Key Insights

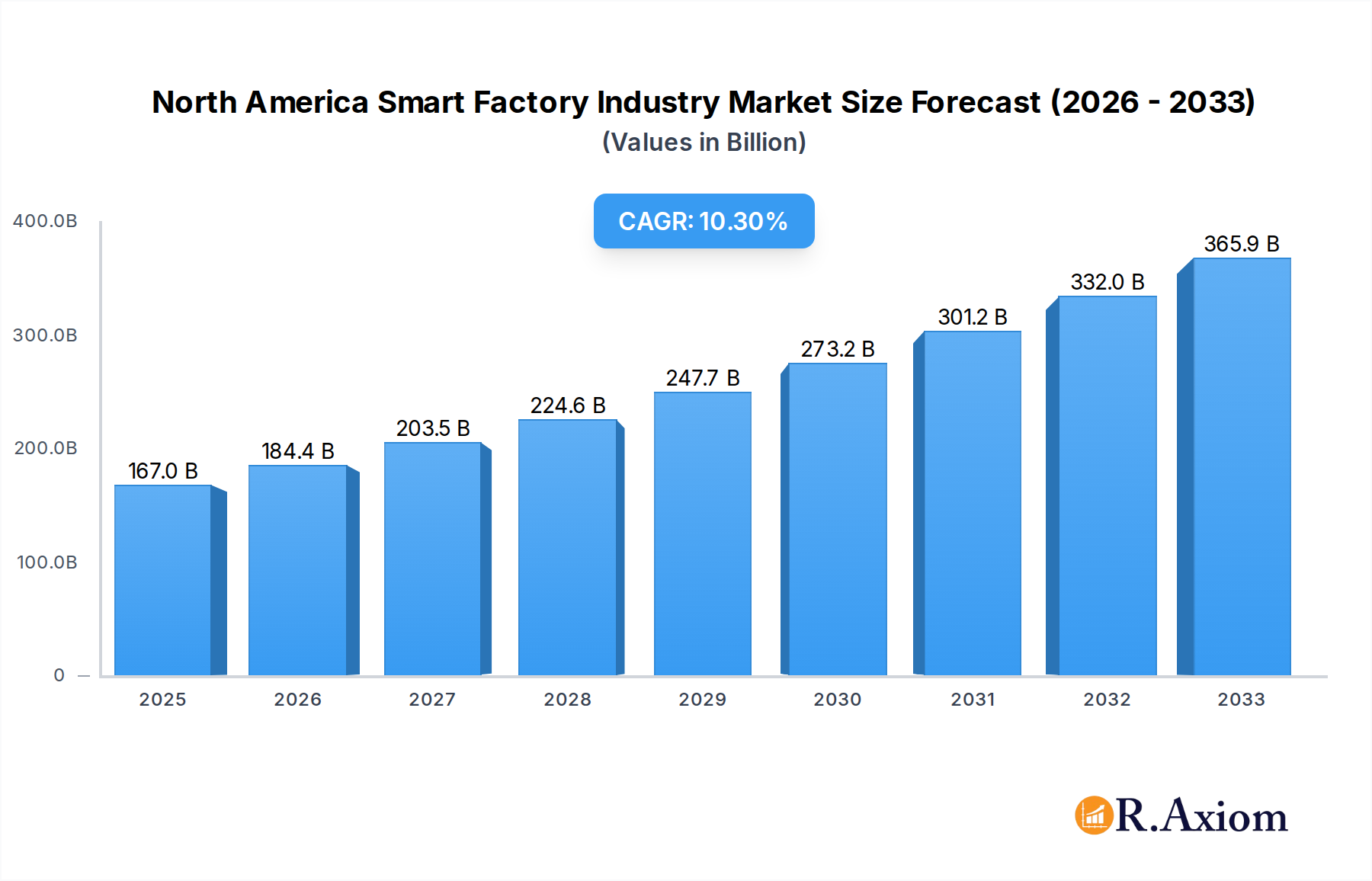

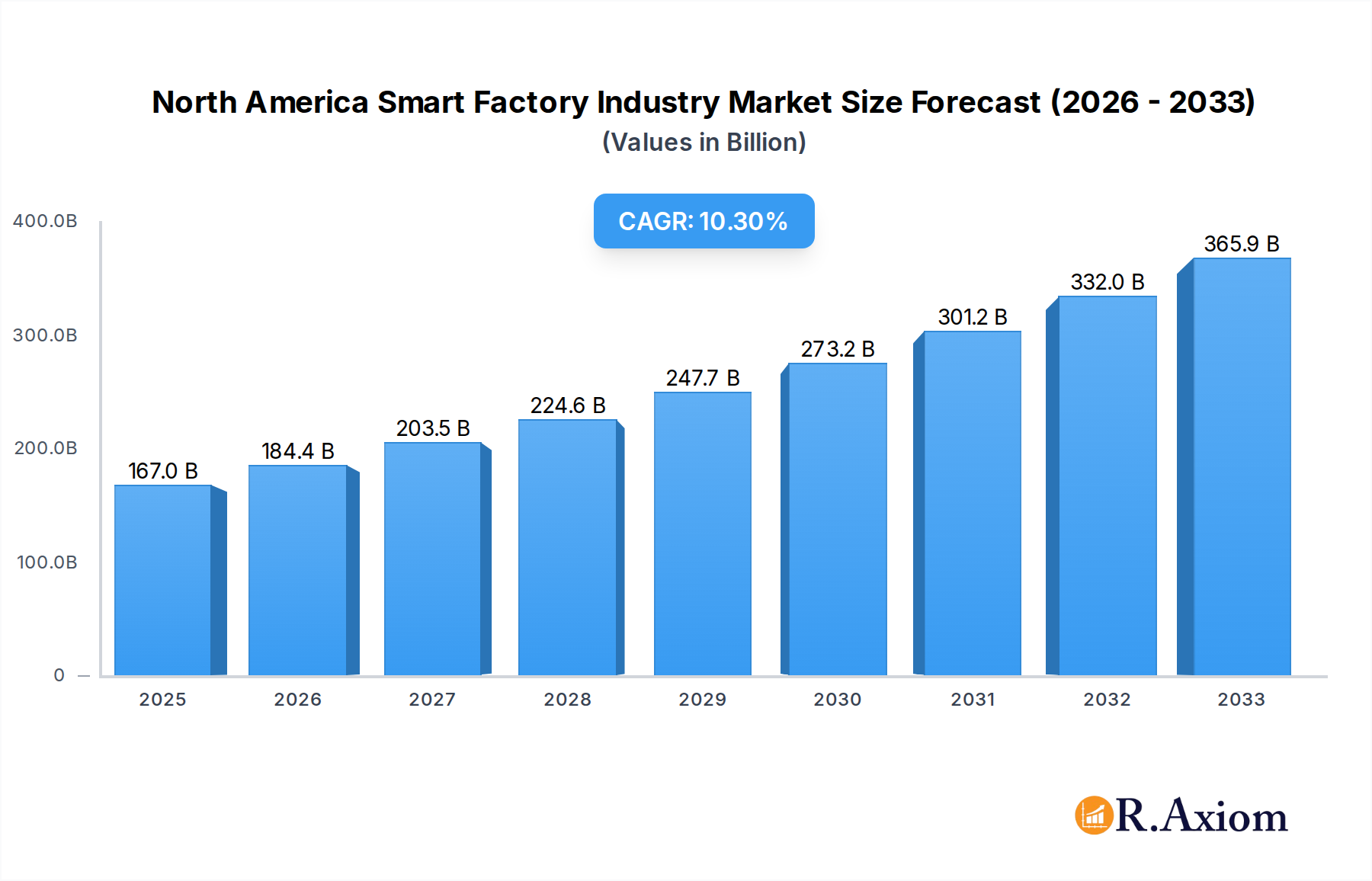

The North America smart factory market is poised for substantial growth, projected to reach an estimated USD 167.02 billion in 2025. This robust expansion is driven by an impressive Compound Annual Growth Rate (CAGR) of 10.49% throughout the forecast period of 2025-2033. This remarkable growth signifies a rapid adoption of advanced automation and digital technologies across various manufacturing sectors in the region. Key drivers fueling this surge include the increasing demand for enhanced productivity, improved operational efficiency, and superior product quality, all of which are hallmarks of smart factory implementations. The imperative to reduce operational costs, minimize human error, and maintain a competitive edge in the global marketplace is pushing North American industries to invest heavily in these transformative solutions. Furthermore, the growing emphasis on supply chain resilience and the need for real-time data-driven decision-making are also significant contributors to the market's upward trajectory.

North America Smart Factory Industry Market Size (In Billion)

The smart factory ecosystem in North America is characterized by a diverse range of products and technologies, catering to a wide spectrum of industrial needs. The market is segmented by Product, encompassing crucial components like Machine Vision Systems (including cameras, processors, and software), Industrial Robotics (ranging from articulated to collaborative robots), Control Devices (relays, switches, and servo motors), Sensors, and Communication Technologies (wired and wireless). On the technology front, solutions such as Product Lifecycle Management (PLM), Human Machine Interface (HMI), Enterprise Resource and Planning (ERP), Manufacturing Execution Systems (MES), and Programmable Logic Controllers (PLC) are integral to creating intelligent manufacturing environments. The automotive and semiconductor industries are leading the charge in smart factory adoption, followed by significant investments from the pharmaceutical, oil and gas, and food and beverage sectors. This widespread integration underscores the pervasive impact of smart factory solutions across the industrial landscape of North America, promising significant advancements in manufacturing capabilities and economic output.

North America Smart Factory Industry Company Market Share

North America Smart Factory Industry Market Concentration & Innovation

The North American smart factory industry is characterized by a moderate to high level of market concentration, driven by significant investments and strategic acquisitions. Key players such as Honeywell International Inc., ABB Ltd, Siemens AG, and Rockwell Automation Inc. hold substantial market shares, often exceeding 10% individually, with their combined dominance approaching 60% of the total market value. Innovation is primarily fueled by the relentless pursuit of operational efficiency, enhanced productivity, and greater automation across diverse end-user industries. This includes the widespread adoption of Industrial Internet of Things (IIoT) technologies, artificial intelligence (AI) for predictive maintenance, and advanced robotics. Regulatory frameworks, while evolving, generally support the transition to smart manufacturing through initiatives promoting digital transformation and cybersecurity standards, aiming to foster a secure and competitive environment. Product substitutes, such as fully manual processes or less integrated automation solutions, are gradually losing ground as the economic and operational benefits of smart factories become undeniable. End-user trends point towards a demand for highly customizable and agile manufacturing processes, pushing for greater flexibility in production lines. Mergers and acquisition (M&A) activities are a significant indicator of market consolidation and strategic expansion, with deal values in recent years reaching billions of dollars, particularly in areas like AI-driven analytics and cybersecurity solutions for industrial environments. For instance, acquisitions focusing on enhancing machine vision capabilities or expanding collaborative robot offerings are common.

North America Smart Factory Industry Industry Trends & Insights

The North American smart factory industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of over 15% throughout the forecast period of 2025-2033. This expansion is propelled by a confluence of powerful market growth drivers, including the escalating demand for increased production efficiency and the imperative to reduce operational costs. Manufacturers are increasingly recognizing the indispensable role of automation and digitalization in maintaining global competitiveness. Technological disruptions are at the forefront of this transformation, with the integration of AI, machine learning, and IIoT platforms revolutionizing manufacturing processes. These technologies enable predictive maintenance, real-time data analytics, and sophisticated supply chain management, leading to optimized resource allocation and minimized downtime. Consumer preferences are also subtly influencing the industry; a growing demand for personalized products and faster delivery cycles necessitates more agile and responsive manufacturing capabilities, which smart factories are uniquely positioned to provide. The competitive dynamics within the North American smart factory landscape are intense, characterized by fierce competition among established industrial giants and emerging technology providers. Companies are actively investing in research and development to innovate and differentiate their offerings, often focusing on integrated solutions that combine hardware, software, and services. Market penetration is steadily increasing across all major end-user industries, with automotive and semiconductors leading the adoption curve due to their inherent need for precision and high-volume output. The value of the North American smart factory market is estimated to reach over $200 billion by 2025 and is poised for further significant growth, exceeding $500 billion by the end of the forecast period. This growth is underpinned by a strong foundation of technological advancements, supportive economic policies, and a growing understanding of the long-term benefits of intelligent manufacturing systems.

Dominant Markets & Segments in North America Smart Factory Industry

The North American smart factory industry exhibits distinct dominance across various segments, reflecting the specific needs and adoption rates of different end-user industries and technological applications. The Automotive sector stands out as a dominant end-user industry, driven by the continuous need for high-volume production, precision, and the integration of advanced robotics and machine vision systems for assembly and quality control. The increasing shift towards electric vehicles (EVs) and autonomous driving technology further amplifies this demand for sophisticated manufacturing solutions.

Within the Product segmentation, Industrial Robotics commands a significant market share, with articulated robots and collaborative industry robots (cobots) witnessing substantial adoption. Cobots, in particular, are gaining traction due to their flexibility, ease of integration, and ability to work alongside human operators, enhancing safety and productivity. Machine Vision Systems, encompassing cameras, processors, and software, are also crucial, playing a vital role in quality inspection, defect detection, and process monitoring across various manufacturing lines.

In the Technology segment, Programmable Logic Controllers (PLCs) and Manufacturing Execution Systems (MES) are foundational, forming the backbone of industrial automation and operational management. The growing integration of Supervisory Controller and Data Acquisition (SCADA) systems with IIoT platforms is enabling real-time data collection and enhanced control over complex manufacturing processes.

Key drivers for the dominance of these segments include:

- Economic Policies: Government initiatives promoting advanced manufacturing and Industry 4.0 adoption, such as tax incentives and grants for technology upgrades.

- Infrastructure: The robust existing industrial infrastructure across North America, facilitating the integration of new smart factory solutions.

- Technological Advancements: Continuous innovation in AI, robotics, sensors, and connectivity, making smart factory solutions more powerful, affordable, and accessible.

- Skilled Workforce Development: Increasing focus on training and upskilling the workforce to manage and operate advanced manufacturing technologies.

The Semiconductor industry also represents a highly dominant end-user segment, characterized by its stringent requirements for precision, cleanliness, and automation in wafer fabrication and assembly processes. The demand for advanced sensors and highly sophisticated machine vision systems for microscopic inspection is a key driver here.

North America Smart Factory Industry Product Developments

Product developments in the North American smart factory industry are continuously pushing the boundaries of automation and intelligence. Innovations are focused on enhancing the capabilities of machine vision systems with AI-powered object recognition and defect analysis, making them more accurate and efficient. Industrial robotics are evolving with greater dexterity, collaborative features, and enhanced safety protocols, enabling them to perform more complex tasks alongside human workers. The integration of advanced sensors for real-time condition monitoring and predictive maintenance is also a key trend. Furthermore, the development of integrated software solutions, such as cloud-based MES and PLM platforms, offers manufacturers seamless data flow and improved operational visibility. These advancements collectively contribute to increased production throughput, superior quality control, and optimized resource utilization.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North America Smart Factory Industry, segmented across Product, Technology, and End-user Industry. The Product segmentation includes Machine Vision Systems (Cameras, Processors, Software, Enclosures, Frame Grabbers, Integration Services, Lighting), Industrial Robotics (Articulated Robots, Cartesian Robots, Cylindrical Robots, SCARA Robots, Parallel Robots, Collaborative Industry Robots), Control Devices (Relays and Switches, Servo Motors and Drives), Sensors, and Communication Technologies (Wired, Wireless), alongside Other Products. The Technology segmentation covers Product Lifecycle Management (PLM), Human Machine Interface (HMI), Enterprise Resource and Planning (ERP), Manufacturing Execution System (MES), Distributed Control System (DCS), Supervisory Controller and Data Acquisition (SCADA), and Programmable Logic Controller (PLC), with a category for Other Technologies. The End-user Industry segmentation analyzes Automotive, Semiconductors, Oil and Gas, Chemical and Petrochemical, Pharmaceutical, Aerospace and Defense, Food and Beverage, and Mining, with a segment for Other End-user Industries. Growth projections indicate a substantial expansion in the Industrial Robotics and Machine Vision Systems segments, driven by demand for automation and quality control. The MES and SCADA segments within Technology are also expected to witness significant growth due to the increasing need for real-time data management and process optimization.

Key Drivers of North America Smart Factory Industry Growth

The North American smart factory industry is propelled by several key drivers. Foremost is the pervasive drive for enhanced operational efficiency and cost reduction across all manufacturing sectors. Technological advancements, particularly in AI, IIoT, and robotics, are enabling more sophisticated automation and data-driven decision-making, creating a competitive imperative for adoption. Government initiatives promoting Industry 4.0 and digital transformation, coupled with a growing skilled workforce trained in advanced manufacturing techniques, further accelerate growth. Additionally, the increasing demand for customized products and faster delivery cycles necessitates agile and flexible production capabilities, which smart factories provide. The industry is projected to experience substantial growth, with estimated market expansion exceeding 15% CAGR from 2025 to 2033, reaching hundreds of billions of dollars in value.

Challenges in the North America Smart Factory Industry Sector

Despite its robust growth, the North American smart factory industry faces significant challenges. The high initial investment cost for implementing advanced automation and IIoT solutions can be a substantial barrier, particularly for small and medium-sized enterprises (SMEs). Cybersecurity threats and concerns regarding data privacy are also prominent, requiring robust security protocols and continuous vigilance. A shortage of skilled labor capable of operating and maintaining complex smart factory systems presents another hurdle, necessitating significant investment in workforce training and development. Furthermore, the integration of legacy systems with new technologies can be complex and time-consuming, leading to potential interoperability issues. Supply chain disruptions, as witnessed in recent years, can also impact the availability of critical components and equipment, affecting deployment timelines.

Emerging Opportunities in North America Smart Factory Industry

Emerging opportunities in the North American smart factory industry are abundant, driven by innovation and evolving market demands. The expanding adoption of collaborative robots (cobots) in diverse applications, from assembly lines to logistics, presents a significant growth avenue. The integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance, quality control, and process optimization is creating new value propositions. The increasing focus on sustainable manufacturing practices is also opening doors for smart factory solutions that optimize energy consumption and reduce waste. Furthermore, the burgeoning demand for personalized products and shorter lead times is driving the need for highly flexible and agile manufacturing systems. Opportunities also lie in developing and implementing cybersecurity solutions tailored for industrial environments, ensuring the secure operation of connected factories.

Leading Players in the North America Smart Factory Industry Market

- Honeywell International Inc.

- ABB Ltd

- Cognex Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Fanuc Corporation

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Yokogawa Electric Corporation

- FLIR Systems Inc

- Kuka AG

- Emerson Electric Company

Key Developments in North America Smart Factory Industry Industry

- 2023/08: Siemens AG announced a significant expansion of its digital twin capabilities, integrating AI for enhanced simulation and predictive analysis in manufacturing processes.

- 2023/07: Rockwell Automation Inc. acquired a leading provider of autonomous mobile robot solutions, bolstering its logistics and material handling automation offerings.

- 2023/06: ABB Ltd launched a new generation of collaborative robots designed for enhanced flexibility and ease of use in SMEs.

- 2023/05: Honeywell International Inc. introduced advanced IIoT platform enhancements focused on predictive maintenance and operational intelligence for industrial clients.

- 2023/04: Cognex Corporation unveiled new machine vision systems with significantly improved AI capabilities for faster and more accurate defect detection.

- 2023/03: Fanuc Corporation showcased its latest advancements in AI-driven robotics, focusing on adaptive control and optimized path planning.

- 2023/02: Mitsubishi Electric Corporation expanded its industrial automation portfolio with new smart sensors and IIoT connectivity solutions.

- 2023/01: Schneider Electric SE partnered with a major cloud provider to enhance its industrial software solutions for data analytics and remote monitoring.

Strategic Outlook for North America Smart Factory Industry Market

The strategic outlook for the North American smart factory industry is exceptionally positive, driven by ongoing digital transformation initiatives and the pursuit of operational excellence. The market is expected to witness sustained growth, fueled by increasing investments in automation, AI, and IIoT technologies across a broad spectrum of industries. Companies that focus on delivering integrated, end-to-end solutions, encompassing both hardware and software, along with robust cybersecurity measures, will be well-positioned for success. Strategic partnerships and collaborations will remain crucial for addressing complex integration challenges and expanding market reach. The continuous evolution of regulatory frameworks and the growing demand for sustainable manufacturing will also shape future strategies, emphasizing the importance of agility and innovation in navigating the dynamic landscape. The overall trend points towards a more intelligent, connected, and efficient manufacturing ecosystem.

North America Smart Factory Industry Segmentation

-

1. Product

-

1.1. Machine Vision Systems

- 1.1.1. Cameras

- 1.1.2. Processors

- 1.1.3. Software

- 1.1.4. Enclosures

- 1.1.5. Frame Grabbers

- 1.1.6. Integration Services

- 1.1.7. Lighting

-

1.2. Industrial Robotics

- 1.2.1. Articulated Robots

- 1.2.2. Cartesian Robots

- 1.2.3. Cylindrical Robots

- 1.2.4. SCARA Robots

- 1.2.5. Parallel Robots

- 1.2.6. Collaborative Industry Robots

-

1.3. Control Devices

- 1.3.1. Relays and Switches

- 1.3.2. Servo Motors and Drives

- 1.4. Sensors

-

1.5. Communication Technologies

- 1.5.1. Wired

- 1.5.2. Wireless

- 1.6. Other Products

-

1.1. Machine Vision Systems

-

2. Technology

- 2.1. Product Lifecycle Management (PLM)

- 2.2. Human Machine Interface (HMI)

- 2.3. Enterprise Resource and Planning (ERP)

- 2.4. Manufacturing Execution System (MES)

- 2.5. Distributed Control System (DCS)

- 2.6. Supervisory Controller and Data Acquisition (SCADA

- 2.7. Programmable Logic Controller (PLC)

- 2.8. Other Technologies

-

3. End-user Industry

- 3.1. Automotive

- 3.2. Semiconductors

- 3.3. Oil and Gas

- 3.4. Chemical and Petrochemical

- 3.5. Pharmaceutical

- 3.6. Aerospace and Defense

- 3.7. Food and Beverage

- 3.8. Mining

- 3.9. Other End-user Industries

North America Smart Factory Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

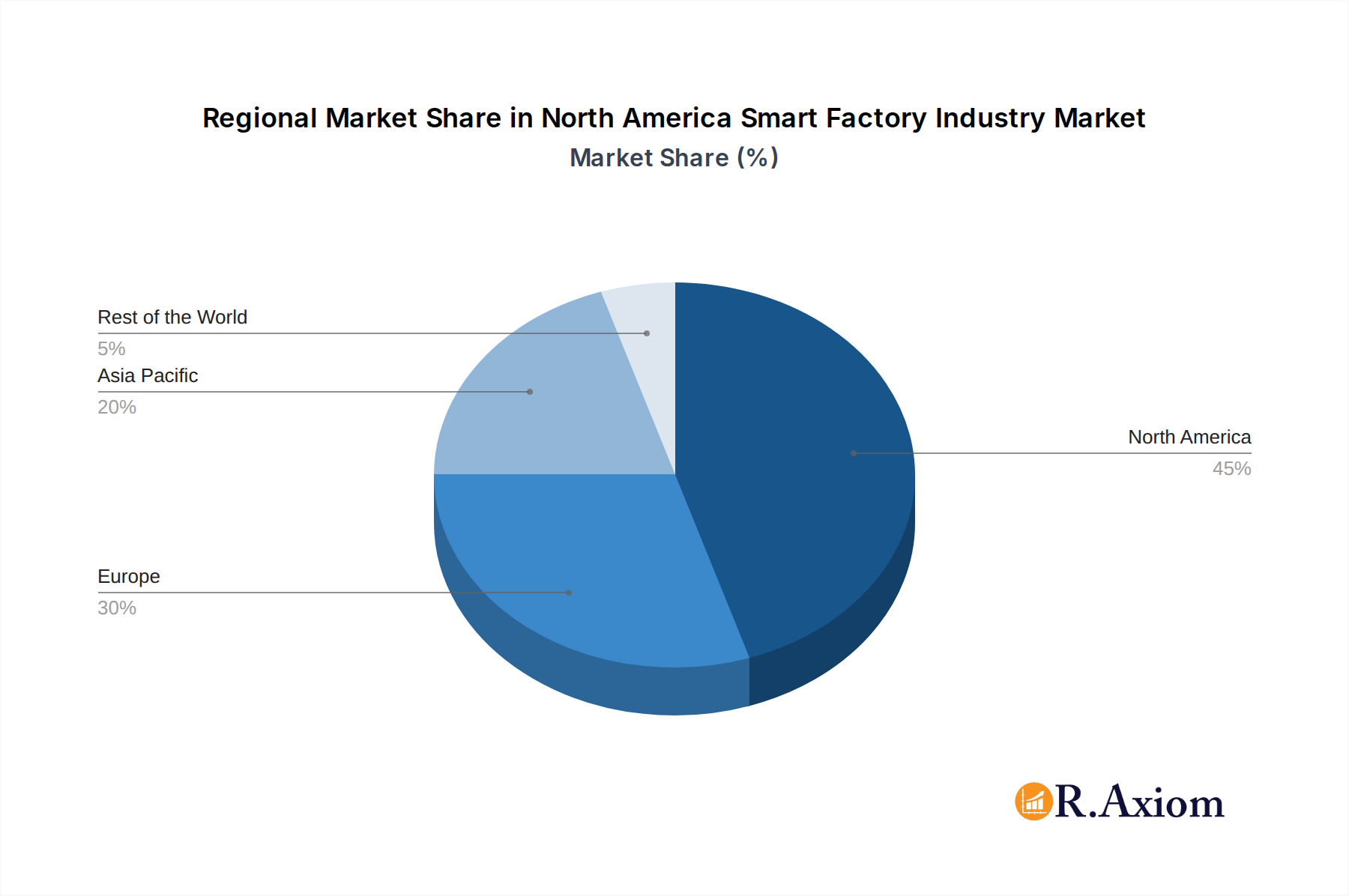

North America Smart Factory Industry Regional Market Share

Geographic Coverage of North America Smart Factory Industry

North America Smart Factory Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Machine Vision Systems

- 5.1.1.1. Cameras

- 5.1.1.2. Processors

- 5.1.1.3. Software

- 5.1.1.4. Enclosures

- 5.1.1.5. Frame Grabbers

- 5.1.1.6. Integration Services

- 5.1.1.7. Lighting

- 5.1.2. Industrial Robotics

- 5.1.2.1. Articulated Robots

- 5.1.2.2. Cartesian Robots

- 5.1.2.3. Cylindrical Robots

- 5.1.2.4. SCARA Robots

- 5.1.2.5. Parallel Robots

- 5.1.2.6. Collaborative Industry Robots

- 5.1.3. Control Devices

- 5.1.3.1. Relays and Switches

- 5.1.3.2. Servo Motors and Drives

- 5.1.4. Sensors

- 5.1.5. Communication Technologies

- 5.1.5.1. Wired

- 5.1.5.2. Wireless

- 5.1.6. Other Products

- 5.1.1. Machine Vision Systems

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Product Lifecycle Management (PLM)

- 5.2.2. Human Machine Interface (HMI)

- 5.2.3. Enterprise Resource and Planning (ERP)

- 5.2.4. Manufacturing Execution System (MES)

- 5.2.5. Distributed Control System (DCS)

- 5.2.6. Supervisory Controller and Data Acquisition (SCADA

- 5.2.7. Programmable Logic Controller (PLC)

- 5.2.8. Other Technologies

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Automotive

- 5.3.2. Semiconductors

- 5.3.3. Oil and Gas

- 5.3.4. Chemical and Petrochemical

- 5.3.5. Pharmaceutical

- 5.3.6. Aerospace and Defense

- 5.3.7. Food and Beverage

- 5.3.8. Mining

- 5.3.9. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Smart Factory Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Machine Vision Systems

- 6.1.1.1. Cameras

- 6.1.1.2. Processors

- 6.1.1.3. Software

- 6.1.1.4. Enclosures

- 6.1.1.5. Frame Grabbers

- 6.1.1.6. Integration Services

- 6.1.1.7. Lighting

- 6.1.2. Industrial Robotics

- 6.1.2.1. Articulated Robots

- 6.1.2.2. Cartesian Robots

- 6.1.2.3. Cylindrical Robots

- 6.1.2.4. SCARA Robots

- 6.1.2.5. Parallel Robots

- 6.1.2.6. Collaborative Industry Robots

- 6.1.3. Control Devices

- 6.1.3.1. Relays and Switches

- 6.1.3.2. Servo Motors and Drives

- 6.1.4. Sensors

- 6.1.5. Communication Technologies

- 6.1.5.1. Wired

- 6.1.5.2. Wireless

- 6.1.6. Other Products

- 6.1.1. Machine Vision Systems

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Product Lifecycle Management (PLM)

- 6.2.2. Human Machine Interface (HMI)

- 6.2.3. Enterprise Resource and Planning (ERP)

- 6.2.4. Manufacturing Execution System (MES)

- 6.2.5. Distributed Control System (DCS)

- 6.2.6. Supervisory Controller and Data Acquisition (SCADA

- 6.2.7. Programmable Logic Controller (PLC)

- 6.2.8. Other Technologies

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Automotive

- 6.3.2. Semiconductors

- 6.3.3. Oil and Gas

- 6.3.4. Chemical and Petrochemical

- 6.3.5. Pharmaceutical

- 6.3.6. Aerospace and Defense

- 6.3.7. Food and Beverage

- 6.3.8. Mining

- 6.3.9. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ABB Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Cognex Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mitsubishi Electric Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Siemens AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Schneider Electric SE

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Fanuc Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Robert Bosch GmbH

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rockwell Automation Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Yokogawa Electric Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 FLIR Systems Inc *List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Kuka AG

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Emerson Electric Company

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Smart Factory Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Smart Factory Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Smart Factory Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: North America Smart Factory Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: North America Smart Factory Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: North America Smart Factory Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Smart Factory Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 6: North America Smart Factory Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 7: North America Smart Factory Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: North America Smart Factory Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States North America Smart Factory Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Smart Factory Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Smart Factory Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Smart Factory Industry?

The projected CAGR is approximately 10.49%.

2. Which companies are prominent players in the North America Smart Factory Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Cognex Corporation, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, Fanuc Corporation, Robert Bosch GmbH, Rockwell Automation Inc, Yokogawa Electric Corporation, FLIR Systems Inc *List Not Exhaustive, Kuka AG, Emerson Electric Company.

3. What are the main segments of the North America Smart Factory Industry?

The market segments include Product, Technology, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 167.02 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Adoption of Internet of Things (IoT) Technologies Across the Value Chain; Rising Demand for Energy Efficiency.

6. What are the notable trends driving market growth?

Semiconductor Industry is Observing a Significant Growth.

7. Are there any restraints impacting market growth?

; Huge Capital Investments for Transformations; Vulnerable to Cyber Attacks.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Smart Factory Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Smart Factory Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Smart Factory Industry?

To stay informed about further developments, trends, and reports in the North America Smart Factory Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence