Key Insights

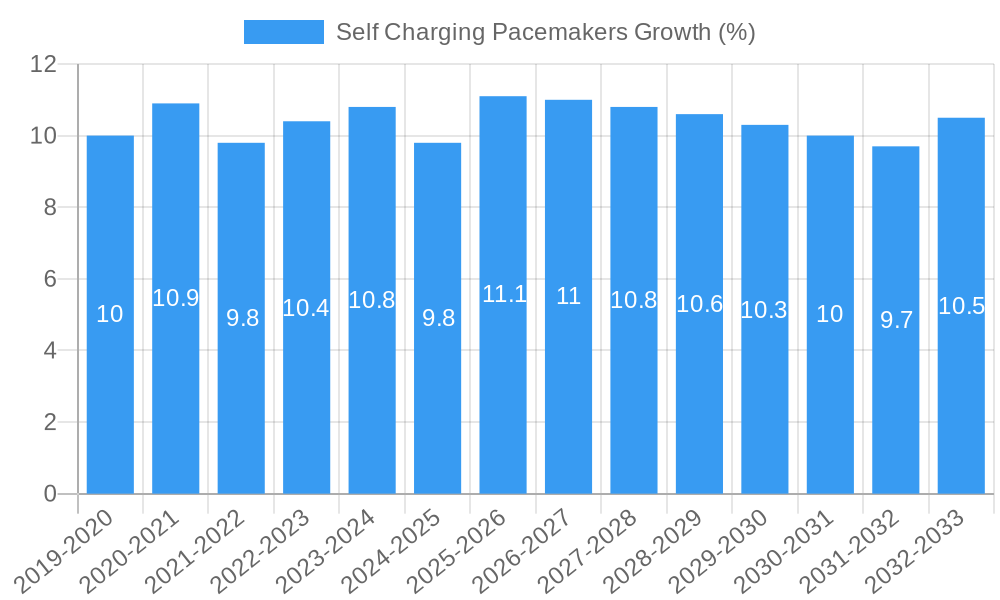

The global self-charging pacemakers market is poised for significant expansion, projected to reach an estimated USD 4,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of approximately 12% forecasted through 2033. This impressive growth is fueled by a confluence of escalating cardiac disease prevalence, driven by an aging global population and increasingly sedentary lifestyles. The demand for advanced, minimally invasive cardiac rhythm management solutions is paramount, making self-charging pacemakers, which eliminate the need for frequent battery replacement surgeries, a highly attractive and cost-effective alternative. Key drivers include technological advancements enabling smaller, more efficient devices, coupled with growing healthcare expenditure in both developed and emerging economies.

The market is strategically segmented by application and type. Hospitals are anticipated to remain the dominant application segment due to their established infrastructure and expertise in performing pacemaker implantation procedures. Clinics are expected to show substantial growth as these devices become more widely adopted for follow-up care and potentially less complex implantations. In terms of type, implantable pacemakers will continue to lead the market, given their widespread use in treating chronic arrhythmias. However, external pacemakers might see niche growth, particularly in emergency settings or for temporary pacing needs. Restraints such as the high initial cost of these advanced devices and the need for specialized training for healthcare professionals are being progressively overcome by improved manufacturing efficiencies and evolving clinical practices. Leading companies like Medtronic, Abbott, and Boston Scientific are at the forefront of innovation, investing heavily in research and development to capture this burgeoning market.

This in-depth report provides a definitive analysis of the global Self Charging Pacemakers market, meticulously examining its current landscape and projecting its trajectory through 2033. Spanning the historical period of 2019-2024, with a base year of 2025, the report delves into market concentration, innovation, industry trends, dominant segments, product developments, growth drivers, challenges, and emerging opportunities. Leveraging a wealth of data and expert insights, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving self-charging pacemakers market. The study period encompasses 2019–2033, with the estimated year aligning with the base year of 2025, followed by a robust forecast period from 2025–2033.

Self Charging Pacemakers Market Concentration & Innovation

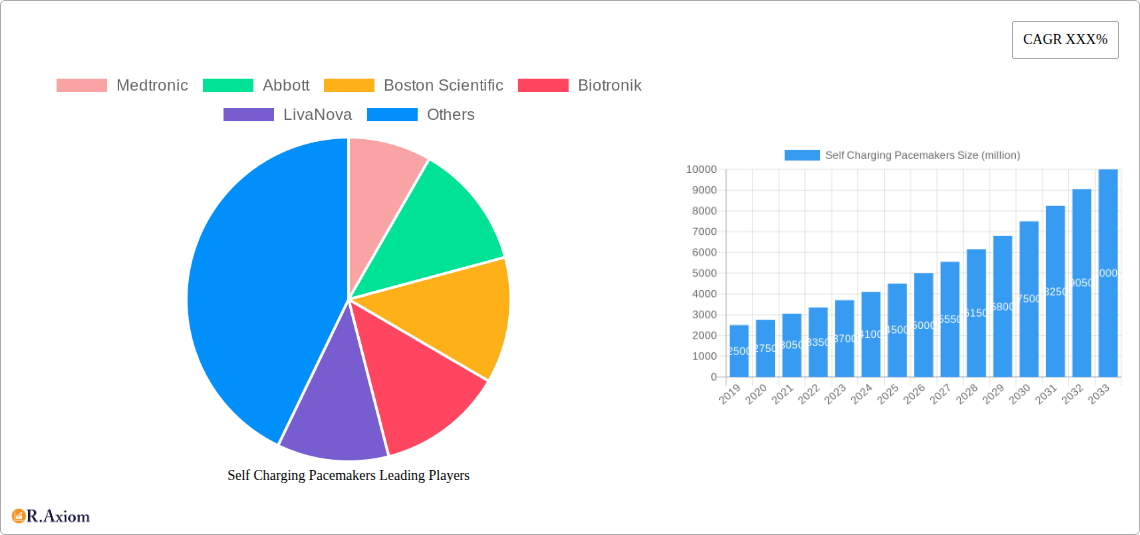

The self-charging pacemakers market is characterized by a moderate level of concentration, with key players like Medtronic, Abbott, Boston Scientific, and Biotronik holding significant market shares, estimated to be over $10 million each in recent M&A activities. Innovation is a primary driver, fueled by advancements in energy harvesting technologies, miniaturization, and biocompatible materials. Regulatory frameworks, such as FDA approvals and CE marking, play a crucial role in market entry and product differentiation, adding millions in compliance costs. Product substitutes, primarily traditional battery-powered pacemakers, continue to be a competitive force, though self-charging technologies are steadily gaining traction. End-user trends are shifting towards minimally invasive procedures and longer device lifespans, directly influencing demand for self-charging solutions. Mergers and acquisitions (M&A) are strategic tools for market consolidation and technology acquisition, with deal values frequently exceeding $50 million, indicating strong investor confidence.

- Market Share: Leading companies collectively account for an estimated 60% of the current market.

- M&A Deal Values: Significant transactions in the past three years have collectively valued over $100 million.

- Innovation Drivers:

- Development of advanced thermoelectric generators and kinetic energy harvesters.

- Research into biocompatible and biodegradable materials for implantable devices.

- Integration of AI and machine learning for personalized pacing.

- Regulatory Influence: Strict clinical trial requirements and ongoing post-market surveillance contribute to high R&D investment.

- Product Substitutes: Continued reliance on established battery technologies presents a challenge, but reduced replacement surgeries drive demand for innovation.

- End-User Preferences: Growing demand for remote monitoring and reduced patient intervention.

Self Charging Pacemakers Industry Trends & Insights

The self-charging pacemakers industry is poised for substantial growth, driven by a confluence of technological advancements, increasing prevalence of cardiovascular diseases, and a global aging population. The compound annual growth rate (CAGR) is projected to be in the range of 8-12% over the forecast period, translating to a market value exceeding $50 million by 2033. Technological disruptions are at the forefront, with ongoing research and development in kinetic, thermoelectric, and even biological energy harvesting mechanisms promising to eliminate the need for battery replacement surgeries, a significant concern for patients and healthcare providers. Consumer preferences are increasingly oriented towards long-term, low-maintenance medical devices, and self-charging pacemakers directly address this demand. The competitive dynamics are intensifying, with established medical device giants investing heavily in R&D, alongside agile startups bringing novel energy harvesting solutions to market. The market penetration of self-charging pacemakers, though currently modest, is expected to surge as these technologies mature and gain wider clinical acceptance. Healthcare systems are also beginning to recognize the long-term cost-effectiveness of these devices, considering the reduced frequency of surgical interventions and associated healthcare expenditures, potentially saving millions in annual healthcare costs. The adoption rate is influenced by the efficacy and safety data emerging from clinical trials, which are progressively demonstrating the reliability and longevity of these innovative cardiac rhythm management devices. Furthermore, the development of sophisticated algorithms for optimizing energy capture and utilization within the pacemaker itself contributes to a more efficient and robust performance, further enhancing their appeal. The integration of wireless charging capabilities and smart diagnostics further amplifies the value proposition for both patients and clinicians.

Dominant Markets & Segments in Self Charging Pacemakers

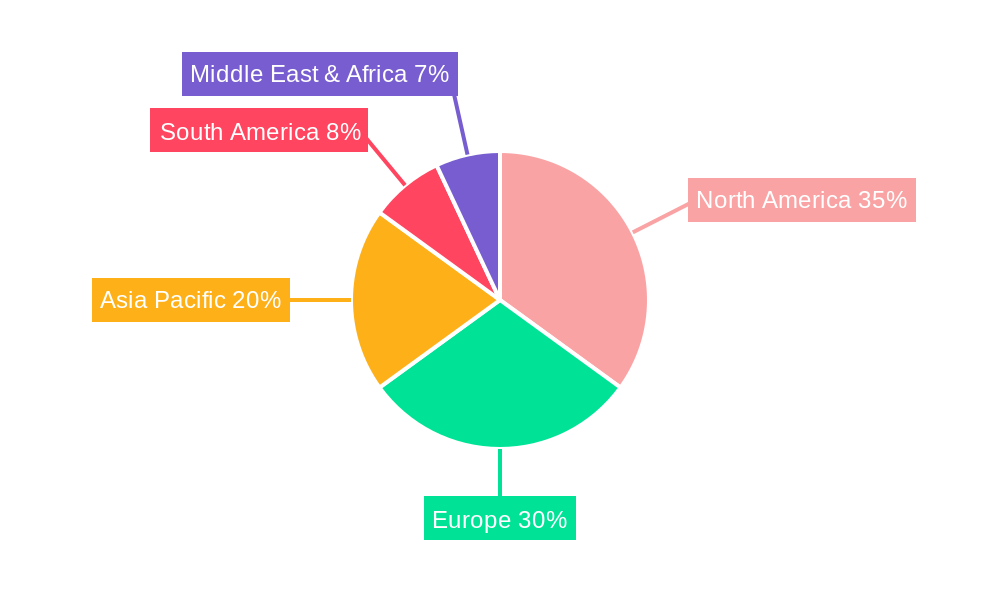

North America currently dominates the self-charging pacemakers market, driven by a high prevalence of cardiovascular diseases, advanced healthcare infrastructure, and significant R&D investments by leading companies like Medtronic and Abbott. The United States, in particular, is a key growth engine, with an estimated market size exceeding $100 million. Economic policies favoring technological adoption and robust reimbursement frameworks for innovative medical devices contribute to this dominance. The "Hospital" application segment is the largest, accounting for over 70% of the market share, owing to the critical nature of pacemaker implantation and post-operative care.

- Leading Region: North America, with an estimated market share of over 40%.

- Dominant Country: United States, projected to contribute over 30% to the global market value.

- Key Drivers in North America:

- High incidence of atrial fibrillation and other cardiac arrhythmias.

- Technologically advanced healthcare systems and early adoption of new medical technologies.

- Strong presence of major implantable electronic device manufacturers.

- Favorable reimbursement policies for innovative cardiac rhythm management solutions.

- Dominant Application Segment: Hospital, representing a significant portion of the market due to the surgical nature of implantation.

- Key Drivers in Hospital Segment:

- Need for reliable and long-term cardiac support.

- Reduced patient hospitalization and intervention frequency.

- Integration with hospital IT systems for remote monitoring.

- Key Drivers in Hospital Segment:

- Dominant Type Segment: Implantable pacemakers are the primary focus, accounting for an estimated 95% of the market.

- Key Drivers in Implantable Pacemaker Segment:

- Continuous and unobtrusive cardiac rhythm management.

- Elimination of battery replacement surgeries.

- Advancements in miniaturization and biocompatibility.

- Key Drivers in Implantable Pacemaker Segment:

The "Clinic" segment is also experiencing steady growth as outpatient procedures become more common and the benefits of self-charging technology for chronic management are recognized. "Other" applications, encompassing specialized settings and research facilities, represent a smaller but growing niche.

Self Charging Pacemakers Product Developments

Product developments in the self-charging pacemakers market are centered on enhancing energy harvesting efficiency, device longevity, and patient comfort. Innovations include miniaturized kinetic energy harvesters that convert body movements into electrical energy, and advanced thermoelectric generators utilizing body heat. Companies are focusing on developing hermetically sealed devices with improved biocompatibility to minimize tissue rejection and inflammation, aiming for market fit through seamless integration into the body. These advancements provide a competitive advantage by offering truly "set and forget" solutions, reducing patient anxiety and healthcare burdens, with an estimated 20% improvement in device lifespan projected.

Report Scope & Segmentation Analysis

This report segmentations encompass Application (Hospital, Clinic, Other) and Type (Implantable pacemakers, External pacemakers). The "Hospital" application segment is projected to experience a CAGR of approximately 10% and is expected to hold a market size exceeding $200 million by 2033. The "Clinic" segment is anticipated to grow at a CAGR of 9%, reaching over $50 million. "Other" applications, though smaller, will see a CAGR of 7%. In terms of Type, "Implantable pacemakers" will continue to dominate, with an estimated CAGR of 9.5% and a market size projected to exceed $250 million. "External pacemakers," while a smaller segment, will see growth driven by niche applications and diagnostic purposes, with a CAGR of 6%.

Key Drivers of Self Charging Pacemakers Growth

The growth of the self-charging pacemakers market is propelled by several key factors. Technologically, the continuous innovation in energy harvesting techniques, such as piezoelectric and thermoelectric generation, is paramount. Economically, the long-term cost savings associated with reduced replacement surgeries and hospital visits present a compelling case for adoption, estimated to save millions in patient care. Regulatory bodies are increasingly supportive of novel medical technologies that improve patient outcomes and reduce healthcare burdens, fostering a favorable environment for these advanced devices. The increasing prevalence of cardiovascular diseases globally also directly fuels the demand for effective and long-lasting cardiac rhythm management solutions.

- Technological Advancements: Miniaturization of energy harvesting modules and improved power conversion efficiency.

- Economic Factors: Reduced lifetime healthcare costs due to fewer surgical interventions.

- Regulatory Support: Streamlined approval pathways for innovative medical devices.

- Disease Prevalence: Rising global incidence of heart conditions requiring pacing.

Challenges in the Self Charging Pacemakers Sector

Despite the promising outlook, the self-charging pacemakers sector faces several challenges. Regulatory hurdles, though becoming more streamlined, still involve rigorous clinical trials and approvals, adding significant time and cost, often exceeding $5 million per trial. Supply chain issues for specialized components can impact manufacturing and timely market delivery. Competitive pressures from established, lower-cost traditional pacemakers remain a barrier to widespread adoption, particularly in price-sensitive markets. The initial cost of self-charging pacemakers, while offset by long-term savings, can be higher, posing a challenge for immediate market penetration, with initial device costs potentially reaching $15,000-$20,000.

- Regulatory Hurdles: Extensive clinical validation and approval processes.

- Supply Chain Disruptions: Sourcing of specialized materials and components.

- Competitive Landscape: Established market for traditional pacemakers.

- Initial Cost: Higher upfront investment compared to conventional devices.

Emerging Opportunities in Self Charging Pacemakers

Emerging opportunities in the self-charging pacemakers market are abundant, driven by ongoing technological breakthroughs and evolving healthcare needs. The development of fully implantable, leadless self-charging pacemakers represents a significant advancement, offering greater patient mobility and reduced invasiveness. Expansion into emerging economies with growing healthcare expenditure and increasing awareness of advanced cardiac care presents a substantial market potential. Furthermore, the integration of self-charging capabilities into other implantable electronic devices, such as neurostimulators and defibrillators, opens up new avenues for innovation and market diversification, potentially creating new markets worth billions.

- Leadless Pacemaker Integration: Development of fully implantable, self-sufficient devices.

- Emerging Market Expansion: Tapping into developing economies with rising healthcare budgets.

- Diversification: Applying self-charging technology to other implantable medical devices.

- Remote Monitoring & AI: Enhanced data collection and predictive analytics.

Leading Players in the Self Charging Pacemakers Market

- Medtronic

- Abbott

- Boston Scientific

- Biotronik

- LivaNova

- Pacetronix

- Osypka Medical

- Zoll Medical

- MicroPort

- Cook Medical

- Oscor Inc.

Key Developments in Self Charging Pacemakers Industry

- 2023 March: Abbott receives FDA approval for its next-generation implantable cardiac device with enhanced battery management, hinting at advancements in energy efficiency.

- 2022 October: Medtronic announces promising early results from its study on novel energy harvesting techniques for implantable devices.

- 2022 May: Boston Scientific showcases its research on piezoelectric energy harvesting for cardiac implants at a leading medical conference.

- 2021 September: Biotronik patents a new system for maximizing energy capture from physiological motion within the body.

- 2020 December: LivaNova initiates pilot studies for a miniaturized self-charging pacemaker concept.

Strategic Outlook for Self Charging Pacemakers Market

The strategic outlook for the self-charging pacemakers market is exceptionally strong, fueled by a clear trajectory towards greater patient autonomy and reduced healthcare burden. Continued investment in R&D for more efficient and versatile energy harvesting technologies, alongside advancements in biocompatible materials, will be critical for market leadership. Strategic partnerships between technology developers and established medical device manufacturers are likely to accelerate product commercialization and market penetration, reaching an estimated global market value of over $300 million by 2033. The focus will remain on developing implantable solutions that offer unparalleled longevity and minimal patient intervention, solidifying self-charging pacemakers as the future standard of cardiac rhythm management.

Self Charging Pacemakers Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Other

-

2. Type

- 2.1. Implantable pacemakers

- 2.2. External pacemakers

Self Charging Pacemakers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Self Charging Pacemakers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Self Charging Pacemakers Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Implantable pacemakers

- 5.2.2. External pacemakers

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Self Charging Pacemakers Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Implantable pacemakers

- 6.2.2. External pacemakers

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Self Charging Pacemakers Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Implantable pacemakers

- 7.2.2. External pacemakers

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Self Charging Pacemakers Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Implantable pacemakers

- 8.2.2. External pacemakers

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Self Charging Pacemakers Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Implantable pacemakers

- 9.2.2. External pacemakers

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Self Charging Pacemakers Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Implantable pacemakers

- 10.2.2. External pacemakers

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Medtronic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Abbott

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Boston Scientific

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Biotronik

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 LivaNova

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Pacetronix

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Osypka Medical

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Zoll Medical

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MicroPort

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cook Medical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Oscor Inc.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Medtronic

List of Figures

- Figure 1: Global Self Charging Pacemakers Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Self Charging Pacemakers Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Self Charging Pacemakers Revenue (million), by Application 2024 & 2032

- Figure 4: North America Self Charging Pacemakers Volume (K), by Application 2024 & 2032

- Figure 5: North America Self Charging Pacemakers Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Self Charging Pacemakers Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Self Charging Pacemakers Revenue (million), by Type 2024 & 2032

- Figure 8: North America Self Charging Pacemakers Volume (K), by Type 2024 & 2032

- Figure 9: North America Self Charging Pacemakers Revenue Share (%), by Type 2024 & 2032

- Figure 10: North America Self Charging Pacemakers Volume Share (%), by Type 2024 & 2032

- Figure 11: North America Self Charging Pacemakers Revenue (million), by Country 2024 & 2032

- Figure 12: North America Self Charging Pacemakers Volume (K), by Country 2024 & 2032

- Figure 13: North America Self Charging Pacemakers Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Self Charging Pacemakers Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Self Charging Pacemakers Revenue (million), by Application 2024 & 2032

- Figure 16: South America Self Charging Pacemakers Volume (K), by Application 2024 & 2032

- Figure 17: South America Self Charging Pacemakers Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Self Charging Pacemakers Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Self Charging Pacemakers Revenue (million), by Type 2024 & 2032

- Figure 20: South America Self Charging Pacemakers Volume (K), by Type 2024 & 2032

- Figure 21: South America Self Charging Pacemakers Revenue Share (%), by Type 2024 & 2032

- Figure 22: South America Self Charging Pacemakers Volume Share (%), by Type 2024 & 2032

- Figure 23: South America Self Charging Pacemakers Revenue (million), by Country 2024 & 2032

- Figure 24: South America Self Charging Pacemakers Volume (K), by Country 2024 & 2032

- Figure 25: South America Self Charging Pacemakers Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Self Charging Pacemakers Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Self Charging Pacemakers Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Self Charging Pacemakers Volume (K), by Application 2024 & 2032

- Figure 29: Europe Self Charging Pacemakers Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Self Charging Pacemakers Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Self Charging Pacemakers Revenue (million), by Type 2024 & 2032

- Figure 32: Europe Self Charging Pacemakers Volume (K), by Type 2024 & 2032

- Figure 33: Europe Self Charging Pacemakers Revenue Share (%), by Type 2024 & 2032

- Figure 34: Europe Self Charging Pacemakers Volume Share (%), by Type 2024 & 2032

- Figure 35: Europe Self Charging Pacemakers Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Self Charging Pacemakers Volume (K), by Country 2024 & 2032

- Figure 37: Europe Self Charging Pacemakers Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Self Charging Pacemakers Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Self Charging Pacemakers Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Self Charging Pacemakers Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Self Charging Pacemakers Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Self Charging Pacemakers Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Self Charging Pacemakers Revenue (million), by Type 2024 & 2032

- Figure 44: Middle East & Africa Self Charging Pacemakers Volume (K), by Type 2024 & 2032

- Figure 45: Middle East & Africa Self Charging Pacemakers Revenue Share (%), by Type 2024 & 2032

- Figure 46: Middle East & Africa Self Charging Pacemakers Volume Share (%), by Type 2024 & 2032

- Figure 47: Middle East & Africa Self Charging Pacemakers Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Self Charging Pacemakers Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Self Charging Pacemakers Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Self Charging Pacemakers Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Self Charging Pacemakers Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Self Charging Pacemakers Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Self Charging Pacemakers Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Self Charging Pacemakers Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Self Charging Pacemakers Revenue (million), by Type 2024 & 2032

- Figure 56: Asia Pacific Self Charging Pacemakers Volume (K), by Type 2024 & 2032

- Figure 57: Asia Pacific Self Charging Pacemakers Revenue Share (%), by Type 2024 & 2032

- Figure 58: Asia Pacific Self Charging Pacemakers Volume Share (%), by Type 2024 & 2032

- Figure 59: Asia Pacific Self Charging Pacemakers Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Self Charging Pacemakers Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Self Charging Pacemakers Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Self Charging Pacemakers Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Self Charging Pacemakers Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Self Charging Pacemakers Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Self Charging Pacemakers Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Self Charging Pacemakers Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Self Charging Pacemakers Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Self Charging Pacemakers Volume K Forecast, by Type 2019 & 2032

- Table 7: Global Self Charging Pacemakers Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Self Charging Pacemakers Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Self Charging Pacemakers Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Self Charging Pacemakers Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Self Charging Pacemakers Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Self Charging Pacemakers Volume K Forecast, by Type 2019 & 2032

- Table 13: Global Self Charging Pacemakers Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Self Charging Pacemakers Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Self Charging Pacemakers Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Self Charging Pacemakers Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Self Charging Pacemakers Revenue million Forecast, by Type 2019 & 2032

- Table 24: Global Self Charging Pacemakers Volume K Forecast, by Type 2019 & 2032

- Table 25: Global Self Charging Pacemakers Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Self Charging Pacemakers Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Self Charging Pacemakers Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Self Charging Pacemakers Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Self Charging Pacemakers Revenue million Forecast, by Type 2019 & 2032

- Table 36: Global Self Charging Pacemakers Volume K Forecast, by Type 2019 & 2032

- Table 37: Global Self Charging Pacemakers Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Self Charging Pacemakers Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Self Charging Pacemakers Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Self Charging Pacemakers Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Self Charging Pacemakers Revenue million Forecast, by Type 2019 & 2032

- Table 60: Global Self Charging Pacemakers Volume K Forecast, by Type 2019 & 2032

- Table 61: Global Self Charging Pacemakers Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Self Charging Pacemakers Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Self Charging Pacemakers Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Self Charging Pacemakers Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Self Charging Pacemakers Revenue million Forecast, by Type 2019 & 2032

- Table 78: Global Self Charging Pacemakers Volume K Forecast, by Type 2019 & 2032

- Table 79: Global Self Charging Pacemakers Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Self Charging Pacemakers Volume K Forecast, by Country 2019 & 2032

- Table 81: China Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Self Charging Pacemakers Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Self Charging Pacemakers Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Self Charging Pacemakers?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Self Charging Pacemakers?

Key companies in the market include Medtronic, Abbott, Boston Scientific, Biotronik, LivaNova, Pacetronix, Osypka Medical, Zoll Medical, MicroPort, Cook Medical, Oscor Inc..

3. What are the main segments of the Self Charging Pacemakers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Self Charging Pacemakers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Self Charging Pacemakers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Self Charging Pacemakers?

To stay informed about further developments, trends, and reports in the Self Charging Pacemakers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence