Key Insights

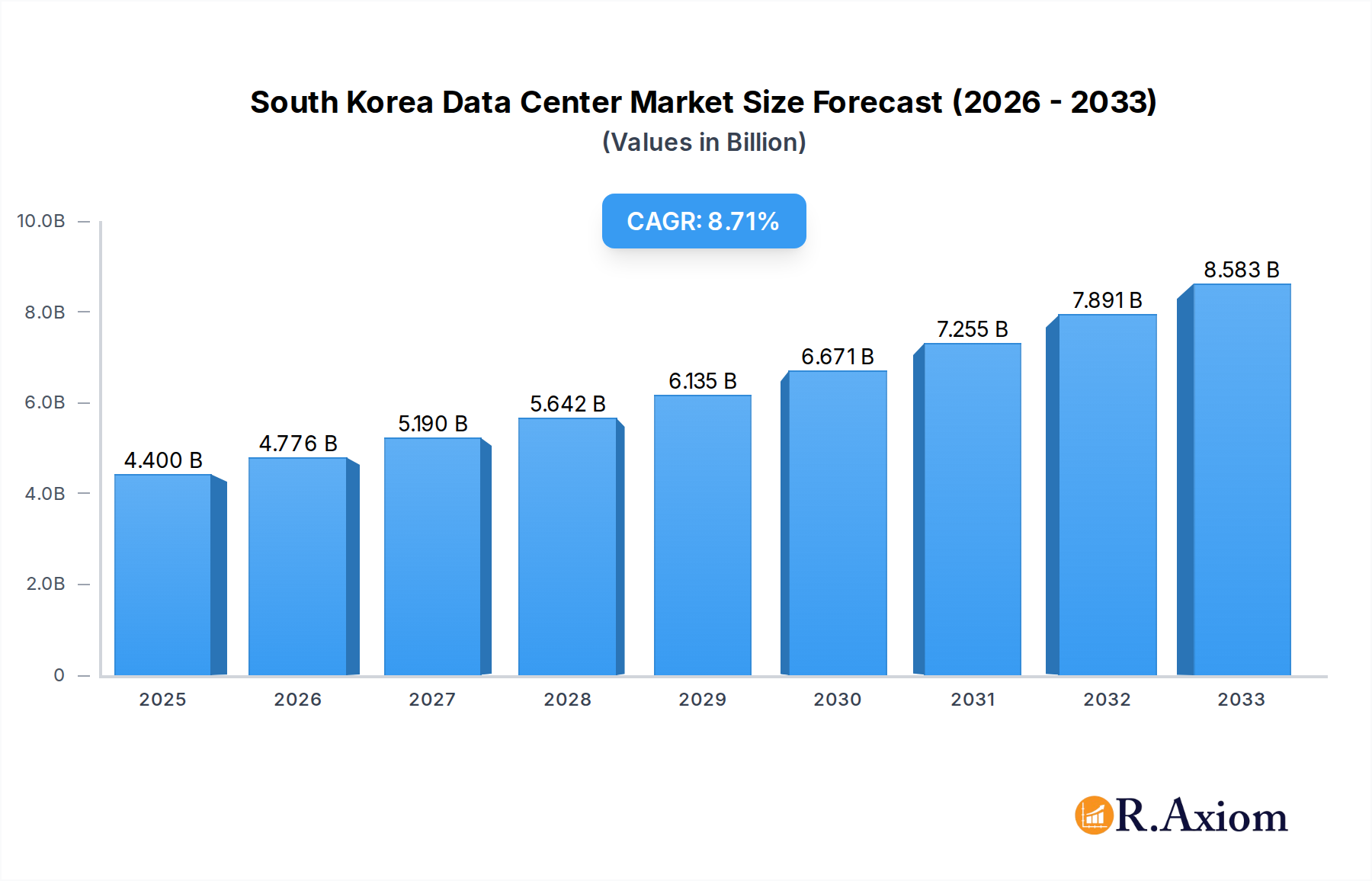

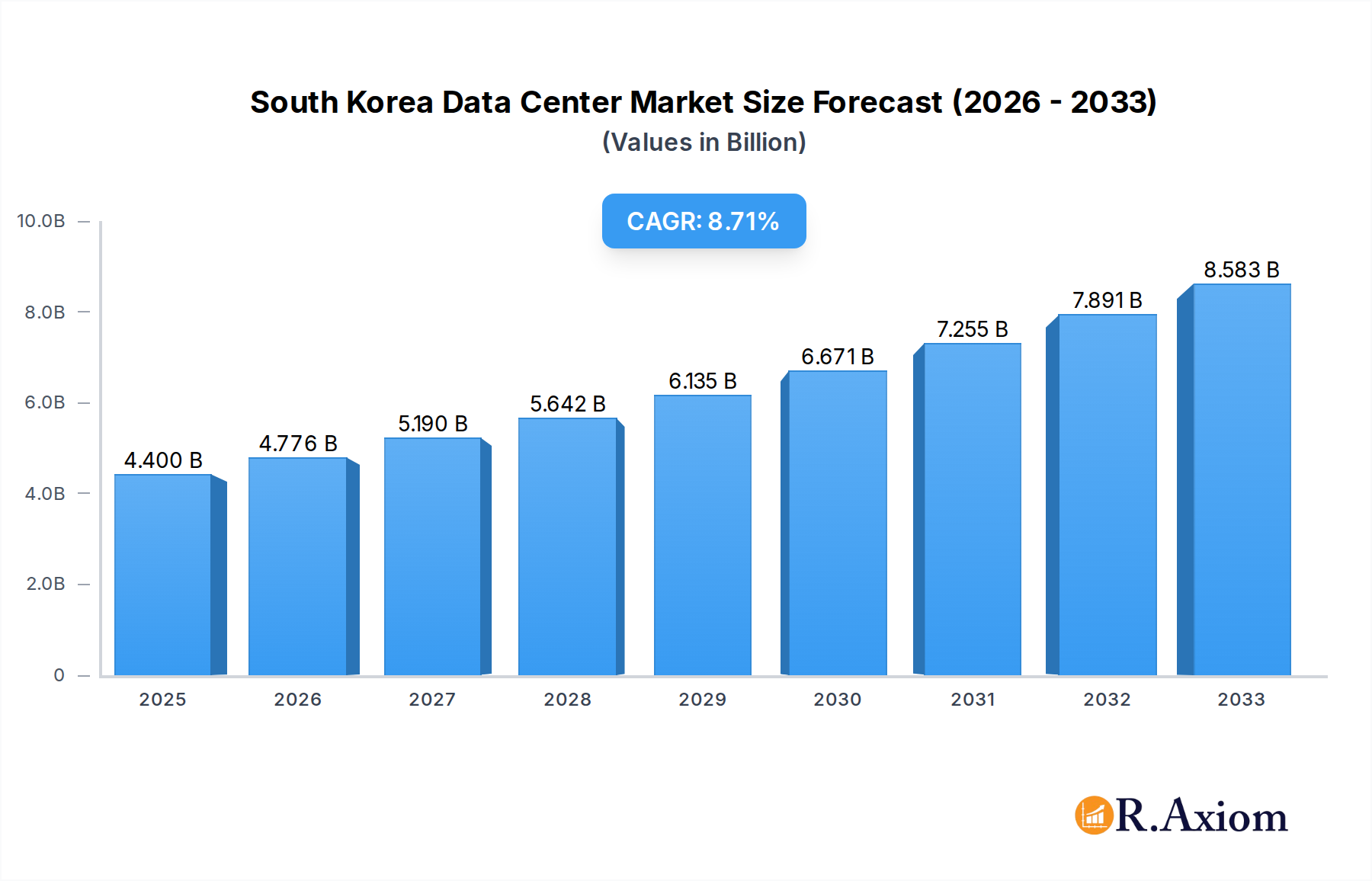

The South Korean data center market is poised for significant expansion, driven by a surge in digital transformation and the escalating demand for cloud services, e-commerce, and advanced technologies. With a market size of approximately $4.4 billion in 2025 and a robust CAGR of 8.69%, the sector is set to experience substantial growth throughout the forecast period of 2025-2033. Key market drivers include the rapid adoption of 5G technology, the burgeoning media and entertainment industry, and the increasing investments by hyperscale cloud providers and BFSI institutions to support their digital infrastructure. The growing reliance on data-intensive applications across government, manufacturing, and telecom sectors further fuels this demand. Strategic investments in building out infrastructure in key hubs like Busan and Greater Seoul, alongside the development of advanced data center sizes ranging from Medium to Mega and Tier 3 and 4 classifications, are crucial for accommodating this growth. The market's trajectory indicates a strong future, with a continuous need for scalable and high-performance data center solutions to support South Korea's digital economy.

South Korea Data Center Market Market Size (In Billion)

The competitive landscape features established players like Naver, Lotte Data Communication, Equinix, and SK Broadband, alongside emerging entities like Digital Edge and Digital Realty, all vying for market share through strategic expansions and partnerships. The colocation segment, encompassing both hyperscale and retail services, is a primary focus, catering to diverse end-user needs. While the market benefits from strong government support for digital infrastructure and high internet penetration rates, potential restraints such as rising operational costs, energy consumption concerns, and the availability of skilled labor could pose challenges. However, the overarching trend of increasing data generation and the imperative for secure, reliable data storage and processing solutions will likely outweigh these restraints, ensuring sustained market momentum. The absorption of non-utilized space within existing facilities will also play a role in market dynamics as new capacities come online.

South Korea Data Center Market Company Market Share

This in-depth report provides a detailed analysis of the South Korea Data Center Market, offering critical insights for stakeholders, investors, and industry professionals. We cover the historical period from 2019 to 2024 and forecast growth through 2033, with 2025 as the base year. This study delves into market concentration, innovation, industry trends, dominant segments, product developments, key growth drivers, challenges, emerging opportunities, leading players, and pivotal industry developments.

South Korea Data Center Market Market Concentration & Innovation

The South Korea Data Center Market is characterized by a dynamic interplay of established players and emerging innovators, contributing to a moderate to high market concentration. Key companies such as Naver, Lotte Data Communication, Equinix Inc, Telstra Corporation Limited, LG CNS, SK Broadband, Digital Edge (Singapore) Holdings Pte Ltd, Digital Realty Trust Inc, Telehouse (KDDI Corporation), KINX, KT Corporation, and Dreammark are actively shaping the competitive landscape. While specific market share percentages require granular analysis within the full report, the presence of large hyperscale providers and colocation specialists indicates a competitive environment. Innovation in the South Korean market is primarily driven by the burgeoning demand for cloud computing, AI, and 5G services, necessitating advanced infrastructure. Regulatory frameworks, while supportive of digital transformation, can also present compliance challenges. Product substitutes are limited in the core data center services, but the increasing adoption of edge computing and hybrid cloud solutions represents a nuanced competitive dynamic. End-user demand for reliable, low-latency, and high-capacity infrastructure is a constant driver for innovation. Merger and acquisition activities are expected to play a role in market consolidation and expansion, with deal values anticipated to reflect the strategic importance of South Korea's digital infrastructure.

South Korea Data Center Market Industry Trends & Insights

The South Korea Data Center Market is experiencing robust growth, propelled by several key factors. The nation's advanced digital economy, coupled with a high internet penetration rate and a strong adoption of emerging technologies like artificial intelligence, big data analytics, and the Internet of Things (IoT), is fueling an unprecedented demand for data processing and storage capabilities. The relentless expansion of cloud services, both public and private, by major providers, alongside the increasing adoption of hybrid and multi-cloud strategies by enterprises across all sectors, directly translates into a greater need for scalable and reliable data center infrastructure. The government's commitment to digital transformation initiatives and its vision for becoming a global leader in the digital economy further stimulates investment and development within the data center sector.

Technological disruptions are continuously reshaping the industry. The advent of 5G networks, with their promise of ultra-low latency and massive connectivity, is creating new use cases and demanding geographically distributed edge data centers to support real-time applications. Furthermore, advancements in cooling technologies, power efficiency solutions, and automated management systems are crucial for optimizing operational costs and environmental impact, addressing growing sustainability concerns. The rise of AI and machine learning workloads necessitates high-performance computing capabilities and specialized infrastructure within data centers.

Consumer preferences are shifting towards seamless digital experiences, which depend on fast, reliable access to online services and content. This demand directly influences the requirements for data center capacity and proximity. The media and entertainment industry, with its increasing reliance on streaming services and the production of high-resolution content, is a significant contributor to this trend. Similarly, the BFSI sector's need for secure, resilient, and compliant data handling for financial transactions and customer data is a constant driver for data center investment. The e-commerce sector's rapid growth, particularly accelerated by evolving shopping habits, requires robust infrastructure to manage online transactions, inventory, and customer engagement.

The competitive dynamics within the South Korean market are intense. A mix of global hyperscale providers, established domestic telecommunications companies, and specialized colocation providers are vying for market share. Strategic partnerships, mergers, and acquisitions are common as companies seek to expand their footprint, enhance their service offerings, and gain a competitive edge. The continuous evolution of digital infrastructure requirements means that companies must remain agile and innovative to meet the ever-growing and changing demands of end-users. The projected Compound Annual Growth Rate (CAGR) for the South Korea Data Center Market is expected to be significant, reflecting these strong market forces.

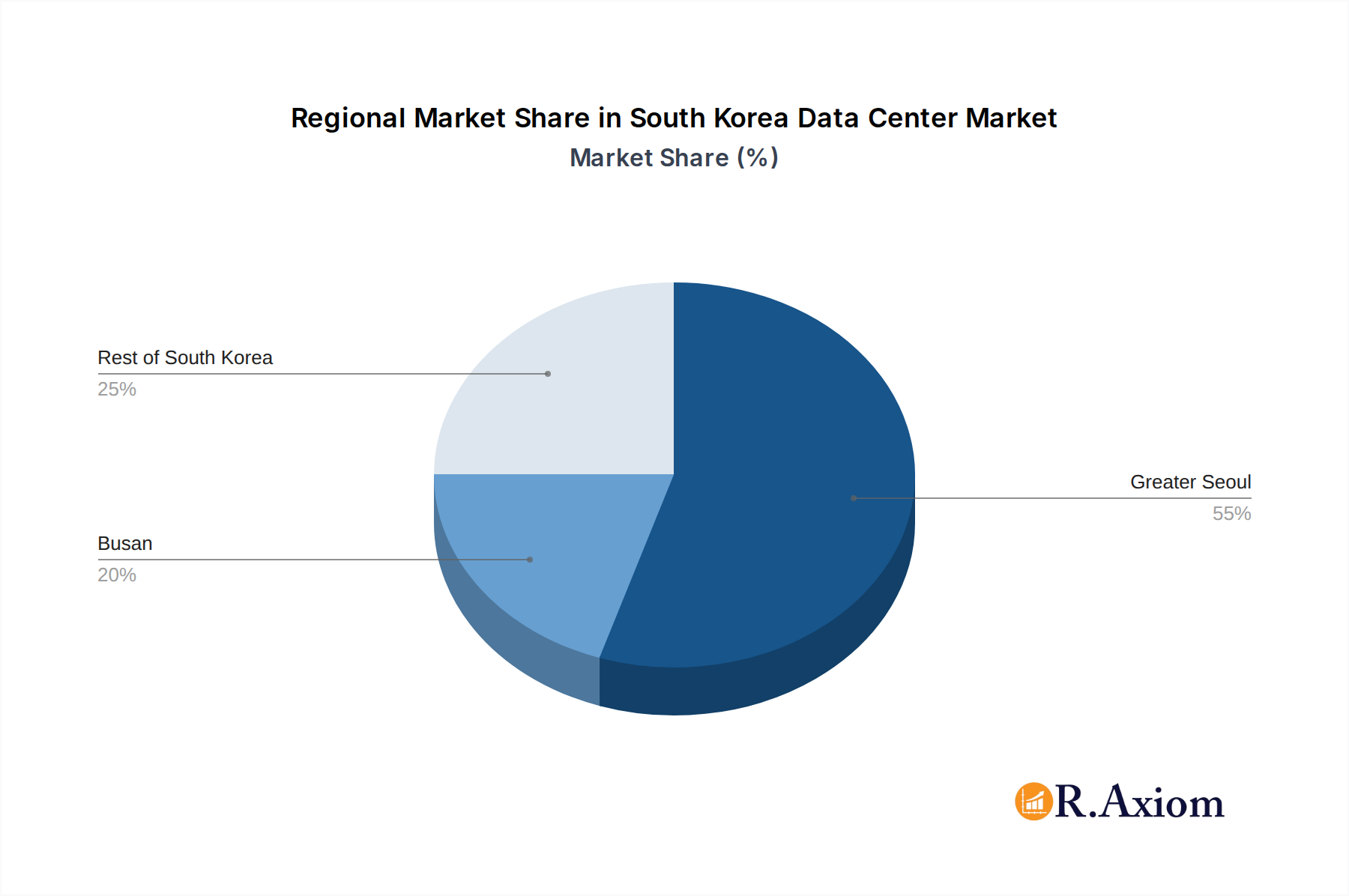

Dominant Markets & Segments in South Korea Data Center Market

The South Korea Data Center Market exhibits distinct dominance across various geographical hotspots and service segments, driven by economic policies, robust infrastructure development, and concentrated end-user demand.

Hotspot Dominance:

Greater Seoul: This region is overwhelmingly the dominant hotspot for data center development and operation.

- Key Drivers:

- Concentration of Enterprises: Seoul is the economic and business hub of South Korea, hosting the headquarters of a vast majority of large corporations across all end-user segments, including BFSI, Cloud, E-Commerce, Government, Manufacturing, Media & Entertainment, and Telecom.

- Availability of Skilled Workforce: The region possesses a deep pool of IT professionals and skilled labor essential for data center operations and management.

- Proximity to End-Users: Locating data centers in or near Greater Seoul ensures low latency for critical applications and services demanded by businesses and consumers in the capital region.

- Extensive Connectivity: Seoul benefits from advanced telecommunications infrastructure, fiber optic networks, and connectivity to international subsea cables, crucial for data transfer and accessibility.

- Government Support & Investment: The national government and Seoul Metropolitan Government often prioritize digital infrastructure development in the capital region, offering incentives and streamlined approvals.

- Key Drivers:

Busan: While smaller in scale compared to Seoul, Busan is emerging as a significant secondary market.

- Key Drivers:

- Strategic Port Location: As South Korea's largest port city, Busan offers advantages for international connectivity and potential for data sovereignty considerations.

- Government Initiatives for Regional Development: Efforts to decentralize digital infrastructure and foster regional economic growth are driving investment into Busan.

- Availability of Land and Power: Compared to the densely populated Seoul area, Busan may offer more accessible and potentially lower-cost land for large-scale data center developments.

- Key Drivers:

Rest of South Korea: This encompasses other major cities and industrial zones.

- Key Drivers:

- Diversification and Disaster Recovery: Companies are increasingly looking to build facilities outside of the primary hub for redundancy and disaster recovery purposes.

- Lower Operational Costs: Land and power costs can be more competitive in these regions.

- Specialized Industrial Needs: Certain manufacturing and research facilities may require localized data center presence.

- Key Drivers:

Data Center Size Dominance:

Mega and Large: These categories are witnessing the most significant growth, driven by hyperscale cloud providers and large enterprises.

- Key Drivers:

- Hyperscale Cloud Computing: The demand for massive compute and storage resources from global cloud giants like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud necessitates the construction of hyperscale facilities.

- Economies of Scale: Larger data centers offer better operational efficiency and cost-effectiveness for both providers and users.

- Consolidation of IT Infrastructure: Enterprises are increasingly consolidating their IT infrastructure into fewer, larger, and more advanced facilities.

- Key Drivers:

Medium and Small: These sizes cater to specific enterprise needs, edge computing, and colocation retail services.

- Key Drivers:

- Edge Computing Deployments: The need for low-latency processing closer to the end-user is driving the development of smaller, distributed data centers.

- Niche Applications: Specific industries or applications may require tailored, smaller-scale solutions.

- Retail Colocation Services: Smaller footprint options appeal to businesses that do not require entire halls or large halls.

- Key Drivers:

Tier Type Dominance:

- Tier 3 and Tier 4: These high-availability tiers are paramount for mission-critical applications and services.

- Key Drivers:

- Business Continuity: The demand for 99.999% uptime for critical services in BFSI, E-Commerce, and Government sectors necessitates Tier 3 and Tier 4 certifications.

- Regulatory Compliance: Many industries have strict regulatory requirements for data availability and resilience.

- Customer Expectations: End-users expect uninterrupted access to digital services, pushing data center operators to invest in advanced redundancy and fault tolerance.

- Key Drivers:

Absorption: Non-Utilized:

- Low Non-Utilized Capacity: The market is characterized by high absorption rates, especially in prime locations like Greater Seoul.

- Key Drivers:

- Rapid Digital Transformation: The accelerated adoption of digital services and cloud computing leads to high demand that often outpaces supply.

- Strategic Investments by Hyperscalers: Continuous investment and expansion by major cloud providers keep utilization rates high.

- Key Drivers:

Colocation Type Dominance:

Hyperscale and Wholesale: These segments are experiencing the most significant growth, driven by cloud providers and large enterprises.

- Key Drivers:

- Hyperscale Demand: As mentioned, global cloud providers are the primary drivers of hyperscale and wholesale colocation.

- Enterprise Outsourcing: Larger enterprises are increasingly opting for wholesale colocation to house their private clouds and dedicated infrastructure.

- Scalability and Flexibility: Wholesale offerings provide the scale and customization required by large organizations.

- Key Drivers:

Retail: This segment caters to a broader range of businesses with smaller space requirements.

- Key Drivers:

- SME Growth: Small and medium-sized enterprises require flexible and scalable colocation solutions.

- Connectivity Hubs: Retail colocation facilities often serve as critical connection points for various networks and cloud exchanges.

- Key Drivers:

End User Dominance:

- Cloud, Telecom, BFSI, and E-Commerce: These sectors are the primary drivers of data center demand.

- Key Drivers:

- Cloud Computing Expansion: The fundamental need for cloud infrastructure makes the Cloud sector a leading consumer.

- 5G Rollout and Network Expansion: The Telecom sector's investment in 5G and related services requires extensive data center capacity.

- Digital Transformation in Finance: The BFSI sector's reliance on data for transactions, analytics, and customer service fuels demand.

- Online Retail Growth: The booming E-Commerce market necessitates robust infrastructure for online platforms, logistics, and customer data.

- Key Drivers:

South Korea Data Center Market Product Developments

Product developments in the South Korea Data Center Market are intensely focused on enhancing efficiency, scalability, and sustainability. Innovations in power management, cooling solutions (such as liquid cooling for high-density computing), and modular data center designs are gaining traction. The market is also seeing advancements in software-defined networking (SDN) and storage solutions to enable greater flexibility and automation. Competitive advantages are being forged through the integration of AI-driven operational management for predictive maintenance and resource optimization, as well as the adoption of renewable energy sources and energy-efficient hardware to meet growing environmental demands.

Report Scope & Segmentation Analysis

This report segments the South Korea Data Center Market across key dimensions including geographical Hotspot (Busan, Greater Seoul, Rest of South Korea), Data Center Size (Large, Massive, Medium, Mega, Small), Tier Type (Tier 1 and 2, Tier 3, Tier 4), Absorption (Non-Utilized), Colocation Type (Hyperscale, Retail, Wholesale), and End User (BFSI, Cloud, E-Commerce, Government, Manufacturing, Media & Entertainment, Telecom, Other End User).

- Hotspot: Greater Seoul is expected to lead in market size and growth due to its economic significance, with Busan and other regions emerging as growth centers for diversification and cost advantages.

- Data Center Size: Mega and Large data centers will dominate in terms of capacity and investment due to hyperscale demand, while Small and Medium facilities will cater to edge computing and specialized enterprise needs.

- Tier Type: Tier 3 and Tier 4 facilities will see continued investment as demand for high availability and resilience remains critical for mission-critical applications.

- Absorption: Non-Utilized capacity is expected to remain low in prime locations due to robust demand, particularly from cloud providers.

- Colocation Type: Hyperscale and Wholesale colocation will drive market growth, reflecting the expansion of global cloud providers and large enterprises.

- End User: The Cloud, Telecom, BFSI, and E-Commerce sectors are projected to be the largest contributors to market revenue, driven by their ongoing digital transformation initiatives and increasing data consumption.

Key Drivers of South Korea Data Center Market Growth

The South Korea Data Center Market is propelled by several powerful growth drivers:

- Digital Transformation and Cloud Adoption: The pervasive adoption of cloud computing services by businesses of all sizes, fueled by the need for scalability, flexibility, and cost-efficiency.

- 5G Network Expansion: The rapid rollout and increasing adoption of 5G technology are generating massive amounts of data and requiring localized processing at the edge.

- Emerging Technologies: The growth of AI, IoT, big data analytics, and machine learning necessitates significant data processing and storage infrastructure.

- Government Initiatives: Proactive government policies and investments aimed at fostering digital innovation and establishing South Korea as a leading digital economy hub.

- E-Commerce and Digital Media Growth: The booming online retail sector and the increasing consumption of digital content drive demand for high-capacity and low-latency data services.

Challenges in the South Korea Data Center Market Sector

Despite robust growth, the South Korea Data Center Market faces several challenges:

- High Land and Real Estate Costs: Particularly in prime locations like Greater Seoul, the cost of acquiring land for data center development can be prohibitive.

- Stringent Environmental Regulations: Increasing focus on sustainability and energy efficiency can lead to higher compliance costs and the need for innovative, greener technologies.

- Power Availability and Grid Capacity: Securing reliable and sufficient power supply for large-scale data centers can be a bottleneck in certain areas.

- Skilled Workforce Shortage: The demand for specialized IT professionals and data center engineers is growing, leading to potential talent acquisition challenges.

- Supply Chain Disruptions: Global supply chain issues can impact the timely procurement of critical hardware and equipment.

Emerging Opportunities in South Korea Data Center Market

The South Korea Data Center Market presents significant emerging opportunities:

- Edge Computing: The increasing demand for low-latency applications in areas like autonomous vehicles, smart cities, and real-time analytics opens avenues for smaller, distributed data centers.

- Green Data Centers: Growing emphasis on sustainability creates opportunities for data center operators that can implement renewable energy solutions and achieve high energy efficiency.

- AI and High-Performance Computing (HPC): The burgeoning AI sector requires specialized data centers with high-density power and advanced cooling solutions.

- Data Sovereignty and Localization: As data privacy regulations evolve, opportunities may arise for localized data storage and processing facilities.

- Colocation Services for Emerging Technologies: Developing tailored colocation solutions for new technological demands, such as blockchain or quantum computing.

Leading Players in the South Korea Data Center Market Market

- Naver

- Lotte Data Communication

- Equinix Inc

- Telstra Corporation Limited

- LG CNS

- SK Broadband

- Digital Edge (Singapore) Holdings Pte Ltd

- Digital Realty Trust Inc

- Telehouse (KDDI Corporation)

- KINX

- KT Corporation

- Dreammark

Key Developments in South Korea Data Center Market Industry

- November 2022: A company has started the construction of its second data center, Gak Sejong Center, in Sejong City, expected to be completed by the end of 2023.

- October 2022: A strategic partnership was entered into with Zadara, an edge cloud services provider, to offer its zstorage, storage-as-a-service, to the Korean market through KINX's CloudHub.

- January 2022: A company is aiming to open two data centers, SL2x and SL3x, in Seoul, scheduled for opening by 2023 and 2024 respectively, each expected to provide an IT load capacity of 24MW.

Strategic Outlook for South Korea Data Center Market Market

The strategic outlook for the South Korea Data Center Market remains exceptionally strong, driven by continuous digital transformation, the widespread adoption of advanced technologies, and supportive government policies. Key growth catalysts include the escalating demand for hyperscale cloud services, the critical infrastructure needs for the burgeoning 5G ecosystem and edge computing deployments, and the increasing sophistication of AI and big data analytics. The market is poised for sustained expansion as both domestic and international players invest in building out capacity, focusing on energy efficiency and sustainability to meet evolving regulatory and corporate social responsibility demands. Strategic collaborations and the potential for further M&A activities will continue to shape the competitive landscape, fostering innovation and ensuring the availability of robust, reliable, and scalable data center solutions to power South Korea's digital future.

South Korea Data Center Market Segmentation

-

1. Hotspot

- 1.1. Busan

- 1.2. Greater Seoul

- 1.3. Rest of South Korea

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

5. Colocation Type

- 5.1. Hyperscale

- 5.2. Retail

- 5.3. Wholesale

-

6. End User

- 6.1. BFSI

- 6.2. Cloud

- 6.3. E-Commerce

- 6.4. Government

- 6.5. Manufacturing

- 6.6. Media & Entertainment

- 6.7. Telecom

- 6.8. Other End User

South Korea Data Center Market Segmentation By Geography

- 1. South Korea

South Korea Data Center Market Regional Market Share

Geographic Coverage of South Korea Data Center Market

South Korea Data Center Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.69% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. Busan

- 5.1.2. Greater Seoul

- 5.1.3. Rest of South Korea

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.5. Market Analysis, Insights and Forecast - by Colocation Type

- 5.5.1. Hyperscale

- 5.5.2. Retail

- 5.5.3. Wholesale

- 5.6. Market Analysis, Insights and Forecast - by End User

- 5.6.1. BFSI

- 5.6.2. Cloud

- 5.6.3. E-Commerce

- 5.6.4. Government

- 5.6.5. Manufacturing

- 5.6.6. Media & Entertainment

- 5.6.7. Telecom

- 5.6.8. Other End User

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. South Korea

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. South Korea Data Center Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Hotspot

- 6.1.1. Busan

- 6.1.2. Greater Seoul

- 6.1.3. Rest of South Korea

- 6.2. Market Analysis, Insights and Forecast - by Data Center Size

- 6.2.1. Large

- 6.2.2. Massive

- 6.2.3. Medium

- 6.2.4. Mega

- 6.2.5. Small

- 6.3. Market Analysis, Insights and Forecast - by Tier Type

- 6.3.1. Tier 1 and 2

- 6.3.2. Tier 3

- 6.3.3. Tier 4

- 6.4. Market Analysis, Insights and Forecast - by Absorption

- 6.4.1. Non-Utilized

- 6.5. Market Analysis, Insights and Forecast - by Colocation Type

- 6.5.1. Hyperscale

- 6.5.2. Retail

- 6.5.3. Wholesale

- 6.6. Market Analysis, Insights and Forecast - by End User

- 6.6.1. BFSI

- 6.6.2. Cloud

- 6.6.3. E-Commerce

- 6.6.4. Government

- 6.6.5. Manufacturing

- 6.6.6. Media & Entertainment

- 6.6.7. Telecom

- 6.6.8. Other End User

- 6.1. Market Analysis, Insights and Forecast - by Hotspot

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Naver

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Lotte Data Communication

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Equinix Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Telstra Corporation Limited5

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 LG CNS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 SK Broadband

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Digital Edge (Singapore) Holdings Pte Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Digital Realty Trust Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Telehouse (KDDI Corporation)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 KINX

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 KT Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Dreammark

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Naver

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Korea Data Center Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South Korea Data Center Market Share (%) by Company 2025

List of Tables

- Table 1: South Korea Data Center Market Revenue billion Forecast, by Hotspot 2020 & 2033

- Table 2: South Korea Data Center Market Volume K Unit Forecast, by Hotspot 2020 & 2033

- Table 3: South Korea Data Center Market Revenue billion Forecast, by Data Center Size 2020 & 2033

- Table 4: South Korea Data Center Market Volume K Unit Forecast, by Data Center Size 2020 & 2033

- Table 5: South Korea Data Center Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 6: South Korea Data Center Market Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 7: South Korea Data Center Market Revenue billion Forecast, by Absorption 2020 & 2033

- Table 8: South Korea Data Center Market Volume K Unit Forecast, by Absorption 2020 & 2033

- Table 9: South Korea Data Center Market Revenue billion Forecast, by Colocation Type 2020 & 2033

- Table 10: South Korea Data Center Market Volume K Unit Forecast, by Colocation Type 2020 & 2033

- Table 11: South Korea Data Center Market Revenue billion Forecast, by End User 2020 & 2033

- Table 12: South Korea Data Center Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 13: South Korea Data Center Market Revenue billion Forecast, by Region 2020 & 2033

- Table 14: South Korea Data Center Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 15: South Korea Data Center Market Revenue billion Forecast, by Hotspot 2020 & 2033

- Table 16: South Korea Data Center Market Volume K Unit Forecast, by Hotspot 2020 & 2033

- Table 17: South Korea Data Center Market Revenue billion Forecast, by Data Center Size 2020 & 2033

- Table 18: South Korea Data Center Market Volume K Unit Forecast, by Data Center Size 2020 & 2033

- Table 19: South Korea Data Center Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 20: South Korea Data Center Market Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 21: South Korea Data Center Market Revenue billion Forecast, by Absorption 2020 & 2033

- Table 22: South Korea Data Center Market Volume K Unit Forecast, by Absorption 2020 & 2033

- Table 23: South Korea Data Center Market Revenue billion Forecast, by Colocation Type 2020 & 2033

- Table 24: South Korea Data Center Market Volume K Unit Forecast, by Colocation Type 2020 & 2033

- Table 25: South Korea Data Center Market Revenue billion Forecast, by End User 2020 & 2033

- Table 26: South Korea Data Center Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 27: South Korea Data Center Market Revenue billion Forecast, by Country 2020 & 2033

- Table 28: South Korea Data Center Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Korea Data Center Market?

The projected CAGR is approximately 8.69%.

2. Which companies are prominent players in the South Korea Data Center Market?

Key companies in the market include Naver, Lotte Data Communication, Equinix Inc, Telstra Corporation Limited5 , LG CNS, SK Broadband, Digital Edge (Singapore) Holdings Pte Ltd, Digital Realty Trust Inc, Telehouse (KDDI Corporation), KINX, KT Corporation, Dreammark.

3. What are the main segments of the South Korea Data Center Market?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption, Colocation Type, End User .

4. Can you provide details about the market size?

The market size is estimated to be USD 4.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Awareness of Energy Consumption Control.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

High Risk Associated with Data.

8. Can you provide examples of recent developments in the market?

November 2022: The company has started the construction of its second data center, Gak Sejong Center, which is built in Sejong City. It is expected to be completed by the end of 2023.October 2022: The company entered into a strategic partnership with Zadara, an edge cloud services provider, to provide its zstorage, storage-as-a-service, to the Korean market through KINX's CloudHub.January 2022: The company is aiming to open two data centers, SL2x and SL3x, in Seoul which are scheduled to open by 2023 and 2024 respectively. Both of the data centers are expected to provide an IT load capacity of 24MW each.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Korea Data Center Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Korea Data Center Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Korea Data Center Market?

To stay informed about further developments, trends, and reports in the South Korea Data Center Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence