Key Insights

The Polish Third-Party Logistics (3PL) market is poised for significant expansion, driven by the burgeoning e-commerce sector, robust manufacturing output, and the escalating demand for optimized supply chain operations. Projected to grow at a Compound Annual Growth Rate (CAGR) of 5.63%, the market is estimated at 35.71 billion in the base year 2025. Key growth catalysts include the rapid rise of e-commerce, which necessitates sophisticated warehousing and distribution networks, the increasing complexity of global supply chains, compelling businesses to outsource logistics functions, and a persistent focus on enhancing operational efficiency to reduce costs and accelerate delivery times. The industry is segmented by service offerings, encompassing domestic and international transportation management, and value-added warehousing and distribution. Key end-user industries include manufacturing, automotive, oil & gas, chemicals, distributive trade, pharmaceuticals & healthcare, and construction, with manufacturing and automotive anticipated to be the dominant segments, reflecting Poland's strong industrial foundation. While precise segment-level market sizing requires further in-depth analysis, the overall market trajectory indicates substantial growth across all categories. The competitive landscape features a blend of global logistics leaders and agile regional providers, signifying a dynamic market that rewards both established expertise and localized market understanding.

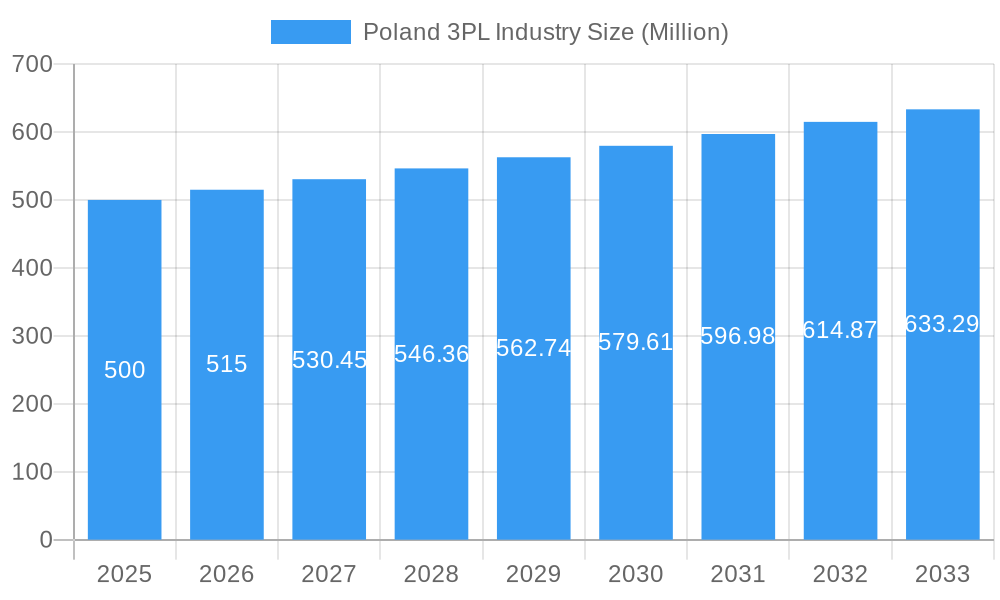

Poland 3PL Industry Market Size (In Billion)

Despite inherent challenges, the Polish 3PL market's growth trajectory remains strong. Potential constraints include developing infrastructure in certain regions, competitive pressures from lower-cost providers in adjacent markets, and the imperative for continuous technological adoption, such as automation and real-time visibility solutions. Nevertheless, government-led initiatives focused on infrastructure development and logistics sector enhancement are expected to alleviate some of these impediments. The forecast period, spanning from 2025 to 2033, indicates a sustained upward trend for the Polish 3PL industry, presenting considerable opportunities for businesses focused on advanced logistics solutions and integrated supply chain technologies. The ongoing expansion of e-commerce, particularly cross-border transactions, is anticipated to further amplify the demand for efficient and dependable 3PL services.

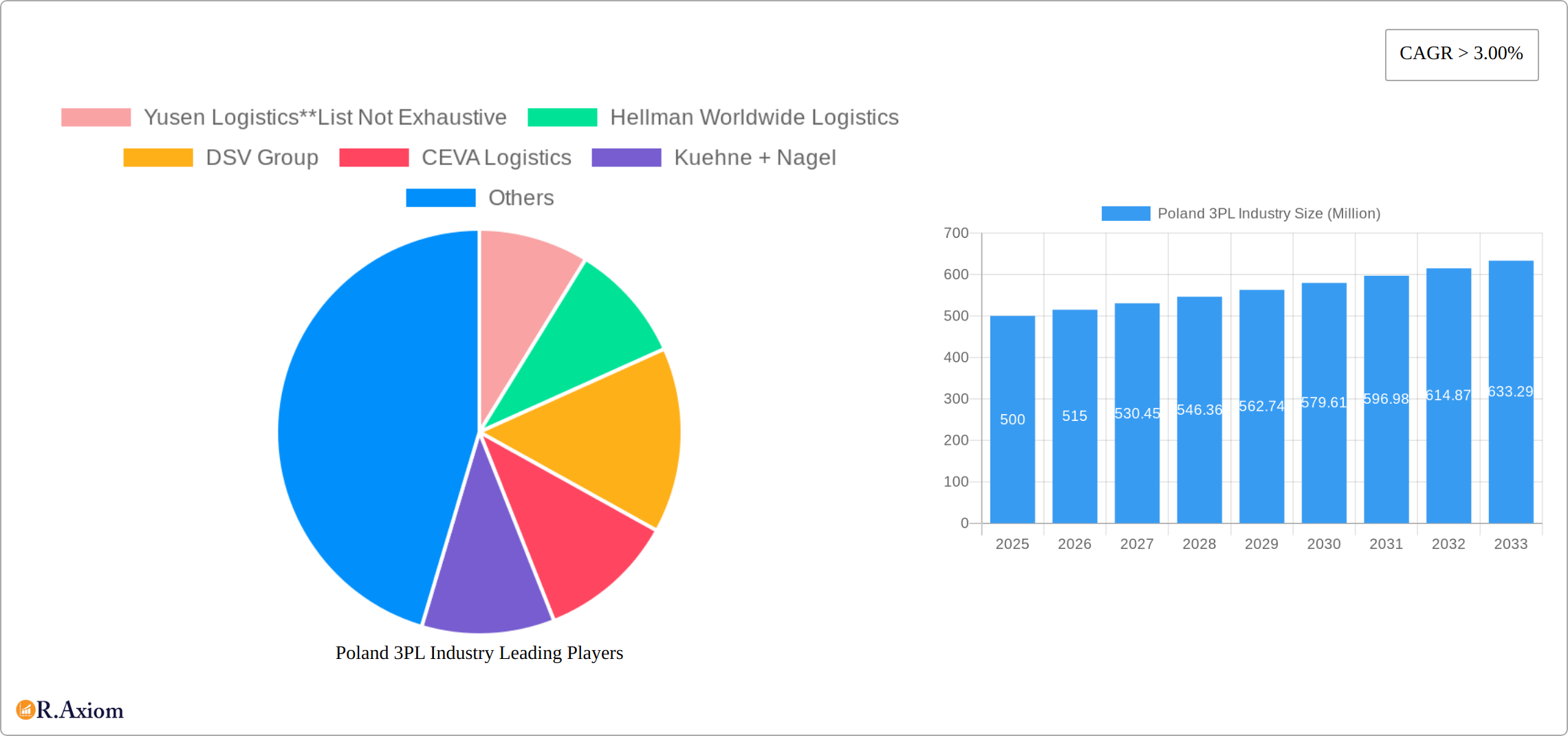

Poland 3PL Industry Company Market Share

Poland 3PL Industry: Market Analysis & Forecast Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Poland 3PL (Third-Party Logistics) industry, covering market size, growth drivers, key players, and future trends. The report utilizes data from the historical period (2019-2024), the base year (2025), and projects the market's trajectory through the forecast period (2025-2033). The study period covers 2019-2033, with an estimated year of 2025. The report is crucial for industry stakeholders, investors, and businesses seeking to understand and navigate the dynamic Polish 3PL landscape.

Poland 3PL Industry Market Concentration & Innovation

The Polish 3PL market presents a dynamic competitive landscape shaped by moderate concentration, robust innovation, and evolving regulatory frameworks. While several major international players like Yusen Logistics, Hellman Worldwide Logistics, DSV Group, and Kuehne + Nagel hold significant market share, a vibrant ecosystem of smaller, specialized 3PL providers caters to niche market demands. This section delves into the intricacies of market structure, innovation drivers, regulatory influences, competitive pressures, end-user trends, and the significant role of mergers and acquisitions (M&A).

- Market Share & Consolidation: The top 5 players currently hold an estimated xx% of the market share (2025 data), indicating a moderately concentrated market. However, the landscape is evolving, with smaller players actively seeking growth through specialization and strategic partnerships.

- M&A Activity: The Polish 3PL sector has experienced considerable M&A activity in recent years (2019-2024), driven by the pursuit of economies of scale, geographical expansion, service diversification, and access to advanced technologies. The total M&A deal value during this period reached approximately $xx Million, signifying significant investment and consolidation within the industry.

- Innovation Drivers: Technological advancements are pivotal to the Polish 3PL market's evolution. Automation, artificial intelligence (AI), blockchain technology, and advanced data analytics are transforming warehouse operations, transportation management, and supply chain visibility. Simultaneously, increasingly stringent regulatory frameworks related to data security, environmental sustainability (e.g., carbon footprint reduction), and labor practices are influencing innovation and shaping the operational strategies of 3PL providers.

- End-User Trends & Sectoral Demand: The Polish 3PL market is propelled by strong growth in various end-user sectors. The booming e-commerce sector, coupled with the increasing demand for specialized logistics solutions (e.g., temperature-controlled transportation for pharmaceuticals, just-in-time delivery for manufacturing), fuels significant growth across Manufacturing & Automotive, Pharma & Healthcare, and Distributive Trade sectors. This heightened demand necessitates adaptable and innovative solutions from 3PL providers.

Poland 3PL Industry Industry Trends & Insights

The Polish 3PL market exhibits robust growth, projected at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This expansion is fueled by several interconnected factors: the exponential growth of e-commerce, the increasing outsourcing of logistics functions by businesses of all sizes (including SMEs seeking operational efficiency and cost reduction), and a widespread focus on supply chain optimization and resilience.

Market penetration of 3PL services is steadily increasing, particularly among SMEs seeking to streamline their operations and reduce costs. The adoption of advanced technologies, such as Warehouse Management Systems (WMS), Transportation Management Systems (TMS), and sophisticated analytics platforms, is significantly enhancing operational efficiency, facilitating data-driven decision-making, and improving overall supply chain visibility. Furthermore, consumer expectations for faster and more reliable delivery services are driving 3PL providers to invest in advanced technologies and optimize their logistics networks. This intense competitive landscape fosters innovation and a customer-centric approach, pushing the industry towards higher standards of service quality and efficiency.

Dominant Markets & Segments in Poland 3PL Industry

The Polish 3PL market displays a diverse range of segments, each exhibiting unique growth trajectories and competitive dynamics. The market can be effectively analyzed through two key perspectives: services offered and end-user industries served.

By Services:

- Value-added Warehousing and Distribution: This segment is experiencing particularly strong growth, driven by the increasing demand for specialized warehousing solutions. Temperature-controlled storage, value-added services (kitting, labeling, packaging), and customized inventory management are particularly in demand, especially within the Pharma & Healthcare and food & beverage sectors.

- International Transportation Management: The growth of cross-border trade and globalization fuels this segment's expansion, demanding efficient and reliable international freight forwarding and customs brokerage services.

- Domestic Transportation Management: This remains a substantial segment, benefiting from robust domestic trade and industrial activities. Optimizing last-mile delivery and efficient regional transportation networks are key aspects of this segment.

By End-User:

- Distributive Trade (Wholesale and Retail, including e-commerce): This remains the largest and fastest-growing end-user segment, reflecting the explosive growth of e-commerce in Poland and the rising demand for efficient order fulfillment and last-mile delivery solutions.

- Manufacturing & Automotive: This segment benefits from Poland's robust manufacturing sector and the presence of significant automotive manufacturing facilities. Just-in-time delivery and efficient supply chain management are crucial for this sector.

- Pharma & Healthcare: This sector's growth is driven by increasing healthcare spending and stringent regulatory requirements for temperature-sensitive pharmaceutical products. Specialized logistics solutions are critical for ensuring the safe and reliable transport and storage of these products.

Key Drivers: The dominance of these segments is facilitated by favorable economic policies, government infrastructure investments (improving transportation networks), and the increasing complexity of supply chains requiring specialized 3PL expertise.

Poland 3PL Industry Product Developments

The Polish 3PL market is witnessing rapid product innovation, driven by technological advancements. Providers are increasingly adopting automation technologies, such as automated guided vehicles (AGVs) and robotics, to enhance warehouse efficiency and reduce labor costs. The integration of advanced analytics and artificial intelligence (AI) is improving forecasting accuracy, optimizing routes, and enabling proactive risk management. These innovations are providing significant competitive advantages to 3PL providers, allowing them to offer superior service levels and cost-effective solutions to their clients.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Polish 3PL market, segmented by services (Domestic Transportation Management, International Transportation Management, Value-added Warehousing and Distribution) and end-users (Manufacturing & Automotive, Oil & Gas and Chemicals, Distributive Trade, Pharma & Healthcare, Construction, and Other End Users). Each segment's market size, growth projections, competitive dynamics, and key influencing factors (industry trends, technological adoption, regulatory changes) are thoroughly examined. The report highlights the varying growth rates and competitive intensity across segments, providing valuable insights for strategic decision-making.

Key Drivers of Poland 3PL Industry Growth

The Polish 3PL industry's growth is propelled by several factors. The rise of e-commerce significantly boosts demand for warehousing and delivery services. Government initiatives fostering infrastructure development and streamlining logistics processes create a supportive environment. Moreover, increasing manufacturing activity and foreign direct investment contribute to the demand for efficient 3PL solutions. Technological advancements further enhance efficiency and offer opportunities for service diversification.

Challenges in the Poland 3PL Industry Sector

The Polish 3PL sector faces several key challenges that require strategic adaptation and investment. The persistent shortage of drivers impacts transportation management capabilities and necessitates innovative solutions for workforce recruitment and retention. Fluctuations in fuel prices and geopolitical instability introduce uncertainty and increase operational costs, requiring effective risk management strategies. The intensely competitive market demands continuous innovation, operational efficiency, and cost optimization to maintain profitability. Finally, adapting to evolving regulatory requirements, particularly concerning sustainability and environmental protection, adds complexity and necessitates proactive compliance measures. Addressing these challenges requires a multifaceted approach that includes technological advancements, strategic partnerships, and a focus on workforce development.

Emerging Opportunities in Poland 3PL Industry

Emerging opportunities include growth in specialized logistics such as cold chain solutions and reverse logistics. Investment in technology like AI and automation creates efficiencies and cost savings. Expansion into new market segments like renewable energy logistics holds promise. The focus on sustainable practices and green logistics presents opportunities for differentiation and attracting environmentally conscious clients.

Leading Players in the Poland 3PL Industry Market

- Yusen Logistics

- Hellman Worldwide Logistics

- DSV Group

- CEVA Logistics

- Kuehne + Nagel

- Kerry Logistics

- Ekol - Logistics 4.0

- Erontrans Logistics Services

- Raben

- Geis Global Logistics

- Geodis

- Dartom

- DHL Supply Chain

- Feige Logistics

- ID Logistics

Key Developments in Poland 3PL Industry Industry

- 2022 Q4: X company launched a new automated warehouse facility in Warsaw.

- 2023 Q1: Y company acquired Z company, expanding its cold chain logistics capabilities.

- 2023 Q3: New regulations regarding sustainable practices in logistics were implemented.

Strategic Outlook for Poland 3PL Industry Market

The Polish 3PL market exhibits strong growth potential, driven by e-commerce expansion, infrastructure development, and technological advancements. Companies focusing on innovation, sustainability, and specialization will gain a competitive edge. Strategic partnerships and acquisitions will play a crucial role in consolidating market share and expanding service offerings. The future landscape will be defined by companies adept at managing supply chain complexities and embracing digital transformation.

Poland 3PL Industry Segmentation

-

1. Services

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End-User

- 2.1. Manufacturing & Automotive

- 2.2. Oil & Gas and Chemicals

- 2.3. Distribu

- 2.4. Pharma & Healthcare

- 2.5. Construction

- 2.6. Other End Users

Poland 3PL Industry Segmentation By Geography

- 1. Poland

Poland 3PL Industry Regional Market Share

Geographic Coverage of Poland 3PL Industry

Poland 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Manufacturing & Automotive

- 5.2.2. Oil & Gas and Chemicals

- 5.2.3. Distribu

- 5.2.4. Pharma & Healthcare

- 5.2.5. Construction

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Poland 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Manufacturing & Automotive

- 6.2.2. Oil & Gas and Chemicals

- 6.2.3. Distribu

- 6.2.4. Pharma & Healthcare

- 6.2.5. Construction

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Yusen Logistics**List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hellman Worldwide Logistics

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DSV Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CEVA Logistics

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kuehne + Nagel

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Kerry Logistics

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ekol - Logistics 4 0

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Erontrans Logistics Services

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Raben

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Geis Global Logistics

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Geodis

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Dartom

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 DHL Supply Chain

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Feige Logistics

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 ID Logistics

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Yusen Logistics**List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Poland 3PL Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: Poland 3PL Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 2: Poland 3PL Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: Poland 3PL Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Poland 3PL Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 5: Poland 3PL Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 6: Poland 3PL Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland 3PL Industry?

The projected CAGR is approximately 5.63%.

2. Which companies are prominent players in the Poland 3PL Industry?

Key companies in the market include Yusen Logistics**List Not Exhaustive, Hellman Worldwide Logistics, DSV Group, CEVA Logistics, Kuehne + Nagel, Kerry Logistics, Ekol - Logistics 4 0, Erontrans Logistics Services, Raben, Geis Global Logistics, Geodis, Dartom, DHL Supply Chain, Feige Logistics, ID Logistics.

3. What are the main segments of the Poland 3PL Industry?

The market segments include Services, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.71 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Number of Partnerships among Automobile Manufacturers and Logistics Partners; Growth in international trade.

6. What are the notable trends driving market growth?

Boom in the Warehousing Sector.

7. Are there any restraints impacting market growth?

Nature of Supply Chain Business.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland 3PL Industry?

To stay informed about further developments, trends, and reports in the Poland 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence