Key Insights

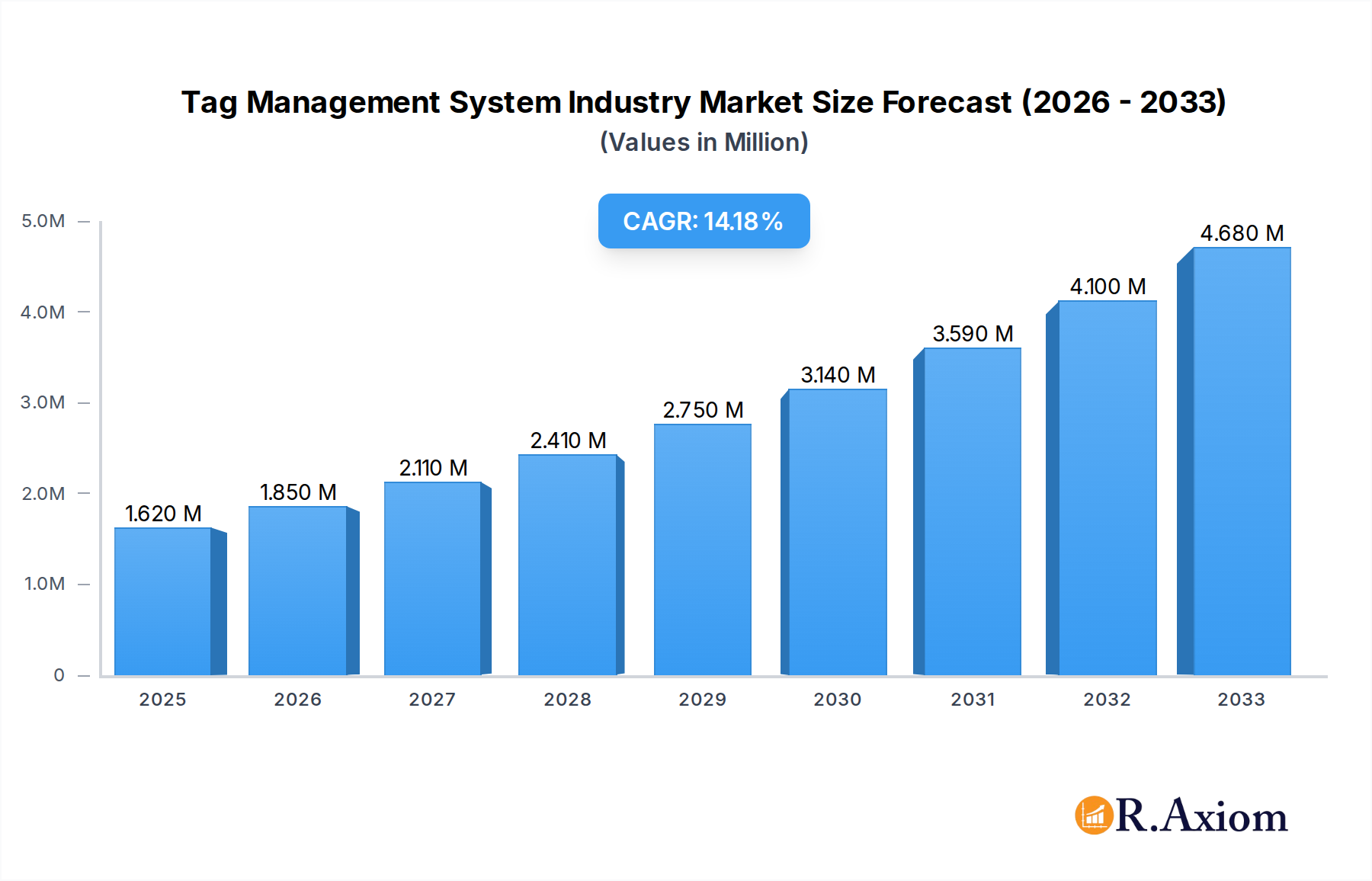

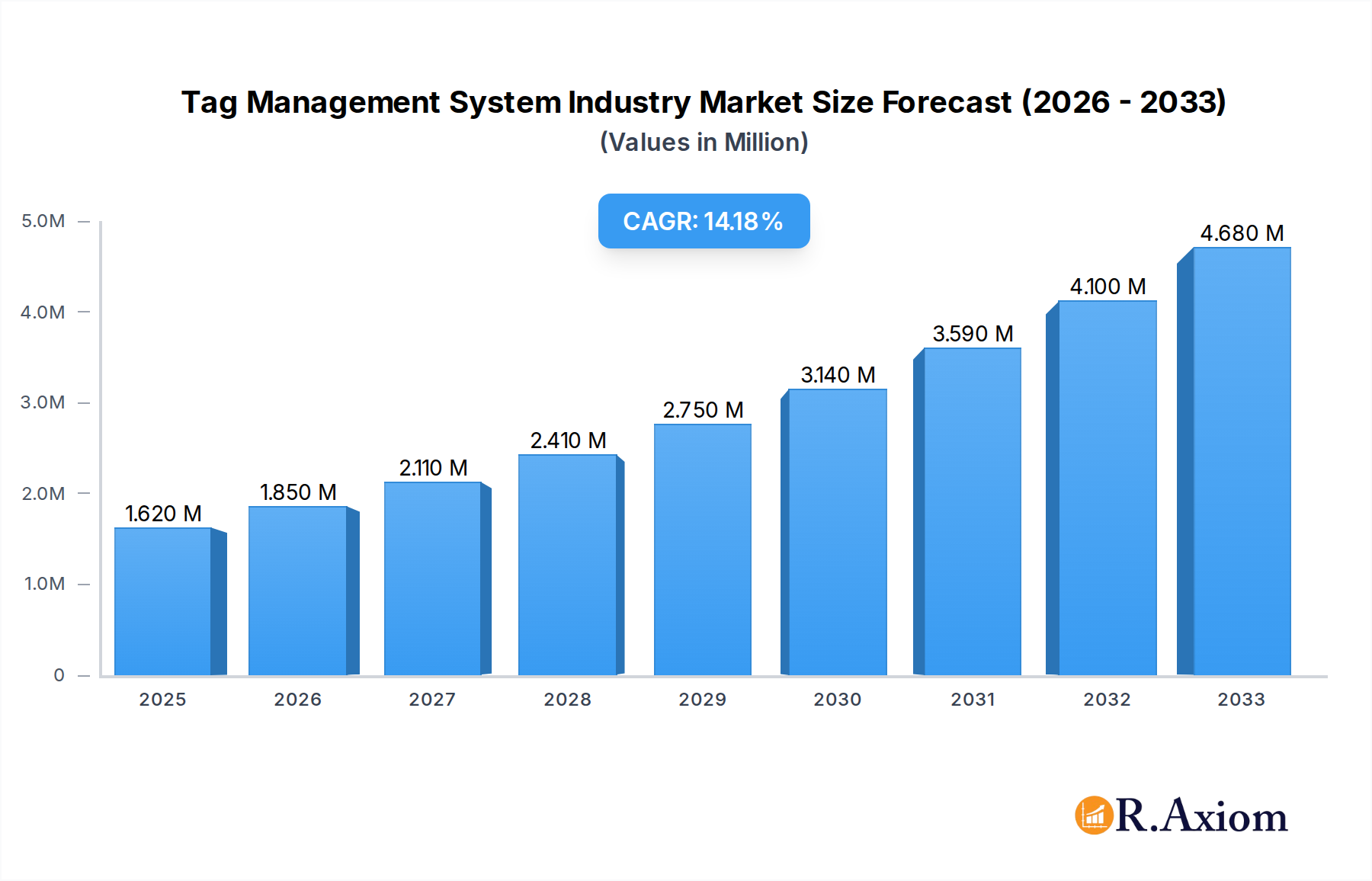

The Tag Management System (TMS) market is poised for robust expansion, projected to reach $1.62 million by 2025 and sustain a significant Compound Annual Growth Rate (CAGR) of 14.05% through 2033. This impressive growth is primarily fueled by the escalating need for efficient digital data collection, analysis, and activation across various industries. Key drivers include the increasing complexity of the digital marketing landscape, the imperative for enhanced website performance and user experience, and the growing importance of data privacy regulations. Businesses are increasingly adopting TMS solutions to streamline the deployment and management of marketing and analytics tags, thereby reducing manual intervention, minimizing errors, and accelerating time-to-market for new campaigns and tracking initiatives. The shift towards cloud-based deployment models is also a dominant trend, offering greater scalability, flexibility, and cost-effectiveness compared to on-premises solutions.

Tag Management System Industry Market Size (In Million)

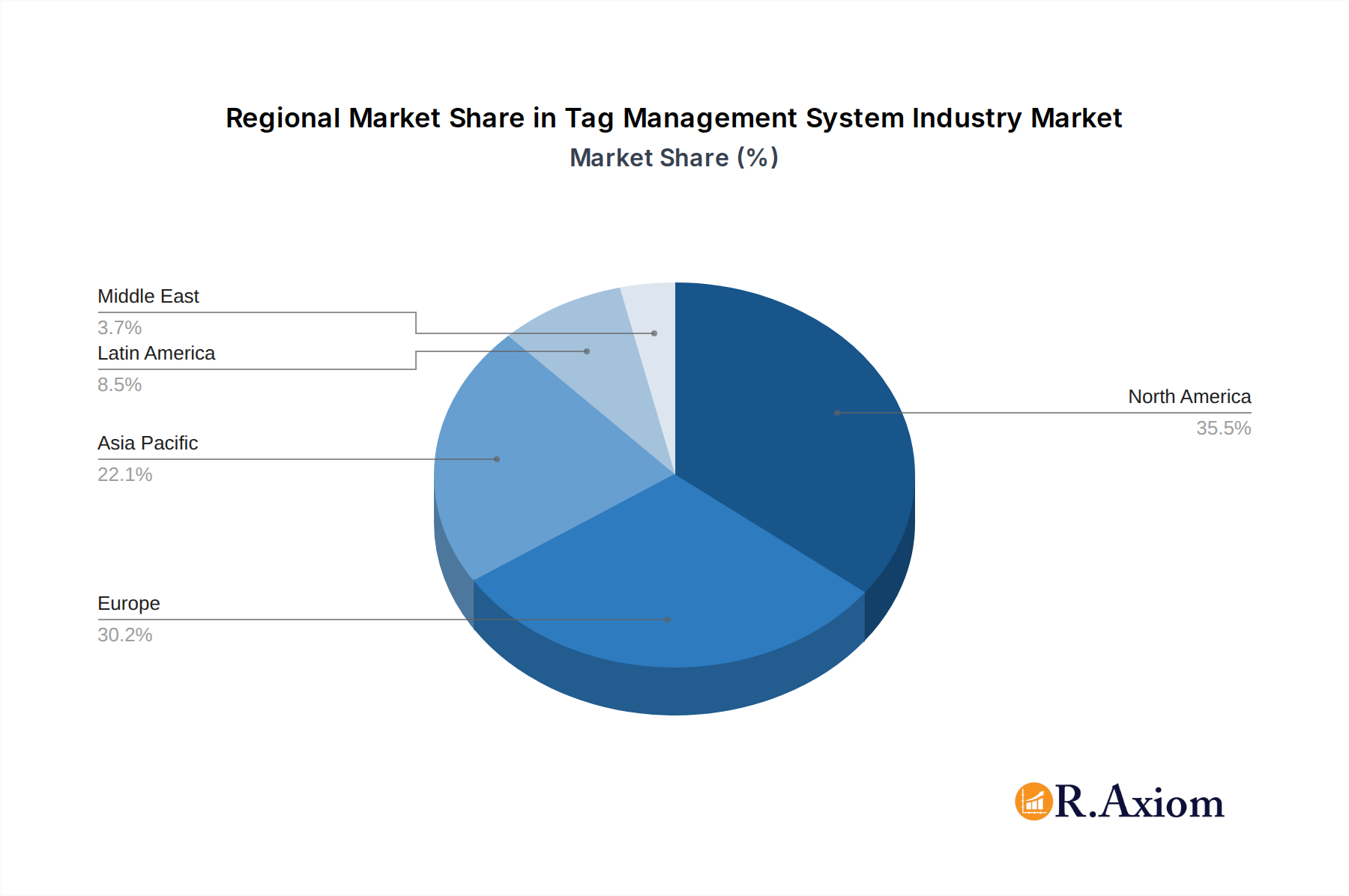

The TMS market segmentation by application highlights the widespread adoption in Campaign Management, Content Management, and Compliance Management, reflecting the critical role these systems play in optimizing marketing efforts, personalizing customer experiences, and ensuring adherence to data privacy laws. The BFSI, Retail & E-commerce, and Healthcare sectors are emerging as significant end-users, driven by their heavy reliance on digital channels and vast amounts of customer data. While the market benefits from strong growth drivers, it faces certain restraints such as the initial cost of implementation for smaller businesses and the potential for vendor lock-in. However, ongoing technological advancements, such as AI-powered tag management and enhanced integration capabilities, are expected to further bolster market growth and adoption rates globally, with North America and Europe leading the charge in market share, followed closely by the rapidly growing Asia Pacific region.

Tag Management System Industry Company Market Share

Here's the SEO-optimized and detailed report description for the Tag Management System Industry, structured as requested:

Tag Management System Industry Market Concentration & Innovation

The global Tag Management System (TMS) industry exhibits a moderate to high level of market concentration, with a handful of major players dominating a significant portion of the market share. Companies like Adobe Inc., Google Inc., and Oracle Corporation leverage their extensive product ecosystems and established customer bases to maintain a strong presence. However, the market also fosters innovation through specialized players such as Qubit Digital Ltd, Tealium Inc., and Ensighten Inc., who offer advanced features and niche solutions. The primary innovation drivers include the increasing demand for data privacy compliance (e.g., GDPR, CCPA), the need for streamlined digital marketing campaign execution, and the continuous evolution of web and mobile technologies. Regulatory frameworks play a crucial role, pushing for greater transparency and control over data collection and usage, thereby stimulating the development of sophisticated tag governance features within TMS. Product substitutes, such as custom-coded tag implementations, are gradually being phased out due to their complexity and lack of scalability compared to dedicated TMS solutions. End-user trends indicate a growing adoption across all sectors, with particular emphasis on industries managing large volumes of customer data and complex marketing efforts. Merger and acquisition (M&A) activities are prevalent, seen in various significant deals valued in the hundreds of millions to billions of dollars, as larger enterprises seek to acquire innovative technologies and expand their market reach. For instance, strategic acquisitions by major cloud providers aim to integrate TMS capabilities into their broader digital transformation suites.

Tag Management System Industry Industry Trends & Insights

The Tag Management System industry is experiencing robust growth driven by several key trends. The escalating importance of data-driven decision-making across all business functions necessitates efficient and centralized tag management. This is fueling the adoption of sophisticated TMS solutions that enable marketers and data analysts to deploy, manage, and govern website tags and third-party scripts seamlessly. The projected Compound Annual Growth Rate (CAGR) for the TMS market is anticipated to be substantial, estimated to be in the double digits, reflecting its critical role in modern digital strategies. Market penetration is steadily increasing, particularly among small and medium-sized businesses (SMBs) who are recognizing the value of simplified tag deployment and improved website performance. Technological disruptions, such as the deprecation of third-party cookies, are prompting a shift towards first-party data strategies, where TMS plays a pivotal role in collecting and managing this valuable information. Furthermore, the increasing complexity of the digital landscape, with the proliferation of websites, mobile apps, and various marketing technologies, demands a unified approach to tag implementation, which TMS provides. Consumer preferences for personalized experiences and enhanced data privacy are also influencing the market, pushing businesses to adopt TMS solutions that offer granular control over data collection and consent management. Competitive dynamics are characterized by intense innovation, with established players continuously enhancing their platforms with features like AI-powered tag optimization, advanced analytics, and robust compliance tools. The integration of TMS with other marketing and analytics platforms is a key differentiator, offering end-to-end solutions for campaign management, customer journey mapping, and performance measurement. The continuous evolution of regulatory requirements worldwide further solidifies the need for reliable and compliant tag management, driving ongoing market expansion. The increasing focus on data governance and security is pushing organizations to invest in TMS solutions that offer robust access controls and audit trails.

Dominant Markets & Segments in Tag Management System Industry

The Cloud deployment segment is demonstrably dominant within the Tag Management System industry, with an estimated market size projected to reach several billion dollars by 2033. This dominance is driven by the inherent scalability, flexibility, and cost-effectiveness of cloud-based solutions, catering to businesses of all sizes. The Retail & E-commerce end-user segment also stands out as a leading adopter, contributing significantly to the market's expansion. This is primarily due to the high volume of online transactions, the critical need for conversion tracking, personalized marketing campaigns, and robust customer data management in this sector. The Campaign Management application segment further underscores the market's focus, as TMS solutions are instrumental in deploying and managing marketing tags for advertising, analytics, and A/B testing, directly impacting campaign performance and ROI.

Key drivers for cloud adoption include:

- Scalability: Cloud TMS can effortlessly scale to accommodate fluctuating website traffic and an increasing number of tags.

- Accessibility: Remote access and collaboration features facilitate seamless management across distributed teams.

- Reduced Infrastructure Costs: Eliminates the need for on-premises hardware and maintenance.

- Faster Deployment: Quicker implementation and updates compared to on-premises solutions.

The dominance of Retail & E-commerce is fueled by:

- Conversion Optimization: Real-time tracking of sales, cart abandonment, and user behavior for performance enhancement.

- Personalized Marketing: Enabling targeted advertising and personalized website experiences based on customer data.

- Customer Journey Analytics: Providing insights into customer interactions across various touchpoints.

- Competitive Pressure: The need to stay ahead in a highly competitive online marketplace.

Campaign Management's leading position is attributed to:

- Efficient Tag Deployment: Streamlining the process of adding and updating tags for various marketing channels.

- Performance Measurement: Enabling accurate tracking of campaign effectiveness and ROI.

- A/B Testing: Facilitating experimentation with different marketing strategies and website variations.

- Data Integration: Seamlessly integrating tag data with analytics and advertising platforms.

The BFSI (Banking, Financial Services, and Insurance) sector is also a significant and growing market, driven by stringent regulatory compliance requirements and the need for secure customer data management. The Healthcare industry's adoption is rising due to the increasing digitization of patient data and the need for compliance with privacy regulations like HIPAA. The On-premises deployment type, while less dominant than cloud, still holds a considerable market share, particularly within large enterprises with strict data security policies or legacy IT infrastructures. Compliance Management as an application is gaining traction across all end-users, as global data privacy regulations become more pervasive, necessitating robust tag governance.

Tag Management System Industry Product Developments

Product innovations in the Tag Management System industry are focused on enhancing efficiency, compliance, and data utilization. Leading companies are developing AI-powered tag optimization tools to automatically identify redundant or underperforming tags, improving website performance and reducing data waste. Advanced features for consent management are becoming standard, ensuring adherence to evolving privacy regulations like GDPR and CCPA. Competitive advantages are being carved out through seamless integration with broader marketing technology stacks, providing end-to-end data solutions. The trend towards server-side tagging is gaining momentum, offering improved speed, security, and control over data collection, addressing limitations of traditional client-side implementations. These developments cater to the growing demand for precise data governance and improved user experiences.

Report Scope & Segmentation Analysis

This report delves into the global Tag Management System Industry, segmenting the market comprehensively to provide granular insights. The Deployment Type segmentation includes Cloud and On-premises solutions, analyzing market penetration and growth projections for each. The Application segmentation encompasses Campaign Management, Content Management, Compliance Management, and Other Applications, detailing their respective market sizes and competitive dynamics. Further segmentation by End-User includes critical sectors such as BFSI, Retail & E-commerce, Healthcare, Manufacturing, and Other End-Users, with specific growth forecasts and market share analysis for each. The competitive landscape within each segment is thoroughly examined, highlighting the key players and their strategic positioning.

Key Drivers of Tag Management System Industry Growth

The Tag Management System industry's growth is propelled by several pivotal factors.

- Digital Transformation Initiatives: Businesses worldwide are investing heavily in digital transformation, requiring robust tools for managing their online presence and data.

- Data Privacy Regulations: Stringent regulations like GDPR, CCPA, and LGPD mandate greater control and transparency over data collection, driving demand for compliance-focused TMS solutions.

- Evolving Marketing Strategies: The shift towards personalized marketing, omnichannel experiences, and data-driven decision-making necessitates efficient tag management for analytics and campaign execution.

- Third-Party Cookie Deprecation: The phasing out of third-party cookies is forcing organizations to focus on first-party data collection and management, where TMS plays a crucial role.

- Technological Advancements: Innovations such as server-side tagging and AI-driven optimization enhance the capabilities and appeal of TMS.

Challenges in the Tag Management System Industry Sector

Despite strong growth prospects, the Tag Management System industry faces several challenges.

- Regulatory Complexity: Keeping pace with evolving and fragmented global data privacy regulations presents a significant compliance hurdle.

- Technical Integration Issues: Ensuring seamless integration with diverse and often legacy technology stacks can be complex and resource-intensive.

- Talent Shortage: A lack of skilled professionals capable of effectively managing and optimizing TMS platforms can hinder adoption and ROI.

- Data Security Concerns: While TMS aims to improve data governance, breaches and misuse of data remain a critical concern for businesses and users.

- Market Saturation and Differentiation: With numerous providers, differentiating offerings and demonstrating unique value propositions can be challenging.

Emerging Opportunities in Tag Management System Industry

Emerging opportunities within the Tag Management System industry are abundant, driven by innovation and evolving market needs.

- Server-Side Tagging: The growing adoption of server-side tagging presents a significant opportunity for enhanced data control, speed, and privacy, moving beyond traditional client-side limitations.

- AI and Machine Learning Integration: Leveraging AI and ML for automated tag optimization, predictive analytics, and personalized customer experiences opens new revenue streams.

- Growth in Emerging Markets: The increasing digital adoption in developing economies offers substantial untapped potential for TMS solutions.

- Focus on First-Party Data: As third-party cookies decline, TMS platforms that facilitate robust first-party data collection and activation will be highly sought after.

- Integration with Data Warehousing and CDP: Deeper integrations with Customer Data Platforms (CDPs) and data warehouses can unlock advanced analytics and marketing automation capabilities.

Leading Players in the Tag Management System Industry Market

- Qubit Digital Ltd

- Tealium Inc

- Fjord Technologies S A S

- IBM Corporation

- Piwik Pro Sp z o o

- Yottaa Inc

- Hub'Scan Inc

- Datalicious Pty Ltd

- Adobe Inc

- Oracle Corporation

- OpenX Software Ltd

- Ensighten Inc

- Google Inc

- Signal Group Inc

Key Developments in Tag Management System Industry Industry

- September 2023: Atlan launched Tag Management, a new way for data teams to manage data access across the modern data stack. Tags are essential metadata that can be assigned to data assets to monitor sensitive data for discovery, compliance, and protection use cases. With the launch of Tag Management, Atlan enables bi-directional tag movement in and out of Atlan. This means data teams can start using Atlan as the control plane for tags, ensuring that data assets in Atlan are tagged and protected everywhere in the data ecosystem.

- March 2022: Mouse Flow and Google Tag jointly developed Tag Management Software for E-commerce companies, where users can integrate the shopping cart value into a Mouseflow recording variable to monitor further the value of conversions and the possible loss of sales. This will enable the retailer to fix the problems that are costing money.

Strategic Outlook for Tag Management System Industry Market

The strategic outlook for the Tag Management System industry is highly positive, characterized by continuous innovation and expanding market relevance. The ongoing digital transformation across all sectors, coupled with the increasing stringency of global data privacy regulations, will continue to drive the demand for comprehensive TMS solutions. The anticipated deprecation of third-party cookies further solidifies the importance of robust tag management for first-party data strategies. Emerging technologies like server-side tagging and AI-driven optimization are poised to redefine the capabilities of TMS platforms, offering enhanced performance, security, and personalization. Strategic collaborations and acquisitions are expected to shape the competitive landscape, as larger players seek to consolidate their offerings and specialized providers focus on niche innovations. The market's future lies in its ability to provide integrated, compliant, and data-empowering solutions that address the complex needs of modern digital businesses.

Tag Management System Industry Segmentation

-

1. Deployment Type

- 1.1. Cloud

- 1.2. On-premises

-

2. Application

- 2.1. Campaign Management

- 2.2. Content Management

- 2.3. Compliance Management

- 2.4. Other Applications

-

3. End-User

- 3.1. BFSI

- 3.2. Retail & E-commerce

- 3.3. Healthcare

- 3.4. Manufacturing

- 3.5. Other End-Users

Tag Management System Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. Japan

- 3.2. India

- 3.3. Rest of Asia Pacific

-

4. Latin America

- 4.1. Mexico

- 4.2. Brazil

- 4.3. Rest of Latin America

- 5. Middle East

Tag Management System Industry Regional Market Share

Geographic Coverage of Tag Management System Industry

Tag Management System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.05% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 5.1.1. Cloud

- 5.1.2. On-premises

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Campaign Management

- 5.2.2. Content Management

- 5.2.3. Compliance Management

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. BFSI

- 5.3.2. Retail & E-commerce

- 5.3.3. Healthcare

- 5.3.4. Manufacturing

- 5.3.5. Other End-Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6. Global Tag Management System Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6.1.1. Cloud

- 6.1.2. On-premises

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Campaign Management

- 6.2.2. Content Management

- 6.2.3. Compliance Management

- 6.2.4. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. BFSI

- 6.3.2. Retail & E-commerce

- 6.3.3. Healthcare

- 6.3.4. Manufacturing

- 6.3.5. Other End-Users

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7. North America Tag Management System Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7.1.1. Cloud

- 7.1.2. On-premises

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Campaign Management

- 7.2.2. Content Management

- 7.2.3. Compliance Management

- 7.2.4. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End-User

- 7.3.1. BFSI

- 7.3.2. Retail & E-commerce

- 7.3.3. Healthcare

- 7.3.4. Manufacturing

- 7.3.5. Other End-Users

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8. Europe Tag Management System Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8.1.1. Cloud

- 8.1.2. On-premises

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Campaign Management

- 8.2.2. Content Management

- 8.2.3. Compliance Management

- 8.2.4. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End-User

- 8.3.1. BFSI

- 8.3.2. Retail & E-commerce

- 8.3.3. Healthcare

- 8.3.4. Manufacturing

- 8.3.5. Other End-Users

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9. Asia Pacific Tag Management System Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9.1.1. Cloud

- 9.1.2. On-premises

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Campaign Management

- 9.2.2. Content Management

- 9.2.3. Compliance Management

- 9.2.4. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End-User

- 9.3.1. BFSI

- 9.3.2. Retail & E-commerce

- 9.3.3. Healthcare

- 9.3.4. Manufacturing

- 9.3.5. Other End-Users

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10. Latin America Tag Management System Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10.1.1. Cloud

- 10.1.2. On-premises

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Campaign Management

- 10.2.2. Content Management

- 10.2.3. Compliance Management

- 10.2.4. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End-User

- 10.3.1. BFSI

- 10.3.2. Retail & E-commerce

- 10.3.3. Healthcare

- 10.3.4. Manufacturing

- 10.3.5. Other End-Users

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11. Middle East Tag Management System Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11.1.1. Cloud

- 11.1.2. On-premises

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Campaign Management

- 11.2.2. Content Management

- 11.2.3. Compliance Management

- 11.2.4. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by End-User

- 11.3.1. BFSI

- 11.3.2. Retail & E-commerce

- 11.3.3. Healthcare

- 11.3.4. Manufacturing

- 11.3.5. Other End-Users

- 11.1. Market Analysis, Insights and Forecast - by Deployment Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Qubit Digital Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Tealium Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Fjord Technologies S A S

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 IBM Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Piwik Pro Sp z o o

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Yottaa Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hub'Scan Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Datalicious Pty Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Adobe Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Oracle Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 OpenX Software Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ensighten Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Google Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Signal Group Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Qubit Digital Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Tag Management System Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Tag Management System Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Tag Management System Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 4: North America Tag Management System Industry Volume (K Unit), by Deployment Type 2025 & 2033

- Figure 5: North America Tag Management System Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 6: North America Tag Management System Industry Volume Share (%), by Deployment Type 2025 & 2033

- Figure 7: North America Tag Management System Industry Revenue (Million), by Application 2025 & 2033

- Figure 8: North America Tag Management System Industry Volume (K Unit), by Application 2025 & 2033

- Figure 9: North America Tag Management System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Tag Management System Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: North America Tag Management System Industry Revenue (Million), by End-User 2025 & 2033

- Figure 12: North America Tag Management System Industry Volume (K Unit), by End-User 2025 & 2033

- Figure 13: North America Tag Management System Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 14: North America Tag Management System Industry Volume Share (%), by End-User 2025 & 2033

- Figure 15: North America Tag Management System Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Tag Management System Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Tag Management System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Tag Management System Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Tag Management System Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 20: Europe Tag Management System Industry Volume (K Unit), by Deployment Type 2025 & 2033

- Figure 21: Europe Tag Management System Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 22: Europe Tag Management System Industry Volume Share (%), by Deployment Type 2025 & 2033

- Figure 23: Europe Tag Management System Industry Revenue (Million), by Application 2025 & 2033

- Figure 24: Europe Tag Management System Industry Volume (K Unit), by Application 2025 & 2033

- Figure 25: Europe Tag Management System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 26: Europe Tag Management System Industry Volume Share (%), by Application 2025 & 2033

- Figure 27: Europe Tag Management System Industry Revenue (Million), by End-User 2025 & 2033

- Figure 28: Europe Tag Management System Industry Volume (K Unit), by End-User 2025 & 2033

- Figure 29: Europe Tag Management System Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 30: Europe Tag Management System Industry Volume Share (%), by End-User 2025 & 2033

- Figure 31: Europe Tag Management System Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Tag Management System Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Tag Management System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Tag Management System Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Tag Management System Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 36: Asia Pacific Tag Management System Industry Volume (K Unit), by Deployment Type 2025 & 2033

- Figure 37: Asia Pacific Tag Management System Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 38: Asia Pacific Tag Management System Industry Volume Share (%), by Deployment Type 2025 & 2033

- Figure 39: Asia Pacific Tag Management System Industry Revenue (Million), by Application 2025 & 2033

- Figure 40: Asia Pacific Tag Management System Industry Volume (K Unit), by Application 2025 & 2033

- Figure 41: Asia Pacific Tag Management System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 42: Asia Pacific Tag Management System Industry Volume Share (%), by Application 2025 & 2033

- Figure 43: Asia Pacific Tag Management System Industry Revenue (Million), by End-User 2025 & 2033

- Figure 44: Asia Pacific Tag Management System Industry Volume (K Unit), by End-User 2025 & 2033

- Figure 45: Asia Pacific Tag Management System Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 46: Asia Pacific Tag Management System Industry Volume Share (%), by End-User 2025 & 2033

- Figure 47: Asia Pacific Tag Management System Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Tag Management System Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Tag Management System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Tag Management System Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Latin America Tag Management System Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 52: Latin America Tag Management System Industry Volume (K Unit), by Deployment Type 2025 & 2033

- Figure 53: Latin America Tag Management System Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 54: Latin America Tag Management System Industry Volume Share (%), by Deployment Type 2025 & 2033

- Figure 55: Latin America Tag Management System Industry Revenue (Million), by Application 2025 & 2033

- Figure 56: Latin America Tag Management System Industry Volume (K Unit), by Application 2025 & 2033

- Figure 57: Latin America Tag Management System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Latin America Tag Management System Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Latin America Tag Management System Industry Revenue (Million), by End-User 2025 & 2033

- Figure 60: Latin America Tag Management System Industry Volume (K Unit), by End-User 2025 & 2033

- Figure 61: Latin America Tag Management System Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 62: Latin America Tag Management System Industry Volume Share (%), by End-User 2025 & 2033

- Figure 63: Latin America Tag Management System Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Latin America Tag Management System Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Latin America Tag Management System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Latin America Tag Management System Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: Middle East Tag Management System Industry Revenue (Million), by Deployment Type 2025 & 2033

- Figure 68: Middle East Tag Management System Industry Volume (K Unit), by Deployment Type 2025 & 2033

- Figure 69: Middle East Tag Management System Industry Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 70: Middle East Tag Management System Industry Volume Share (%), by Deployment Type 2025 & 2033

- Figure 71: Middle East Tag Management System Industry Revenue (Million), by Application 2025 & 2033

- Figure 72: Middle East Tag Management System Industry Volume (K Unit), by Application 2025 & 2033

- Figure 73: Middle East Tag Management System Industry Revenue Share (%), by Application 2025 & 2033

- Figure 74: Middle East Tag Management System Industry Volume Share (%), by Application 2025 & 2033

- Figure 75: Middle East Tag Management System Industry Revenue (Million), by End-User 2025 & 2033

- Figure 76: Middle East Tag Management System Industry Volume (K Unit), by End-User 2025 & 2033

- Figure 77: Middle East Tag Management System Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 78: Middle East Tag Management System Industry Volume Share (%), by End-User 2025 & 2033

- Figure 79: Middle East Tag Management System Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: Middle East Tag Management System Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: Middle East Tag Management System Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East Tag Management System Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Tag Management System Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 2: Global Tag Management System Industry Volume K Unit Forecast, by Deployment Type 2020 & 2033

- Table 3: Global Tag Management System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Tag Management System Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Global Tag Management System Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Global Tag Management System Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 7: Global Tag Management System Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Tag Management System Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Tag Management System Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 10: Global Tag Management System Industry Volume K Unit Forecast, by Deployment Type 2020 & 2033

- Table 11: Global Tag Management System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Tag Management System Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 13: Global Tag Management System Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 14: Global Tag Management System Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 15: Global Tag Management System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Tag Management System Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Global Tag Management System Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 22: Global Tag Management System Industry Volume K Unit Forecast, by Deployment Type 2020 & 2033

- Table 23: Global Tag Management System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Tag Management System Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 25: Global Tag Management System Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 26: Global Tag Management System Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 27: Global Tag Management System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: Global Tag Management System Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 29: United Kingdom Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: United Kingdom Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Germany Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: France Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: France Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Tag Management System Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 38: Global Tag Management System Industry Volume K Unit Forecast, by Deployment Type 2020 & 2033

- Table 39: Global Tag Management System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Tag Management System Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Global Tag Management System Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 42: Global Tag Management System Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 43: Global Tag Management System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 44: Global Tag Management System Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 45: Japan Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Japan Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: India Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Rest of Asia Pacific Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Rest of Asia Pacific Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: Global Tag Management System Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 52: Global Tag Management System Industry Volume K Unit Forecast, by Deployment Type 2020 & 2033

- Table 53: Global Tag Management System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 54: Global Tag Management System Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 55: Global Tag Management System Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 56: Global Tag Management System Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 57: Global Tag Management System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 58: Global Tag Management System Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 59: Mexico Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Mexico Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Brazil Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Brazil Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Rest of Latin America Tag Management System Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Rest of Latin America Tag Management System Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Global Tag Management System Industry Revenue Million Forecast, by Deployment Type 2020 & 2033

- Table 66: Global Tag Management System Industry Volume K Unit Forecast, by Deployment Type 2020 & 2033

- Table 67: Global Tag Management System Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 68: Global Tag Management System Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Global Tag Management System Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 70: Global Tag Management System Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 71: Global Tag Management System Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 72: Global Tag Management System Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Tag Management System Industry?

The projected CAGR is approximately 14.05%.

2. Which companies are prominent players in the Tag Management System Industry?

Key companies in the market include Qubit Digital Ltd, Tealium Inc, Fjord Technologies S A S, IBM Corporation, Piwik Pro Sp z o o, Yottaa Inc, Hub'Scan Inc, Datalicious Pty Ltd, Adobe Inc, Oracle Corporation, OpenX Software Ltd, Ensighten Inc, Google Inc, Signal Group Inc.

3. What are the main segments of the Tag Management System Industry?

The market segments include Deployment Type, Application, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.62 Million as of 2022.

5. What are some drivers contributing to market growth?

User-friendly and Feature-packed Software; Better Customer Experience Deliverance; Ability to Build a Unified Ecosystem.

6. What are the notable trends driving market growth?

Tag Management Systems to Play a Significant Role in Retail and E-commerce Sector.

7. Are there any restraints impacting market growth?

High Initial Fee for Tag Management Systems.

8. Can you provide examples of recent developments in the market?

September 2023 : Atlan launched Tag Management, a new way for data teams to manage data access across the modern data stack. Tags are essential metadata that can be assigned to data assets to monitor sensitive data for discovery, compliance, and protection use cases. With the launch of Tag Management, Atlan enables bi-directional tag movement in and out of Atlan. This means data teams can start using Atlan as the control plane for tags, ensuring that data assets in Atlan are tagged and protected everywhere in the data ecosystem.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Tag Management System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Tag Management System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Tag Management System Industry?

To stay informed about further developments, trends, and reports in the Tag Management System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence