Key Insights

The United States automotive parts die casting market is set for substantial growth, fueled by escalating demand for lightweight, high-performance vehicle components. With a projected market size of $3580.4 million in the base year 2025, and a Compound Annual Growth Rate (CAGR) of 4.7% anticipated through 2033, the sector is positioned for significant expansion. Key growth catalysts include the rising production of electric vehicles (EVs) and the widespread adoption of advanced driver-assistance systems (ADAS), both requiring sophisticated die-cast parts. Aluminum and magnesium alloys are anticipated to lead raw material adoption due to their superior strength-to-weight ratios, vital for improving fuel efficiency and EV range. Pressure die casting is expected to dominate due to its cost-effectiveness and high-volume production capabilities for complex automotive components like engine blocks, transmission housings, and structural elements.

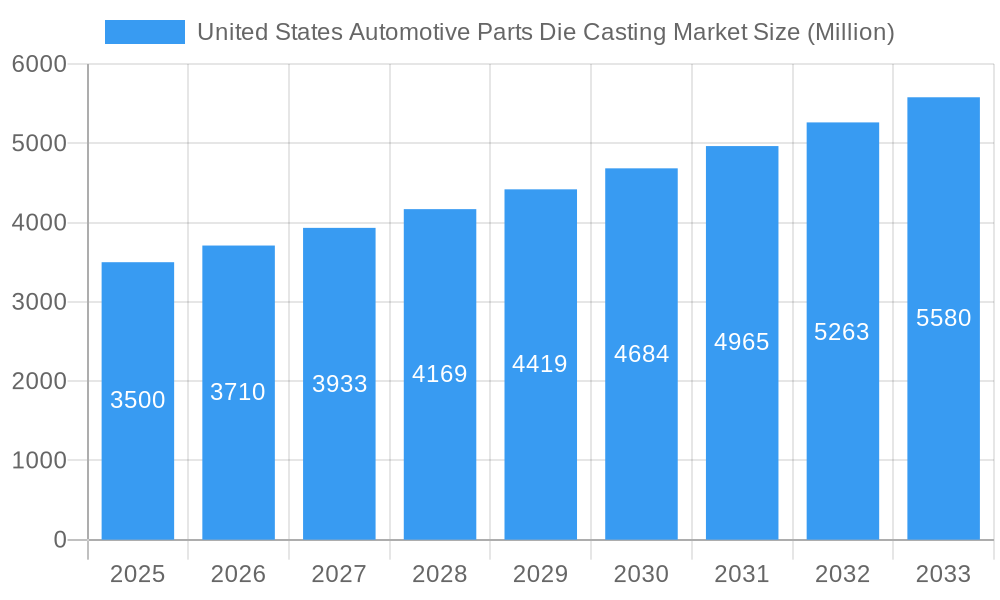

United States Automotive Parts Die Casting Market Market Size (In Billion)

Evolving trends such as increasingly intricate automotive designs and a heightened focus on sustainable manufacturing practices are shaping market dynamics. Manufacturers are prioritizing investments in advanced die casting technologies, including automation and precision tooling, to achieve stringent quality standards and minimize waste. Market restraints include raw material price volatility and the significant capital investment required for advanced die casting facilities. Nevertheless, leading companies like Georg Fischer Limited, Endurance Technologies, and Rheinmetall AG are strategically enhancing their capacities and R&D efforts to leverage opportunities within the U.S. automotive sector, particularly for critical components supporting the evolving automotive landscape.

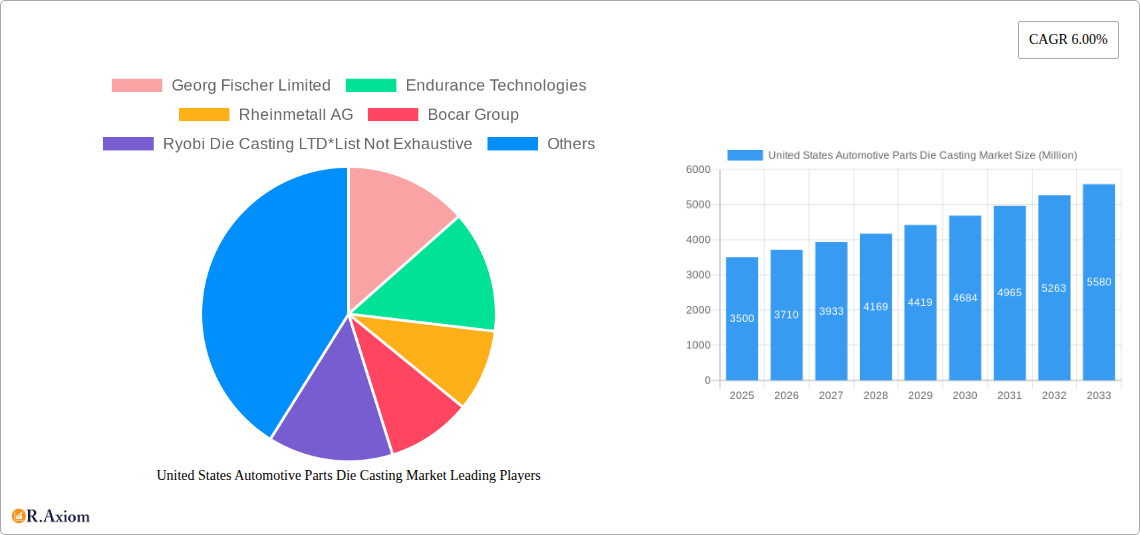

United States Automotive Parts Die Casting Market Company Market Share

Discover the comprehensive outlook for the United States Automotive Parts Die Casting Market, detailing its market size, growth trajectory, and future forecasts.

United States Automotive Parts Die Casting Market Market Concentration & Innovation

The United States automotive parts die casting market exhibits a dynamic landscape characterized by a moderate level of concentration, with several key players dominating significant portions of the market share. Innovation serves as a crucial differentiator, driven by advancements in die casting technologies, automation, and material science. The pursuit of lighter, stronger, and more fuel-efficient automotive components fuels continuous R&D. Regulatory frameworks, particularly concerning emissions standards and manufacturing safety, play a pivotal role in shaping production processes and material choices. The market is also influenced by evolving end-user trends, such as the increasing demand for electric vehicles (EVs) and advanced driver-assistance systems (ADAS), which necessitate specialized die-cast parts. Consequently, mergers and acquisitions (M&A) are active, reflecting strategic moves to expand capabilities, gain market access, and consolidate operations. For instance, recent M&A activities in the broader automotive parts sector have seen deal values in the range of tens to hundreds of millions of dollars, indicating a strong appetite for strategic consolidation. The integration of advanced manufacturing techniques like additive manufacturing alongside traditional die casting processes is a significant innovation driver. The emphasis on sustainability and circular economy principles is also prompting companies to invest in research for recycled aluminum alloys and energy-efficient die casting methods, further intensifying the competitive environment and pushing the boundaries of product development.

United States Automotive Parts Die Casting Market Industry Trends & Insights

The United States automotive parts die casting market is poised for significant growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.8% during the forecast period of 2025–2033. This expansion is underpinned by a confluence of robust industry trends and evolving market dynamics. A primary growth driver is the relentless demand for lightweight automotive components to enhance fuel efficiency and reduce emissions, aligning with stringent environmental regulations. The ongoing shift towards electric vehicles (EVs) presents a substantial opportunity, as EVs often incorporate a higher number of intricate, lightweight die-cast parts for battery housings, motor components, and structural elements. Technological disruptions, including the adoption of Industry 4.0 principles, automation, and advanced simulation software, are revolutionizing die casting processes, leading to improved precision, reduced cycle times, and enhanced quality. The integration of artificial intelligence (AI) and machine learning (ML) in process optimization and quality control is becoming increasingly prevalent, offering predictive maintenance and real-time adjustments. Consumer preferences are also shaping the market, with a growing demand for sophisticated vehicle features and enhanced performance, which directly translate into the need for complex and high-quality die-cast parts. Competitive dynamics are intense, characterized by strategic partnerships, technological collaborations, and a constant drive for cost optimization. Key players are investing heavily in expanding their production capacities and diversifying their product portfolios to cater to the evolving needs of automotive OEMs. The increasing complexity of automotive designs and the demand for integrated components are pushing the boundaries of traditional die casting, leading to innovation in tooling and casting techniques. The market penetration of advanced die casting solutions is expected to rise as manufacturers strive for greater efficiency and superior product performance, solidifying the market's upward trajectory.

Dominant Markets & Segments in United States Automotive Parts Die Casting Market

The United States automotive parts die casting market is currently dominated by the Pressure Die Casting process, which accounts for an estimated 75% of the market value. This dominance is attributed to its efficiency, cost-effectiveness, and suitability for high-volume production of complex geometries required for a wide array of automotive components. Economic policies supporting domestic manufacturing and the automotive industry's robust supply chain infrastructure in the U.S. further solidify this segment's leadership.

Raw Material analysis reveals that Aluminium is the overwhelmingly dominant material, comprising approximately 85% of the market share. Its lightweight nature, excellent strength-to-weight ratio, and recyclability make it the material of choice for meeting modern automotive demands for fuel efficiency and performance. The established infrastructure for aluminum sourcing and processing in the United States directly contributes to its widespread adoption.

Key Drivers for Pressure Die Casting Dominance:

- High production rates and efficiency.

- Cost-effectiveness for mass production.

- Ability to produce intricate shapes and thin walls.

- Versatility for a broad range of automotive components.

Key Drivers for Aluminium Dominance:

- Superior lightweight properties for fuel economy.

- Excellent corrosion resistance and durability.

- High recyclability, aligning with sustainability goals.

- Mature and accessible supply chain within the U.S.

While Aluminium reigns supreme, Magnesium is witnessing increasing adoption, particularly for components where extreme weight reduction is critical, such as steering wheel frames and seat components. Its market share, though smaller at around 10%, is projected to grow as EV adoption increases and the demand for ultra-lightweight solutions intensifies. Zinc die casting, at an estimated 5% market share, finds its niche in smaller, intricate parts like door handles and interior trim components due to its excellent fluidity and surface finish.

The dominance of these segments is further reinforced by continuous investment in advanced die casting machinery and tooling, enabling manufacturers to meet the evolving specifications of automotive OEMs. The U.S. government's focus on revitalizing domestic manufacturing and supporting the automotive sector through various incentives also plays a crucial role in sustaining the dominance of these key processes and raw materials.

United States Automotive Parts Die Casting Market Product Developments

Product development in the United States automotive parts die casting market is heavily focused on innovation in lightweighting and structural integrity. Companies are actively developing complex, integrated components that reduce part count and assembly time. Advances in die design and casting simulations are enabling the production of increasingly intricate geometries with tight tolerances, crucial for components like battery enclosures for electric vehicles, advanced engine parts, and chassis components designed for enhanced safety and performance. The competitive advantage lies in the ability to deliver high-quality, cost-effective solutions that meet the stringent demands of evolving automotive platforms, particularly in the rapidly growing EV sector.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the United States Automotive Parts Die Casting Market, encompassing detailed segmentation across key areas. The Process segmentation includes Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, and Others, each analyzed for their market share, growth trajectory, and specific applications within the automotive industry. Pressure Die Casting remains the dominant process, benefiting from its suitability for high-volume production. Vacuum Die Casting is gaining traction for its ability to produce denser, stronger castings with fewer defects.

The Raw Material segmentation focuses on Aluminium, Magnesium, and Zinc, with Aluminium holding the largest market share due to its lightweight properties. Growth projections for each material are detailed, alongside an assessment of their respective competitive dynamics and adoption trends. Aluminium die casting is projected to continue its dominance, driven by EV manufacturing. Magnesium is expected to see significant growth due to its ultra-lightweight characteristics.

Key Drivers of United States Automotive Parts Die Casting Market Growth

The growth of the United States automotive parts die casting market is primarily driven by the escalating demand for lightweight vehicle components to improve fuel efficiency and reduce emissions, directly supporting the transition towards more sustainable transportation. The burgeoning electric vehicle (EV) market is a significant catalyst, requiring specialized and complex die-cast parts for battery systems, powertrains, and lightweight chassis structures. Technological advancements in die casting, including automation, advanced simulation software, and the adoption of Industry 4.0 principles, are enhancing efficiency, quality, and cost-effectiveness. Furthermore, supportive government policies aimed at boosting domestic manufacturing and promoting automotive innovation, coupled with ongoing research and development in material science to create stronger and lighter alloys, are propelling market expansion.

Challenges in the United States Automotive Parts Die Casting Market Sector

The United States automotive parts die casting market faces several significant challenges that could temper its growth trajectory. Fluctuations in raw material prices, particularly for aluminium, can impact profitability and create cost pressures for manufacturers. Stringent environmental regulations, while driving innovation, also necessitate substantial investment in compliance and the adoption of greener manufacturing processes, which can be capital-intensive. Intense global competition from regions with lower manufacturing costs poses a continuous threat to domestic players. Supply chain disruptions, as evidenced by recent global events, can lead to production delays and increased operational costs. Moreover, the skilled labor shortage in the manufacturing sector can hinder expansion and the adoption of advanced technologies.

Emerging Opportunities in United States Automotive Parts Die Casting Market

Emerging opportunities within the United States automotive parts die casting market are largely centered around the rapid growth of the electric vehicle (EV) sector, creating demand for specialized components like battery housings, motor components, and thermal management systems. The increasing adoption of advanced driver-assistance systems (ADAS) also necessitates the production of intricate die-cast parts for sensor housings and control units. The push towards sustainable manufacturing is opening avenues for companies investing in greener die casting technologies and the use of recycled materials. Furthermore, the ongoing trend of vehicle lightweighting, driven by both fuel efficiency mandates and performance enhancements, presents continuous opportunities for innovative die-cast solutions. The potential for additive manufacturing integration with die casting processes also offers new avenues for complex part creation and customization.

Leading Players in the United States Automotive Parts Die Casting Market Market

- Georg Fischer Limited

- Endurance Technologies

- Rheinmetall AG

- Bocar Group

- Ryobi Die Casting LTD

- Nemak

- Form Technologies Inc

- Shiloh Industries

- Rockman Industries

Key Developments in United States Automotive Parts Die Casting Market Industry

- 2023: Increased investment in automation and robotics across major die casting facilities to enhance efficiency and reduce labor dependency.

- 2023: Strategic partnerships formed between die casting manufacturers and automotive OEMs to co-develop lightweight components for next-generation EV platforms.

- 2022: Adoption of advanced simulation software for die design and process optimization, leading to reduced lead times and improved casting quality.

- 2022: Focus on developing die casting solutions for complex battery enclosures and thermal management systems for electric vehicles.

- 2021: Expansion of production capacity by several key players to meet the growing demand from the North American automotive market.

- 2020: Increased emphasis on sustainability initiatives, including the utilization of recycled aluminium alloys and energy-efficient casting processes.

Strategic Outlook for United States Automotive Parts Die Casting Market Market

The strategic outlook for the United States automotive parts die casting market is highly positive, driven by the transformative shift towards electric mobility and the continuous demand for lightweight, high-performance components. Key growth catalysts include ongoing technological advancements in die casting processes, such as increased automation and the integration of AI, which promise enhanced efficiency and precision. The expansion of EV production in North America presents a significant avenue for growth, requiring specialized and complex die-cast parts. Companies that invest in R&D for advanced materials, sustainable manufacturing practices, and innovative product designs tailored for EV applications are well-positioned to capitalize on future market opportunities and maintain a competitive edge.

United States Automotive Parts Die Casting Market Segmentation

-

1. Process

- 1.1. Pressure Die Casting

- 1.2. Vacuum Die Casting

- 1.3. Squeeze Die Casting

- 1.4. Others

-

2. Raw Material

- 2.1. Aluminium

- 2.2. Magnesium

- 2.3. Zinc

United States Automotive Parts Die Casting Market Segmentation By Geography

- 1. United States

United States Automotive Parts Die Casting Market Regional Market Share

Geographic Coverage of United States Automotive Parts Die Casting Market

United States Automotive Parts Die Casting Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Process

- 5.1.1. Pressure Die Casting

- 5.1.2. Vacuum Die Casting

- 5.1.3. Squeeze Die Casting

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Raw Material

- 5.2.1. Aluminium

- 5.2.2. Magnesium

- 5.2.3. Zinc

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Process

- 6. United States Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Process

- 6.1.1. Pressure Die Casting

- 6.1.2. Vacuum Die Casting

- 6.1.3. Squeeze Die Casting

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Raw Material

- 6.2.1. Aluminium

- 6.2.2. Magnesium

- 6.2.3. Zinc

- 6.1. Market Analysis, Insights and Forecast - by Process

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Georg Fischer Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Endurance Technologies

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Rheinmetall AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bocar Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ryobi Die Casting LTD*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nemak

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Form Technologies In

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shiloh Industries

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rockman Industries

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Georg Fischer Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Automotive Parts Die Casting Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: United States Automotive Parts Die Casting Market Share (%) by Company 2025

List of Tables

- Table 1: United States Automotive Parts Die Casting Market Revenue million Forecast, by Process 2020 & 2033

- Table 2: United States Automotive Parts Die Casting Market Revenue million Forecast, by Raw Material 2020 & 2033

- Table 3: United States Automotive Parts Die Casting Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: United States Automotive Parts Die Casting Market Revenue million Forecast, by Process 2020 & 2033

- Table 5: United States Automotive Parts Die Casting Market Revenue million Forecast, by Raw Material 2020 & 2033

- Table 6: United States Automotive Parts Die Casting Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Automotive Parts Die Casting Market?

The projected CAGR is approximately 4.7%.

2. Which companies are prominent players in the United States Automotive Parts Die Casting Market?

Key companies in the market include Georg Fischer Limited, Endurance Technologies, Rheinmetall AG, Bocar Group, Ryobi Die Casting LTD*List Not Exhaustive, Nemak, Form Technologies In, Shiloh Industries, Rockman Industries.

3. What are the main segments of the United States Automotive Parts Die Casting Market?

The market segments include Process, Raw Material.

4. Can you provide details about the market size?

The market size is estimated to be USD 3580.4 million as of 2022.

5. What are some drivers contributing to market growth?

Surge in Trend of Yacht Tourism.

6. What are the notable trends driving market growth?

Cost Issues and Resource Inefficiencies.

7. Are there any restraints impacting market growth?

Higher Rentals During Peak Season.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Automotive Parts Die Casting Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Automotive Parts Die Casting Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Automotive Parts Die Casting Market?

To stay informed about further developments, trends, and reports in the United States Automotive Parts Die Casting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence