of all sizes. However, factors like fluctuating fuel prices and driver shortages pose challenges to sustained growth. The industry is also witnessing a shift towards specialized services catering to specific industry needs, such as temperature-controlled logistics for pharmaceuticals and specialized handling for high-tech components. Competition among established players like DB Schenker, DHL Supply Chain, and FedEx Supply Chain is intense, spurring innovation and driving down costs for clients.

North America Logistics Contract Industry Market Size (In Billion)

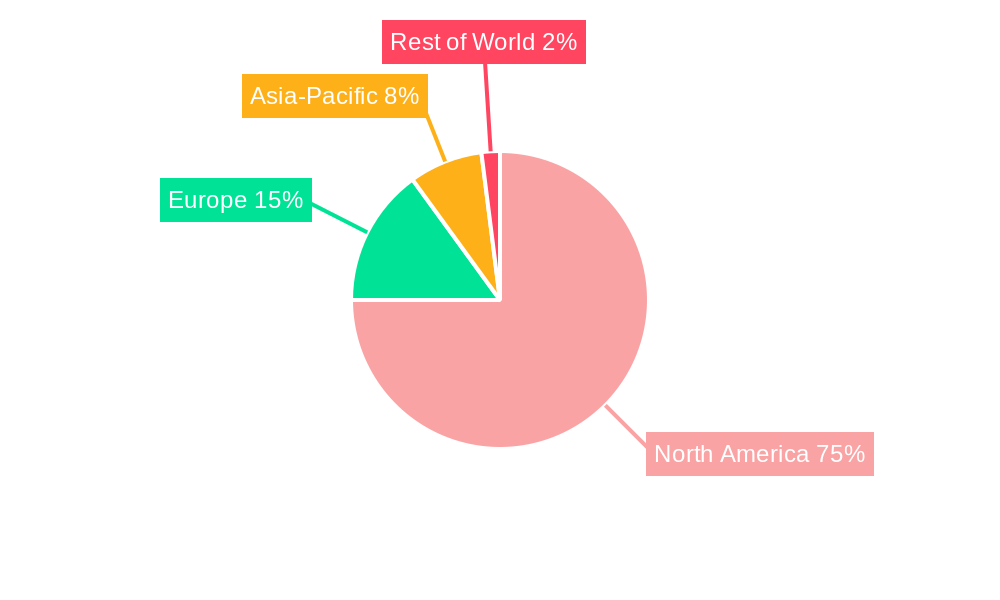

The segmented market reveals significant regional variations. While the United States dominates the North American market, Canada and Mexico present substantial growth opportunities. The "Insourced" segment, while holding a significant share, is projected to see slower growth than the "Outsourced" segment due to businesses increasingly outsourcing non-core functions for greater operational flexibility and cost efficiency. Within end-user segments, the manufacturing and automotive sectors are the largest contributors, followed by consumer goods and retail. The high-tech and healthcare sectors are also exhibiting significant growth, driven by their need for specialized handling and stringent regulatory compliance. The overall forecast suggests a positive outlook for the North American logistics contract industry, with continued growth driven by technological advancements, e-commerce expansion, and the evolving needs of diverse end-user sectors. However, businesses operating within this space must adapt to challenges like workforce availability and economic fluctuations to maintain profitability and market share.

North America Logistics Contract Industry Company Market Share

North America Logistics Contract Industry Market Concentration & Innovation

This comprehensive report analyzes the North America logistics contract industry, examining market concentration, innovation drivers, regulatory landscapes, and competitive dynamics from 2019-2033. The study delves into the impact of mergers and acquisitions (M&A) activities, evaluating deal values and their influence on market share distribution amongst key players like DB Schenker, DHL Supply Chain, FedEx Supply Chain, and UPS Supply Chain Solutions. We assess the innovative technologies shaping the sector, including automation, AI, and blockchain, and examine their adoption rates and impact on operational efficiency. Furthermore, the report explores the evolving regulatory environment and its implications for industry players, considering factors such as trade agreements and environmental regulations. Finally, the report provides detailed analysis of end-user trends across various sectors, including manufacturing, consumer goods, and healthcare, and offers insights into substitution effects driven by alternative logistics solutions. Key metrics such as market share held by leading players and the total value of M&A deals concluded during the study period will be presented.

- Market Share Analysis: Detailed breakdown of market share held by top players (e.g., DHL, FedEx, UPS) and emerging competitors.

- M&A Activity: Analysis of significant M&A transactions, including deal values and strategic implications for the market.

- Innovation Drivers: Examination of technological advancements, including automation, AI, and data analytics, driving industry transformation.

- Regulatory Landscape: Assessment of the regulatory framework's impact on market growth and competition.

- End-User Trends: Analysis of changing demand patterns across various industries.

North America Logistics Contract Industry Industry Trends & Insights

This report delivers a comprehensive analysis of the North American contract logistics market from 2019 to 2033, examining key growth drivers, technological disruptions, evolving consumer expectations, and the fiercely competitive landscape. Utilizing a robust blend of quantitative and qualitative data, the report provides detailed market trend analysis and forecasts, including compound annual growth rate (CAGR) and market penetration rates across various segments. We delve into the significant impact of e-commerce expansion, supply chain optimization strategies, and the accelerating adoption of advanced technologies such as robotics, artificial intelligence (AI), and the Internet of Things (IoT) on market expansion. The analysis further explores how shifting consumer preferences for faster, more transparent, and sustainable delivery options are influencing industry dynamics. We also examine how competitive pressures are shaping pricing strategies, service offerings, and the overall market evolution. Finally, the report offers a forward-looking perspective, projecting growth trajectories and identifying key challenges and opportunities poised to shape the future of the industry.

Dominant Markets & Segments in North America Logistics Contract Industry

This report pinpoints the dominant regions, countries, and segments within the North American contract logistics industry, drawing on data from 2019-2033. While the United States, with its substantial economy and advanced infrastructure, maintains a leading market position, we analyze the growth potential of Canada and Mexico, considering key factors like economic development, trade agreements (e.g., USMCA), and infrastructure investments. The market segmentation analysis encompasses contract logistics by type (insourced vs. outsourced) and end-user industry (manufacturing, automotive, consumer goods, high-tech, healthcare, and others). We identify the segments exhibiting the highest market share and growth rates, providing a detailed explanation of the factors driving this dominance. This includes an in-depth examination of regional variations within the United States and the unique characteristics of the Canadian and Mexican markets.

- By Type:

- Insourced: A comprehensive analysis of the market size, growth trends, and key characteristics of insourced contract logistics, including cost structures and operational efficiencies.

- Outsourced: A detailed examination of the market size, growth trends, and key benefits of outsourced contract logistics, including access to specialized expertise and scalability.

- By End User:

- Manufacturing and Automotive: In-depth analysis of market size, growth drivers (e.g., automation needs, Just-in-Time manufacturing), challenges (e.g., supply chain disruptions), and key players, including case studies of successful partnerships.

- Consumer Goods and Retail: Analysis of market size, growth drivers (e.g., e-commerce boom, omnichannel fulfillment), challenges (e.g., last-mile delivery complexities), and key players, with a focus on omnichannel strategies.

- High-tech: Analysis of market size, growth drivers (e.g., complex supply chains, specialized handling requirements), challenges (e.g., managing high-value goods), and key players, including an examination of reverse logistics.

- Healthcare and Pharmaceuticals: Analysis of market size, growth drivers (e.g., temperature-sensitive goods, stringent regulatory compliance), challenges (e.g., cold chain management), and key players, with specific attention to GDP (Good Distribution Practices).

- Other End Users: An overview of other end-user sectors and their contributions to the overall market, including emerging sectors and their specific logistics needs.

- By Country:

- United States: A detailed analysis of the US market, including key regional variations, infrastructure strengths and weaknesses, and significant regulatory aspects.

- Canada: An analysis of the Canadian market, considering factors such as infrastructure, trade relations with the US, and regional economic disparities.

- Mexico: An analysis of the Mexican market, focusing on its role within North American supply chains, nearshoring trends, and its evolving infrastructure.

North America Logistics Contract Industry Product Developments

The North American contract logistics industry is experiencing significant product innovation, driven by technological advancements and evolving customer needs. The integration of automation technologies like robotics and AI-powered solutions is enhancing efficiency and reducing operational costs. Furthermore, the adoption of advanced data analytics and real-time tracking systems provides enhanced visibility and control throughout the supply chain. This leads to improved decision-making and optimized inventory management. These innovations deliver competitive advantages for companies offering superior speed, accuracy, and transparency in their logistics solutions, thereby shaping the competitive landscape of the market.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North America logistics contract industry, covering the period 2019-2033. The base year is 2025, and the forecast period extends to 2033. The market is segmented by type (insourced and outsourced), end-user (manufacturing, automotive, consumer goods, high-tech, healthcare and pharmaceuticals, and others), and geography (United States, Canada, and Mexico). For each segment, we present market size, growth projections, and competitive analysis. The report provides insights into growth drivers, challenges, and emerging opportunities for each segment, allowing stakeholders to make informed strategic decisions.

Key Drivers of North America Logistics Contract Industry Growth

The expansion of the North American contract logistics market is propelled by several interconnected drivers. The explosive growth of e-commerce continues to fuel demand for efficient and scalable logistics solutions, significantly driving the adoption of outsourced services. Simultaneously, technological advancements, encompassing automation, AI, and data analytics, are boosting operational efficiency, reducing costs, and enhancing supply chain visibility. Globalization and the increase in cross-border trade necessitate specialized logistics expertise, further stimulating market growth. Finally, evolving regulatory landscapes, including those focused on sustainability, supply chain security, and transparency, are reshaping the industry and creating new opportunities for innovative logistics providers.

Challenges in the North America Logistics Contract Industry Sector

The North American contract logistics industry faces a multitude of challenges. Persistent driver shortages, coupled with fluctuating fuel prices, exert considerable pressure on operational costs and delivery times, impacting profitability. The increasingly complex regulatory environment and heightened emphasis on environmental sustainability add layers of complexity and cost. Furthermore, intense competition necessitates continuous innovation and adaptation to evolving technologies, posing ongoing hurdles for firms. This report quantifies the impact of these challenges whenever possible, providing insights into their influence on pricing strategies and overall market dynamics.

Emerging Opportunities in North America Logistics Contract Industry

Despite the challenges, the North American contract logistics market presents a wealth of emerging opportunities. The unrelenting growth of e-commerce continues to drive demand for sophisticated last-mile delivery solutions and specialized warehousing services, including fulfillment centers and micro-fulfillment centers. Technological innovation, particularly in areas such as automation, AI, blockchain, and predictive analytics, offers significant potential to optimize efficiency, enhance transparency, and reduce costs across the entire supply chain. The escalating focus on environmental sustainability is propelling the adoption of eco-friendly logistics practices, creating new market niches for businesses committed to sustainable solutions. These factors are poised to significantly shape the future trajectory of the North American contract logistics industry.

Leading Players in the North America Logistics Contract Industry Market

- DB Schenker

- Deutsche Post DHL Group (DHL Supply Chain)

- Neovia Logistics Services LLC

- SCI

- FedEx Corporation (FedEx Supply Chain)

- United Parcel Service Inc (UPS Supply Chain Solutions)

- Schnedier National

- 3 Other Companies (Key Information/Overview)

- Yusen Logistics Co Ltd

- Penske Logistics Inc

- Kuehne + Nagel International AG

- CEVA Logistics

- PiVAL International

- TIBA

- XPO Logistics Inc

- Americold

- Hellmann Worldwide Logistics GmbH & Co KG

- Geodis

- J B Hunt Transport Services Inc

- Ryder System Inc

Key Developments in North America Logistics Contract Industry Industry

- June 2022: DHL Supply Chain utilized over 100 million LocusBots units across its North American facilities, showcasing significant automation advancements.

- February 2022: Deutsche Post DHL Group invested USD 400 million to expand its healthcare logistics network by 27%, highlighting the industry's focus on the healthcare sector.

Strategic Outlook for North America Logistics Contract Industry Market

The North American contract logistics market exhibits strong future potential, driven by e-commerce growth, technological innovation, and the increasing need for efficient and resilient supply chains. The integration of advanced technologies such as AI, automation, and blockchain will further streamline operations and enhance visibility. Focus on sustainable and environmentally conscious practices will create opportunities for specialized services. Continued market consolidation through M&A activity is expected, resulting in larger, more integrated players capable of providing comprehensive logistics solutions. The overall outlook remains positive, with significant growth anticipated in the coming years.

North America Logistics Contract Industry Segmentation

-

1. Type

- 1.1. Insourced

- 1.2. Outsourced

-

2. End User

- 2.1. Manufacturing and Automotive

- 2.2. Consumer Goods and Retail

- 2.3. High-tech

- 2.4. Healthcare and Pharmaceuticals

- 2.5. Other End Users

North America Logistics Contract Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Logistics Contract Industry Regional Market Share

Geographic Coverage of North America Logistics Contract Industry

North America Logistics Contract Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Insourced

- 5.1.2. Outsourced

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing and Automotive

- 5.2.2. Consumer Goods and Retail

- 5.2.3. High-tech

- 5.2.4. Healthcare and Pharmaceuticals

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Logistics Contract Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Insourced

- 6.1.2. Outsourced

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing and Automotive

- 6.2.2. Consumer Goods and Retail

- 6.2.3. High-tech

- 6.2.4. Healthcare and Pharmaceuticals

- 6.2.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Deutsche Post DHL Group (DHL Supply Chain)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Neovia Logistics Services LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SCI

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FedEx Corporation (FedEx Supply Chain)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 United Parcel Service Inc (UPS Supply Chain Solutions)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Schnedier National*6 3 Other Companies (Key Information/Overview)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yusen Logistics Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Penske Logistics Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kuehne + Nagel International AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 CEVA Logistics

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 PiVAL International

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 TIBA

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 XPO Logistics Inc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Americold

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Hellmann Worldwide Logistics GmbH & Co KG

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Geodis

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 J B Hunt Transport Services Inc

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Ryder System Inc

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Logistics Contract Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Logistics Contract Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Logistics Contract Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: North America Logistics Contract Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: North America Logistics Contract Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: North America Logistics Contract Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: North America Logistics Contract Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: North America Logistics Contract Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Logistics Contract Industry?

The projected CAGR is approximately 1.85%.

2. Which companies are prominent players in the North America Logistics Contract Industry?

Key companies in the market include DB Schenker, Deutsche Post DHL Group (DHL Supply Chain), Neovia Logistics Services LLC, SCI, FedEx Corporation (FedEx Supply Chain), United Parcel Service Inc (UPS Supply Chain Solutions), Schnedier National*6 3 Other Companies (Key Information/Overview), Yusen Logistics Co Ltd, Penske Logistics Inc, Kuehne + Nagel International AG, CEVA Logistics, PiVAL International, TIBA, XPO Logistics Inc, Americold, Hellmann Worldwide Logistics GmbH & Co KG, Geodis, J B Hunt Transport Services Inc, Ryder System Inc.

3. What are the main segments of the North America Logistics Contract Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 158.59 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increased Outsourcing of Services4.; Increasing Demand For Contract Logistics In Italy. France. And Poland4.; Growth Of Ecommerce Sector Across Europe.

6. What are the notable trends driving market growth?

Growing E-commerce in the Region Driving the Contract Logistics Market.

7. Are there any restraints impacting market growth?

4.; Increasing Competition In The European Contract Logistics Market.

8. Can you provide examples of recent developments in the market?

Jun 2022: DHL Supply Chain, in contract logistics in the Americas and a division of Deutsche Post DHL Group, revealed that LocusBots from Locus Robotics had selected more than 100 million units in its North American facilities. The achievement was made at the DHL facility in Hanover Township, Pennsylvania, while completing orders for a significant clothes retailer. The facility where the milestone was reached is one of over a dozen DHL locations in North America that employ more than 2,000 LocusBots-more than any other contract logistics provider.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Logistics Contract Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Logistics Contract Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Logistics Contract Industry?

To stay informed about further developments, trends, and reports in the North America Logistics Contract Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence