Key Insights

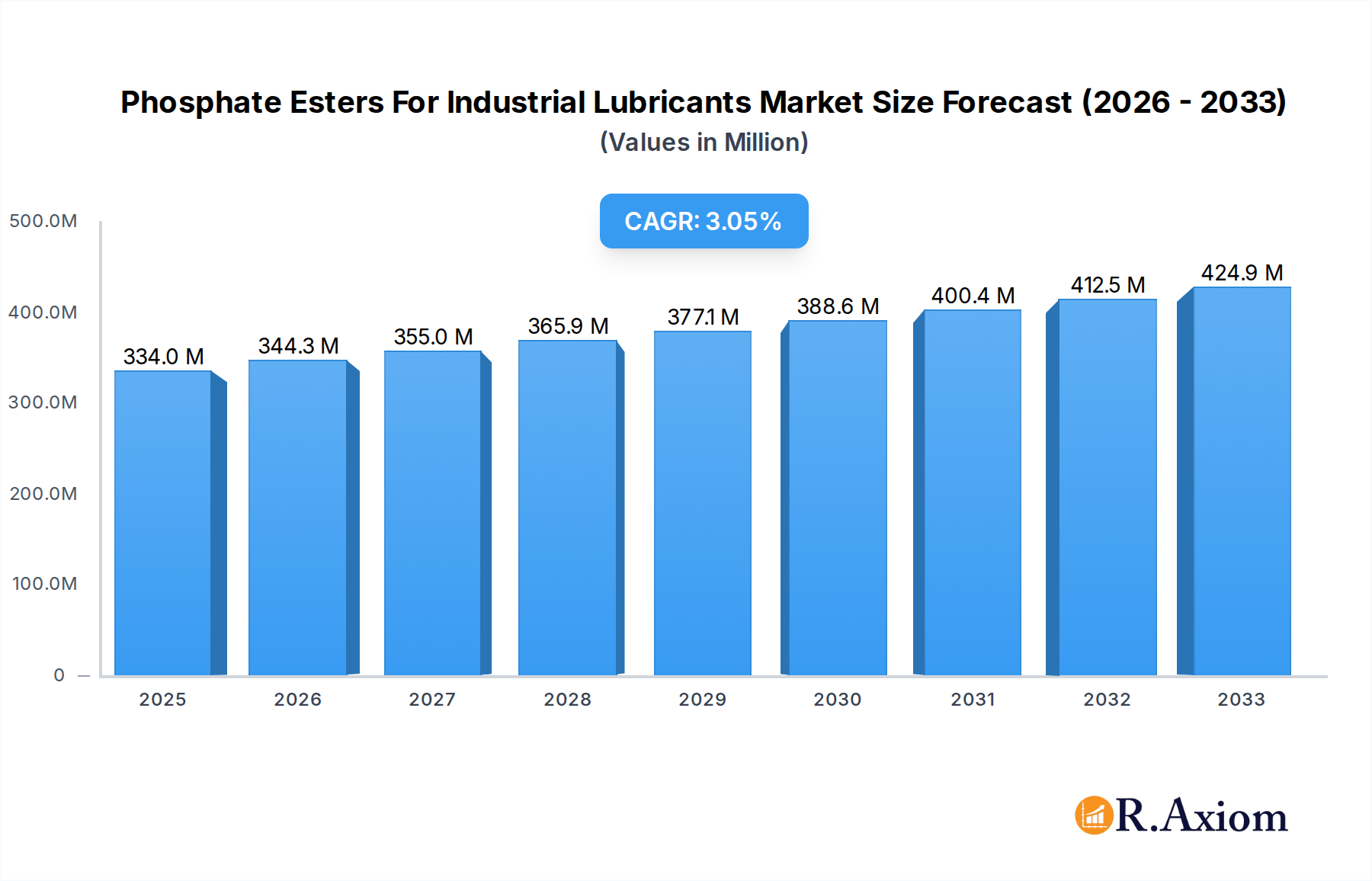

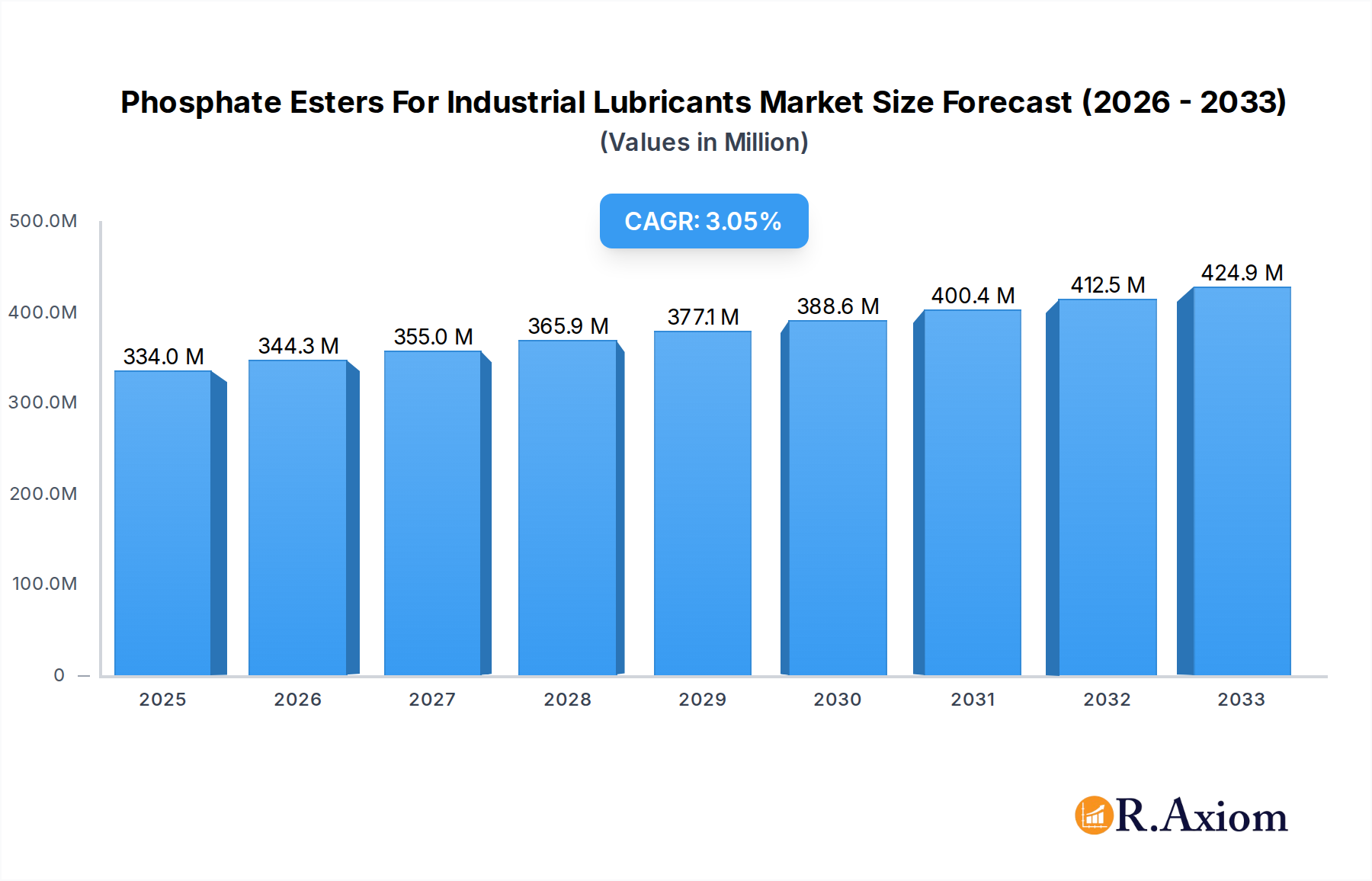

The global market for Phosphate Esters for Industrial Lubricants is projected to experience steady growth, reaching an estimated $334 million by 2025. This expansion is driven by the increasing demand for high-performance lubricants across various industrial applications, particularly in sectors like manufacturing, automotive, and heavy machinery. Phosphate esters are highly valued for their excellent lubricating properties, including wear resistance, extreme pressure performance, and fire retardancy, making them crucial components in formulations designed to enhance equipment longevity and operational efficiency. The market's CAGR of 3.1% over the forecast period (2025-2033) indicates a mature yet robust growth trajectory, fueled by ongoing technological advancements in lubricant formulations and a growing emphasis on sustainable and eco-friendly industrial practices. Emerging economies, with their expanding industrial bases, are expected to contribute significantly to this market's upward trend.

Phosphate Esters For Industrial Lubricants Market Size (In Million)

Key trends shaping the Phosphate Esters for Industrial Lubricants market include the development of advanced formulations that offer improved biodegradability and reduced environmental impact, aligning with stricter regulatory landscapes and corporate sustainability goals. The growing adoption of fire-resistant hydraulic fluids in sectors like mining and metal processing, where safety is paramount, will also bolster demand. Conversely, fluctuations in raw material prices and the development of alternative lubrication technologies could present some restraints. The market is segmented by application into Hydraulic Oils, Rolling Oils, and Others, with Hydraulic Oils currently holding a dominant share due to their widespread use. By type, Monophosphate, Diphosphate, and Triphosphate esters cater to diverse performance requirements. Leading companies such as LANXESS, BASF, and ExxonMobil are at the forefront of innovation, investing in research and development to meet evolving industry needs and maintain a competitive edge in this dynamic market.

Phosphate Esters For Industrial Lubricants Company Market Share

Here's a comprehensive, SEO-optimized report description for "Phosphate Esters For Industrial Lubricants," designed for immediate use without modification:

Phosphate Esters For Industrial Lubricants Market Concentration & Innovation

The global phosphate esters for industrial lubricants market exhibits a moderate level of concentration, with key players like LANXESS, Chemtura (now part of Lanxess), Dow, ExxonMobil, and BASF holding significant market share. The market is driven by continuous innovation, particularly in developing high-performance, environmentally friendly lubricant additives. Regulatory frameworks, such as REACH in Europe and EPA regulations in the US, are increasingly influencing product development, pushing for reduced toxicity and improved biodegradability. Product substitutes, including synthetic esters and polyalphaolefins (PAOs), pose a competitive challenge, necessitating constant evolution in phosphate ester formulations. End-user trends, such as the demand for lubricants with extended service life, improved thermal stability, and enhanced fire resistance in industries like aerospace, automotive, and metalworking, are key innovation drivers. Mergers and acquisitions (M&A) have played a crucial role in market consolidation, with estimated deal values reaching in the tens of millions of dollars annually over the historical period. For instance, the acquisition of Chemtura by Lanxess in 2017 represented a significant M&A event, reshaping the competitive landscape and market share distribution. The study estimates the market share of the top five players to be around 60% in 2025.

Phosphate Esters For Industrial Lubricants Industry Trends & Insights

The industrial lubricants market is experiencing robust growth, propelled by an increasing demand for high-performance lubricants that enhance equipment efficiency, reduce wear and tear, and extend operational lifespan. Phosphate esters, with their inherent properties of fire resistance, anti-wear, and extreme pressure (EP) performance, are integral to meeting these demands across a multitude of industrial applications. The global market for phosphate esters in industrial lubricants is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 5.8% from 2019 to 2033, reaching an estimated market size of over $3,500 million by 2033. This growth is fueled by several key factors. Firstly, the burgeoning manufacturing sector, particularly in emerging economies in Asia-Pacific, is driving demand for advanced industrial lubricants. Automation and the increasing complexity of machinery in sectors like automotive manufacturing, metalworking, and power generation necessitate lubricants with superior protective capabilities, a niche that phosphate esters effectively fill.

Secondly, technological advancements in lubricant formulation are leading to the development of next-generation phosphate esters with improved environmental profiles. This includes formulations with lower volatile organic compound (VOC) content, enhanced biodegradability, and reduced toxicity, aligning with stringent environmental regulations and growing corporate sustainability initiatives. The market penetration of bio-based and eco-friendly lubricants is on the rise, prompting manufacturers to invest in R&D to create phosphate ester additives that meet these green criteria without compromising performance.

Thirdly, the increasing stringency of safety regulations, especially concerning fire hazards in industrial settings, is a significant market driver. Phosphate esters are widely adopted as fire-retardant additives in hydraulic fluids, turbine oils, and compressor oils used in high-risk environments like mining, aerospace, and oil and gas exploration. Their ability to suppress flames and prevent catastrophic failures makes them indispensable in these critical applications.

Finally, the competitive dynamics are shaped by both established global players and regional manufacturers. Companies are focusing on expanding their product portfolios, enhancing their manufacturing capacities, and forging strategic partnerships to capture market share. The trend towards customized lubricant solutions for specific industrial needs is also creating opportunities for specialized phosphate ester manufacturers. The market penetration of phosphate esters in the overall industrial lubricants market is estimated to be around 15% in 2025.

Dominant Markets & Segments in Phosphate Esters For Industrial Lubricants

The phosphate esters for industrial lubricants market is characterized by dominant regional influences and specific application and type segmentations.

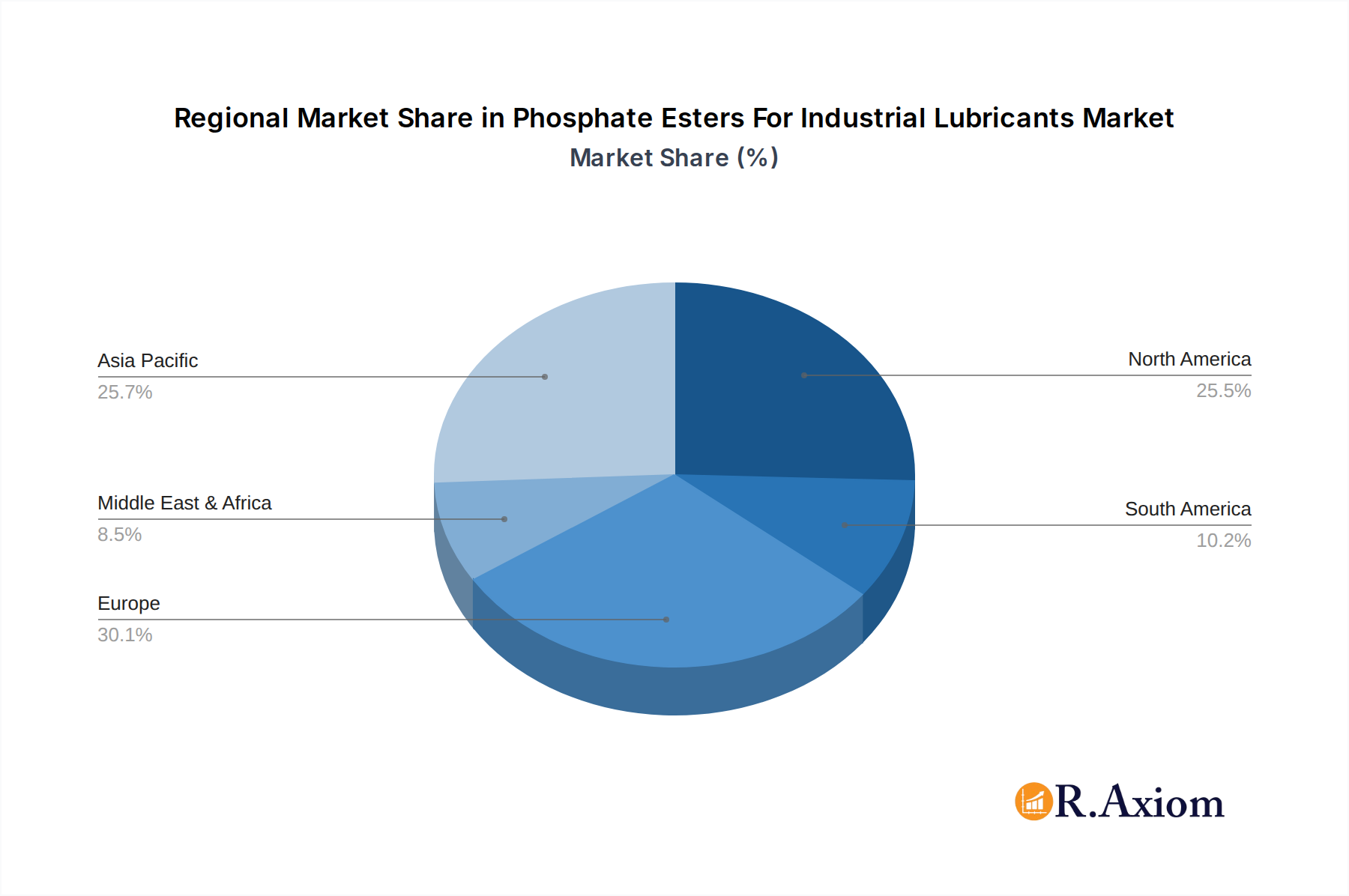

Dominant Regions and Countries: Asia-Pacific stands out as the dominant market for phosphate esters in industrial lubricants, driven by its robust manufacturing base, rapid industrialization, and significant investments in infrastructure development. Countries like China, India, and South Korea are leading the demand due to their expansive automotive, electronics, and heavy machinery industries. Economic policies that encourage industrial growth and foreign investment further bolster the market in this region. The sheer volume of manufacturing output in Asia-Pacific translates directly into substantial demand for industrial lubricants and their essential additive components.

North America, particularly the United States, also represents a significant market. This dominance is attributed to the presence of advanced industries such as aerospace, oil and gas, and specialized manufacturing, which demand high-performance lubricants with critical properties like fire resistance and extreme pressure capabilities. Stringent environmental and safety regulations in North America also push the adoption of advanced lubricant solutions.

Dominant Application Segments:

- Hydraulic Oils: This segment represents a substantial portion of the phosphate ester market due to the widespread use of hydraulic systems across diverse industries. Hydraulic fluids are critical for power transmission and control in manufacturing, construction, and transportation equipment. The demand for fire-resistant hydraulic fluids, especially in mining, steel production, and aviation, fuels the use of phosphate esters. The market size for phosphate esters in hydraulic oils is projected to be over $1,800 million in 2025.

- Rolling Oils: In the metalworking industry, rolling oils are essential for lubricating and cooling during metal rolling processes. Phosphate esters are utilized for their anti-wear and EP properties, which are crucial for preventing damage to rolling machinery and ensuring high-quality metal products. The growing demand for steel and aluminum in automotive and construction sectors directly impacts the consumption of rolling oils.

- Others: This encompasses a broad range of applications, including turbine oils, compressor oils, gear oils, and metalworking fluids. The fire-retardant properties of phosphate esters are particularly valued in turbine oils for power generation and compressor oils in industries where fire safety is paramount.

Dominant Type Segments:

- Triphosphate: Triphosphate esters are generally considered to offer superior performance characteristics, including enhanced fire resistance and extreme pressure properties, making them highly sought after in demanding industrial applications. Their complex molecular structure contributes to their effectiveness in high-stress environments. The market size for triphosphates is estimated to be over $1,500 million in 2025.

- Diphosphate: Diphosphate esters offer a balance of performance and cost-effectiveness, making them a versatile choice for various lubricant formulations. They provide good anti-wear and EP capabilities.

- Monophosphate: Monophosphate esters are often used in specific formulations where their unique properties, such as improved solubility or specific additive interactions, are beneficial.

Phosphate Esters For Industrial Lubricants Product Developments

Recent product developments in phosphate esters for industrial lubricants focus on enhancing environmental compatibility, improving high-temperature performance, and offering superior fire resistance. Innovations include the development of low-VOC (Volatile Organic Compound) formulations that meet stringent air quality regulations. Manufacturers are also introducing phosphate esters with improved biodegradability and reduced aquatic toxicity to cater to the growing demand for eco-friendly lubricants. Novel chemistries are being explored to provide enhanced anti-wear and extreme pressure (EP) protection, extending equipment lifespan and reducing maintenance costs. These developments aim to provide competitive advantages by meeting specific end-user requirements and regulatory mandates, ensuring market fit and sustained growth.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global phosphate esters for industrial lubricants market. The market is segmented by Application into Hydraulic Oils, Rolling Oils, and Others. The Hydraulic Oils segment is projected to exhibit a CAGR of approximately 6.1% from 2025 to 2033, driven by the widespread use of hydraulic systems in manufacturing and construction. The Rolling Oils segment is anticipated to grow at a CAGR of around 5.5%, supported by the metal fabrication industry. The "Others" segment, encompassing turbine oils, compressor oils, and gear oils, is expected to witness a CAGR of approximately 5.7%, fueled by the demand for specialized lubricants in power generation and industrial machinery.

The market is further segmented by Type into Monophosphate, Diphosphate, and Triphosphate. The Triphosphate segment is forecast to lead the market in terms of value, with an estimated market size of over $1,500 million in 2025, due to its superior performance characteristics. The Diphosphate segment is expected to grow at a CAGR of around 5.9%, while the Monophosphate segment is projected to expand at a CAGR of approximately 5.3%. Competitive dynamics within each segment are influenced by performance requirements, cost considerations, and regulatory compliance.

Key Drivers of Phosphate Esters For Industrial Lubricants Growth

Several key drivers are propelling the growth of the phosphate esters for industrial lubricants market. Technologically, the increasing demand for high-performance lubricants with superior fire resistance, anti-wear, and extreme pressure (EP) properties is paramount. Economic factors, such as the expansion of manufacturing sectors globally, particularly in emerging economies, directly translate to higher lubricant consumption. Regulatory drivers, including stricter safety standards in hazardous environments and growing environmental consciousness, are pushing for the adoption of advanced, safer lubricant additives like phosphate esters. For instance, the aviation industry's strict fire safety regulations necessitate the use of phosphate ester-based hydraulic fluids, a critical growth driver. The estimated market size for phosphate esters for industrial lubricants is projected to reach over $3,500 million by 2033.

Challenges in the Phosphate Esters For Industrial Lubricants Sector

The phosphate esters for industrial lubricants sector faces several challenges. Regulatory hurdles, particularly concerning the environmental impact and potential health concerns associated with certain phosphate ester formulations, can lead to restrictions or the need for costly reformulation. Supply chain issues, including the availability and price volatility of raw materials, can impact production costs and product availability. Competitive pressures from alternative lubricant technologies, such as synthetic esters and polyalphaolefins (PAOs), which are gaining traction due to their performance and environmental profiles, present a constant challenge. The estimated impact of these challenges could slow market growth by up to 1.5% annually if not adequately addressed.

Emerging Opportunities in Phosphate Esters For Industrial Lubricants

Emerging opportunities in the phosphate esters for industrial lubricants market lie in the development of highly biodegradable and environmentally friendly formulations that meet stringent eco-labeling requirements. The increasing adoption of electric vehicles (EVs) presents a unique opportunity, as specialized lubricants are required for EV components, and phosphate esters may find applications here. Growth in renewable energy sectors, such as wind turbines, requires lubricants with exceptional durability and fire resistance, creating demand for advanced phosphate ester additives. Furthermore, the expansion of specialized industrial applications, like advanced robotics and high-precision manufacturing, opens avenues for customized lubricant solutions incorporating tailored phosphate ester chemistries. The market is expected to see opportunities in developing novel chemistries for extreme temperature applications, valued in the millions of dollars.

Leading Players in the Phosphate Esters For Industrial Lubricants Market

- LANXESS

- Chemtura

- Dow

- ExxonMobil

- BASF

- Colonial Chem

- Akzo Nobel

- Elementis Specialties

- Solvay

- Ashland

- IsleChem

- Custom Synthesis

- Croda

- Stepan

- Eastman

- Clariant

- Castrol Limited

- Kao

- Ajinomoto

- Fortune

- Zhenxing

- Ankang

- Xinhang

- Valtris

- Siltech

- Sialco Materials

Key Developments in Phosphate Esters For Industrial Lubricants Industry

- 2023 October: LANXESS launches a new line of fire-resistant hydraulic fluids incorporating advanced phosphate ester technology, enhancing safety in mining operations.

- 2023 May: Dow introduces novel phosphate ester additives offering improved thermal stability for high-temperature industrial lubricant applications.

- 2022 November: BASF expands its portfolio of environmentally acceptable lubricants (EALs) with new phosphate ester formulations designed for marine applications.

- 2022 July: Chemtura (now part of Lanxess) announces significant investment in R&D for biodegradable phosphate esters to meet growing sustainability demands.

- 2021 September: ExxonMobil develops a new generation of extreme pressure additives for industrial gear oils, leveraging phosphate ester chemistry for enhanced wear protection.

- 2021 March: Solvay introduces a range of high-performance phosphate esters for aerospace applications, meeting stringent industry certifications.

Strategic Outlook for Phosphate Esters For Industrial Lubricants Market

The strategic outlook for the phosphate esters for industrial lubricants market is positive, driven by sustained demand from key industrial sectors and ongoing innovation. Future growth catalysts include the increasing emphasis on operational efficiency, extended equipment life, and enhanced safety standards across manufacturing, power generation, and transportation. The push for sustainability will continue to drive the development of eco-friendly and biodegradable phosphate ester formulations. Opportunities for market expansion lie in emerging economies and in specialized applications requiring high-performance lubricant additives. Strategic collaborations and mergers will likely continue to shape the competitive landscape, with companies focusing on strengthening their product portfolios and expanding their global reach, aiming for market growth in the billions of dollars.

Phosphate Esters For Industrial Lubricants Segmentation

-

1. Application

- 1.1. Hydraulic Oils

- 1.2. Rolling Oils

- 1.3. Others

-

2. Type

- 2.1. Monophosphate

- 2.2. Diphosphate

- 2.3. Triphosphate

Phosphate Esters For Industrial Lubricants Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Phosphate Esters For Industrial Lubricants Regional Market Share

Geographic Coverage of Phosphate Esters For Industrial Lubricants

Phosphate Esters For Industrial Lubricants REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Phosphate Esters For Industrial Lubricants Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hydraulic Oils

- 5.1.2. Rolling Oils

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Monophosphate

- 5.2.2. Diphosphate

- 5.2.3. Triphosphate

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Phosphate Esters For Industrial Lubricants Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hydraulic Oils

- 6.1.2. Rolling Oils

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Monophosphate

- 6.2.2. Diphosphate

- 6.2.3. Triphosphate

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Phosphate Esters For Industrial Lubricants Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hydraulic Oils

- 7.1.2. Rolling Oils

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Monophosphate

- 7.2.2. Diphosphate

- 7.2.3. Triphosphate

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Phosphate Esters For Industrial Lubricants Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hydraulic Oils

- 8.1.2. Rolling Oils

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Monophosphate

- 8.2.2. Diphosphate

- 8.2.3. Triphosphate

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Phosphate Esters For Industrial Lubricants Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hydraulic Oils

- 9.1.2. Rolling Oils

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Monophosphate

- 9.2.2. Diphosphate

- 9.2.3. Triphosphate

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Phosphate Esters For Industrial Lubricants Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hydraulic Oils

- 10.1.2. Rolling Oils

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Monophosphate

- 10.2.2. Diphosphate

- 10.2.3. Triphosphate

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Colonial Chem

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 LANXESS

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Chemtura

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Dow

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ExxonMobil

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Akzo Nobel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Elementis Specialties

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Solvay

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ashland

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 IsleChem

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 BASF

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Custom Synthesis

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Croda

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Stepan

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Eastman

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Clariant

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Castrol Limited

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Kao

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Ajinomoto

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Fortune

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Zhenxing

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Ankang

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Xinhang

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Valtris

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Siltech

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Sialco Materials

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.1 Colonial Chem

List of Figures

- Figure 1: Global Phosphate Esters For Industrial Lubricants Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Phosphate Esters For Industrial Lubricants Revenue (million), by Application 2025 & 2033

- Figure 3: North America Phosphate Esters For Industrial Lubricants Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Phosphate Esters For Industrial Lubricants Revenue (million), by Type 2025 & 2033

- Figure 5: North America Phosphate Esters For Industrial Lubricants Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Phosphate Esters For Industrial Lubricants Revenue (million), by Country 2025 & 2033

- Figure 7: North America Phosphate Esters For Industrial Lubricants Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Phosphate Esters For Industrial Lubricants Revenue (million), by Application 2025 & 2033

- Figure 9: South America Phosphate Esters For Industrial Lubricants Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Phosphate Esters For Industrial Lubricants Revenue (million), by Type 2025 & 2033

- Figure 11: South America Phosphate Esters For Industrial Lubricants Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Phosphate Esters For Industrial Lubricants Revenue (million), by Country 2025 & 2033

- Figure 13: South America Phosphate Esters For Industrial Lubricants Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Phosphate Esters For Industrial Lubricants Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Phosphate Esters For Industrial Lubricants Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Phosphate Esters For Industrial Lubricants Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Phosphate Esters For Industrial Lubricants Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Phosphate Esters For Industrial Lubricants Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Phosphate Esters For Industrial Lubricants Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Phosphate Esters For Industrial Lubricants Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Phosphate Esters For Industrial Lubricants Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Phosphate Esters For Industrial Lubricants Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Phosphate Esters For Industrial Lubricants Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Phosphate Esters For Industrial Lubricants Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Phosphate Esters For Industrial Lubricants Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Phosphate Esters For Industrial Lubricants Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Phosphate Esters For Industrial Lubricants Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Phosphate Esters For Industrial Lubricants?

The projected CAGR is approximately 3.1%.

2. Which companies are prominent players in the Phosphate Esters For Industrial Lubricants?

Key companies in the market include Colonial Chem, LANXESS, Chemtura, Dow, ExxonMobil, Akzo Nobel, Elementis Specialties, Solvay, Ashland, IsleChem, BASF, Custom Synthesis, Croda, Stepan, Eastman, Clariant, Castrol Limited, Kao, Ajinomoto, Fortune, Zhenxing, Ankang, Xinhang, Valtris, Siltech, Sialco Materials.

3. What are the main segments of the Phosphate Esters For Industrial Lubricants?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 334 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Phosphate Esters For Industrial Lubricants," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Phosphate Esters For Industrial Lubricants report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Phosphate Esters For Industrial Lubricants?

To stay informed about further developments, trends, and reports in the Phosphate Esters For Industrial Lubricants, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence