Key Insights

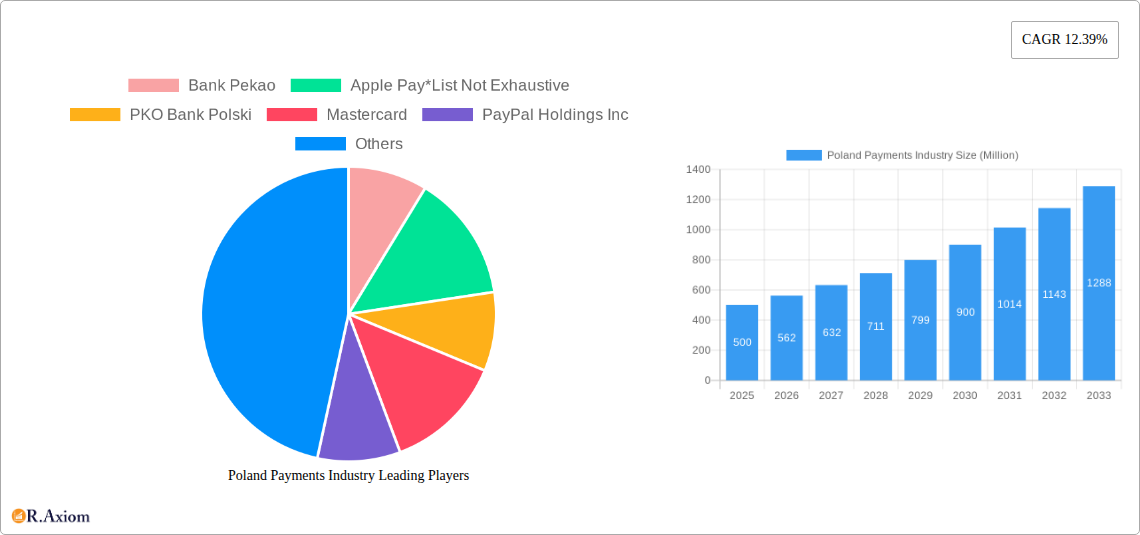

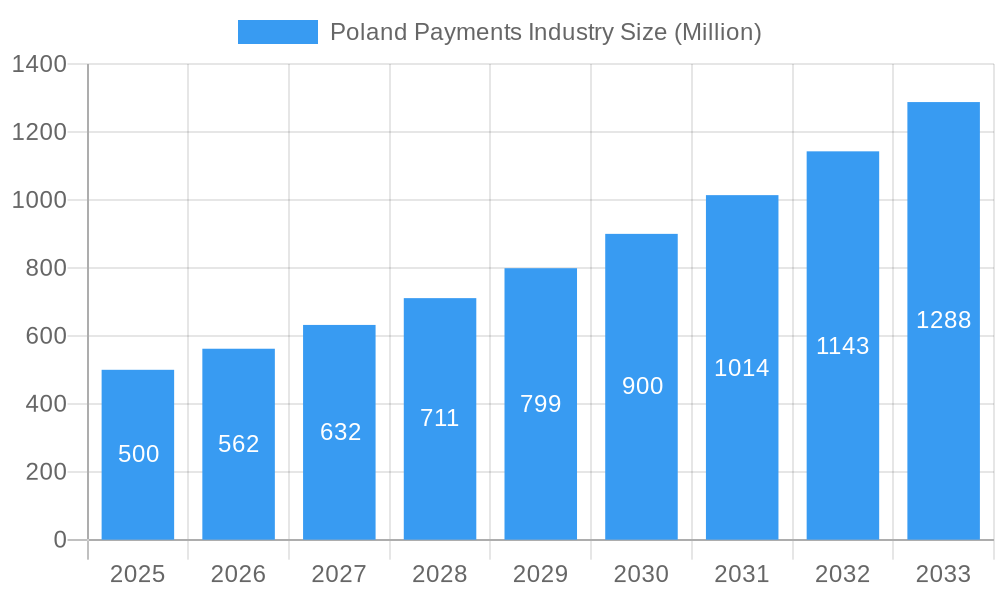

The Polish payments industry, currently experiencing robust growth, is projected to maintain a significant Compound Annual Growth Rate (CAGR) of 12.39% from 2025 to 2033. This expansion is driven by several key factors. The increasing adoption of digital technologies, particularly smartphones and internet penetration, fuels the shift towards online and mobile payment methods. Furthermore, a burgeoning e-commerce sector and the growing preference for contactless transactions are significantly boosting the market. Government initiatives promoting digital financial inclusion also contribute to this positive trajectory. The industry is segmented by payment mode (Point of Sale and Online Sale) and end-user industry (Retail, Entertainment, Healthcare, Hospitality, and Others). Key players such as Bank Pekao, PKO Bank Polski, Mastercard, PayPal, and PayU are driving innovation and competition within the market. While specific market size figures for 2025 are unavailable, extrapolating from the provided CAGR and considering the regional economic context, a reasonable estimate for the Polish payments market size in 2025 would fall within a range consistent with neighbouring European markets with comparable economic development. This suggests a significant market value in the hundreds of millions of USD. However, precise figures require access to more detailed financial data. The industry faces potential restraints such as cybersecurity concerns and the need for robust regulatory frameworks to ensure consumer protection and financial stability.

Poland Payments Industry Market Size (In Million)

The future growth of the Polish payments industry hinges on continued technological advancements, particularly in areas such as biometric authentication and Artificial Intelligence (AI)-driven fraud detection. Expansion into underserved segments, including rural populations, also presents significant opportunities. Furthermore, the increasing integration of payment systems with other financial services, such as lending and investment platforms, will further drive market expansion. The strategic partnerships between financial institutions and technology providers will play a crucial role in shaping the industry's landscape. Continued investment in secure and user-friendly payment solutions will be essential to maintain consumer trust and drive the adoption of innovative payment technologies within Poland.

Poland Payments Industry Company Market Share

This comprehensive report provides a detailed analysis of the Poland payments industry, encompassing market size, segmentation, competitive landscape, and future growth prospects. Covering the period from 2019 to 2033, with a focus on 2025, this report is an invaluable resource for industry stakeholders, investors, and strategists. The study incorporates in-depth analysis of key players, including Bank Pekao, PKO Bank Polski, Mastercard, PayPal Holdings Inc, PayU, Santander Bank Polska, DotPay, American Express, and Tap2Pay me, along with emerging trends such as Apple Pay and Buy Now, Pay Later (BNPL) services.

Poland Payments Industry Market Concentration & Innovation

This section analyzes the market concentration, innovation drivers, regulatory landscape, and competitive dynamics within the Polish payments industry. The report delves into the market share of key players like Bank Pekao and PKO Bank Polski, assessing their dominance and influence. Furthermore, it examines the role of innovation, including the adoption of contactless payments and mobile wallets like Apple Pay, and the impact of regulatory frameworks on market evolution. The analysis also considers the impact of mergers and acquisitions (M&A) activities, including the deal values and their influence on market structure. For example, the report will quantify the market share of the top 5 players in 2024 as xx% and projects the market concentration ratio (CR5) to reach xx% by 2033. The analysis also covers the impact of fintech innovation and its effect on traditional banking institutions, as well as an overview of emerging technologies such as blockchain and their potential disruptive influence. The total value of M&A deals in the Polish payments industry between 2019 and 2024 is estimated at xx Million.

- Market share analysis of key players

- Assessment of innovation drivers (e.g., contactless payments, mobile wallets)

- Analysis of regulatory frameworks and their impact

- Examination of M&A activities and their implications

Poland Payments Industry Industry Trends & Insights

This section provides a comprehensive overview of the Poland payments industry trends and insights, including market size projections, Compound Annual Growth Rate (CAGR), and market penetration rates for various payment methods. It examines growth drivers such as increasing digitalization, rising smartphone penetration, and the growing adoption of e-commerce. The analysis also considers the impact of technological disruptions like the rise of fintech companies and the increasing popularity of mobile payment solutions. The report further explores consumer preferences and evolving payment behaviors, influencing the competitive dynamics within the industry. The report projects a CAGR of xx% for the Poland payments industry during the forecast period (2025-2033). Market penetration of online payments is estimated at xx% in 2025, projected to reach xx% by 2033.

Dominant Markets & Segments in Poland Payments Industry

This section identifies the leading segments within the Polish payments market, considering both mode of payment (Point of Sale vs. Online Sale) and end-user industry (Retail, Entertainment, Healthcare, Hospitality, and Others). A detailed analysis will showcase the dominant segment and underlying drivers of its success.

By Mode of Payment: The report will analyze the market size and growth trajectory for both Point of Sale (POS) and Online Sale payments, identifying the dominant mode and factors contributing to its leadership. For example, factors driving the dominance of online payments might include the increasing adoption of e-commerce and the convenience offered by digital payment solutions.

By End-user Industry: The report will determine the leading end-user industry for payment transactions. This might be Retail, driven by high transaction volumes, or another sector with unique growth drivers. For instance, the growth of the entertainment industry could be attributed to the popularity of online streaming services and digital ticketing platforms. Each segment will be analyzed, highlighting key drivers:

- Retail: Strong growth driven by e-commerce expansion and rising consumer spending.

- Entertainment: Fueled by the digitalization of media consumption and online ticketing.

- Healthcare: Growth driven by increasing adoption of digital health solutions and online bill payments.

- Hospitality: Expansion driven by online booking platforms and contactless payment options in hotels and restaurants.

- Other End-user Industries: Analysis of growth opportunities and factors influencing market dynamics in other sectors.

Poland Payments Industry Product Developments

This section summarizes the latest product innovations and technological advancements in the Polish payments industry. The focus will be on analyzing the impact of new technologies, like contactless payment systems, mobile wallets, and Buy Now, Pay Later (BNPL) solutions, on market competition and consumer behavior. The competitive advantages offered by various payment solutions will be highlighted, with a clear focus on market fit and consumer adoption rates.

Report Scope & Segmentation Analysis

This report covers the Poland payments industry from 2019 to 2033, with a base year of 2025. The market is segmented by mode of payment (Point of Sale and Online Sale) and end-user industry (Retail, Entertainment, Healthcare, Hospitality, and Others). Growth projections, market sizes, and competitive dynamics are analyzed for each segment. For example, the retail segment is projected to account for xx Million in 2025, growing to xx Million by 2033. The online sales segment is anticipated to exhibit faster growth compared to POS, driven by e-commerce expansion.

Key Drivers of Poland Payments Industry Growth

The Polish payments industry's growth is driven by several key factors, including the rising adoption of e-commerce, increasing smartphone penetration, and government initiatives promoting digitalization. The expansion of contactless payments and mobile wallets also contributes significantly. Furthermore, the introduction of new payment technologies such as BNPL services fuels market growth.

Challenges in the Poland Payments Industry Sector

The Polish payments industry faces challenges such as maintaining consumer trust in online transactions and ensuring cybersecurity. Regulatory hurdles and the need for robust infrastructure to support digital payments also pose obstacles. Competition from established players and emerging fintech companies also creates pressure on profitability and market share. The increasing cost of implementing and maintaining secure payment systems also presents a challenge.

Emerging Opportunities in Poland Payments Industry

The Polish payments industry presents various opportunities, including expanding into underserved markets, developing innovative payment solutions tailored to specific consumer needs, and leveraging technological advancements such as blockchain for enhanced security and efficiency. The adoption of open banking and the growth of BNPL are key opportunities, as is the expansion into rural areas with limited access to traditional banking services.

Leading Players in the Poland Payments Industry Market

- Bank Pekao

- Apple Pay

- PKO Bank Polski

- Mastercard

- PayPal Holdings Inc

- PayU

- Santander Bank Polska

- DotPay

- American Express

- Tap2Pay me

Key Developments in Poland Payments Industry Industry

- May 2022: Allegro launched a new card and smartphone contactless payment option for cash-on-delivery purchases via its "One Kurier" delivery service. This enhances customer convenience and drives adoption of digital payments.

- May 2022: PKO BP announced the completion of its BNPL (Buy Now, Pay Later) solution, set to be integrated into most online stores in Poland. This will significantly expand the reach of BNPL services and drive market competition.

Strategic Outlook for Poland Payments Industry Market

The Polish payments industry is poised for robust growth, driven by technological advancements, increasing digital adoption, and supportive regulatory policies. The continued expansion of e-commerce, rising smartphone penetration, and the emergence of innovative payment solutions will create significant opportunities for industry players. The focus on enhancing security, improving customer experience, and expanding financial inclusion will further shape the market's future trajectory.

Poland Payments Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Poland Payments Industry Segmentation By Geography

- 1. Poland

Poland Payments Industry Regional Market Share

Geographic Coverage of Poland Payments Industry

Poland Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Poland Payments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6.1.1. Point of Sale

- 6.1.1.1. Card Pay

- 6.1.1.2. Digital Wallet (includes Mobile Wallets)

- 6.1.1.3. Cash

- 6.1.1.4. Others

- 6.1.2. Online Sale

- 6.1.2.1. Others (

- 6.1.1. Point of Sale

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Entertainment

- 6.2.3. Healthcare

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bank Pekao

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Apple Pay*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 PKO Bank Polski

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mastercard

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 PayPal Holdings Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PayU

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Santander Bank Polska

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 DotPay

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 American Express

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tap2Pay me

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Bank Pekao

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Poland Payments Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Poland Payments Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 2: Poland Payments Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Poland Payments Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Poland Payments Industry Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 5: Poland Payments Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Poland Payments Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Payments Industry?

The projected CAGR is approximately 12.5%.

2. Which companies are prominent players in the Poland Payments Industry?

Key companies in the market include Bank Pekao, Apple Pay*List Not Exhaustive, PKO Bank Polski, Mastercard, PayPal Holdings Inc, PayU, Santander Bank Polska, DotPay, American Express, Tap2Pay me.

3. What are the main segments of the Poland Payments Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 210.15 billion as of 2022.

5. What are some drivers contributing to market growth?

Advancements in the Polish Payments Market; Initiatives by the Government to improve cashless payment methods.

6. What are the notable trends driving market growth?

Advancements in the Polish Payments Market.

7. Are there any restraints impacting market growth?

Lack of a standard legislative policy remains especially in the case of cross-border transactions.

8. Can you provide examples of recent developments in the market?

May 2022 - Allegro announced a new service implemented in one of the platform's delivery methods - One Kurier. Customers using this method and paying for cash-on-delivery purchases can pay by card or smartphone using the contactless method on the courier's device used to manage shipments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Payments Industry?

To stay informed about further developments, trends, and reports in the Poland Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence