Key Insights

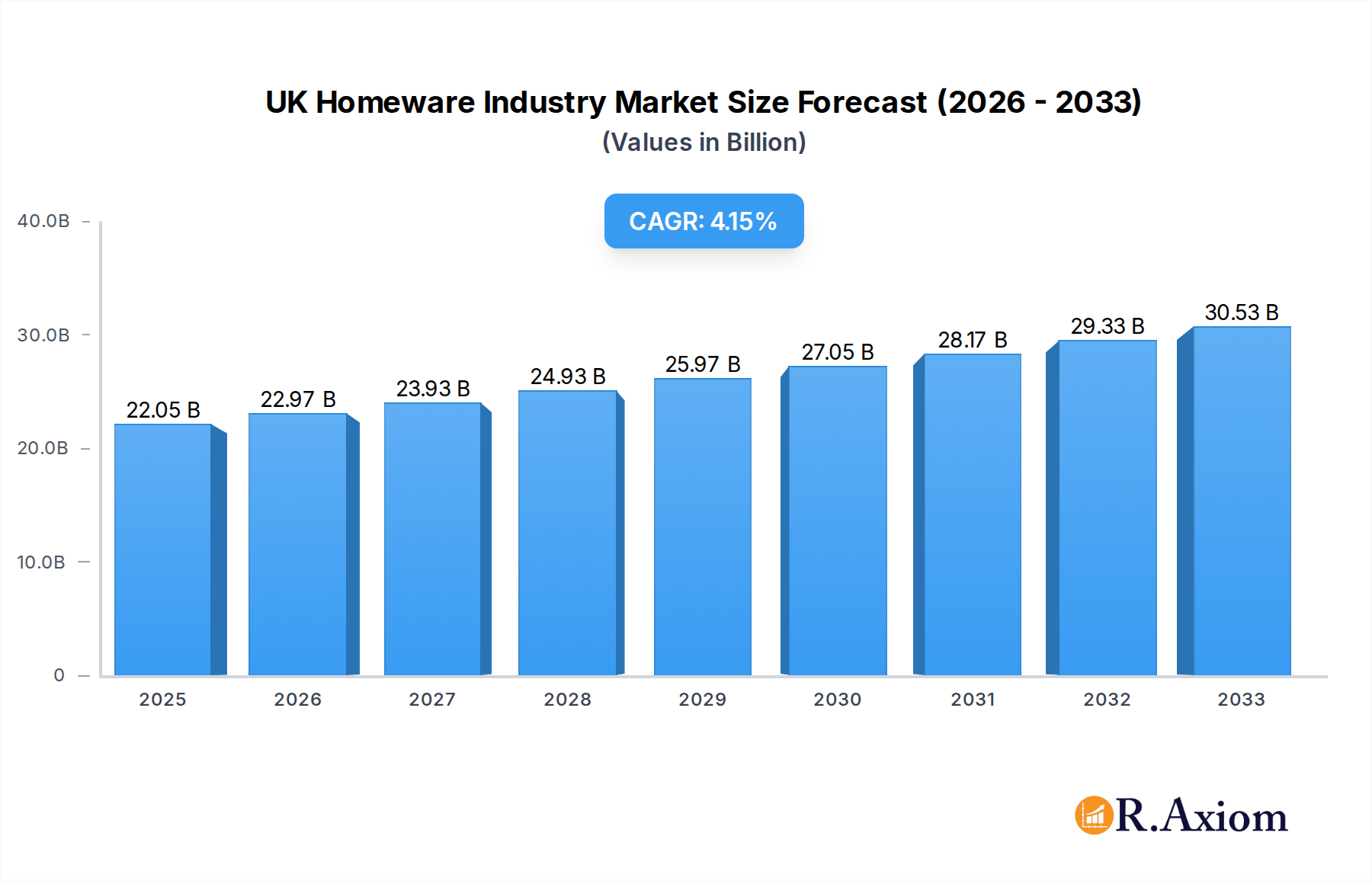

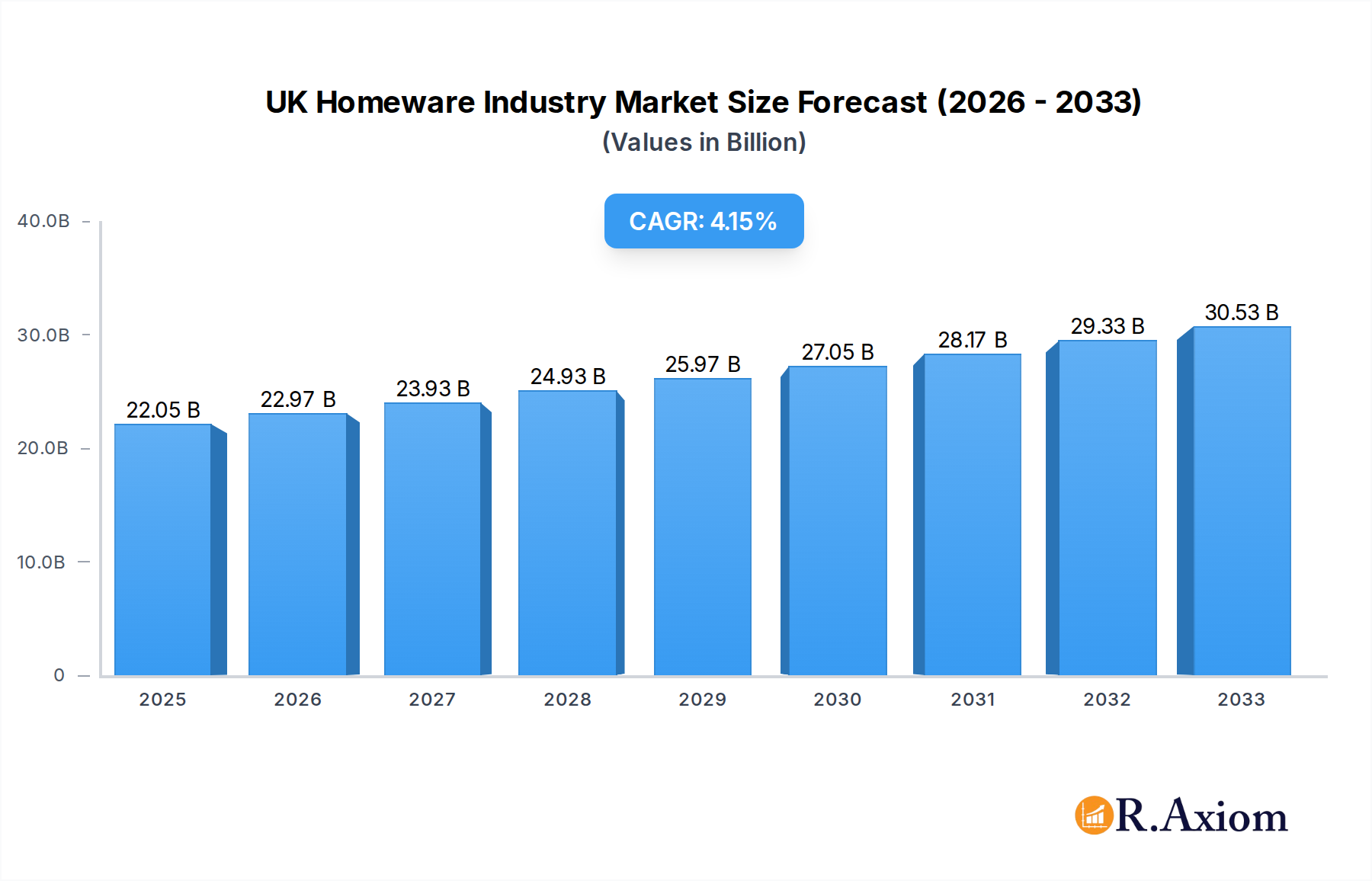

The UK homeware industry is poised for robust expansion, driven by evolving consumer lifestyles and a growing emphasis on home aesthetics and functionality. With a current market size of £21.20 million, the sector is projected to experience a Compound Annual Growth Rate (CAGR) of 4.17% over the forecast period. This sustained growth is underpinned by several key drivers. A significant factor is the increasing disposable income among UK households, allowing for greater investment in home furnishings and improvements. Furthermore, the ongoing trend of home renovations and interior design upgrades, fueled by social media influence and a desire for personalized living spaces, continues to stimulate demand. The pandemic's legacy of increased time spent at home has also cemented a focus on creating comfortable and stylish environments, directly benefiting the homeware market. Emerging trends such as the rise of sustainable and eco-friendly homeware products, smart home integration, and the demand for multi-functional furniture are further shaping consumer preferences and creating new avenues for market growth.

UK Homeware Industry Market Size (In Billion)

While the overall outlook is positive, certain restraints may influence the pace of growth. Economic uncertainties and inflationary pressures could impact consumer spending on non-essential items. However, the market's resilience is evident in its segmentation. The "Home Furniture" and "Home Appliances" segments are expected to remain dominant, supported by consistent demand for essential and upgrade purchases. The "Online Distribution Channels" are witnessing substantial growth, reflecting a shift in consumer purchasing behavior towards e-commerce convenience, a trend further amplified by leading online retailers and established brands expanding their digital presence. Geographically, the UK, as a key market within Europe, is a significant contributor, with strong performance also anticipated from North America and the Asia Pacific regions, driven by their respective economic strengths and consumer spending habits.

UK Homeware Industry Company Market Share

Here is a comprehensive, SEO-optimized report description for the UK Homeware Industry:

Title: UK Homeware Industry Market Outlook 2025-2033: Growth Drivers, Trends, Innovations & Competitive Landscape

Meta Description: Deep dive into the UK Homeware Industry with market size forecasts, key trends, product segment analysis, and leading players like IKEA, Bosch, and Dyson. Explore opportunities and challenges for the 2025-2033 forecast period.

UK Homeware Industry Market Concentration & Innovation

The UK Homeware Industry is characterized by a moderate level of market concentration, with a few dominant players influencing market dynamics alongside a vibrant landscape of smaller, specialized businesses. Innovation remains a critical driver, fueled by technological advancements in product design, sustainable manufacturing practices, and the integration of smart home solutions. Regulatory frameworks, particularly concerning environmental standards and consumer safety, are increasingly shaping industry practices, demanding greater accountability and sustainable sourcing. Product substitutes, such as rental services for furniture or DIY solutions, present ongoing competition, necessitating continuous value proposition refinement. End-user trends are rapidly evolving, with a growing emphasis on personalization, sustainability, and seamless online-to-offline shopping experiences. Merger and acquisition (M&A) activities, while not consistently high in deal value, indicate strategic consolidations and market expansion efforts. For instance, key M&A deals contribute to market consolidation and the integration of new technologies or product lines. The market share of top players is estimated to be around 65% of the total market value. M&A deal values are projected to reach xx Million in the forecast period.

UK Homeware Industry Industry Trends & Insights

The UK Homeware Industry is poised for significant growth, driven by a confluence of economic, technological, and societal factors. The estimated market size for the UK Homeware Industry in the base year 2025 is xx Million. The forecast period from 2025 to 2033 anticipates a Compound Annual Growth Rate (CAGR) of xx%, indicating a robust expansion trajectory. Key growth drivers include increasing disposable incomes, a growing trend towards home renovation and interior design, and the sustained demand for durable and aesthetically pleasing home furnishings and appliances. Technological disruptions are profoundly reshaping the industry. The integration of Artificial Intelligence (AI) and the Internet of Things (IoT) in home appliances is creating new product categories and enhancing user experiences, from smart kitchen gadgets to automated climate control systems. The rise of e-commerce and online distribution channels has democratized access to a wider range of products and brands, forcing traditional retailers to adapt their strategies and enhance their digital presence. Consumer preferences are shifting towards sustainable, eco-friendly products, reflecting a growing environmental consciousness. This trend is influencing material sourcing, manufacturing processes, and product lifecycle management, creating opportunities for brands that prioritize ethical production. The competitive dynamics within the industry are intensifying, with both established global giants and agile start-ups vying for market share. Key players are increasingly focusing on customer-centric approaches, offering personalized design services, and investing in supply chain optimization to meet evolving demands for convenience and speed. Market penetration for smart home devices is expected to reach xx% by 2033, significantly impacting the home appliance segment. The online distribution channel is projected to capture xx% of the total homeware market share by 2033.

Dominant Markets & Segments in UK Homeware Industry

The UK Homeware Industry exhibits distinct dominance across various segments, driven by specific consumer needs and economic conditions.

Product Segments

- Home Furniture: This segment holds a substantial market share, estimated at xx% of the total industry value. Dominance is fueled by the persistent demand for functional and decorative pieces, driven by new home purchases, renovations, and evolving lifestyle preferences. Key drivers include urbanization, the growing rental market, and the desire for flexible and multi-functional furniture. Economic policies supporting housing development and consumer confidence play a crucial role in this segment's buoyancy.

- Home Appliances: Representing approximately xx% of the market, this segment is characterized by rapid technological innovation. Dominance is maintained by the constant need for energy-efficient, smart, and user-friendly appliances that enhance convenience and sustainability. Factors such as rising energy costs, government incentives for energy-efficient models, and the integration of smart home ecosystems are key growth enablers. Leading companies like Bosch Group and Koninklijke Philips NV are instrumental in driving innovation and market penetration.

- Floor Covering Products: This segment accounts for around xx% of the market. Dominance is driven by the cyclical nature of renovations and the demand for both aesthetic appeal and durability. Victoria PLC is a significant player in this segment, with its strategic acquisitions bolstering its market position. Economic upturns and increased consumer spending on home improvements directly influence this segment's performance. Infrastructure development and the availability of diverse materials like vinyl and carpet contribute to its strength.

- Home Décor Products: With an estimated xx% market share, this segment is highly influenced by aesthetic trends and discretionary spending. Dominance is achieved through a wide variety of decorative items, from lighting to artwork and accessories. The rise of social media platforms and influencer marketing significantly impacts consumer preferences and drives demand. The accessibility of a vast range of products through online channels further strengthens this segment.

- Home Textiles: This segment, comprising bedding, towels, and soft furnishings, holds roughly xx% of the market. Dominance is achieved through the constant need for replacement and the desire for comfort and style. Trends towards natural and sustainable materials, as well as personalized textile designs, are key growth drivers. The competitive landscape includes both large retailers and niche online boutiques.

Distribution Channels

- Online Distribution Channels: This channel has emerged as a dominant force, capturing an estimated xx% of the market. Its dominance is propelled by unparalleled convenience, a wider product selection, competitive pricing, and the ability to reach a national consumer base. Way Fair UK and DFS Furniture PLC are prominent beneficiaries of this shift. The robust growth of e-commerce infrastructure and digital payment systems further cements its leading position.

- Specialty Stores: Holding approximately xx% of the market, specialty stores thrive by offering curated selections, expert advice, and a personalized shopping experience. Their dominance lies in catering to specific niche markets within homeware, such as high-end kitchenware or bespoke furniture. Companies like Kitchen Craft and Cuisinart leverage this channel for brand building and customer engagement.

- Supermarket and Hypermarkets: These channels, accounting for around xx% of the market, offer convenience and accessibility for basic homeware items. Their dominance stems from their high foot traffic and ability to bundle homeware products with other household necessities. However, their market share in specialized or high-value homeware is limited.

- Other Distribution Channels: This category, representing the remaining xx% of the market, includes direct-to-consumer (DTC) brands, independent retailers, and pop-up shops. These channels contribute to market diversity and often cater to specific consumer segments seeking unique or artisanal products.

UK Homeware Industry Product Developments

The UK Homeware Industry is witnessing a surge in product developments driven by technological advancements and evolving consumer demands. Innovations in home appliances focus on enhanced energy efficiency, AI integration for personalized user experiences, and smart connectivity, as seen with Dyson's advancements in air purification and vacuum technology. In home furniture, there's a growing emphasis on sustainable materials, modular designs for flexible living spaces, and smart furniture with integrated charging capabilities. Home textiles are seeing innovations in natural and recycled fibers, antimicrobial treatments, and advanced dyeing techniques for vibrant and long-lasting colors. Floor covering products are benefiting from advancements in durability, water resistance, and eco-friendly manufacturing processes, exemplified by Gerflor's sustainable vinyl flooring solutions. Home décor products are increasingly incorporating smart lighting, personalized 3D-printed items, and eco-conscious materials. These developments aim to provide consumers with products that are not only functional and aesthetically pleasing but also contribute to a healthier and more sustainable living environment, offering significant competitive advantages to early adopters.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the UK Homeware Industry, meticulously segmented across key product categories and distribution channels.

Product Segmentation

- Home Furniture: This segment is projected to experience steady growth, driven by evolving living spaces and consumer demand for comfort and style. Market size is estimated at xx Million, with a projected CAGR of xx% during the forecast period. Competitive dynamics are characterized by established retailers and an increasing number of online-only brands.

- Home Textiles: Valued at xx Million, this segment is expected to grow at a CAGR of xx%. Key drivers include the demand for sustainable materials and personalized design options. Competition is fierce, with both mass-market retailers and premium brands vying for consumer attention.

- Home Appliances: With a market size of xx Million and a projected CAGR of xx%, this segment is significantly influenced by technological innovation. Smart appliances and energy-efficient models are key growth catalysts. Key players are investing heavily in R&D to maintain a competitive edge.

- Floor Covering Products: This segment, estimated at xx Million, is anticipated to grow at a CAGR of xx%. Growth is linked to the renovation market and the demand for durable and aesthetically pleasing options. Victoria PLC's strategic acquisitions indicate a focus on consolidating market share.

- Home Décor Products: Valued at xx Million with a projected CAGR of xx%, this segment is driven by consumer trends and discretionary spending. Online platforms play a crucial role in accessibility and driving niche market growth.

- Other Products: This segment, encompassing a variety of homeware items not explicitly listed, is projected to be valued at xx Million, with a CAGR of xx%.

Distribution Channel Segmentation

- Supermarket and Hypermarkets: While offering convenience, this channel's growth is projected to be moderate, with a market share of xx%.

- Specialty Stores: This segment is expected to maintain a steady growth trajectory, valued at xx Million, driven by specialized offerings and expert advice.

- Online Distribution Channels: This channel is projected to dominate, with a substantial market size of xx Million and a high CAGR of xx%, driven by convenience and expanding reach.

- Other Distribution Channels: This segment is expected to see growth, contributing xx Million to the market, driven by niche players and emerging DTC models.

Key Drivers of UK Homeware Industry Growth

The UK Homeware Industry's growth is propelled by several interconnected factors. Economic recovery and increased consumer confidence translate into higher disposable incomes, directly fueling spending on home furnishings and enhancements. Technological advancements are continuously introducing innovative products, from smart home appliances to sustainable materials, enhancing functionality and appeal. The persistent trend of home renovation and interior design, amplified by a growing interest in creating comfortable and personalized living spaces, remains a significant catalyst. Furthermore, government initiatives promoting energy efficiency and sustainable building practices are driving demand for eco-friendly homeware products. The increasing prevalence of remote working has also led to a greater focus on optimizing home environments, further stimulating market growth.

Challenges in the UK Homeware Industry Sector

Despite robust growth prospects, the UK Homeware Industry faces several challenges. Regulatory hurdles, particularly concerning environmental standards and product safety, can increase compliance costs and necessitate product redesign. Supply chain disruptions, exacerbated by global events and logistical complexities, can lead to increased lead times and higher operational expenses. Intense competition, both from domestic and international players, puts pressure on pricing and profit margins. Economic volatility and fluctuating consumer spending power can impact discretionary purchases, a significant component of homeware sales. The rising cost of raw materials and manufacturing also presents a considerable challenge, potentially impacting affordability for consumers. Furthermore, the need to adapt to rapidly changing consumer preferences and technological obsolescence requires continuous investment and agile business strategies.

Emerging Opportunities in UK Homeware Industry

The UK Homeware Industry is ripe with emerging opportunities. The growing demand for sustainable and ethically sourced products presents a significant avenue for brands that prioritize eco-friendly practices and materials. The integration of smart home technology and the Internet of Things (IoT) offers substantial potential for innovation in connected appliances and intelligent living solutions. The expansion of e-commerce and direct-to-consumer (DTC) models allows businesses to reach a wider audience and build stronger customer relationships. Personalization and customization are increasingly sought after by consumers, creating opportunities for bespoke furniture and décor. Furthermore, the rising interest in small-space living and multi-functional furniture opens up niches for innovative product design. The increasing focus on well-being and creating comfortable home environments also presents opportunities for products related to comfort, relaxation, and air quality.

Leading Players in the UK Homeware Industry Market

- Inter IKEA Group

- Kitchen Craft

- Bosch Group

- Cuisinart

- Dyson

- Milliken

- Bed Bath and Beyond UK

- DFS Furniture PLC

- Koninklijke Philips NV

- Villeroy and Boch

- Victoria PLC

- Way Fair UK

- Gerflor

Key Developments in UK Homeware Industry Industry

- October 2022: Victoria PLC, the United Kingdom-based flooring designer, manufacturer, and distributor, announced the acquisition of Florida-based International Wholesale Tile LLC (IWT), significantly expanding its global reach and product portfolio in the flooring segment.

- February 2022: Victoria PLC, the international designer, manufacturer, and distributor of innovative flooring, completed the acquisition of B3 Ceramics Danismanlik (Graniser), further strengthening its position in the global flooring market through strategic consolidation and market expansion.

Strategic Outlook for UK Homeware Industry Market

The strategic outlook for the UK Homeware Industry is highly positive, driven by sustained consumer interest in home improvement and personalization. Future growth will likely be propelled by further integration of smart technologies into home appliances, increasing the appeal of connected living. The emphasis on sustainability will continue to shape product development and supply chain management, presenting opportunities for brands that align with environmental consciousness. E-commerce and omnichannel strategies will remain critical for market penetration, enabling wider reach and enhanced customer engagement. Strategic partnerships and acquisitions are expected to continue as companies seek to consolidate market share, expand product offerings, and leverage technological advancements. The industry's ability to adapt to evolving consumer preferences for convenience, customization, and ethical consumption will be paramount to its continued success and expansion in the coming years.

UK Homeware Industry Segmentation

-

1. Product

- 1.1. Home Furniture

- 1.2. Home Textiles

- 1.3. Home Appliances

- 1.4. Floor Covering Products

- 1.5. Home Décor Products

- 1.6. Other Pr

-

2. Distribution Channel

- 2.1. Supermarket and Hypermarkets

- 2.2. Specialty Stores

- 2.3. Online Distribution Channels

- 2.4. Other Distribution Channels

UK Homeware Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

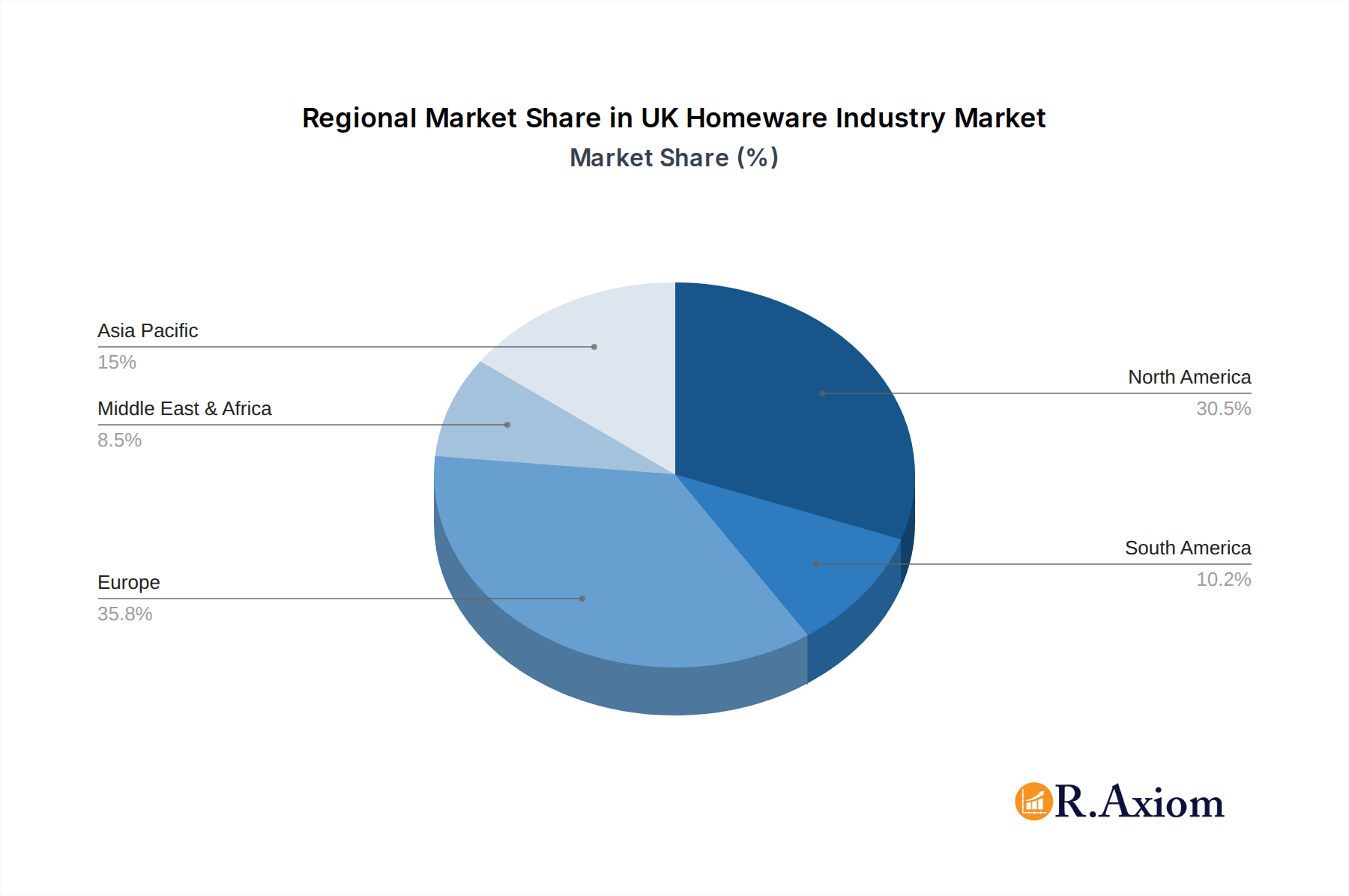

UK Homeware Industry Regional Market Share

Geographic Coverage of UK Homeware Industry

UK Homeware Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Home Furniture

- 5.1.2. Home Textiles

- 5.1.3. Home Appliances

- 5.1.4. Floor Covering Products

- 5.1.5. Home Décor Products

- 5.1.6. Other Pr

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarket and Hypermarkets

- 5.2.2. Specialty Stores

- 5.2.3. Online Distribution Channels

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global UK Homeware Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Home Furniture

- 6.1.2. Home Textiles

- 6.1.3. Home Appliances

- 6.1.4. Floor Covering Products

- 6.1.5. Home Décor Products

- 6.1.6. Other Pr

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarket and Hypermarkets

- 6.2.2. Specialty Stores

- 6.2.3. Online Distribution Channels

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America UK Homeware Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Home Furniture

- 7.1.2. Home Textiles

- 7.1.3. Home Appliances

- 7.1.4. Floor Covering Products

- 7.1.5. Home Décor Products

- 7.1.6. Other Pr

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarket and Hypermarkets

- 7.2.2. Specialty Stores

- 7.2.3. Online Distribution Channels

- 7.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. South America UK Homeware Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Home Furniture

- 8.1.2. Home Textiles

- 8.1.3. Home Appliances

- 8.1.4. Floor Covering Products

- 8.1.5. Home Décor Products

- 8.1.6. Other Pr

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarket and Hypermarkets

- 8.2.2. Specialty Stores

- 8.2.3. Online Distribution Channels

- 8.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Europe UK Homeware Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Home Furniture

- 9.1.2. Home Textiles

- 9.1.3. Home Appliances

- 9.1.4. Floor Covering Products

- 9.1.5. Home Décor Products

- 9.1.6. Other Pr

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarket and Hypermarkets

- 9.2.2. Specialty Stores

- 9.2.3. Online Distribution Channels

- 9.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East & Africa UK Homeware Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Home Furniture

- 10.1.2. Home Textiles

- 10.1.3. Home Appliances

- 10.1.4. Floor Covering Products

- 10.1.5. Home Décor Products

- 10.1.6. Other Pr

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarket and Hypermarkets

- 10.2.2. Specialty Stores

- 10.2.3. Online Distribution Channels

- 10.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Asia Pacific UK Homeware Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Home Furniture

- 11.1.2. Home Textiles

- 11.1.3. Home Appliances

- 11.1.4. Floor Covering Products

- 11.1.5. Home Décor Products

- 11.1.6. Other Pr

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarket and Hypermarkets

- 11.2.2. Specialty Stores

- 11.2.3. Online Distribution Channels

- 11.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Inter IKEA Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Kitchen Craft

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bosch Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cuisinart

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Dyson

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Milliken

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bed Bath and Beyond UK

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 DFS Furniture PLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Koninklijke Philips NV

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Villeroy and Boch

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Victoria PLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Way Fair UK

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Victoria PLC

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Gerflor

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Inter IKEA Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UK Homeware Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global UK Homeware Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America UK Homeware Industry Revenue (Million), by Product 2025 & 2033

- Figure 4: North America UK Homeware Industry Volume (K Unit), by Product 2025 & 2033

- Figure 5: North America UK Homeware Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America UK Homeware Industry Volume Share (%), by Product 2025 & 2033

- Figure 7: North America UK Homeware Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 8: North America UK Homeware Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 9: North America UK Homeware Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America UK Homeware Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America UK Homeware Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America UK Homeware Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America UK Homeware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America UK Homeware Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: South America UK Homeware Industry Revenue (Million), by Product 2025 & 2033

- Figure 16: South America UK Homeware Industry Volume (K Unit), by Product 2025 & 2033

- Figure 17: South America UK Homeware Industry Revenue Share (%), by Product 2025 & 2033

- Figure 18: South America UK Homeware Industry Volume Share (%), by Product 2025 & 2033

- Figure 19: South America UK Homeware Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 20: South America UK Homeware Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 21: South America UK Homeware Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: South America UK Homeware Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: South America UK Homeware Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: South America UK Homeware Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: South America UK Homeware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America UK Homeware Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe UK Homeware Industry Revenue (Million), by Product 2025 & 2033

- Figure 28: Europe UK Homeware Industry Volume (K Unit), by Product 2025 & 2033

- Figure 29: Europe UK Homeware Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Europe UK Homeware Industry Volume Share (%), by Product 2025 & 2033

- Figure 31: Europe UK Homeware Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 32: Europe UK Homeware Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 33: Europe UK Homeware Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Europe UK Homeware Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Europe UK Homeware Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe UK Homeware Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Europe UK Homeware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe UK Homeware Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa UK Homeware Industry Revenue (Million), by Product 2025 & 2033

- Figure 40: Middle East & Africa UK Homeware Industry Volume (K Unit), by Product 2025 & 2033

- Figure 41: Middle East & Africa UK Homeware Industry Revenue Share (%), by Product 2025 & 2033

- Figure 42: Middle East & Africa UK Homeware Industry Volume Share (%), by Product 2025 & 2033

- Figure 43: Middle East & Africa UK Homeware Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 44: Middle East & Africa UK Homeware Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 45: Middle East & Africa UK Homeware Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East & Africa UK Homeware Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Middle East & Africa UK Homeware Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East & Africa UK Homeware Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East & Africa UK Homeware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa UK Homeware Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific UK Homeware Industry Revenue (Million), by Product 2025 & 2033

- Figure 52: Asia Pacific UK Homeware Industry Volume (K Unit), by Product 2025 & 2033

- Figure 53: Asia Pacific UK Homeware Industry Revenue Share (%), by Product 2025 & 2033

- Figure 54: Asia Pacific UK Homeware Industry Volume Share (%), by Product 2025 & 2033

- Figure 55: Asia Pacific UK Homeware Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 56: Asia Pacific UK Homeware Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 57: Asia Pacific UK Homeware Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Asia Pacific UK Homeware Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: Asia Pacific UK Homeware Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Asia Pacific UK Homeware Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Asia Pacific UK Homeware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific UK Homeware Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Homeware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Global UK Homeware Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: Global UK Homeware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global UK Homeware Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global UK Homeware Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global UK Homeware Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global UK Homeware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 8: Global UK Homeware Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 9: Global UK Homeware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global UK Homeware Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global UK Homeware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global UK Homeware Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global UK Homeware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 20: Global UK Homeware Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 21: Global UK Homeware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global UK Homeware Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global UK Homeware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global UK Homeware Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Brazil UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Brazil UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Argentina UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Argentina UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Global UK Homeware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 32: Global UK Homeware Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 33: Global UK Homeware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 34: Global UK Homeware Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global UK Homeware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global UK Homeware Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: United Kingdom UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Germany UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Germany UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: France UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: France UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Italy UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Italy UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Spain UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Spain UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Russia UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Russia UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Benelux UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Benelux UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: Nordics UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Nordics UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global UK Homeware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 56: Global UK Homeware Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 57: Global UK Homeware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 58: Global UK Homeware Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 59: Global UK Homeware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global UK Homeware Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Turkey UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Turkey UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Israel UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Israel UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: GCC UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: GCC UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: North Africa UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 68: North Africa UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 69: South Africa UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: South Africa UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: Global UK Homeware Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 74: Global UK Homeware Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 75: Global UK Homeware Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 76: Global UK Homeware Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 77: Global UK Homeware Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 78: Global UK Homeware Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 79: China UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: China UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 81: India UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 82: India UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 83: Japan UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 84: Japan UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 85: South Korea UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: South Korea UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: ASEAN UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Oceania UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Oceania UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific UK Homeware Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific UK Homeware Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Homeware Industry?

The projected CAGR is approximately 4.17%.

2. Which companies are prominent players in the UK Homeware Industry?

Key companies in the market include Inter IKEA Group, Kitchen Craft, Bosch Group, Cuisinart, Dyson, Milliken, Bed Bath and Beyond UK, DFS Furniture PLC, Koninklijke Philips NV, Villeroy and Boch, Victoria PLC, Way Fair UK, Victoria PLC, Gerflor.

3. What are the main segments of the UK Homeware Industry?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.20 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Restaurants and Food Chains globally; Rise in the share of people opting for vegan and vegetarian foods.

6. What are the notable trends driving market growth?

Increased Spending on Furniture and Appliances is Driving the Market's Growth.

7. Are there any restraints impacting market growth?

Rise in price of electric appliances globally; Rising inflation decreasing the purchasing power.

8. Can you provide examples of recent developments in the market?

October 2022: Victoria PLC, the United Kingdom-based flooring designer, manufacturer, and distributor, announced the acquisition of Florida-based International Wholesale Tile LLC (IWT).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Homeware Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Homeware Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Homeware Industry?

To stay informed about further developments, trends, and reports in the UK Homeware Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence