Key Insights

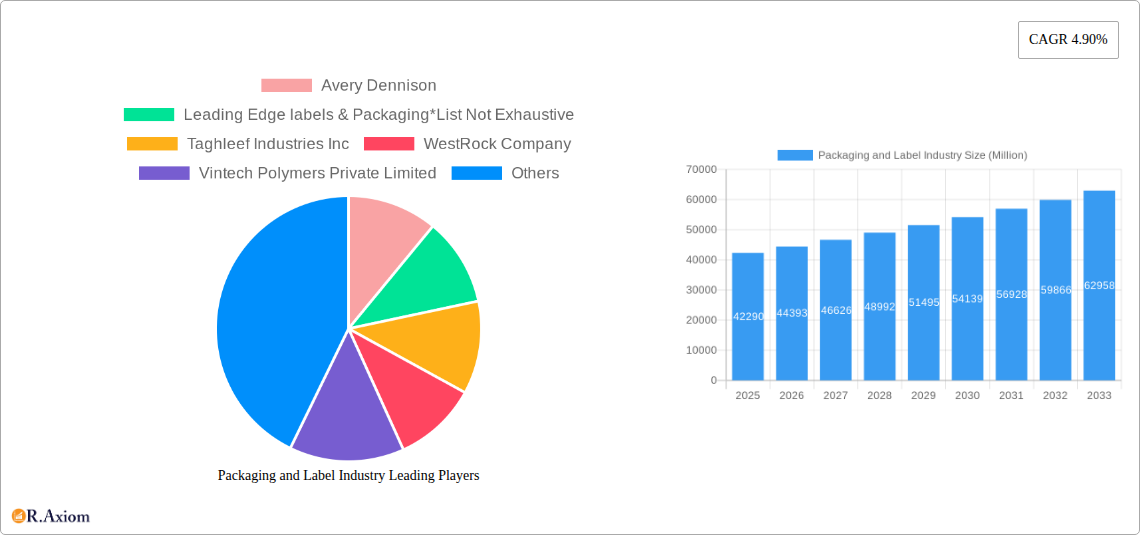

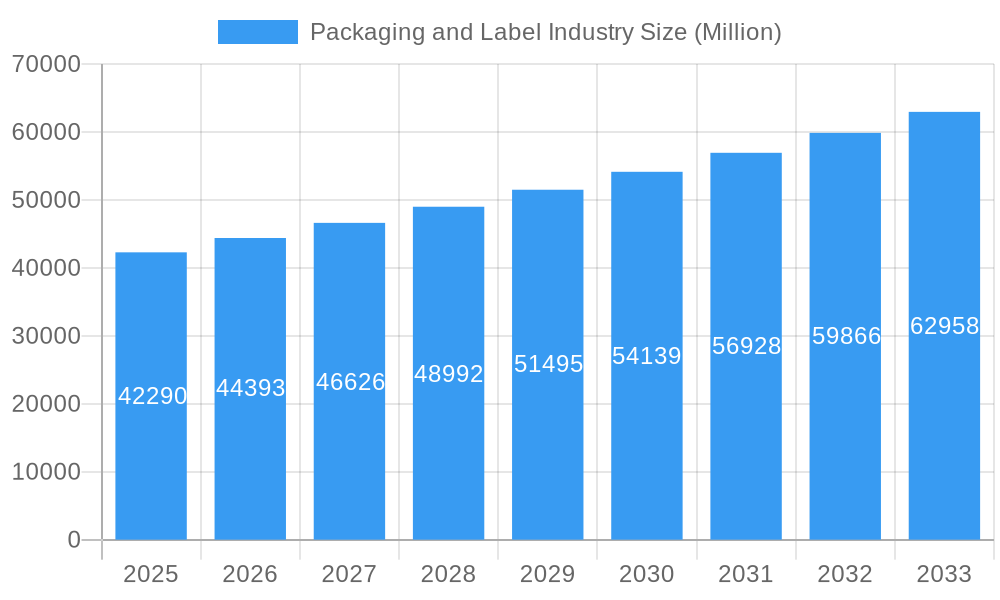

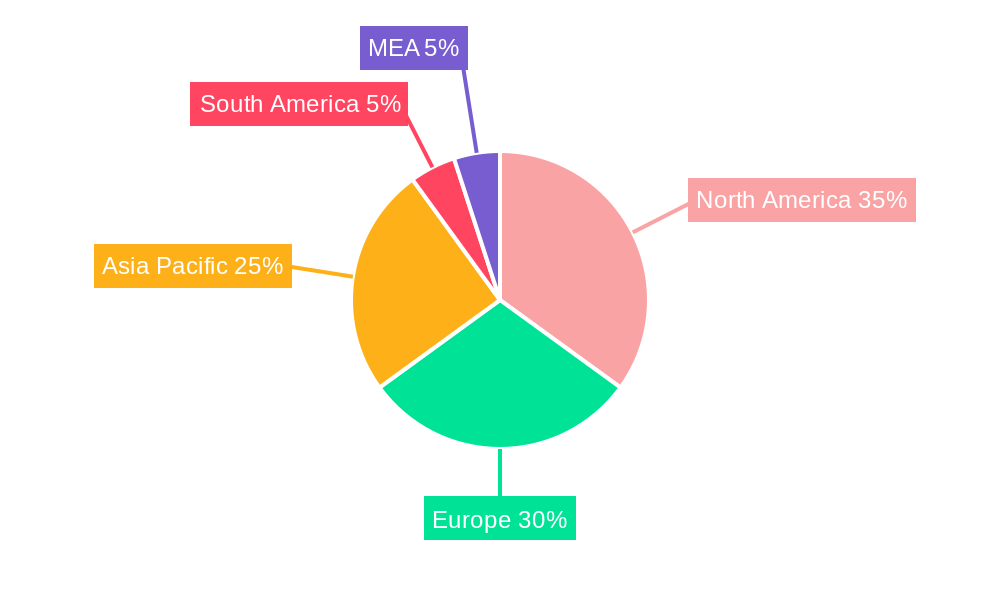

The global packaging and label industry, currently valued at $42.29 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 4.90% from 2025 to 2033. This expansion is driven by several key factors. The rising demand for convenient and tamper-evident packaging across diverse sectors like food and beverages, pharmaceuticals, and healthcare is a significant contributor. Furthermore, evolving consumer preferences towards sustainable and eco-friendly packaging solutions, such as those made from recycled paper or biodegradable materials (PLA, PO), are fueling innovation and market growth. The increasing adoption of advanced printing technologies like digital printing, offering greater flexibility and customization, also plays a crucial role. Segmentation analysis reveals a strong preference for pressure-sensitive labels, followed by shrink and stretch sleeves, reflecting the diverse needs of various end-use industries. The geographical distribution of market share shows a strong presence in North America and Europe, with the Asia-Pacific region poised for significant growth driven by expanding economies and increasing consumer spending. Major players like Avery Dennison, CCL Industries, and 3M are leading the market with their innovative product offerings and extensive distribution networks.

Packaging and Label Industry Market Size (In Billion)

The industry faces certain challenges, however. Fluctuations in raw material prices, particularly for plastics, can impact profitability. Stringent environmental regulations regarding packaging waste are also pushing companies to invest in sustainable solutions, increasing costs in the short term. Despite these constraints, the long-term outlook remains positive, fueled by ongoing technological advancements and the burgeoning demand for effective and aesthetically appealing packaging across a wide array of products. The competitive landscape is characterized by both large multinational corporations and specialized regional players, creating a dynamic and innovative market environment. Further growth is expected in specialized segments, such as functional and security labels and in-mold labels, reflecting the need for enhanced product protection and brand security.

Packaging and Label Industry Company Market Share

Packaging and Label Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the global packaging and label industry, offering invaluable insights for stakeholders across the value chain. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages extensive market research and data analysis to offer actionable strategies for growth and success. The global packaging and label market is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period.

Packaging and Label Industry Market Concentration & Innovation

The global packaging and label industry is characterized by a moderate level of concentration, with several major players controlling a significant market share. Avery Dennison, CCL Industries, and 3M are among the leading companies, holding a combined market share of approximately xx%. However, the market also features numerous smaller, specialized players, particularly in niche segments like functional and security labels. Innovation is a key driver, fueled by evolving consumer preferences, sustainability concerns, and technological advancements such as digital printing and smart packaging.

- Market Share: Top 5 players hold approximately xx% of the global market share in 2025.

- M&A Activity: Significant M&A activity has been observed, with deal values exceeding xx Million in the past five years, reflecting industry consolidation and expansion strategies. For example, Fort Dearborn’s acquisition of Hammer Packaging Corporation in March 2021 significantly expanded their market reach and capabilities.

- Regulatory Frameworks: Stringent environmental regulations and food safety standards are driving innovation towards sustainable and eco-friendly packaging solutions.

- Product Substitutes: The emergence of biodegradable and compostable materials poses a competitive threat to traditional packaging materials.

- End-User Trends: Growing demand for personalized and customized packaging solutions is driving the adoption of advanced printing technologies and customized label designs.

Packaging and Label Industry Industry Trends & Insights

The packaging and label industry is experiencing significant transformation driven by several key trends. The global market is projected to reach xx Million by 2033, driven by rising consumer demand, increasing e-commerce penetration, and the growing adoption of sustainable packaging solutions. Technological advancements, particularly in digital printing and smart packaging, are revolutionizing the industry. The shift towards e-commerce has significantly boosted the demand for e-commerce-friendly packaging, including corrugated boxes and flexible packaging.

Consumer preference for sustainable and eco-friendly products is driving increased demand for biodegradable and compostable packaging materials. This trend is further reinforced by stricter environmental regulations and growing consumer awareness of environmental issues. Competitive dynamics are intense, with companies investing heavily in research and development to bring innovative products and services to market, particularly in the area of sustainable packaging materials. The market is witnessing significant consolidation through mergers and acquisitions, leading to a more concentrated landscape.

Dominant Markets & Segments in Packaging and Label Industry

The Asia-Pacific region holds a dominant position in the global packaging and label market, driven by strong economic growth, expanding middle class, and increasing industrial activity. Within this region, countries like China and India are major contributors, showcasing significant growth potential.

- By Product Type: Pressure-sensitive labels hold the largest market share, followed by shrink and stretch sleeves. The functional & security label segment demonstrates high growth potential due to increasing demand for tamper-evident and anti-counterfeiting measures.

- By End-User Industry: The food & beverages industry dominates the market, closely followed by the pharmaceutical & healthcare sector, which is experiencing growth due to stringent regulations and safety concerns.

- By Material: Paper and plastic materials (PVC, PET, PE) are widely used, but the demand for sustainable alternatives (PLA, PO) is increasing steadily.

- By Type: Pressure-sensitive labels maintain the largest share due to their ease of application and versatility.

- By Print Process: Flexography printing and digital printing are witnessing rapid growth due to their cost-effectiveness and suitability for high-volume production and personalization.

Key drivers for this dominance include favorable government policies supporting industrial growth, increasing investments in manufacturing infrastructure, and a booming consumer goods market.

Packaging and Label Industry Product Developments

The packaging and label industry is witnessing a dynamic evolution, driven by a trifecta of sustainability, enhanced convenience, and advanced functionality. Key innovations include the widespread adoption of biodegradable and compostable materials, the development of sophisticated reusable packaging systems, and the integration of smart labels equipped with embedded sensors. These smart labels are revolutionizing product traceability, offering robust authentication capabilities, and providing real-time condition monitoring. Such advancements are instrumental in extending product shelf life, significantly elevating the consumer experience, and crucially, addressing pressing environmental concerns with greater efficacy. The transformative power of digital printing technologies is also reshaping the landscape, enabling highly personalized labels and cost-effective, on-demand packaging solutions. This capability directly caters to the burgeoning consumer demand for bespoke products and unique brand interactions.

Report Scope & Segmentation Analysis

This report provides a detailed analysis of the global packaging and label industry, segmented by product type (liner, linerless, VIP, prime, functional & security, promotional), end-user industry (food & beverages, pharmaceutical & healthcare, other end-users), material (PVC, PET, PE, OPP & OPS, other materials, paper, polyester, PP, other materials), type (pressure-sensitive label, shrink sleeve, stretch sleeve), and print process (offset printing, flexography printing, gravure, other analog printing processes, digital printing). Each segment's growth projections, market size, and competitive dynamics are thoroughly analyzed, offering a comprehensive overview of the market landscape. Each segment displays varying growth rates, with sustainable materials and digital printing processes experiencing the most rapid expansion.

Key Drivers of Packaging and Label Industry Growth

The sustained growth trajectory of the packaging and label industry is underpinned by a confluence of powerful drivers. The exponential rise of e-commerce has created an insatiable demand for resilient and protective packaging solutions essential for safe transit. Simultaneously, consumers are increasingly seeking packaging that is not only convenient to use but also aesthetically appealing, driving innovation in design and material. Stringent regulatory frameworks, particularly concerning food safety and the imperative for meticulous product traceability throughout the supply chain, are pushing for higher standards and technological integration. Furthermore, a profound shift in consumer consciousness and corporate responsibility is fueling a surge in demand for sustainable and eco-friendly packaging materials. Complementing these market forces, continuous technological advancements in printing techniques, material science, and smart packaging integration are further accelerating market expansion and unlocking new potential.

Challenges in the Packaging and Label Industry Sector

The packaging and label industry operates within a complex environment, grappling with persistent challenges. Fluctuations in the prices of raw materials can significantly impact manufacturing costs and profitability. The intensifying competitive landscape demands constant innovation and differentiation to maintain market share. Additionally, increasingly stringent environmental regulations necessitate proactive adaptation and investment in greener alternatives. Supply chain disruptions, ranging from material availability to logistical complexities, present ongoing hurdles. The imperative to develop and implement genuinely sustainable packaging options, while meeting performance and cost expectations, remains a significant undertaking. Moreover, navigating the ever-evolving and often conflicting consumer demands for both sustainability and personalized packaging solutions adds a layer of intricate complexity to strategic planning and operational execution.

Emerging Opportunities in Packaging and Label Industry

The packaging and label industry is ripe with emerging opportunities, particularly for forward-thinking companies. The robust and growing demand for sustainable packaging solutions continues to present substantial growth avenues, encompassing compostable, recyclable, and biodegradable options. The integration of smart packaging, leveraging digital technologies for enhanced functionality, is a rapidly expanding sector, offering opportunities in connected packaging, interactive labels, and advanced tracking systems. Specialized labels designed for niche applications, such as high-value goods, pharmaceuticals, and industrial products, also represent a significant untapped market. Expansion into dynamic emerging markets, coupled with the strategic leveraging of digital printing capabilities to deliver truly personalized and customized packaging, offers considerable growth potential. The increasing global focus on product traceability, coupled with the rising threat of counterfeiting, is driving demand for advanced brand protection and anti-counterfeiting measures, creating further avenues for innovation and market penetration.

Leading Players in the Packaging and Label Industry Market

- Avery Dennison Corporation - A global leader in pressure-sensitive materials, labels, and packaging solutions.

- Leading Edge Labels & Packaging - Known for innovative label solutions and a commitment to quality.

- Taghleef Industries Inc - A prominent global manufacturer of bi-oriented plastic films for packaging.

- WestRock Company - A diversified provider of paper and packaging solutions, including labels.

- Vintech Polymers Private Limited - Specializes in the production of advanced polymer films for packaging applications.

- Fort Dearborn Company - A leading producer of pressure-sensitive labels for consumer packaged goods.

- KRIS FLEXIPACKS PVT LTD - Offers a wide range of flexible packaging solutions and labels.

- Constantia Flexibles Group GmbH - A global manufacturer of flexible packaging and labels for the pharmaceutical and food industries.

- Bemis Company (now part of Amcor) - Historically a major player in flexible packaging and labels.

- UPM Raflatac - A leading global supplier of innovative and sustainable self-adhesive label materials.

- Royal Sens Group - Focuses on intelligent packaging and label solutions for product authentication and traceability.

- Klöckner Pentaplast - A leading global manufacturer of plastic films and packaging solutions.

- CCL Industries LLC - A world leader in specialty packaging, labels, and security solutions.

- 3M Company - Offers a broad range of adhesives, films, and label materials for diverse applications.

- Huhtamaki Group - A global specialist in sustainable food packaging solutions, including labels.

- Lintec Corporation - A global manufacturer of adhesive materials and specialty papers, including labels.

- Multi-Color Corporation - One of the largest label companies in the world, serving various industries.

- Fuji Seal International Inc - A leading provider of heat-shrinkable sleeves and labels for product decoration and protection.

- Mondi - A global leader in sustainable packaging and paper solutions, with a strong presence in labels.

- CPC Packaging - Offers a comprehensive range of packaging and label solutions for various markets.

- Berry Global - A leading global manufacturer and supplier of plastic packaging products, including labels.

- GTPL (Global Tape & Label) - A prominent manufacturer of pressure-sensitive tapes and labels.

- Neenah Inc - A leading global producer of specialty paper, including solutions for labels and packaging.

Key Developments in Packaging and Label Industry Industry

- February 2021: Mondi Group launched a range of sustainable paper-based release liners, boosting the eco-friendly packaging segment.

- March 2021: Fort Dearborn Company's acquisition of Hammer Packaging Corporation strengthened its market position and expanded its capabilities.

Strategic Outlook for Packaging and Label Industry Market

The packaging and label industry is poised for continued growth, driven by technological innovation, sustainability concerns, and evolving consumer preferences. The focus on sustainable materials, smart packaging, and personalized solutions will shape future market dynamics. Companies that successfully adapt to these trends and invest in R&D will be well-positioned to capitalize on emerging opportunities.

Packaging and Label Industry Segmentation

-

1. Type

-

1.1. Pressure-Sensitive Label

-

1.1.1. By Print Process

- 1.1.1.1. Offset Printing

- 1.1.1.2. Flexography Printing

- 1.1.1.3. Gravure

- 1.1.1.4. Other Analog Printing Process

- 1.1.1.5. Digital Printing

-

1.1.2. By Product Type

- 1.1.2.1. Liner

- 1.1.2.2. Linerless

- 1.1.2.3. VIP

- 1.1.2.4. Prime

- 1.1.2.5. Functional & Security

- 1.1.2.6. Promotional

-

1.1.3. End-User Industry

- 1.1.3.1. Food & Beverages

- 1.1.3.2. Pharmaceutical & Healthcare

- 1.1.3.3. Other End-Users

-

1.1.1. By Print Process

-

1.2. Shrink & Stretch Sleeve Label

- 1.2.1. Shrink Sleeve

-

1.2.2. By Material

- 1.2.2.1. PVC

- 1.2.2.2. PET

- 1.2.2.3. OPP & OPS

- 1.2.2.4. Other Materials (PO, PLA, etc.)

- 1.3. In-Mold Label

- 1.4. Wet Glue Label

-

1.5. Thermal Transfer Label

- 1.5.1. Paper

- 1.5.2. Polyester

- 1.6. Wrap Around Label

-

1.1. Pressure-Sensitive Label

Packaging and Label Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Middle East

- 5. Latin America

Packaging and Label Industry Regional Market Share

Geographic Coverage of Packaging and Label Industry

Packaging and Label Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pressure-Sensitive Label

- 5.1.1.1. By Print Process

- 5.1.1.1.1. Offset Printing

- 5.1.1.1.2. Flexography Printing

- 5.1.1.1.3. Gravure

- 5.1.1.1.4. Other Analog Printing Process

- 5.1.1.1.5. Digital Printing

- 5.1.1.2. By Product Type

- 5.1.1.2.1. Liner

- 5.1.1.2.2. Linerless

- 5.1.1.2.3. VIP

- 5.1.1.2.4. Prime

- 5.1.1.2.5. Functional & Security

- 5.1.1.2.6. Promotional

- 5.1.1.3. End-User Industry

- 5.1.1.3.1. Food & Beverages

- 5.1.1.3.2. Pharmaceutical & Healthcare

- 5.1.1.3.3. Other End-Users

- 5.1.1.1. By Print Process

- 5.1.2. Shrink & Stretch Sleeve Label

- 5.1.2.1. Shrink Sleeve

- 5.1.2.2. By Material

- 5.1.2.2.1. PVC

- 5.1.2.2.2. PET

- 5.1.2.2.3. OPP & OPS

- 5.1.2.2.4. Other Materials (PO, PLA, etc.)

- 5.1.3. In-Mold Label

- 5.1.4. Wet Glue Label

- 5.1.5. Thermal Transfer Label

- 5.1.5.1. Paper

- 5.1.5.2. Polyester

- 5.1.6. Wrap Around Label

- 5.1.1. Pressure-Sensitive Label

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East

- 5.2.5. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Packaging and Label Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pressure-Sensitive Label

- 6.1.1.1. By Print Process

- 6.1.1.1.1. Offset Printing

- 6.1.1.1.2. Flexography Printing

- 6.1.1.1.3. Gravure

- 6.1.1.1.4. Other Analog Printing Process

- 6.1.1.1.5. Digital Printing

- 6.1.1.2. By Product Type

- 6.1.1.2.1. Liner

- 6.1.1.2.2. Linerless

- 6.1.1.2.3. VIP

- 6.1.1.2.4. Prime

- 6.1.1.2.5. Functional & Security

- 6.1.1.2.6. Promotional

- 6.1.1.3. End-User Industry

- 6.1.1.3.1. Food & Beverages

- 6.1.1.3.2. Pharmaceutical & Healthcare

- 6.1.1.3.3. Other End-Users

- 6.1.1.1. By Print Process

- 6.1.2. Shrink & Stretch Sleeve Label

- 6.1.2.1. Shrink Sleeve

- 6.1.2.2. By Material

- 6.1.2.2.1. PVC

- 6.1.2.2.2. PET

- 6.1.2.2.3. OPP & OPS

- 6.1.2.2.4. Other Materials (PO, PLA, etc.)

- 6.1.3. In-Mold Label

- 6.1.4. Wet Glue Label

- 6.1.5. Thermal Transfer Label

- 6.1.5.1. Paper

- 6.1.5.2. Polyester

- 6.1.6. Wrap Around Label

- 6.1.1. Pressure-Sensitive Label

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Packaging and Label Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Pressure-Sensitive Label

- 7.1.1.1. By Print Process

- 7.1.1.1.1. Offset Printing

- 7.1.1.1.2. Flexography Printing

- 7.1.1.1.3. Gravure

- 7.1.1.1.4. Other Analog Printing Process

- 7.1.1.1.5. Digital Printing

- 7.1.1.2. By Product Type

- 7.1.1.2.1. Liner

- 7.1.1.2.2. Linerless

- 7.1.1.2.3. VIP

- 7.1.1.2.4. Prime

- 7.1.1.2.5. Functional & Security

- 7.1.1.2.6. Promotional

- 7.1.1.3. End-User Industry

- 7.1.1.3.1. Food & Beverages

- 7.1.1.3.2. Pharmaceutical & Healthcare

- 7.1.1.3.3. Other End-Users

- 7.1.1.1. By Print Process

- 7.1.2. Shrink & Stretch Sleeve Label

- 7.1.2.1. Shrink Sleeve

- 7.1.2.2. By Material

- 7.1.2.2.1. PVC

- 7.1.2.2.2. PET

- 7.1.2.2.3. OPP & OPS

- 7.1.2.2.4. Other Materials (PO, PLA, etc.)

- 7.1.3. In-Mold Label

- 7.1.4. Wet Glue Label

- 7.1.5. Thermal Transfer Label

- 7.1.5.1. Paper

- 7.1.5.2. Polyester

- 7.1.6. Wrap Around Label

- 7.1.1. Pressure-Sensitive Label

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Packaging and Label Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Pressure-Sensitive Label

- 8.1.1.1. By Print Process

- 8.1.1.1.1. Offset Printing

- 8.1.1.1.2. Flexography Printing

- 8.1.1.1.3. Gravure

- 8.1.1.1.4. Other Analog Printing Process

- 8.1.1.1.5. Digital Printing

- 8.1.1.2. By Product Type

- 8.1.1.2.1. Liner

- 8.1.1.2.2. Linerless

- 8.1.1.2.3. VIP

- 8.1.1.2.4. Prime

- 8.1.1.2.5. Functional & Security

- 8.1.1.2.6. Promotional

- 8.1.1.3. End-User Industry

- 8.1.1.3.1. Food & Beverages

- 8.1.1.3.2. Pharmaceutical & Healthcare

- 8.1.1.3.3. Other End-Users

- 8.1.1.1. By Print Process

- 8.1.2. Shrink & Stretch Sleeve Label

- 8.1.2.1. Shrink Sleeve

- 8.1.2.2. By Material

- 8.1.2.2.1. PVC

- 8.1.2.2.2. PET

- 8.1.2.2.3. OPP & OPS

- 8.1.2.2.4. Other Materials (PO, PLA, etc.)

- 8.1.3. In-Mold Label

- 8.1.4. Wet Glue Label

- 8.1.5. Thermal Transfer Label

- 8.1.5.1. Paper

- 8.1.5.2. Polyester

- 8.1.6. Wrap Around Label

- 8.1.1. Pressure-Sensitive Label

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Packaging and Label Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Pressure-Sensitive Label

- 9.1.1.1. By Print Process

- 9.1.1.1.1. Offset Printing

- 9.1.1.1.2. Flexography Printing

- 9.1.1.1.3. Gravure

- 9.1.1.1.4. Other Analog Printing Process

- 9.1.1.1.5. Digital Printing

- 9.1.1.2. By Product Type

- 9.1.1.2.1. Liner

- 9.1.1.2.2. Linerless

- 9.1.1.2.3. VIP

- 9.1.1.2.4. Prime

- 9.1.1.2.5. Functional & Security

- 9.1.1.2.6. Promotional

- 9.1.1.3. End-User Industry

- 9.1.1.3.1. Food & Beverages

- 9.1.1.3.2. Pharmaceutical & Healthcare

- 9.1.1.3.3. Other End-Users

- 9.1.1.1. By Print Process

- 9.1.2. Shrink & Stretch Sleeve Label

- 9.1.2.1. Shrink Sleeve

- 9.1.2.2. By Material

- 9.1.2.2.1. PVC

- 9.1.2.2.2. PET

- 9.1.2.2.3. OPP & OPS

- 9.1.2.2.4. Other Materials (PO, PLA, etc.)

- 9.1.3. In-Mold Label

- 9.1.4. Wet Glue Label

- 9.1.5. Thermal Transfer Label

- 9.1.5.1. Paper

- 9.1.5.2. Polyester

- 9.1.6. Wrap Around Label

- 9.1.1. Pressure-Sensitive Label

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East Packaging and Label Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Pressure-Sensitive Label

- 10.1.1.1. By Print Process

- 10.1.1.1.1. Offset Printing

- 10.1.1.1.2. Flexography Printing

- 10.1.1.1.3. Gravure

- 10.1.1.1.4. Other Analog Printing Process

- 10.1.1.1.5. Digital Printing

- 10.1.1.2. By Product Type

- 10.1.1.2.1. Liner

- 10.1.1.2.2. Linerless

- 10.1.1.2.3. VIP

- 10.1.1.2.4. Prime

- 10.1.1.2.5. Functional & Security

- 10.1.1.2.6. Promotional

- 10.1.1.3. End-User Industry

- 10.1.1.3.1. Food & Beverages

- 10.1.1.3.2. Pharmaceutical & Healthcare

- 10.1.1.3.3. Other End-Users

- 10.1.1.1. By Print Process

- 10.1.2. Shrink & Stretch Sleeve Label

- 10.1.2.1. Shrink Sleeve

- 10.1.2.2. By Material

- 10.1.2.2.1. PVC

- 10.1.2.2.2. PET

- 10.1.2.2.3. OPP & OPS

- 10.1.2.2.4. Other Materials (PO, PLA, etc.)

- 10.1.3. In-Mold Label

- 10.1.4. Wet Glue Label

- 10.1.5. Thermal Transfer Label

- 10.1.5.1. Paper

- 10.1.5.2. Polyester

- 10.1.6. Wrap Around Label

- 10.1.1. Pressure-Sensitive Label

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Latin America Packaging and Label Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Pressure-Sensitive Label

- 11.1.1.1. By Print Process

- 11.1.1.1.1. Offset Printing

- 11.1.1.1.2. Flexography Printing

- 11.1.1.1.3. Gravure

- 11.1.1.1.4. Other Analog Printing Process

- 11.1.1.1.5. Digital Printing

- 11.1.1.2. By Product Type

- 11.1.1.2.1. Liner

- 11.1.1.2.2. Linerless

- 11.1.1.2.3. VIP

- 11.1.1.2.4. Prime

- 11.1.1.2.5. Functional & Security

- 11.1.1.2.6. Promotional

- 11.1.1.3. End-User Industry

- 11.1.1.3.1. Food & Beverages

- 11.1.1.3.2. Pharmaceutical & Healthcare

- 11.1.1.3.3. Other End-Users

- 11.1.1.1. By Print Process

- 11.1.2. Shrink & Stretch Sleeve Label

- 11.1.2.1. Shrink Sleeve

- 11.1.2.2. By Material

- 11.1.2.2.1. PVC

- 11.1.2.2.2. PET

- 11.1.2.2.3. OPP & OPS

- 11.1.2.2.4. Other Materials (PO, PLA, etc.)

- 11.1.3. In-Mold Label

- 11.1.4. Wet Glue Label

- 11.1.5. Thermal Transfer Label

- 11.1.5.1. Paper

- 11.1.5.2. Polyester

- 11.1.6. Wrap Around Label

- 11.1.1. Pressure-Sensitive Label

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Avery Dennison

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Leading Edge labels & Packaging*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Taghleef Industries Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 WestRock Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vintech Polymers Private Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Fort Dearborn

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 KRIS FLEXIPACKS PVT LTD

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Fort Dearborn Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Constantia Flexibles Group GmbH

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Bemis Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 UPM Raflatc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Royal Sens Group

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Klockner Pentaplast

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 CCL Industries LLC

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 3M Company

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Huhtamaki Group

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Lintec Corporation

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Multi-Color Corporation

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Fuji Seal International Inc

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Lintec

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Mondi

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 CPC Packaging

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Berry Global

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 GTPL

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 Neenah Inc

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.1 Avery Dennison

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Packaging and Label Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Packaging and Label Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Packaging and Label Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Packaging and Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Packaging and Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Packaging and Label Industry Revenue (Million), by Type 2025 & 2033

- Figure 7: Europe Packaging and Label Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: Europe Packaging and Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Packaging and Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Packaging and Label Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Asia Pacific Packaging and Label Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Asia Pacific Packaging and Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Packaging and Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East Packaging and Label Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Middle East Packaging and Label Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Middle East Packaging and Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Middle East Packaging and Label Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Latin America Packaging and Label Industry Revenue (Million), by Type 2025 & 2033

- Figure 19: Latin America Packaging and Label Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Latin America Packaging and Label Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Latin America Packaging and Label Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Packaging and Label Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Packaging and Label Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Packaging and Label Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Packaging and Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Packaging and Label Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Packaging and Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Packaging and Label Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Packaging and Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Packaging and Label Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Global Packaging and Label Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Packaging and Label Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 12: Global Packaging and Label Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Packaging and Label Industry?

The projected CAGR is approximately 4.90%.

2. Which companies are prominent players in the Packaging and Label Industry?

Key companies in the market include Avery Dennison, Leading Edge labels & Packaging*List Not Exhaustive, Taghleef Industries Inc, WestRock Company, Vintech Polymers Private Limited, Fort Dearborn, KRIS FLEXIPACKS PVT LTD, Fort Dearborn Company, Constantia Flexibles Group GmbH, Bemis Company, UPM Raflatc, Royal Sens Group, Klockner Pentaplast, CCL Industries LLC, 3M Company, Huhtamaki Group, Lintec Corporation, Multi-Color Corporation, Fuji Seal International Inc, Lintec, Mondi, CPC Packaging, Berry Global, GTPL, Neenah Inc.

3. What are the main segments of the Packaging and Label Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.29 Million as of 2022.

5. What are some drivers contributing to market growth?

The issues related to recycling of release liners and the ability to enable direct digital printing is expected to spur demand; Ability to conform to any size and shape. and yet provide the necessary protection.

6. What are the notable trends driving market growth?

Food and Beverage End-User Segment is Expected to Drive Growth of Labels.

7. Are there any restraints impacting market growth?

; Fluctuating Oil Prices.

8. Can you provide examples of recent developments in the market?

March 2021 - Dearborn Company has announced that it has acquired Hammer Packaging Corporation. The combined organization takes advantage of Hammer's state-of-the-art technology to enhance Fort Dearborn's leadership position in the decorative label and packaging marketplace by further expanding the company's geographic footprint, capacity, and capabilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Packaging and Label Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Packaging and Label Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Packaging and Label Industry?

To stay informed about further developments, trends, and reports in the Packaging and Label Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence