Key Insights

The global polyps market is poised for significant expansion, driven by increasing polyp prevalence, advancements in diagnostic technologies, and a focus on early detection. With a projected market size of 71.6 million and a Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period (2024-2033), the market offers substantial opportunities. Key growth factors include the rising incidence of nasal polyps, inflammatory bowel diseases, and precancerous colorectal polyps. Innovative treatments, including novel drug formulations and minimally invasive surgical techniques, are enhancing patient outcomes and market growth. The market is segmented by drug class, with corticosteroids and antibiotics playing vital roles in managing inflammation and infections. Oral and nasal administration routes are prevalent due to ease of use, while hospital and retail pharmacies serve as primary distribution channels.

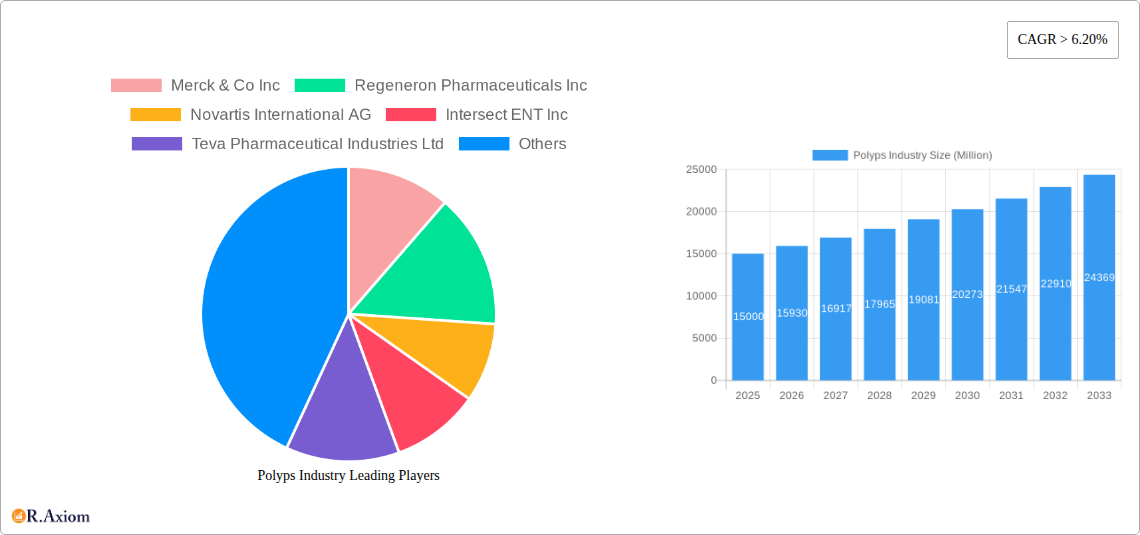

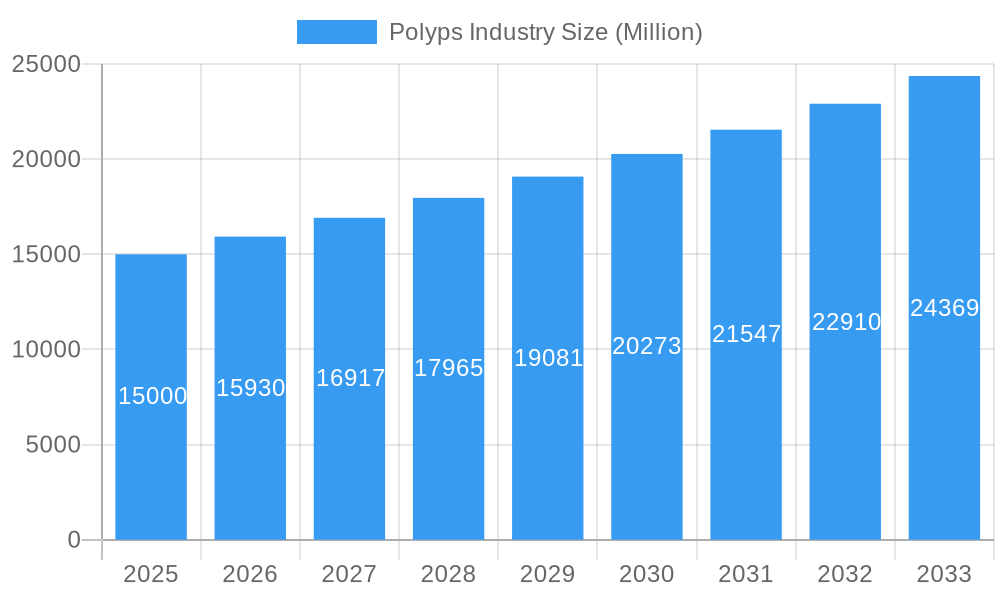

Polyps Industry Market Size (In Million)

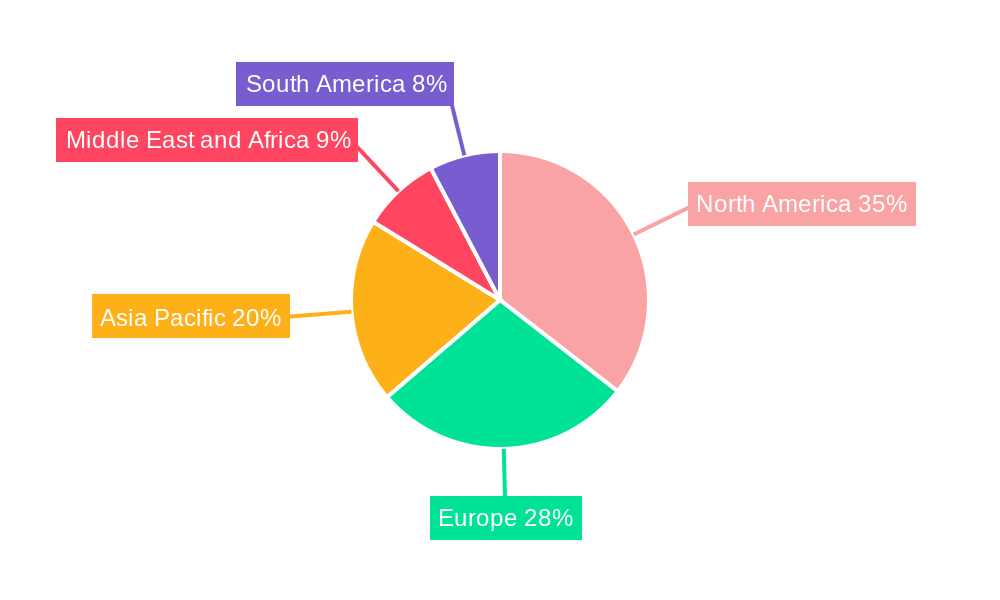

The competitive landscape features leading global pharmaceutical and medical device companies actively engaged in R&D for new and improved polyp therapies. Focus areas include targeted treatments with enhanced efficacy and reduced side effects to address unmet medical needs. Emerging trends such as biologics for inflammatory polyp conditions and AI integration in polyp detection and characterization are expected to reshape the market. However, challenges like high treatment costs, limited healthcare access in some regions, and potential side effects of long-term therapies may present moderate restraints. North America and Europe are anticipated to lead, supported by advanced healthcare infrastructure and higher disposable incomes. The Asia Pacific region is projected for the fastest growth, fueled by increasing healthcare expenditure, rising awareness, and a growing patient pool.

Polyps Industry Company Market Share

This comprehensive report analyzes the global polyps industry, providing critical insights into market dynamics, growth trajectories, and competitive landscapes. Covering the forecast period of 2024-2033, with a base year of 2024, this report utilizes historical data to deliver robust projections and strategic recommendations.

Polyps Industry Market Concentration & Innovation

The Polyps Industry exhibits a dynamic market concentration influenced by significant innovation drivers and evolving regulatory frameworks. Key players like Merck & Co Inc, Regeneron Pharmaceuticals Inc, Novartis International AG, Intersect ENT Inc, Teva Pharmaceutical Industries Ltd, F Hoffmann-La Roche AG, Pfizer Inc, OptiNose US, Norton Waterford Ltd, GlaxoSmithKline PLC, and Sanofi S A are actively shaping the market through strategic investments in research and development. Innovation in drug delivery systems and novel therapeutic compounds is a primary catalyst, addressing unmet patient needs and improving treatment efficacy for polyp-related conditions. The market is also characterized by a moderate level of concentration, with leading companies holding substantial market shares, estimated in the billions of dollars. Mergers and acquisitions (M&A) activities are a significant indicator of this concentration, with deal values reaching hundreds of millions to billions of dollars annually, aimed at consolidating portfolios and expanding market reach. The presence of viable product substitutes, while present, generally offers less targeted or effective solutions compared to specialized polyp treatments. End-user trends are shifting towards minimally invasive procedures and personalized treatment plans, further fueling innovation and R&D investments.

Polyps Industry Industry Trends & Insights

The Polyps Industry is poised for substantial growth, driven by a confluence of factors including an increasing prevalence of polyp-related conditions, advancements in diagnostic tools, and a growing demand for effective treatment solutions. The Compound Annual Growth Rate (CAGR) for the Polyps Industry is projected to be robust, estimated to be between 5.5% and 7.0% during the forecast period. Market penetration is expected to deepen as awareness of polyp-related diseases and their management improves among both healthcare professionals and patients. Technological disruptions, particularly in the realm of nanotechnology for drug delivery and advanced imaging techniques for early detection, are creating new avenues for therapeutic intervention and market expansion. Consumer preferences are leaning towards less invasive treatment options and therapies that offer improved quality of life, with a significant emphasis on patient convenience and reduced side effects.

The competitive dynamics within the Polyps Industry are characterized by intense R&D efforts to develop novel therapeutics and delivery mechanisms. Companies are heavily investing in understanding the underlying mechanisms of polyp formation and progression to identify new therapeutic targets. The rise of biologics and targeted therapies is a significant trend, moving away from broad-spectrum treatments towards more personalized approaches. Furthermore, the increasing burden of chronic respiratory diseases, such as chronic rhinosinusitis with nasal polyps (CRSwNP), is a major growth driver, pushing the demand for effective and long-term solutions. The expanding healthcare infrastructure in emerging economies, coupled with rising disposable incomes, is also contributing to market growth by increasing access to advanced treatments. Strategic collaborations between pharmaceutical giants and specialized biotech firms are becoming more common, fostering innovation and accelerating the development of pipeline drugs. The report will delve into these trends, providing quantitative data on market size and segmentation, and offering forward-looking insights into the evolving industry landscape.

Dominant Markets & Segments in Polyps Industry

The Polyps Industry exhibits distinct dominance across various geographic regions and market segments, driven by a combination of epidemiological factors, healthcare expenditure, and regulatory environments.

Regional Dominance: North America, particularly the United States, currently holds a dominant position in the Polyps Industry. This leadership is attributed to a high prevalence of respiratory conditions, advanced healthcare infrastructure, significant R&D investments by leading pharmaceutical companies like Merck & Co Inc, Pfizer Inc, and Regeneron Pharmaceuticals Inc, and favorable reimbursement policies for advanced polyp treatments. Economic policies in this region actively support innovation and market access for novel therapies.

Europe also represents a significant market, driven by a well-established healthcare system, increasing awareness of polyp-related diseases, and the presence of major players like Novartis International AG, F Hoffmann-La Roche AG, and GlaxoSmithKline PLC. Government initiatives promoting public health and access to medicines further bolster the European market.

The Asia-Pacific region is emerging as a high-growth market, fueled by a rapidly expanding population, increasing disposable incomes, and a growing burden of respiratory diseases. Investments in healthcare infrastructure and a rising demand for advanced medical treatments are key drivers of this growth.

Segment Dominance:

Drug Class:

- Corticosteroids currently dominate the Polyps Industry, owing to their proven efficacy in reducing inflammation and polyp size. They are widely prescribed across various polyp types and are a cornerstone of current treatment regimens.

- Antibiotics play a crucial role in managing secondary infections associated with polyps, contributing significantly to the market.

- Leukotriene Inhibitors are gaining traction for their role in managing allergic inflammation, often a contributing factor to polyp formation.

- Others encompass emerging therapies, biologics, and novel drug classes, which are expected to witness significant growth in the coming years.

Route of Administration:

- Nasal administration remains the dominant route for polyp treatments, offering direct delivery of medication to the affected areas. This includes nasal sprays and drops, leveraging advanced devices like those from OptiNose US.

- Oral administration is also significant, particularly for systemic treatments and managing underlying inflammatory conditions.

- Others include inhaled corticosteroids and other localized delivery methods, which are gaining prominence with technological advancements.

Distribution Channel:

- Hospital Pharmacies represent a substantial distribution channel, especially for injectable biologics and specialized treatments administered under medical supervision.

- Retail Pharmacies are critical for over-the-counter and prescription nasal sprays and oral medications, serving a broader patient population.

- Online Pharmacies are an emerging and rapidly growing channel, offering convenience and accessibility for a range of polyp treatment products, reflecting evolving consumer preferences.

Polyps Industry Product Developments

Product developments in the Polyps Industry are characterized by a strong focus on enhancing therapeutic efficacy, improving patient compliance, and minimizing side effects. Innovations in drug delivery systems, such as advanced nasal spray devices and sustained-release formulations, are gaining prominence, offering more targeted and convenient treatment options. The development of novel biologic therapies targeting specific inflammatory pathways is also a significant trend, providing more personalized and effective treatments for severe cases. These advancements are driven by a deeper understanding of polyp pathophysiology and a growing demand for treatments that offer long-term relief and improved quality of life. Competitive advantages are being established through superior pharmacokinetic profiles, reduced dosing frequency, and enhanced patient adherence facilitated by user-friendly devices.

Report Scope & Segmentation Analysis

This comprehensive report segment analyzes the global Polyps Industry across multiple dimensions, including drug class, route of administration, and distribution channels.

Drug Class Segmentation: The market is segmented into Corticosteroids, Antibiotics, Leukotriene Inhibitors, and Others. Corticosteroids currently lead the market, with substantial projected growth in the "Others" category driven by advancements in biologics and targeted therapies.

Route of Administration Segmentation: Key segments include Oral, Nasal, and Others. Nasal administration remains dominant due to its direct efficacy, while Oral administration addresses systemic inflammation. The "Others" segment is expected to see significant expansion with the introduction of novel delivery systems.

Distribution Channel Segmentation: The analysis covers Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. Hospital pharmacies cater to specialized treatments, retail pharmacies serve the broader patient base, and online pharmacies are exhibiting rapid growth due to convenience and accessibility. Each segment's market size and growth projections are detailed, along with insights into competitive dynamics.

Key Drivers of Polyps Industry Growth

Several key factors are propelling the growth of the Polyps Industry. Technologically, advancements in drug delivery systems, including high-precision nasal sprays and targeted biologics, are enhancing treatment efficacy and patient convenience. Economically, the increasing global healthcare expenditure, coupled with rising disposable incomes in emerging economies, is expanding access to advanced polyp treatments. Regulatory support for novel therapies and expedited approval pathways for innovative drugs also plays a crucial role. Furthermore, the growing awareness among patients and healthcare providers about the impact of polyps on quality of life, particularly in conditions like Chronic Rhinosinusitis with Nasal Polyps (CRSwNP), is a significant market driver. Epidemiological trends, such as the rising prevalence of allergic rhinitis and asthma, which are often associated with nasal polyps, further contribute to market expansion.

Challenges in the Polyps Industry Sector

Despite robust growth, the Polyps Industry faces several challenges. Stringent regulatory hurdles and lengthy approval processes for new drug applications can delay market entry and increase development costs. The high cost of advanced biologic therapies and specialized delivery devices can create affordability issues for a segment of the patient population, impacting market penetration. Supply chain complexities and the potential for manufacturing disruptions for specialized pharmaceutical products also pose a risk. Furthermore, intense competition among established players and emerging biotechs necessitates continuous innovation and competitive pricing strategies. Overcoming these barriers requires strategic partnerships, streamlined regulatory engagement, and innovative pricing models to ensure broader patient access.

Emerging Opportunities in Polyps Industry

Emerging opportunities in the Polyps Industry are abundant, driven by unmet medical needs and technological advancements. The development of novel therapeutic targets for polyp prevention and regression presents a significant opportunity for pipeline drugs. The expanding use of personalized medicine, including genetic profiling to identify individuals at higher risk or those who will best respond to specific treatments, is a growing trend. Furthermore, the increasing focus on minimally invasive surgical techniques and adjunctive therapies offers scope for innovation in both devices and pharmaceuticals. The growing demand for biologics and immunotherapies for refractory polyp cases also represents a substantial market opportunity. As awareness of the link between polyps and other chronic inflammatory diseases grows, opportunities for combination therapies and integrated treatment approaches are likely to emerge.

Leading Players in the Polyps Industry Market

- Merck & Co Inc

- Regeneron Pharmaceuticals Inc

- Novartis International AG

- Intersect ENT Inc

- Teva Pharmaceutical Industries Ltd

- F Hoffmann-La Roche AG

- Pfizer Inc

- OptiNose US

- Norton Waterford Ltd

- GlaxoSmithKline PLC

- Sanofi S A

Key Developments in Polyps Industry Industry

- 2023: Launch of a new biologic therapy for severe Chronic Rhinosinusitis with Nasal Polyps (CRSwNP), showing significant reduction in polyp size and improved symptom scores.

- 2023: Merck & Co Inc acquired a biotechnology company specializing in nasal drug delivery systems, aiming to enhance its respiratory portfolio.

- 2022: Regeneron Pharmaceuticals Inc announced positive Phase III trial results for a novel monoclonal antibody targeting inflammatory pathways implicated in polyp formation.

- 2022: Novartis International AG expanded its pipeline with a new investigational drug for non-allergic nasal polyps.

- 2021: Intersect ENT Inc received FDA approval for an advanced steroid-releasing implant for post-surgical management of nasal polyps.

- 2020: Pfizer Inc announced strategic collaborations to explore new therapeutic avenues for polyp management, focusing on underlying genetic predispositions.

- 2019: GlaxoSmithKline PLC reported significant progress in developing a novel small molecule inhibitor for inflammatory conditions contributing to polyp growth.

Strategic Outlook for Polyps Industry Market

The strategic outlook for the Polyps Industry is highly positive, marked by continuous innovation and expanding market reach. The focus on developing highly targeted therapies, including biologics and personalized medicines, will continue to be a key growth catalyst. Advancements in drug delivery technologies, such as smart inhalers and advanced nasal delivery devices, will further enhance treatment efficacy and patient adherence, driving demand for these innovative solutions. Strategic partnerships and M&A activities are expected to accelerate, enabling companies to consolidate market share, expand their product portfolios, and access new technological capabilities. The growing prevalence of polyp-associated conditions and increasing healthcare investments, particularly in emerging markets, will provide sustained growth opportunities, making the Polyps Industry a dynamic and promising sector for the foreseeable future.

Polyps Industry Segmentation

-

1. Drug Class

- 1.1. Corticosteroids

- 1.2. Antibiotics

- 1.3. Leukotriene Inhibitors

- 1.4. Others

-

2. Route of Administration

- 2.1. Oral

- 2.2. Nasal

- 2.3. Others

-

3. Distribution Channel

- 3.1. Hospital Pharmacies

- 3.2. Retail Pharmacies

- 3.3. Online Pharmacies

Polyps Industry Segmentation By Geography

-

1. North America

- 1.1. United states

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Polyps Industry Regional Market Share

Geographic Coverage of Polyps Industry

Polyps Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Rising Prevalence of Various Immunological Disorders along with the Increasing Geriatric Population; Huge Product Pipeline of Nasal Polyps Treatment with Growing Research Activities

- 3.3. Market Restrains

- 3.3.1. ; High Cost and Complications Associated with Sinus Surgeries; Adverse Reactions Associated with Steroid Therapies

- 3.4. Market Trends

- 3.4.1. Corticosteroids Segment by Drug Class is Expected to Hold the Largest Market Share in the Nasal Polyps Treatment Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Polyps Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 5.1.1. Corticosteroids

- 5.1.2. Antibiotics

- 5.1.3. Leukotriene Inhibitors

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Route of Administration

- 5.2.1. Oral

- 5.2.2. Nasal

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Hospital Pharmacies

- 5.3.2. Retail Pharmacies

- 5.3.3. Online Pharmacies

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 6. North America Polyps Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 6.1.1. Corticosteroids

- 6.1.2. Antibiotics

- 6.1.3. Leukotriene Inhibitors

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Route of Administration

- 6.2.1. Oral

- 6.2.2. Nasal

- 6.2.3. Others

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Hospital Pharmacies

- 6.3.2. Retail Pharmacies

- 6.3.3. Online Pharmacies

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 7. Europe Polyps Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Drug Class

- 7.1.1. Corticosteroids

- 7.1.2. Antibiotics

- 7.1.3. Leukotriene Inhibitors

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Route of Administration

- 7.2.1. Oral

- 7.2.2. Nasal

- 7.2.3. Others

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Hospital Pharmacies

- 7.3.2. Retail Pharmacies

- 7.3.3. Online Pharmacies

- 7.1. Market Analysis, Insights and Forecast - by Drug Class

- 8. Asia Pacific Polyps Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Drug Class

- 8.1.1. Corticosteroids

- 8.1.2. Antibiotics

- 8.1.3. Leukotriene Inhibitors

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Route of Administration

- 8.2.1. Oral

- 8.2.2. Nasal

- 8.2.3. Others

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Hospital Pharmacies

- 8.3.2. Retail Pharmacies

- 8.3.3. Online Pharmacies

- 8.1. Market Analysis, Insights and Forecast - by Drug Class

- 9. Middle East and Africa Polyps Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Drug Class

- 9.1.1. Corticosteroids

- 9.1.2. Antibiotics

- 9.1.3. Leukotriene Inhibitors

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Route of Administration

- 9.2.1. Oral

- 9.2.2. Nasal

- 9.2.3. Others

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Hospital Pharmacies

- 9.3.2. Retail Pharmacies

- 9.3.3. Online Pharmacies

- 9.1. Market Analysis, Insights and Forecast - by Drug Class

- 10. South America Polyps Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Drug Class

- 10.1.1. Corticosteroids

- 10.1.2. Antibiotics

- 10.1.3. Leukotriene Inhibitors

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Route of Administration

- 10.2.1. Oral

- 10.2.2. Nasal

- 10.2.3. Others

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Hospital Pharmacies

- 10.3.2. Retail Pharmacies

- 10.3.3. Online Pharmacies

- 10.1. Market Analysis, Insights and Forecast - by Drug Class

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Merck & Co Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Regeneron Pharmaceuticals Inc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Novartis International AG

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Intersect ENT Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Teva Pharmaceutical Industries Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 F Hoffmann-La Roche AG

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Pfizer Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 OptiNose US

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Norton Waterford Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 GlaxoSmithKline PLC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sanofi S A

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Merck & Co Inc

List of Figures

- Figure 1: Global Polyps Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Polyps Industry Revenue (million), by Drug Class 2025 & 2033

- Figure 3: North America Polyps Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 4: North America Polyps Industry Revenue (million), by Route of Administration 2025 & 2033

- Figure 5: North America Polyps Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 6: North America Polyps Industry Revenue (million), by Distribution Channel 2025 & 2033

- Figure 7: North America Polyps Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 8: North America Polyps Industry Revenue (million), by Country 2025 & 2033

- Figure 9: North America Polyps Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Polyps Industry Revenue (million), by Drug Class 2025 & 2033

- Figure 11: Europe Polyps Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 12: Europe Polyps Industry Revenue (million), by Route of Administration 2025 & 2033

- Figure 13: Europe Polyps Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 14: Europe Polyps Industry Revenue (million), by Distribution Channel 2025 & 2033

- Figure 15: Europe Polyps Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 16: Europe Polyps Industry Revenue (million), by Country 2025 & 2033

- Figure 17: Europe Polyps Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Polyps Industry Revenue (million), by Drug Class 2025 & 2033

- Figure 19: Asia Pacific Polyps Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 20: Asia Pacific Polyps Industry Revenue (million), by Route of Administration 2025 & 2033

- Figure 21: Asia Pacific Polyps Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 22: Asia Pacific Polyps Industry Revenue (million), by Distribution Channel 2025 & 2033

- Figure 23: Asia Pacific Polyps Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: Asia Pacific Polyps Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Asia Pacific Polyps Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Polyps Industry Revenue (million), by Drug Class 2025 & 2033

- Figure 27: Middle East and Africa Polyps Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 28: Middle East and Africa Polyps Industry Revenue (million), by Route of Administration 2025 & 2033

- Figure 29: Middle East and Africa Polyps Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 30: Middle East and Africa Polyps Industry Revenue (million), by Distribution Channel 2025 & 2033

- Figure 31: Middle East and Africa Polyps Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 32: Middle East and Africa Polyps Industry Revenue (million), by Country 2025 & 2033

- Figure 33: Middle East and Africa Polyps Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Polyps Industry Revenue (million), by Drug Class 2025 & 2033

- Figure 35: South America Polyps Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 36: South America Polyps Industry Revenue (million), by Route of Administration 2025 & 2033

- Figure 37: South America Polyps Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 38: South America Polyps Industry Revenue (million), by Distribution Channel 2025 & 2033

- Figure 39: South America Polyps Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 40: South America Polyps Industry Revenue (million), by Country 2025 & 2033

- Figure 41: South America Polyps Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Polyps Industry Revenue million Forecast, by Drug Class 2020 & 2033

- Table 2: Global Polyps Industry Revenue million Forecast, by Route of Administration 2020 & 2033

- Table 3: Global Polyps Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Polyps Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Global Polyps Industry Revenue million Forecast, by Drug Class 2020 & 2033

- Table 6: Global Polyps Industry Revenue million Forecast, by Route of Administration 2020 & 2033

- Table 7: Global Polyps Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 8: Global Polyps Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: United states Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Canada Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Global Polyps Industry Revenue million Forecast, by Drug Class 2020 & 2033

- Table 13: Global Polyps Industry Revenue million Forecast, by Route of Administration 2020 & 2033

- Table 14: Global Polyps Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 15: Global Polyps Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: Germany Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: France Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Italy Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Spain Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Global Polyps Industry Revenue million Forecast, by Drug Class 2020 & 2033

- Table 23: Global Polyps Industry Revenue million Forecast, by Route of Administration 2020 & 2033

- Table 24: Global Polyps Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 25: Global Polyps Industry Revenue million Forecast, by Country 2020 & 2033

- Table 26: China Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Japan Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: India Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Australia Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: South Korea Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Global Polyps Industry Revenue million Forecast, by Drug Class 2020 & 2033

- Table 33: Global Polyps Industry Revenue million Forecast, by Route of Administration 2020 & 2033

- Table 34: Global Polyps Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global Polyps Industry Revenue million Forecast, by Country 2020 & 2033

- Table 36: GCC Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: South Africa Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Global Polyps Industry Revenue million Forecast, by Drug Class 2020 & 2033

- Table 40: Global Polyps Industry Revenue million Forecast, by Route of Administration 2020 & 2033

- Table 41: Global Polyps Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 42: Global Polyps Industry Revenue million Forecast, by Country 2020 & 2033

- Table 43: Brazil Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Argentina Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Polyps Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polyps Industry?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Polyps Industry?

Key companies in the market include Merck & Co Inc, Regeneron Pharmaceuticals Inc, Novartis International AG, Intersect ENT Inc, Teva Pharmaceutical Industries Ltd, F Hoffmann-La Roche AG, Pfizer Inc, OptiNose US, Norton Waterford Ltd, GlaxoSmithKline PLC, Sanofi S A.

3. What are the main segments of the Polyps Industry?

The market segments include Drug Class, Route of Administration, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 71.6 million as of 2022.

5. What are some drivers contributing to market growth?

; Rising Prevalence of Various Immunological Disorders along with the Increasing Geriatric Population; Huge Product Pipeline of Nasal Polyps Treatment with Growing Research Activities.

6. What are the notable trends driving market growth?

Corticosteroids Segment by Drug Class is Expected to Hold the Largest Market Share in the Nasal Polyps Treatment Market.

7. Are there any restraints impacting market growth?

; High Cost and Complications Associated with Sinus Surgeries; Adverse Reactions Associated with Steroid Therapies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Polyps Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Polyps Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Polyps Industry?

To stay informed about further developments, trends, and reports in the Polyps Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence