Key Insights

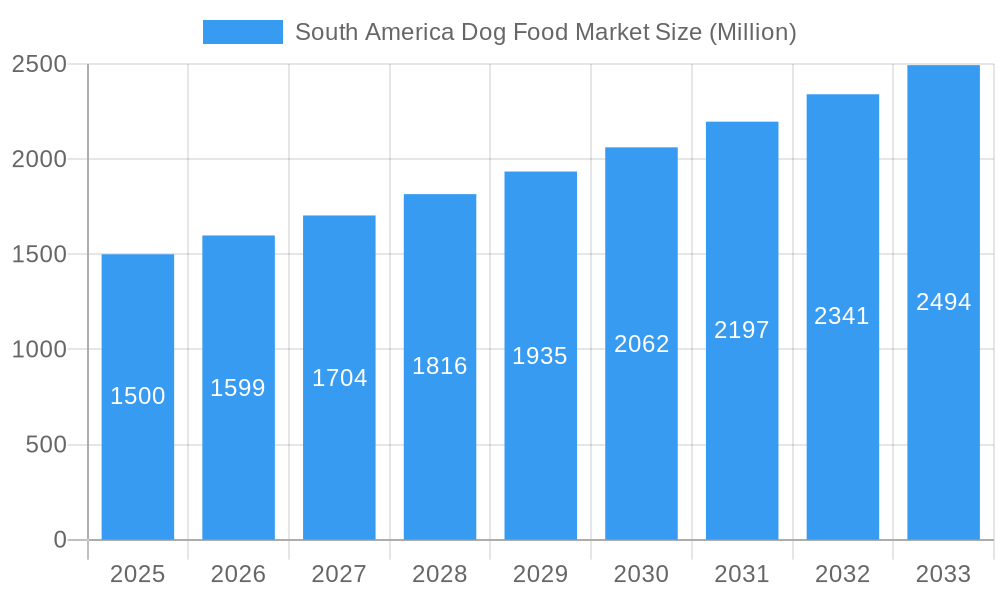

The South American dog food market, projected to reach $12.38 billion by 2033, is set for significant expansion. Driven by a Compound Annual Growth Rate (CAGR) of 8.21% from 2025, this growth is underpinned by increasing pet ownership, particularly in urban centers of Brazil and Argentina. Rising disposable incomes and a growing middle class are fueling demand for premium and specialized dog food. Enhanced awareness of pet health and nutrition further propels the need for high-quality, balanced diets, including veterinary formulations. The market is segmented by country (Brazil, Argentina, Rest of South America), product type (dry, wet, veterinary diets), and distribution channels (convenience, online, specialty, supermarkets/hypermarkets). Brazil and Argentina lead market share due to high pet ownership and economic development. Key players include Mars Incorporated, Nestle (Purina), ADM, BRF Global, and Empresas Carozzi SA.

South America Dog Food Market Market Size (In Billion)

Key trends influencing the South American dog food market include the surge in e-commerce, expanding accessibility and distribution. Growing consumer preference for natural, organic, and grain-free options highlights a focus on healthier pet nutrition. Market restraints include economic volatility impacting consumer expenditure and intense competition requiring continuous product innovation and strategic marketing. The 2025-2033 forecast period offers substantial growth potential, especially for companies adept at meeting evolving consumer demands for premium and specialized dog food. Understanding regional preferences and distribution dynamics is vital for market success.

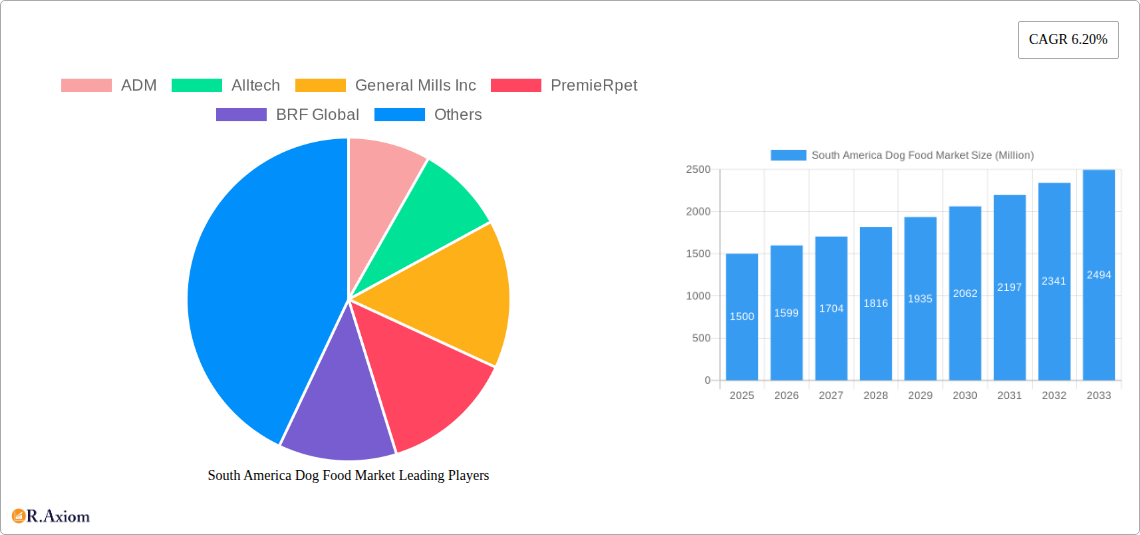

South America Dog Food Market Company Market Share

South America Dog Food Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the South America dog food market, encompassing market size, segmentation, growth drivers, challenges, and key players. The report covers the period 2019-2033, with a focus on the estimated year 2025 and a forecast period of 2025-2033. It offers actionable insights for industry stakeholders, including manufacturers, distributors, and investors. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx%.

South America Dog Food Market Concentration & Innovation

This section analyzes the competitive landscape of the South America dog food market, evaluating market concentration, innovation drivers, regulatory frameworks, and industry dynamics. The market exhibits a moderately concentrated structure, with key players such as Mars Incorporated, Nestlé (Purina), and General Mills Inc. holding significant market share. However, smaller regional players and new entrants continue to exert pressure.

- Market Concentration: The top 5 players account for approximately xx% of the total market share in 2025. This figure is expected to slightly decrease to xx% by 2033 due to increased competition.

- Innovation Drivers: The growing demand for premium and specialized dog food, coupled with rising pet ownership and humanization of pets, drives innovation. This includes the development of functional foods with added health benefits (e.g., joint health, weight management), novel protein sources, and sustainable packaging.

- Regulatory Framework: Varying regulatory standards across South American countries impact product formulation and labeling. Compliance costs and differing regulations pose challenges for companies operating across multiple countries.

- Product Substitutes: Homemade dog food and other pet food alternatives present competition to the commercial dog food sector. However, the convenience and nutritional balance of commercial dog food continue to be key advantages.

- End-User Trends: Consumers are increasingly discerning, prioritizing high-quality ingredients, natural formulations, and transparency in sourcing. Demand for organic, grain-free, and hypoallergenic options is surging.

- M&A Activities: The South American dog food market has witnessed several mergers and acquisitions in recent years. These transactions, totaling approximately xx Million in value during the historical period (2019-2024), have primarily focused on expanding product portfolios and market reach.

South America Dog Food Market Industry Trends & Insights

The South America dog food market is experiencing a dynamic evolution, propelled by a confluence of socioeconomic shifts and evolving consumer priorities. A primary catalyst for this growth is the escalating rate of pet ownership across the region, a trend deeply intertwined with increasing urbanization and a shift towards more companion-centric lifestyles. Coupled with this is a discernible rise in disposable incomes in several South American nations, empowering pet owners to invest more significantly in the well-being and nutritional needs of their canine companions. Consumer preferences are also undergoing a transformation, with a growing demand for high-quality, natural, and scientifically formulated pet food options. Technological advancements are playing a pivotal role, with innovations in manufacturing processes leading to enhanced product quality and safety, while the emergence of personalized nutrition solutions caters to the specific dietary requirements and health goals of individual dogs.

The market exhibits a robust growth trajectory, with significant expansion projected throughout the forecast period (2025-2033). This upward trend is underpinned by the aforementioned factors of rising pet ownership, expanding disposable incomes, and a pronounced shift towards premium and specialized pet food offerings. Key emerging trends include a substantial increase in the demand for functional dog foods, designed to address specific health concerns like digestive health, skin and coat condition, and age-related issues, as well as specialized dietary formulations for dogs with allergies or specific medical conditions. Furthermore, the online pet food retail segment is witnessing accelerated adoption, driven by convenience and wider product availability. The competitive landscape is characterized by the strategic maneuvers of established industry giants focusing on continuous product innovation and market expansion, alongside a growing influx of agile, specialized brands carving out niches in the premium and artisanal segments. The penetration of premium dog foods is on a steady ascent, moving from approximately XX% in 2025 to an anticipated **XX%** by 2033, reflecting a heightened consumer commitment to superior canine nutrition.

Dominant Markets & Segments in South America Dog Food Market

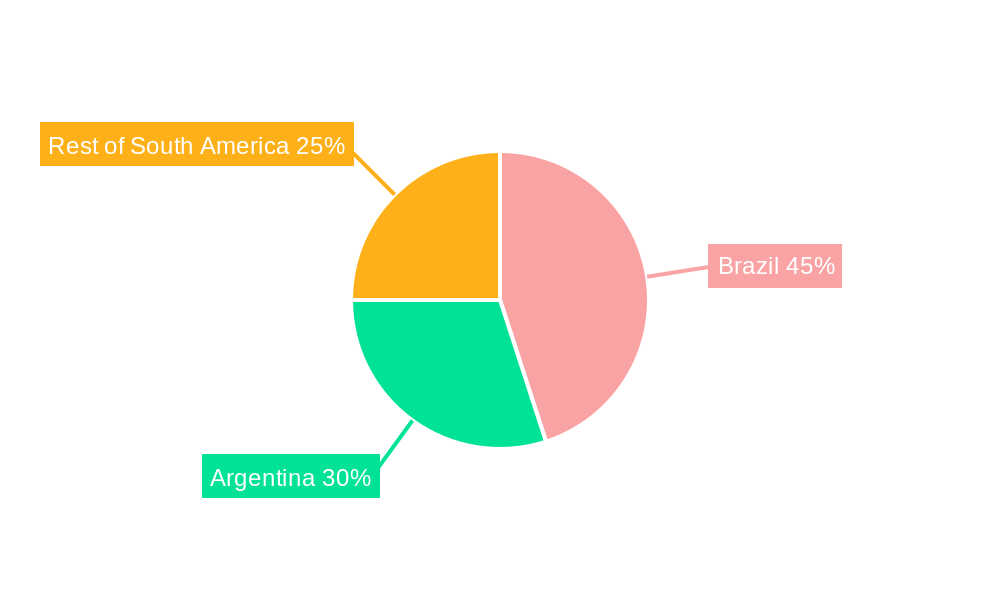

Brazil stands as the undisputed leader in the South America dog food market, commanding the largest share in both volume and value. This dominance is a direct consequence of its substantial population, coupled with exceptionally high pet ownership rates and a well-developed and accessible pet food retail infrastructure. The country's burgeoning middle class and increasing pet humanization further solidify its position as the primary market driver.

- Country Dominance:

- Brazil: The largest and most influential market, propelled by its vast population, high pet ownership statistics, and an expanding middle class with growing purchasing power. Key drivers include rising disposable incomes, the profound "pet humanization" trend, and an extensive and efficient retail network.

- Argentina: A significant player within the South American market, exhibiting substantial growth potential. While slightly smaller than Brazil, its market performance can be influenced by economic fluctuations. The increasing adoption of premium pet food is a notable trend here.

- Rest of South America: This heterogeneous segment encompasses a range of countries with diverse economic landscapes, varying pet ownership rates, and distinct consumer preferences. Growth patterns are varied, influenced by local economic development, regulatory environments, and cultural attitudes towards pet care.

- Pet Food Product: Dry dog food continues to hold the dominant market share due to its convenience, shelf-life, and cost-effectiveness. However, wet dog food is gaining traction as consumers seek more palatable and natural options. Notably, the "Other Veterinary Diets" segment is demonstrating robust growth, driven by an increasing owner awareness of specialized nutritional needs for dogs with specific health conditions, allergies, or life stages.

- Distribution Channel: Supermarkets and hypermarkets remain the primary distribution channels, offering convenience and a wide selection. Specialty pet stores are gaining prominence, catering to consumers seeking premium and specialized products. Convenience stores are also contributing to market reach. The online channel is experiencing exponential growth, fueled by widespread internet penetration, the proliferation of e-commerce platforms, and the increasing consumer demand for home delivery and wider product selection.

South America Dog Food Market Product Developments

The South American dog food market is witnessing a wave of innovative product developments, driven by a discerning consumer base prioritizing their pets' health and well-being. A significant trend is the introduction of functional dog foods, fortified with specific ingredients to enhance health benefits, such as those promoting joint health, aiding in weight management, supporting digestive regularity, and improving skin and coat vitality. The exploration of novel protein sources, including insect-based proteins, duck, and venison, is on the rise, catering to pets with sensitivities or owners seeking more sustainable and hypoallergenic options. Furthermore, a strong emphasis is being placed on sustainability, with manufacturers increasingly adopting eco-friendly packaging solutions, including recyclable materials and biodegradable options, and prioritizing ethically sourced ingredients. Technological advancements are revolutionizing pet food manufacturing, with the implementation of precision nutrition, allowing for tailored nutrient profiles based on a dog's breed, age, activity level, and health status, and the adoption of advanced formulation techniques to optimize bioavailability and palatability. These developments are collectively reshaping the market towards higher-quality, more specialized, and ethically produced dog food.

Report Scope & Segmentation Analysis

This comprehensive report meticulously segments the South America dog food market to provide in-depth analysis and actionable insights. The segmentation is based on key parameters including Country (Argentina, Brazil, Rest of South America), Pet Food Product (Dry Food, Wet Food, Veterinary Diets, Treats & Snacks), and Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, Other Channels). Each segment's current market size, historical growth, and future projections (2025-2033) are analyzed in detail, alongside an assessment of their respective competitive dynamics. For instance, the online channel segment is projected to exhibit the highest Compound Annual Growth Rate (CAGR) during the forecast period, driven by increasing e-commerce adoption and convenience-seeking consumers. Conversely, the supermarkets/hypermarkets segment, while potentially experiencing slower growth, continues to dominate in terms of overall market share due to its broad reach. The Veterinary Diets segment is expected to witness significant, above-average growth, fueled by a heightened pet owner awareness of preventative healthcare, the availability of specialized formulations for specific medical conditions, and the increasing recommendation of therapeutic diets by veterinary professionals.

Key Drivers of South America Dog Food Market Growth

The burgeoning South American dog food market is experiencing robust and sustained growth, propelled by a powerful set of interconnected drivers:

- Rising Pet Ownership: The ongoing trend of increasing urbanization and evolving family structures across South America is significantly contributing to a surge in pet ownership. Dogs are increasingly viewed as integral members of the family, fostering a greater demand for dedicated pet care products, including high-quality food.

- Growing Disposable Incomes: Improvements in economic conditions and the expansion of the middle class in several South American countries are leading to increased discretionary spending on pet care. Owners are more willing and able to invest in premium, specialized, and health-oriented dog food options.

- Humanization of Pets: The deeply ingrained "humanization of pets" trend is a primary growth engine. As pets are increasingly treated as family members, owners are seeking food products that mirror the quality, nutritional value, and even the perceived "premiumness" of human food, leading to a demand for natural, organic, and specialized formulations.

- Increased Awareness of Pet Health: There is a growing understanding among pet owners regarding the critical link between nutrition and their dog's overall health and longevity. This heightened awareness is driving demand for functional dog foods that offer specific health benefits, such as improved digestion, enhanced immune support, and better joint health, as well as preventative care through specialized dietary interventions.

Challenges in the South America Dog Food Market Sector

Several factors challenge the growth of the South America dog food market:

- Economic Volatility: Economic fluctuations in some South American countries can impact consumer spending on non-essential items like pet food.

- Supply Chain Disruptions: Global supply chain disruptions can affect the availability and cost of raw materials.

- Competition: The market is becoming increasingly competitive, with both established players and new entrants vying for market share. This necessitates continuous product innovation and competitive pricing.

Emerging Opportunities in South America Dog Food Market

The South America dog food market presents several significant opportunities:

- Premiumization: The growing demand for premium and specialized dog food presents an opportunity for companies to develop and market high-value products.

- Online Sales: The expansion of e-commerce presents opportunities to reach new customer segments through online channels.

- Functional Foods: The increasing awareness of pet health and nutrition is driving demand for dog foods with added health benefits.

Leading Players in the South America Dog Food Market Market

- ADM

- Alltech

- General Mills Inc

- PremieRpet

- BRF Global

- FARMINA PET FOODS

- Mars Incorporated

- Nestle (Purina)

- Empresas Carozzi SA

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc )

- Virba

Key Developments in South America Dog Food Market Industry

- July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. This launch reflects the growing trend towards sustainable and hypoallergenic pet food.

- March 2023: PremieRpet launched a line of superpremium, "Protein-packed" meal toppers/treats for dogs and cats under the brand Natoo. This expansion indicates a focus on premium and value-added pet food products in the Brazilian market.

- March 2023: Blue Buffalo (General Mills Inc.) launched its new high-protein dry dog food line, BLUE Wilderness Premier Blend. This demonstrates continued competition in the premium dog food segment.

Strategic Outlook for South America Dog Food Market Market

The South America dog food market is poised for continued growth, driven by sustained increases in pet ownership, rising disposable incomes, and evolving consumer preferences. Companies that successfully leverage technological advancements, focus on product innovation, and adapt to the evolving needs of discerning consumers are best positioned for success. The market's potential is substantial, especially in countries experiencing economic growth and rising middle-class populations. Focus on sustainability and ethical sourcing practices will play a key role in shaping future market dynamics.

South America Dog Food Market Segmentation

-

1. Pet Food Product

-

1.1. By Sub Product

-

1.1.1. Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.1.1.1. Kibbles

- 1.1.1.1.2. Other Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.2. Wet Pet Food

-

1.1.1. Dry Pet Food

-

1.2. Pet Nutraceuticals/Supplements

- 1.2.1. Milk Bioactives

- 1.2.2. Omega-3 Fatty Acids

- 1.2.3. Probiotics

- 1.2.4. Proteins and Peptides

- 1.2.5. Vitamins and Minerals

- 1.2.6. Other Nutraceuticals

-

1.3. Pet Treats

- 1.3.1. Crunchy Treats

- 1.3.2. Dental Treats

- 1.3.3. Freeze-dried and Jerky Treats

- 1.3.4. Soft & Chewy Treats

- 1.3.5. Other Treats

-

1.4. Pet Veterinary Diets

- 1.4.1. Diabetes

- 1.4.2. Digestive Sensitivity

- 1.4.3. Oral Care Diets

- 1.4.4. Renal

- 1.4.5. Urinary tract disease

- 1.4.6. Other Veterinary Diets

-

1.1. By Sub Product

-

2. Distribution Channel

- 2.1. Convenience Stores

- 2.2. Online Channel

- 2.3. Specialty Stores

- 2.4. Supermarkets/Hypermarkets

- 2.5. Other Channels

South America Dog Food Market Segmentation By Geography

-

1. South America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Peru

- 1.6. Venezuela

- 1.7. Ecuador

- 1.8. Bolivia

- 1.9. Paraguay

- 1.10. Uruguay

South America Dog Food Market Regional Market Share

Geographic Coverage of South America Dog Food Market

South America Dog Food Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 5.1.1. By Sub Product

- 5.1.1.1. Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.1.1.1. Kibbles

- 5.1.1.1.1.2. Other Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.2. Wet Pet Food

- 5.1.1.1. Dry Pet Food

- 5.1.2. Pet Nutraceuticals/Supplements

- 5.1.2.1. Milk Bioactives

- 5.1.2.2. Omega-3 Fatty Acids

- 5.1.2.3. Probiotics

- 5.1.2.4. Proteins and Peptides

- 5.1.2.5. Vitamins and Minerals

- 5.1.2.6. Other Nutraceuticals

- 5.1.3. Pet Treats

- 5.1.3.1. Crunchy Treats

- 5.1.3.2. Dental Treats

- 5.1.3.3. Freeze-dried and Jerky Treats

- 5.1.3.4. Soft & Chewy Treats

- 5.1.3.5. Other Treats

- 5.1.4. Pet Veterinary Diets

- 5.1.4.1. Diabetes

- 5.1.4.2. Digestive Sensitivity

- 5.1.4.3. Oral Care Diets

- 5.1.4.4. Renal

- 5.1.4.5. Urinary tract disease

- 5.1.4.6. Other Veterinary Diets

- 5.1.1. By Sub Product

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Stores

- 5.2.2. Online Channel

- 5.2.3. Specialty Stores

- 5.2.4. Supermarkets/Hypermarkets

- 5.2.5. Other Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. South America

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6. South America Dog Food Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6.1.1. By Sub Product

- 6.1.1.1. Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.1.1.1. Kibbles

- 6.1.1.1.1.2. Other Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.2. Wet Pet Food

- 6.1.1.1. Dry Pet Food

- 6.1.2. Pet Nutraceuticals/Supplements

- 6.1.2.1. Milk Bioactives

- 6.1.2.2. Omega-3 Fatty Acids

- 6.1.2.3. Probiotics

- 6.1.2.4. Proteins and Peptides

- 6.1.2.5. Vitamins and Minerals

- 6.1.2.6. Other Nutraceuticals

- 6.1.3. Pet Treats

- 6.1.3.1. Crunchy Treats

- 6.1.3.2. Dental Treats

- 6.1.3.3. Freeze-dried and Jerky Treats

- 6.1.3.4. Soft & Chewy Treats

- 6.1.3.5. Other Treats

- 6.1.4. Pet Veterinary Diets

- 6.1.4.1. Diabetes

- 6.1.4.2. Digestive Sensitivity

- 6.1.4.3. Oral Care Diets

- 6.1.4.4. Renal

- 6.1.4.5. Urinary tract disease

- 6.1.4.6. Other Veterinary Diets

- 6.1.1. By Sub Product

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Convenience Stores

- 6.2.2. Online Channel

- 6.2.3. Specialty Stores

- 6.2.4. Supermarkets/Hypermarkets

- 6.2.5. Other Channels

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ADM

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Alltech

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 General Mills Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PremieRpet

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BRF Global

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FARMINA PET FOODS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mars Incorporated

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Nestle (Purina)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Empresas Carozzi SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Colgate-Palmolive Company (Hill's Pet Nutrition Inc )

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Virba

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 ADM

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South America Dog Food Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America Dog Food Market Share (%) by Company 2025

List of Tables

- Table 1: South America Dog Food Market Revenue billion Forecast, by Pet Food Product 2020 & 2033

- Table 2: South America Dog Food Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: South America Dog Food Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: South America Dog Food Market Revenue billion Forecast, by Pet Food Product 2020 & 2033

- Table 5: South America Dog Food Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: South America Dog Food Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Brazil South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Argentina South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Chile South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Colombia South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Peru South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Venezuela South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Ecuador South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Bolivia South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Paraguay South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Uruguay South America Dog Food Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Dog Food Market?

The projected CAGR is approximately 8.21%.

2. Which companies are prominent players in the South America Dog Food Market?

Key companies in the market include ADM, Alltech, General Mills Inc, PremieRpet, BRF Global, FARMINA PET FOODS, Mars Incorporated, Nestle (Purina), Empresas Carozzi SA, Colgate-Palmolive Company (Hill's Pet Nutrition Inc ), Virba.

3. What are the main segments of the South America Dog Food Market?

The market segments include Pet Food Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.38 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Meat; Initiatives By the Key Players; Focus on Animal nutrition and Health.

6. What are the notable trends driving market growth?

Brazil dominated the market with the presence of a highly established distribution network.

7. Are there any restraints impacting market growth?

Shift Toward Vegan- Based Diet; Changing Raw Material Prices and Strict Government Rules to Restrict Market Growth.

8. Can you provide examples of recent developments in the market?

July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.March 2023: PremieRpet launched a line of superpremium, "Protein-packed" meal toppers/treats for dogs and cats under the brand Natoo. These are produced at PremieRpet's facility in Brazil.March 2023: Blue Buffalo, a subsidiary of General Mills Inc., launched its new high-protein dry dog food line, BLUE Wilderness Premier Blend. It is formulated with chicken and a blend of antioxidants, vitamins, and minerals.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Dog Food Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Dog Food Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Dog Food Market?

To stay informed about further developments, trends, and reports in the South America Dog Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence