Key Insights

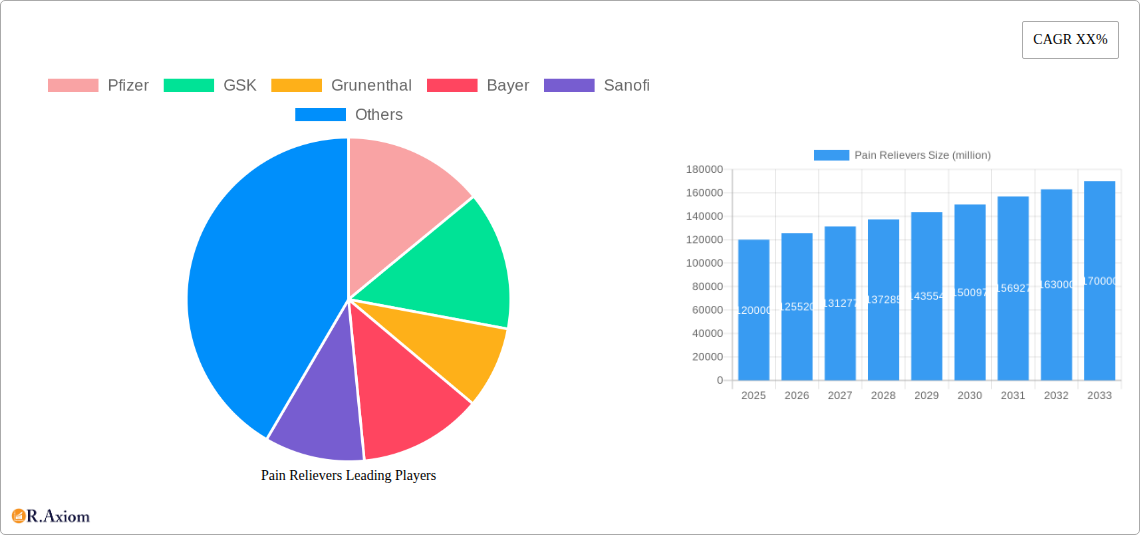

The global pain relievers market is poised for robust growth, projected to reach a significant market size of approximately $120 billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 4.5% through 2033. This expansion is fueled by an increasing prevalence of chronic pain conditions, an aging global population experiencing age-related ailments, and a growing awareness of pain management solutions. The market is further propelled by advancements in drug development, leading to more effective and targeted pain relief options across various applications, including headaches, toothaches, arthralgia, and menstrual pain. The dominance of Nonsteroidal Anti-inflammatory Drugs (NSAIDs) is expected to continue due to their widespread availability and efficacy, while central analgesics are gaining traction for more severe pain management.

Key drivers for this market expansion include the rising incidence of lifestyle-related diseases and the growing demand for over-the-counter (OTC) pain medications. However, the market also faces restraints such as stringent regulatory approvals for new drugs and concerns regarding the potential side effects and addiction associated with certain analgesics. Despite these challenges, the increasing focus on research and development by major pharmaceutical players like Pfizer, GSK, and Bayer, coupled with the expansion of generic pain relievers, is expected to maintain a positive growth trajectory. Geographically, North America and Europe currently lead the market due to high healthcare spending and established patient awareness, while the Asia Pacific region presents significant untapped growth potential driven by its large population and improving healthcare infrastructure.

Pain Relievers Market Concentration & Innovation

The global pain relievers market, projected to reach over a million million in value by 2033, exhibits a dynamic landscape characterized by moderate to high concentration in specific segments, driven by continuous innovation and evolving regulatory frameworks. Key players like Pfizer, GSK, and Bayer command significant market share, leveraging extensive R&D investments and established distribution networks. Innovation in this sector is primarily fueled by the pursuit of safer, more effective analgesics with reduced side effects, particularly in the face of the ongoing opioid crisis and increased scrutiny on prescription painkillers. The development of novel drug delivery systems, combination therapies, and non-opioid alternatives are at the forefront of R&D efforts. Regulatory bodies, such as the FDA and EMA, play a pivotal role in shaping market access and product approval, emphasizing stringent safety and efficacy standards. Product substitutes, including both over-the-counter (OTC) medications and non-pharmacological interventions like physical therapy and acupuncture, present a continuous challenge and opportunity for market players to differentiate their offerings. End-user trends are increasingly leaning towards patient-centric solutions, with a growing demand for personalized pain management strategies and greater access to information regarding treatment options. Mergers and acquisitions (M&A) activity remains a significant driver of market consolidation and strategic growth. Recent M&A deals have seen valuations in the tens of millions, as larger pharmaceutical companies seek to acquire innovative pipelines or expand their portfolios in key therapeutic areas. For instance, acquisitions of specialized biotech firms focusing on novel analgesic mechanisms are becoming more common.

- Market Share Distribution: Dominated by a few key players, with significant concentration in the Nonsteroidal Anti-inflammatory Drugs (NSAIDs) segment.

- Innovation Focus: Novel drug development, opioid alternatives, and improved drug delivery systems.

- Regulatory Impact: Strict approval processes influencing market entry and product claims.

- M&A Deal Value: Averaging in the tens of millions, signifying strategic consolidation.

Pain Relievers Industry Trends & Insights

The global pain relievers market is experiencing robust growth, propelled by a confluence of escalating chronic pain conditions, an aging global population, and increasing healthcare expenditure worldwide. The market is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately xx% from 2025 to 2033, reflecting sustained demand across diverse patient demographics. Technological disruptions are playing a transformative role, with advancements in genomics and personalized medicine paving the way for more targeted and effective pain management solutions. Artificial intelligence (AI) is increasingly being employed in drug discovery and development, accelerating the identification of novel analgesic compounds and optimizing clinical trial processes. Furthermore, the integration of digital health platforms and wearable devices is enabling remote patient monitoring and data-driven therapeutic adjustments, enhancing treatment efficacy and patient adherence. Consumer preferences are undergoing a significant shift, with a growing emphasis on non-addictive and natural pain relief options. This trend is driving demand for herbal analgesics and topical formulations, alongside a renewed interest in complementary and alternative medicine (CAM) approaches. The competitive dynamics are intensifying, characterized by strategic partnerships between pharmaceutical giants and emerging biotechnology companies, as well as significant investments in R&D to address unmet medical needs. Market penetration for OTC pain relievers remains high, supported by accessibility and affordability, while the prescription segment continues to evolve with the introduction of advanced therapies for moderate to severe pain. The COVID-19 pandemic, while initially disrupting supply chains, also highlighted the critical importance of pain management, further solidifying the market's resilience and long-term growth trajectory. The increasing prevalence of conditions like osteoarthritis, back pain, and migraines, exacerbated by sedentary lifestyles and an aging demographic, directly fuels the demand for effective pain relief. The market is also seeing innovation in delivery mechanisms, moving beyond traditional oral pills to include patches, gels, and injectables, offering tailored solutions for specific pain types and patient needs. This diversification of product offerings caters to a broader spectrum of consumer preferences and medical requirements, further driving market expansion.

Dominant Markets & Segments in Pain Relievers

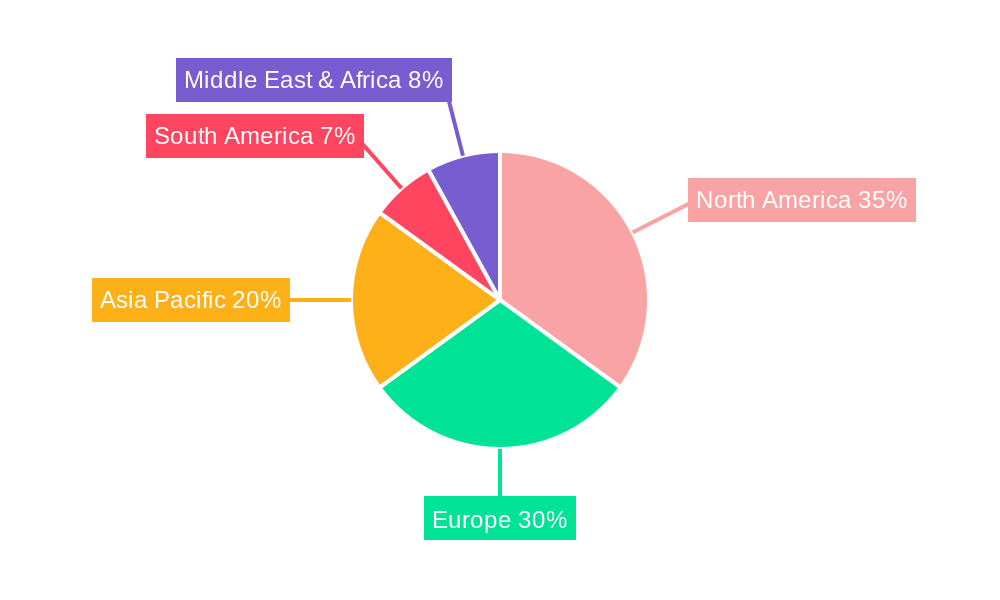

The global pain relievers market is characterized by distinct regional and segment-specific dominance, driven by a complex interplay of socioeconomic factors, disease prevalence, and healthcare infrastructure. Within the Application segment, Arthralgia stands out as a dominant driver, fueled by the rapidly aging global population and the increasing incidence of osteoarthritis and other degenerative joint conditions. Countries with higher life expectancies and a greater prevalence of lifestyle-related chronic diseases typically exhibit stronger demand for arthralgia relief. Economic policies that support robust healthcare systems and encourage preventative care further bolster this segment. Infrastructure development, including the availability of specialized orthopedic clinics and physical therapy centers, also contributes to the sustained growth of arthralgia pain reliever consumption.

In terms of Types, Nonsteroidal Anti-inflammatory Drugs (NSAIDs) currently hold a dominant position in the market. Their widespread availability as both prescription and over-the-counter medications, coupled with their efficacy in managing mild to moderate pain and inflammation associated with conditions like arthritis, headaches, and menstrual cramps, contributes to their substantial market share. The development of both generic and branded NSAIDs ensures competitive pricing and accessibility across diverse economic strata. Furthermore, ongoing research into novel NSAID formulations with improved gastrointestinal safety profiles continues to sustain their market relevance.

The Headache application segment also commands significant market share, driven by the high prevalence of tension headaches, migraines, and cluster headaches globally. Factors such as increased screen time, stress, and environmental factors contribute to the persistent demand for headache relief. The availability of a wide array of OTC and prescription headache medications, including those combining analgesics with caffeine or antiemetics, caters to a broad spectrum of patient needs.

Conversely, the Toothache segment, while consistently present, experiences fluctuations based on dental hygiene awareness and access to dental care. Improving dental health infrastructure and preventative campaigns can moderate demand in this segment over the long term. Menstrual Pain represents another significant application, with a substantial portion of the female population seeking effective relief, driving consistent demand for specialized formulations.

Dominant Application: Arthralgia

- Key Drivers: Aging global population, rising incidence of osteoarthritis, economic policies supporting healthcare, advanced orthopedic infrastructure.

- Market Size: Millions of millions.

- Growth Projection: Sustained growth due to demographic trends.

Dominant Type: Nonsteroidal Anti-inflammatory Drugs (NSAIDs)

- Key Drivers: Widespread availability (OTC & prescription), proven efficacy for mild to moderate pain, ongoing research for improved safety profiles.

- Market Share: Majority of the market by volume.

- Competitive Landscape: Dominated by both branded and generic manufacturers.

Significant Application: Headache

- Key Drivers: High prevalence of migraines and tension headaches, lifestyle factors (stress, screen time).

- Product Variety: Extensive range of OTC and prescription options.

Pain Relievers Product Developments

The pain relievers market is witnessing a surge in product developments focused on enhancing efficacy, safety, and patient convenience. Innovations are primarily directed towards creating novel non-opioid analgesics with unique mechanisms of action to combat chronic pain without the risk of addiction. This includes the exploration of cannabinoid-based therapies, nerve growth factor (NGF) inhibitors, and compounds targeting specific ion channels involved in pain signaling. Furthermore, advancements in drug delivery systems are gaining traction, with a growing emphasis on long-acting formulations, transdermal patches, and targeted delivery mechanisms that minimize systemic exposure and side effects. These developments aim to provide sustained pain relief, improve patient compliance, and offer tailored treatment options for various pain etiologies. The competitive advantage lies in the ability to address unmet medical needs, such as refractory chronic pain, and offer a superior safety profile compared to existing treatments.

Report Scope & Segmentation Analysis

This comprehensive report delves into the global pain relievers market, providing detailed insights into its current status and future trajectory from 2019 to 2033. The market is meticulously segmented to offer a granular understanding of its dynamics.

Application Segmentation:

- Headache: This segment encompasses various types of headaches, including migraines and tension headaches, and is expected to see continued growth driven by lifestyle factors and increasing awareness.

- Toothache: While a significant segment, its growth is influenced by dental health awareness and access to dental care.

- Arthralgia: Driven by the aging population and the prevalence of osteoarthritis, this segment is poised for robust and sustained expansion.

- Menstrual Pain: A consistent market with demand for effective relief solutions tailored for women.

- Other: This category includes pain associated with injuries, post-operative pain, and various other chronic and acute conditions, representing a broad and diverse market.

Type Segmentation:

- Nonsteroidal Anti-inflammatory Drugs (NSAIDs): This category, including both OTC and prescription options, is expected to maintain its dominant market position due to widespread use and proven efficacy.

- Central Analgesics: This segment, encompassing opioids and non-opioid central-acting pain relievers, is undergoing significant shifts due to regulatory scrutiny and the development of safer alternatives.

Key Drivers of Pain Relievers Growth

The global pain relievers market is propelled by several key drivers that are shaping its growth trajectory. The increasing prevalence of chronic pain conditions, such as arthritis, back pain, and migraines, directly fuels the demand for effective pain management solutions. An aging global population, characterized by longer lifespans, is also a significant factor, as elderly individuals are more susceptible to chronic pain. Advances in medical research and pharmaceutical innovation are leading to the development of novel, safer, and more effective pain relievers, expanding treatment options. Furthermore, rising healthcare expenditure globally, coupled with increased patient awareness about pain management options, contributes to market expansion. Technological advancements in drug delivery systems are also playing a crucial role, enabling more targeted and convenient pain relief.

- Rising Chronic Pain Prevalence: Escalating rates of conditions like arthritis and back pain.

- Aging Global Population: Increased susceptibility to chronic pain in older demographics.

- Pharmaceutical Innovation: Development of novel and safer analgesic compounds.

- Increasing Healthcare Expenditure: Greater investment in pain management solutions.

- Enhanced Patient Awareness: Growing understanding and demand for pain relief options.

Challenges in the Pain Relievers Sector

Despite robust growth prospects, the pain relievers sector faces several significant challenges that could impede market expansion. The ongoing opioid crisis and increasing regulatory scrutiny surrounding opioid-based painkillers have led to stricter prescribing guidelines and a push towards non-addictive alternatives. This regulatory pressure can slow down the approval and adoption of certain pain relief products. Supply chain disruptions, exacerbated by geopolitical events and global health crises, can impact the availability and cost of raw materials and finished products. Intense competition from both established pharmaceutical giants and emerging biotech companies, as well as the widespread availability of generic alternatives, can lead to price erosion and pressure on profit margins. Additionally, challenges in accurately diagnosing and treating complex chronic pain conditions, along with patient adherence issues, can limit the effectiveness of available treatments.

- Opioid Crisis & Regulatory Scrutiny: Stricter regulations on opioid painkillers.

- Supply Chain Volatility: Disruptions impacting raw material availability and costs.

- Intense Competition: Pressure from generics and emerging players.

- Diagnostic & Treatment Complexity: Challenges in effectively managing chronic pain.

- Patient Adherence Issues: Difficulty in ensuring consistent medication use.

Emerging Opportunities in Pain Relievers

The pain relievers market is ripe with emerging opportunities driven by evolving consumer preferences and technological advancements. The growing demand for natural and non-addictive pain relief solutions presents a significant opportunity for companies focusing on herbal analgesics, botanical extracts, and other naturally derived compounds. Advancements in biotechnology are enabling the development of highly targeted therapies, including gene therapies and regenerative medicine approaches for chronic pain conditions, representing a substantial future growth area. The integration of digital health technologies, such as AI-powered diagnostics, remote patient monitoring, and personalized pain management apps, offers opportunities to improve treatment efficacy and patient engagement. Furthermore, the expansion of healthcare access in emerging economies presents a vast untapped market for pain relief products. The increasing focus on preventative pain management and wellness is also creating new market niches.

- Natural & Non-Addictive Therapies: Growing consumer preference for herbal and botanical pain relief.

- Targeted Therapies: Development of gene therapies and regenerative medicine for chronic pain.

- Digital Health Integration: AI, remote monitoring, and personalized pain management apps.

- Emerging Markets: Expansion of healthcare access in developing economies.

- Preventative Pain Management: Focus on wellness and proactive pain reduction strategies.

Leading Players in the Pain Relievers Market

- Pfizer

- GSK

- Grunenthal

- Bayer

- Sanofi

- Eli Lilly

- AstraZeneca

- Endo

- Merck

- Depomed

- Yunnan Baiyao

- Teva

- J&J

- Allergan

- Purdue

- Reckitt Benckiser Group Plc

- Novartis AG

- Topical BioMedics

- AdvaCare Pharma

- Sun Pharmaceutical

Key Developments in Pain Relievers Industry

- 2024 Jan: Launch of a novel topical NSAID formulation for localized arthritis pain by Bayer, offering improved skin penetration and reduced systemic absorption.

- 2023 Nov: Grunenthal secures FDA approval for a new non-opioid analgesic targeting neuropathic pain, expanding treatment options for patients with nerve damage.

- 2023 Oct: GSK announces a strategic partnership with a biotech firm to co-develop gene therapy for chronic pain conditions, signaling a move towards cutting-edge treatments.

- 2023 Sep: Pfizer expands its OTC pain relief portfolio with a new combination product for severe headaches, integrating multiple active ingredients for enhanced efficacy.

- 2023 Jul: Purdue Pharma announces a significant restructuring of its opioid business, focusing on pain management alternatives and addiction treatment research.

- 2022 Dec: Eli Lilly receives expanded indication for its monoclonal antibody treatment for chronic migraine, further solidifying its market position.

- 2022 Oct: Teva Pharmaceuticals launches a new generic version of a widely used central analgesic, increasing accessibility and affordability.

- 2022 Aug: Sanofi invests heavily in R&D for novel pain mechanisms, particularly focusing on inflammatory pathways involved in chronic pain.

- 2022 Jun: AstraZeneca announces positive Phase III trial results for a new non-opioid pain reliever, showcasing a strong safety profile and significant efficacy.

- 2022 Apr: Reckitt Benckiser Group Plc acquires a prominent natural pain relief brand, capitalizing on the growing consumer demand for alternative therapies.

Strategic Outlook for Pain Relievers Market

The strategic outlook for the pain relievers market is overwhelmingly positive, driven by a sustained and growing need for effective pain management solutions. The market's future trajectory will be shaped by a continued emphasis on developing non-addictive and safer analgesic alternatives, spurred by ongoing regulatory pressures and patient demand. Innovation in drug delivery systems, including long-acting formulations and targeted therapies, will be crucial for enhancing patient outcomes and compliance. Strategic partnerships and M&A activities are expected to continue as companies seek to consolidate market share, acquire novel pipelines, and expand their global reach. The increasing integration of digital health technologies offers a significant opportunity to personalize pain management and improve patient engagement. Companies that can effectively navigate the evolving regulatory landscape, prioritize patient-centric innovation, and leverage technological advancements are poised for substantial growth and market leadership in the coming years.

Pain Relievers Segmentation

-

1. Application

- 1.1. Headache

- 1.2. Toothache

- 1.3. Arthralgia

- 1.4. Menstrual Pain

- 1.5. Other

-

2. Types

- 2.1. Nonsteroidal Anti-inflammatory Drugs

- 2.2. Central Analgesics

Pain Relievers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pain Relievers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pain Relievers Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Headache

- 5.1.2. Toothache

- 5.1.3. Arthralgia

- 5.1.4. Menstrual Pain

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Nonsteroidal Anti-inflammatory Drugs

- 5.2.2. Central Analgesics

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Pain Relievers Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Headache

- 6.1.2. Toothache

- 6.1.3. Arthralgia

- 6.1.4. Menstrual Pain

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Nonsteroidal Anti-inflammatory Drugs

- 6.2.2. Central Analgesics

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Pain Relievers Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Headache

- 7.1.2. Toothache

- 7.1.3. Arthralgia

- 7.1.4. Menstrual Pain

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Nonsteroidal Anti-inflammatory Drugs

- 7.2.2. Central Analgesics

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Pain Relievers Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Headache

- 8.1.2. Toothache

- 8.1.3. Arthralgia

- 8.1.4. Menstrual Pain

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Nonsteroidal Anti-inflammatory Drugs

- 8.2.2. Central Analgesics

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Pain Relievers Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Headache

- 9.1.2. Toothache

- 9.1.3. Arthralgia

- 9.1.4. Menstrual Pain

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Nonsteroidal Anti-inflammatory Drugs

- 9.2.2. Central Analgesics

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Pain Relievers Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Headache

- 10.1.2. Toothache

- 10.1.3. Arthralgia

- 10.1.4. Menstrual Pain

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Nonsteroidal Anti-inflammatory Drugs

- 10.2.2. Central Analgesics

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Pfizer

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 GSK

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Grunenthal

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bayer

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sanofi

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Eli Lilly

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AstraZeneca

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Endo

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Merck

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Depomed

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Yunnan Baiyao

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Teva

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 J&J

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Allergan

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Purdue

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Reckitt Benckiser Group Plc

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Novartis AG

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Topical BioMedics

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 AdvaCare Pharma

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Sun Pharmaceutical

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Pfizer

List of Figures

- Figure 1: Global Pain Relievers Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Pain Relievers Revenue (million), by Application 2024 & 2032

- Figure 3: North America Pain Relievers Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Pain Relievers Revenue (million), by Types 2024 & 2032

- Figure 5: North America Pain Relievers Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Pain Relievers Revenue (million), by Country 2024 & 2032

- Figure 7: North America Pain Relievers Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Pain Relievers Revenue (million), by Application 2024 & 2032

- Figure 9: South America Pain Relievers Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Pain Relievers Revenue (million), by Types 2024 & 2032

- Figure 11: South America Pain Relievers Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Pain Relievers Revenue (million), by Country 2024 & 2032

- Figure 13: South America Pain Relievers Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Pain Relievers Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Pain Relievers Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Pain Relievers Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Pain Relievers Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Pain Relievers Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Pain Relievers Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Pain Relievers Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Pain Relievers Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Pain Relievers Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Pain Relievers Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Pain Relievers Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Pain Relievers Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Pain Relievers Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Pain Relievers Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Pain Relievers Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Pain Relievers Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Pain Relievers Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Pain Relievers Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Pain Relievers Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Pain Relievers Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Pain Relievers Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Pain Relievers Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Pain Relievers Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Pain Relievers Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Pain Relievers Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Pain Relievers Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Pain Relievers Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Pain Relievers Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Pain Relievers Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Pain Relievers Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Pain Relievers Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Pain Relievers Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Pain Relievers Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Pain Relievers Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Pain Relievers Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Pain Relievers Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Pain Relievers Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Pain Relievers Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pain Relievers?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Pain Relievers?

Key companies in the market include Pfizer, GSK, Grunenthal, Bayer, Sanofi, Eli Lilly, AstraZeneca, Endo, Merck, Depomed, Yunnan Baiyao, Teva, J&J, Allergan, Purdue, Reckitt Benckiser Group Plc, Novartis AG, Topical BioMedics, AdvaCare Pharma, Sun Pharmaceutical.

3. What are the main segments of the Pain Relievers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pain Relievers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pain Relievers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pain Relievers?

To stay informed about further developments, trends, and reports in the Pain Relievers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence