Key Insights

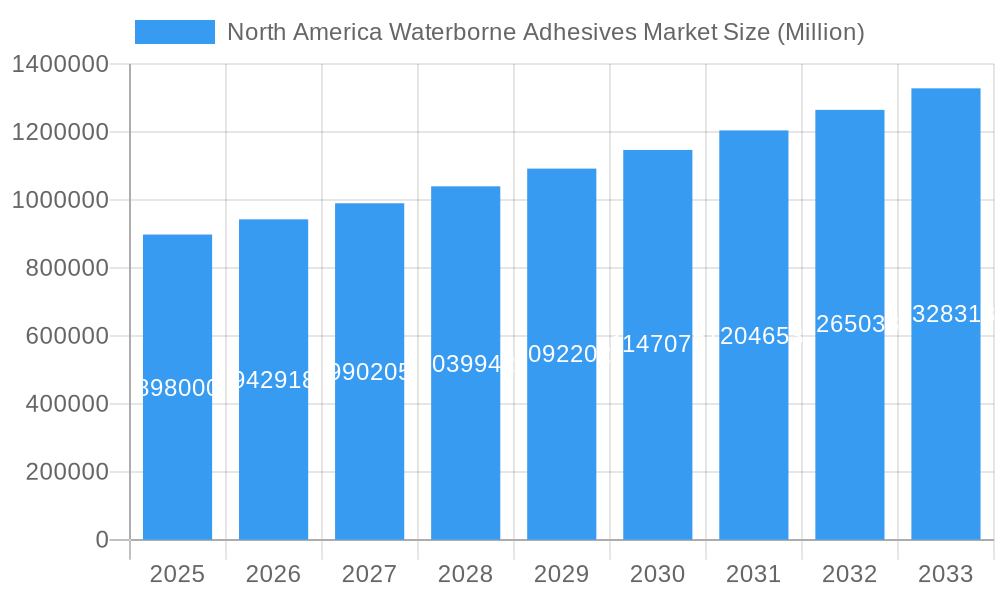

The North American waterborne adhesives market is poised for significant expansion, with a projected market size of $898 billion in 2025. This growth is underpinned by a robust CAGR of 5.19%, indicating a steady and healthy upward trajectory. Several key drivers are fueling this surge, including the increasing demand from the building and construction sector, driven by sustainable building practices and infrastructure development. The paper, board, and packaging industry also presents a substantial opportunity, influenced by the growing e-commerce sector and the push for eco-friendly packaging solutions. Furthermore, advancements in adhesive formulations, particularly in acrylics and polyvinyl acetate (PVA) emulsions, are enhancing performance and broadening application areas, making them attractive alternatives to solvent-based adhesives. The transportation industry's adoption of lighter materials and improved bonding technologies further contributes to market expansion.

North America Waterborne Adhesives Market Market Size (In Billion)

The market dynamics are also shaped by emerging trends such as the rising preference for low-VOC (Volatile Organic Compound) and environmentally friendly adhesive solutions, aligning with stringent environmental regulations across North America. Innovations in bio-based waterborne adhesives are gaining traction, appealing to environmentally conscious consumers and businesses. However, the market also faces certain restraints. Fluctuations in raw material prices, particularly for key components like acrylic monomers and vinyl acetate monomer, can impact profitability. While the study period extends to 2033, the primary focus for analysis remains on the foundational years and forecast period, with 2025 serving as the base year for this estimation. The established market players are actively investing in research and development to introduce advanced formulations and expand their product portfolios to cater to diverse end-user industries, solidifying the market's growth potential.

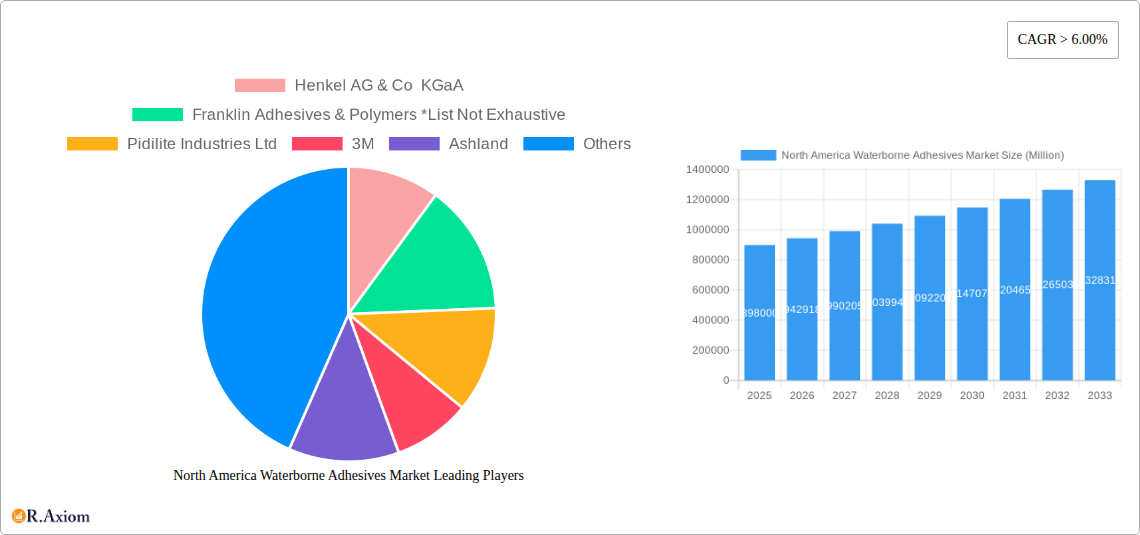

North America Waterborne Adhesives Market Company Market Share

North America Waterborne Adhesives Market Market Concentration & Innovation

The North America Waterborne Adhesives Market is characterized by a moderate level of market concentration, with several key global players holding significant market share. Innovation is a critical driver, fueled by the growing demand for sustainable and eco-friendly adhesive solutions. Regulatory frameworks, particularly those from the EPA and OSHA, are increasingly pushing for lower VOC (Volatile Organic Compound) emissions, directly benefiting waterborne adhesive technologies. Product substitutes, primarily solvent-based adhesives and some mechanical fastening methods, are being steadily displaced by the performance and environmental advantages of waterborne alternatives. End-user trends demonstrate a strong preference for adhesives that offer ease of application, reduced health risks, and compliance with stringent environmental standards. Mergers and acquisitions (M&A) activities are observed as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, acquisitions of smaller, specialized waterborne adhesive manufacturers by larger chemical conglomerates are a recurring theme, contributing to consolidation and strategic alignment. While specific M&A deal values are dynamic, the underlying trend indicates substantial investment in the sector, reflecting confidence in its future growth. The market share distribution is fluid, but companies like Henkel AG & Co KGaA and 3M consistently maintain leading positions due to their extensive product offerings and robust R&D investments.

North America Waterborne Adhesives Market Industry Trends & Insights

The North America Waterborne Adhesives Market is experiencing robust growth, projected to reach approximately $12.5 billion by 2033, with an estimated market size of $9.8 billion in 2025. This growth is underpinned by a projected Compound Annual Growth Rate (CAGR) of approximately 5.2% during the forecast period of 2025–2033. Technological disruptions are a significant factor, with ongoing advancements in polymer science leading to the development of high-performance waterborne adhesives that rival or surpass traditional solvent-based counterparts. These innovations focus on enhancing properties such as bond strength, heat resistance, water resistance, and application speed, thereby broadening their applicability across diverse industries. Consumer preferences are increasingly shifting towards sustainability and health consciousness. The demand for adhesives with low or zero VOC emissions, derived from renewable resources, and offering improved indoor air quality is escalating. This trend is particularly pronounced in end-user industries like building & construction and consumer goods packaging. Competitive dynamics are intensifying, with established players investing heavily in R&D to maintain their technological edge and expand their market penetration. New market entrants, often focusing on niche applications or specialized bio-based formulations, also contribute to the dynamic competitive landscape. The market penetration of waterborne adhesives is steadily increasing, driven by their cost-effectiveness, environmental benefits, and improving performance characteristics. Regulatory mandates for reduced environmental impact and worker safety further accelerate this shift. The transition from solvent-borne to waterborne adhesive systems is a defining trend, influencing product development and market strategies across the entire value chain.

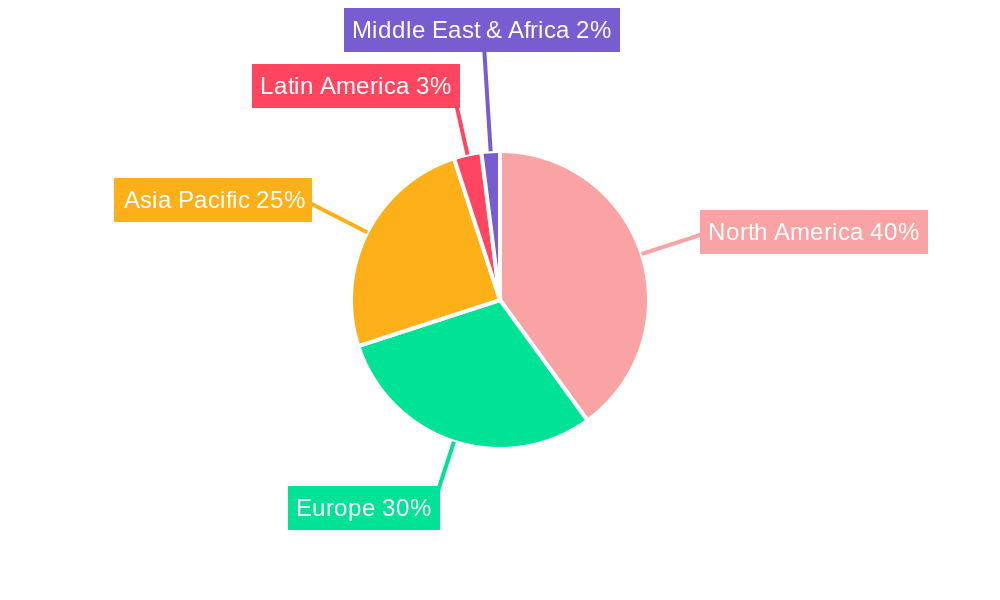

Dominant Markets & Segments in North America Waterborne Adhesives Market

The United States dominates the North America Waterborne Adhesives Market, accounting for the largest share of market revenue and consumption. This dominance is attributed to its large industrial base, significant investments in infrastructure and construction, and a strong consumer market driving demand across various sectors. Canada and Mexico follow, with their respective economies showing steady growth and increasing adoption of sustainable adhesive technologies.

Within the Resin Type segmentation, Acrylics are a dominant force.

- Acrylics: Their versatility, excellent weatherability, and ability to form strong bonds with a wide range of substrates make them highly sought after in applications ranging from construction sealants to pressure-sensitive adhesives for tapes and labels. Growth is driven by their performance in demanding outdoor applications and their compatibility with low-VOC formulations.

- Polyvinyl Acetate (PVA) Emulsion: This segment holds significant market share, particularly in the woodworking & joinery and paper & packaging industries. Its cost-effectiveness and ease of use make it a staple for many applications.

- Ethylene Vinyl Acetate (EVA) Emulsion: EVA emulsions are crucial for applications requiring good flexibility and adhesion to challenging surfaces, finding significant use in paper, board, and packaging, as well as in textile applications.

- Polyurethane: While often considered a specialty segment, waterborne polyurethanes are gaining traction due to their superior toughness, flexibility, and chemical resistance, finding applications in high-performance coatings and adhesives for transportation and textiles.

- Other Resin Types: This category includes various niche polymers and blends catering to specific performance requirements, contributing to the market’s innovation potential.

In terms of End-user Industry, Building & Construction represents the largest and most influential segment.

- Building & Construction: This sector's demand is driven by the widespread use of waterborne adhesives in flooring installation, drywall bonding, window and door sealing, insulation, and roofing applications. Government initiatives promoting energy-efficient buildings and infrastructure development further bolster demand.

- Paper, Board, and Packaging: This segment is a consistent high-volume consumer, utilizing waterborne adhesives for carton sealing, labeling, flexible packaging lamination, and paper converting. The growing e-commerce sector and the demand for sustainable packaging solutions are key growth drivers.

- Woodworking & Joinery: The use of waterborne adhesives in furniture manufacturing, cabinetry, and millwork remains substantial, driven by the need for strong, durable, and environmentally friendly bonding solutions.

- Transportation: While historically dominated by solvent-based adhesives, the automotive and aerospace industries are increasingly adopting waterborne solutions for interior trim, upholstery, and certain structural bonding applications, driven by regulatory compliance and VOC reduction mandates.

- Healthcare: The healthcare sector utilizes waterborne adhesives in medical device assembly, wound care, and diagnostic equipment, where biocompatibility, low extractables, and stringent purity standards are paramount.

- Electrical & Electronics: This segment relies on waterborne adhesives for component assembly, encapsulation, and thermal management in electronic devices, where precision and reliable performance are critical.

- Other End-user Industries: This encompasses a diverse range of applications in textiles, footwear, sporting goods, and general manufacturing, all contributing to the overall market demand for waterborne adhesives.

North America Waterborne Adhesives Market Product Developments

Product developments in the North America Waterborne Adhesives Market are heavily focused on enhancing performance while adhering to stringent environmental regulations. Innovations include the creation of high-strength, fast-curing acrylic and polyurethane dispersions for demanding construction applications, and improved PVA and EVA emulsions for flexible packaging and paper converting. Companies are also investing in bio-based and renewable raw material formulations to meet the growing demand for sustainable solutions. Competitive advantages are being built around adhesives offering superior water resistance, heat stability, and adhesion to challenging substrates, alongside low-VOC content and enhanced worker safety profiles.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North America Waterborne Adhesives Market, segmenting it by Resin Type, End-user Industry, and Geography. The Resin Type segmentation includes Acrylics, Polyvinyl Acetate (PVA) Emulsion, Ethylene Vinyl Acetate (EVA) Emulsion, Polyurethane, and Other Resin Types. The End-user Industry segmentation covers Building & Construction, Paper, Board, and Packaging, Woodworking & Joinery, Transportation, Healthcare, Electrical & Electronics, and Other End-user Industries. Geographically, the market is analyzed for the United States, Canada, and Mexico. Each segment is analyzed for its market size, growth projections, and competitive dynamics, providing actionable insights for stakeholders.

Key Drivers of North America Waterborne Adhesives Market Growth

The North America Waterborne Adhesives Market growth is propelled by several key drivers. Stringent environmental regulations, particularly those mandating reductions in VOC emissions, are a primary catalyst, pushing industries to adopt safer and more sustainable adhesive alternatives. The increasing consumer demand for eco-friendly products further supports this transition. Technological advancements in polymer science are leading to the development of high-performance waterborne adhesives that can match or exceed the capabilities of solvent-based counterparts. Economic growth, especially in the building & construction and packaging sectors, directly correlates with adhesive demand. Furthermore, the expanding e-commerce landscape fuels the need for efficient and sustainable packaging solutions, where waterborne adhesives play a crucial role.

Challenges in the North America Waterborne Adhesives Market Sector

Despite robust growth, the North America Waterborne Adhesives Market faces several challenges. While performance is improving, some niche applications still require the specific properties offered by solvent-based adhesives, posing a challenge for complete market substitution. High initial investment costs for transitioning manufacturing processes to waterborne systems can be a barrier for smaller enterprises. Supply chain disruptions and the volatility of raw material prices can impact production costs and lead times. Intense competition among established players and emerging specialized manufacturers also puts pressure on pricing and profit margins. Navigating complex and evolving regulatory landscapes across different regions can also present compliance hurdles.

Emerging Opportunities in North America Waterborne Adhesives Market

Emerging opportunities in the North America Waterborne Adhesives Market lie in several key areas. The growing emphasis on circular economy principles and the demand for biodegradable and compostable adhesives present a significant opportunity for innovation. The expansion of renewable energy infrastructure, such as wind turbines and solar panels, requires specialized adhesives with excellent durability and weather resistance. The increasing trend towards lightweighting in the transportation sector, particularly in electric vehicles, creates demand for advanced bonding solutions. Furthermore, the healthcare industry's continuous need for biocompatible and high-performance adhesives for medical devices offers a stable and growing market segment. The development of smart adhesives with sensing or self-healing capabilities also represents a future frontier.

Leading Players in the North America Waterborne Adhesives Market Market

- Henkel AG & Co KGaA

- Franklin Adhesives & Polymers

- Pidilite Industries Ltd

- 3M

- Ashland

- Arkema Group

- Dow

- Sika AG

Key Developments in North America Waterborne Adhesives Market Industry

- 2023: Launch of a new line of high-performance, bio-based acrylic adhesives for sustainable packaging applications by a leading chemical manufacturer.

- 2022: Acquisition of a specialized waterborne adhesive producer by a major global player to enhance its portfolio in the construction sector.

- 2021: Significant investment in R&D for developing advanced waterborne polyurethane dispersions to meet stringent automotive industry requirements.

- 2020: Introduction of low-VOC, fast-curing PVA emulsions for woodworking applications, addressing growing demand for healthier indoor environments.

Strategic Outlook for North America Waterborne Adhesives Market Market

The strategic outlook for the North America Waterborne Adhesives Market remains highly optimistic. The persistent drive towards sustainability, coupled with evolving regulatory demands and technological advancements, will continue to fuel market expansion. Companies that focus on developing innovative, high-performance, and environmentally friendly adhesive solutions, particularly those derived from renewable resources, will be well-positioned for growth. Strategic partnerships, targeted M&A activities, and a keen understanding of end-user industry needs will be crucial for maintaining a competitive edge. The market's trajectory points towards increased adoption of waterborne adhesives across a broader spectrum of applications, solidifying their position as the preferred choice for bonding solutions.

North America Waterborne Adhesives Market Segmentation

-

1. Resin Type

- 1.1. Acrylics

- 1.2. Polyvinyl Acetate (PVA) Emulsion

- 1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 1.4. Polyuret

- 1.5. Other Resin Types

-

2. End-user Industry

- 2.1. Building & Construction

- 2.2. Paper, Board, and Packaging

- 2.3. Woodworking & Joinery

- 2.4. Transportation

- 2.5. Healthcare

- 2.6. Electrical & Electronics

- 2.7. Other End-user Industries

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Waterborne Adhesives Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Waterborne Adhesives Market Regional Market Share

Geographic Coverage of North America Waterborne Adhesives Market

North America Waterborne Adhesives Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Acrylics

- 5.1.2. Polyvinyl Acetate (PVA) Emulsion

- 5.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 5.1.4. Polyuret

- 5.1.5. Other Resin Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Building & Construction

- 5.2.2. Paper, Board, and Packaging

- 5.2.3. Woodworking & Joinery

- 5.2.4. Transportation

- 5.2.5. Healthcare

- 5.2.6. Electrical & Electronics

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. North America Waterborne Adhesives Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Acrylics

- 6.1.2. Polyvinyl Acetate (PVA) Emulsion

- 6.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 6.1.4. Polyuret

- 6.1.5. Other Resin Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Building & Construction

- 6.2.2. Paper, Board, and Packaging

- 6.2.3. Woodworking & Joinery

- 6.2.4. Transportation

- 6.2.5. Healthcare

- 6.2.6. Electrical & Electronics

- 6.2.7. Other End-user Industries

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. United States North America Waterborne Adhesives Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 7.1.1. Acrylics

- 7.1.2. Polyvinyl Acetate (PVA) Emulsion

- 7.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 7.1.4. Polyuret

- 7.1.5. Other Resin Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Building & Construction

- 7.2.2. Paper, Board, and Packaging

- 7.2.3. Woodworking & Joinery

- 7.2.4. Transportation

- 7.2.5. Healthcare

- 7.2.6. Electrical & Electronics

- 7.2.7. Other End-user Industries

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 8. Canada North America Waterborne Adhesives Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 8.1.1. Acrylics

- 8.1.2. Polyvinyl Acetate (PVA) Emulsion

- 8.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 8.1.4. Polyuret

- 8.1.5. Other Resin Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Building & Construction

- 8.2.2. Paper, Board, and Packaging

- 8.2.3. Woodworking & Joinery

- 8.2.4. Transportation

- 8.2.5. Healthcare

- 8.2.6. Electrical & Electronics

- 8.2.7. Other End-user Industries

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 9. Mexico North America Waterborne Adhesives Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 9.1.1. Acrylics

- 9.1.2. Polyvinyl Acetate (PVA) Emulsion

- 9.1.3. Ethylene Vinyl Acetate (EVA) Emulsion

- 9.1.4. Polyuret

- 9.1.5. Other Resin Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Building & Construction

- 9.2.2. Paper, Board, and Packaging

- 9.2.3. Woodworking & Joinery

- 9.2.4. Transportation

- 9.2.5. Healthcare

- 9.2.6. Electrical & Electronics

- 9.2.7. Other End-user Industries

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Resin Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Henkel AG & Co KGaA

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Franklin Adhesives & Polymers *List Not Exhaustive

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Pidilite Industries Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 3M

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Ashland

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Arkema Group

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Dow

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Sika AG

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.1 Henkel AG & Co KGaA

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Waterborne Adhesives Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Waterborne Adhesives Market Share (%) by Company 2025

List of Tables

- Table 1: North America Waterborne Adhesives Market Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 2: North America Waterborne Adhesives Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: North America Waterborne Adhesives Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Waterborne Adhesives Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Waterborne Adhesives Market Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 6: North America Waterborne Adhesives Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 7: North America Waterborne Adhesives Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: North America Waterborne Adhesives Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: North America Waterborne Adhesives Market Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 10: North America Waterborne Adhesives Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 11: North America Waterborne Adhesives Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: North America Waterborne Adhesives Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Waterborne Adhesives Market Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 14: North America Waterborne Adhesives Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 15: North America Waterborne Adhesives Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: North America Waterborne Adhesives Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Waterborne Adhesives Market?

The projected CAGR is approximately 3.39%.

2. Which companies are prominent players in the North America Waterborne Adhesives Market?

Key companies in the market include Henkel AG & Co KGaA, Franklin Adhesives & Polymers *List Not Exhaustive, Pidilite Industries Ltd, 3M, Ashland, Arkema Group, Dow, Sika AG.

3. What are the main segments of the North America Waterborne Adhesives Market?

The market segments include Resin Type, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.89 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing investments in Infrastructure & Construction Industry; Favourable Govermnent Policies for Adhesives Industry; Other Drivers.

6. What are the notable trends driving market growth?

Construction Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

; Limited Resistance to Moisture and Water; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Waterborne Adhesives Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Waterborne Adhesives Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Waterborne Adhesives Market?

To stay informed about further developments, trends, and reports in the North America Waterborne Adhesives Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence